Diesel Generator Demand, 7 GW Capacity Gap, 104-Week Lead Times, and PJM Interconnection Delays (2021 to 2026)

Data Center Power Constraints, 190 GW Hyperscale Pipeline Meets Grid Delays

The explosive growth in AI-driven data center construction is colliding with an aging and inadequate global power grid, forcing developers to procure on-site generators not just for backup but as a primary solution to bridge multi-year interconnection delays. This marks a fundamental shift from the 2021 to 2024 period, when generators were primarily an insurance policy for rare emergencies. The market is now defined by physical constraints, where the demand for reliable power has completely outstripped the grid’s ability to supply it.

- In the period from January 1, 2025, to today, the role of backup generators has transformed from an emergency fail-safe to a mission-critical bridging solution. Grid interconnection queues in key markets like the PJM territory now extend five years or more, making on-site generation the only viable path to bring new data center capacity online within a reasonable timeframe.

- The scale of the impending demand is massive, with an announced 190 GW of new hyperscale capacity in the development pipeline as of early 2026. This construction boom is running directly into power and equipment shortages, which have already caused the cancellation or delay of projects representing a 7 GW capacity gap in the U.S. for 2026.

- The strategic implication is that the data center generator market is no longer a niche for emergency preparedness but a core enabler of the digital economy. The market’s growth is now a direct function of grid inadequacy; as long as the grid lags, the generator market will thrive.

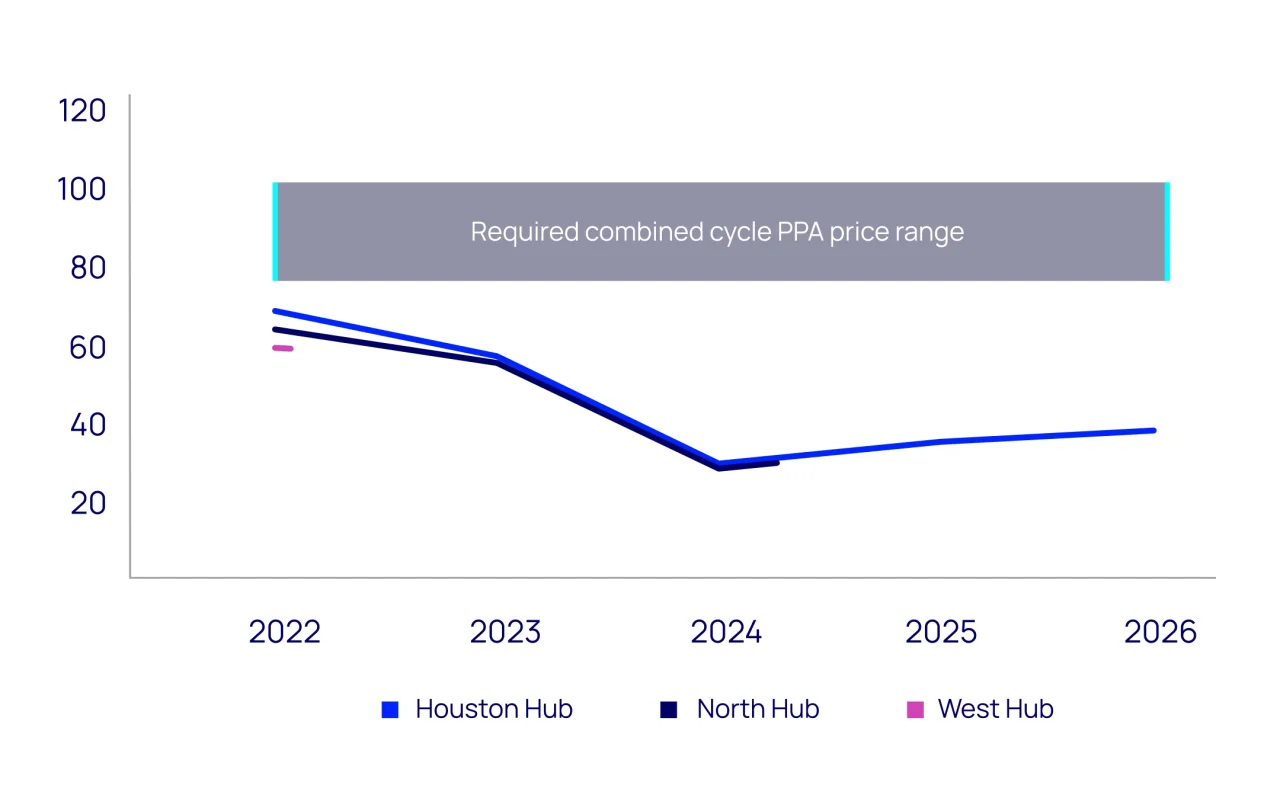

Power Prices Insufficient for New Plant Construction

The section discusses data center power constraints and grid delays. The chart explains a fundamental cause of these grid issues: power prices are not high enough to incentivize the construction of new power plants, which creates the bottleneck the section describes.

(Source: Wood Mackenzie)

$11.3 M per MW Cost, Data Center Project Delays from Power Shortages

Supply chain bottlenecks and power unavailability are now the primary sources of financial risk and project cancellations in the data center sector, directly impacting timelines and capital expenditure. While demand is at an all-time high, the physical inability to procure and commission power equipment has become the main limiting factor for growth. This is a significant change from the 2021-2023 period, where financing and land acquisition were the top concerns.

- Nearly half of U.S. AI data centers planned for 2026 have been canceled or delayed, primarily due to power shortages and equipment backlogs. This creates a vicious cycle where developers order equipment even earlier to de-risk projects, further extending lead times for the entire industry.

- Procurement lead times for essential hardware have reached critical levels. Diesel generators now require 72 to 104 weeks for delivery, while lead times for critical grid hardware like high-voltage transformers exceed two years, severely hampering project schedules.

- These delays have a direct financial impact, as power infrastructure accounts for 30-40% of a data center’s total capital expenditure, which averages $11.3 million per MW. Any delay in commissioning power systems holds up the entire multi-million dollar investment.

Table: Data Center Buildout Cost & Supply Chain Delays

| Metric | Value | Strategic Implication | Source |

|---|---|---|---|

| Generator Lead Time | 72–104 weeks | Projects must be planned 2-3 years in advance to secure power equipment, making generators a critical path item. | Second Watt |

| Transformer Lead Time | >2 years | Grid connection and on-site power distribution are severely constrained, forcing reliance on existing or temporary power solutions. | Enverus |

| Average Cost per MW | $11.3 million | The high capital cost makes any project delay extremely expensive, prioritizing speed-to-market and de-risking power delivery. | Aptly Technology |

| Power Infrastructure % of CAPEX | 30% – 40% | Power systems represent the single largest capital outlay after servers, making power strategy central to financial planning. | Aptly Technology |

| AI Data Center Cancellations (US) | 7 GW in 2026 | The market is physically constrained by power and equipment availability, not by a lack of demand or investment capital. | Tech Insider |

US vs. Global, Data Center Power Demand Surges Amid Regional Constraints

While data center construction is a global phenomenon, North America, particularly the United States, faces the most acute power shortages, with demand in key regions far exceeding available grid capacity. This geographic concentration of both demand and constraints defines the current market. Before 2024, development was more distributed, but the AI boom has focused immense pressure on a few power-rich, fiber-connected regions, which are now becoming power-constrained.

- The United States is the epicenter of this trend, with installed diesel generator capacity at data centers surging to 55 GW. This capacity, intended for backup, now nearly matches the entire estimated power usage of the global data center market in early 2025, highlighting the scale of on-site power deployment.

- Specific regions are becoming regulatory hotspots. In Virginia, a major data center hub, growing scrutiny over diesel emissions from backup generators presents a significant long-term risk and a model for potential regulations in other burgeoning data center markets.

- Although the U.S. is the current hotspot, the global pipeline of 190 GW of hyperscale capacity indicates that similar power challenges are emerging in Europe and Southeast Asia. Europe’s data center market alone is projected to require over 5, 700 MW of new backup power by 2029.

US States Deploy On-Site Data Center Power

The section focuses on regional power constraints, particularly in the US. The chart directly illustrates a US-specific, regional solution to these constraints by showing how states are using on-site power generation to overcome grid limitations.

(Source: Wood Mackenzie)

Technology Maturity, TRL 9 Diesel Generators vs. Emerging Fuel Cell Alternatives

Diesel and natural gas generators remain the only TRL 9 technologies capable of providing immediate, large-scale, and long-duration backup power, making them the default choice for mission-critical facilities. The period between 2021 and 2024 saw significant hype around emerging alternatives. However, the post-2025 reality is that these alternatives, while promising, have not yet achieved the scale, cost-effectiveness, or supply chain maturity to displace incumbents for bulk power needs.

- Proven reliability and fast-start capability ensure that TRL 9 diesel generators remain the bedrock of data center resilience. Their ability to handle large electrical loads and store fuel for 24-48 hours of operation is a capability that no other technology can currently match at scale.

- Emerging alternatives are finding niche roles. Fuel cells from providers like Bloom Energy have been deployed at over 400 MW of data centers, proving their viability for cleaner on-site power, particularly in regions with strict air quality rules. However, this is a fraction of the tens of gigawatts provided by diesel.

- Battery storage, with costs between $250 and $580 per k Wh, is becoming cost-effective for short-duration power conditioning and bridging the gap until generators start. Yet, it is not a viable replacement for the long-duration backup that diesel generators provide during extended outages.

Global Nuclear Reactor Construction Sees Modest Rebound

The section contrasts mature power technologies (diesel) with emerging alternatives. The chart, showing a rebound in nuclear construction, highlights a key emerging alternative for providing the large-scale, stable power data centers require, fitting the section’s theme.

(Source: World Nuclear Industry Status Report)

SWOT Analysis, Data Center Generator Market Strengths and Regulatory Threats

The data center generator market’s primary strength is its indispensable role in ensuring digital infrastructure uptime, a need amplified by grid instability and the non-negotiable reliability requirements of AI. This strength, however, is counterbalanced by significant long-term threats from environmental regulations and the maturation of cleaner, alternative technologies. The analysis reveals a market that is booming due to external failures (the grid) but is also vulnerable to long-term systemic shifts in policy and technology.

APAC Data Center Power Market to Near $15B

The section is a SWOT analysis of the data center generator market. This chart, by sizing the APAC power market, provides crucial data for the ‘Opportunities’ component of the SWOT, identifying a massive and growing market for generator suppliers.

(Source: Market Data Forecast)

Table: SWOT Analysis for Data Center Backup Generators

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Provided emergency backup for “five nines” uptime; mature TRL 9 technology. | Mission-critical enabler for the AI boom; used as bridge power during multi-year grid delays. | The market driver shifted from hypothetical risk (outages) to a constant, predictable constraint (grid connection delays). |

| Weaknesses | Considered a sunk cost; ESG concerns over diesel emissions were a growing topic of discussion. | Extreme lead times (72-104 weeks) and supply chain bottlenecks for the entire power ecosystem are delaying projects. | The supply chain, not manufacturing capacity, was validated as the primary weakness and constraint on market growth. |

| Opportunities | Growth tied to general data center construction; adoption in edge computing. | “Bridge power” is now a primary use case; data centers are exploring microgrids and selling ancillary services back to the grid. | The generator’s role evolved from a passive asset to an active operational component, opening new revenue models. |

| Threats | Competition from improving battery technology; early pilots of hydrogen fuel cells. | Intensified regulatory scrutiny on emissions (e.g., Virginia); significant ESG pressure from investors and customers. | The threat shifted from a distant technological challenge to an immediate regulatory and financial risk for new diesel-heavy projects. |

Scenario Outlook, Monitoring Grid Queues and Hyperscaler Capex for Market Signals

The trajectory of the data center generator market in the next 12-24 months will be determined by the interplay between grid interconnection queue times and the capital expenditure guidance from major hyperscalers. These two factors are the most reliable lead indicators for future demand and market dynamics.

- If this happens: Grid interconnection queues, particularly in markets served by operators like PJM, continue to lengthen beyond the current five-year average. Watch this: Quarterly interconnection queue reports from ISOs/RTOs and utility filings. This could be happening: The market for “bridge power” using natural gas and diesel generators will accelerate, and equipment lead times will extend further, solidifying the market for incumbents.

- If this happens: Hyperscalers such as Amazon (AWS), Microsoft (Azure), and Google (GCP) increase their 2026-2027 capital expenditure guidance for infrastructure. Watch this: Quarterly earnings calls and investor day presentations from these companies. This could be happening: Orders for entire power islands (generators, switchgear) will be placed years in advance, providing a clear demand signal and further solidifying the backlog for manufacturers like Caterpillar and Cummins.

- If this happens: The U.S. Environmental Protection Agency (EPA) or influential state regulators (e.g., California, Virginia) enact stricter emissions standards for stationary diesel engines. Watch this: Regulatory dockets and public announcements from the EPA and state air quality boards. This could be happening: The total cost of ownership for diesel will rise, accelerating the adoption of natural gas, HVO, and hydrogen fuel cells for new builds, even if they carry a higher upfront capital cost.

US Power Grids See Billions in Investment

The section is about monitoring market signals, including grid activity, to find future trends. The chart, which shows billions being invested in US power grids, is a perfect example of the kind of market signal this section would analyze to understand future power capacity.

(Source: Wood Mackenzie)

The questions your competitors are already asking

This report covers one angle of the data center generator market, now driven by grid-scale constraints. The questions that matter most depend on your work.

- Which diesel generator manufacturers are gaining or losing ground in the data center market?

- What is the outlook for on-site generator deployment in AI data centers by 2026?

- Which hyperscale operators are adopting on-site generation to bridge PJM interconnection delays?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.