DAC Energy Supply, EDF’s 500 k Tonne Return Carbon Deal and 23 GW Renewable Power Portfolio (2021-2025)

500, 000 Tonne Project, EDF’s DAC Enablement Strategy Defines Commercial Scale

Large-scale renewable energy supply has become the primary bottleneck and key enabler for commercializing Direct Air Capture (DAC), shifting the strategic focus from pure technology development to energy infrastructure partnerships. This pivot redefines industry adoption, positioning energy providers as central players in the carbon removal market.

- Prior to 2025, DAC adoption was characterized by smaller-scale pilots focused on proving the viability of capture technology in isolation.

- In 2025, the market shifted towards utility-scale projects, exemplified by the March agreement for EDF Renewables North America to power a 500, 000 tonnes/year DAC park in Texas developed by Return Carbon and using Skytree technology.

- This move illustrates a new adoption model where energy majors like EDF leverage existing assets, such as their 23 GW North American renewables portfolio, to de-risk capital-intensive DAC projects rather than developing proprietary capture systems.

- This enabler strategy contrasts with vertically integrated competitors like Occidental, whose 1 million ton/year STRATOS plant, also expected to start operations in 2025, represents a technology-ownership model.

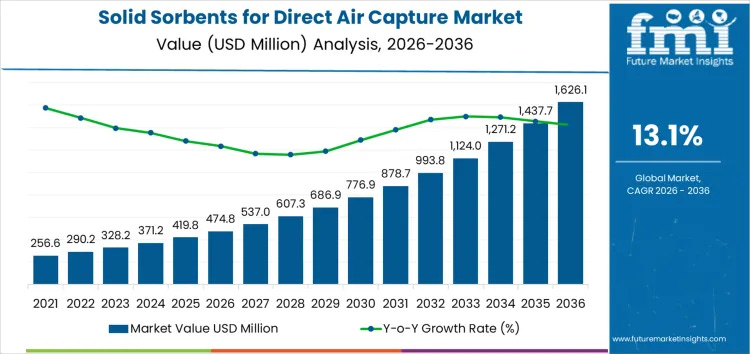

DAC Sorbent Market to Exceed $1.6B by 2036

A commercial-scale DAC project of 500,000 tonnes requires a mature and scalable supply chain for its core components. This chart, showing significant projected growth in the DAC sorbent market, demonstrates the industrial readiness and economic viability of the supply chain needed to support such a large-scale project.

(Source: Carbon Removal Updates – Substack)

EDF Investment Strategy, De-Risking DAC with Power Purchase Agreements

Instead of direct capital expenditure into high-risk DAC technology, leading energy firms are using Power Purchase Agreements (PPAs) as a form of strategic investment to catalyze the carbon removal market. This approach minimizes direct financial exposure to nascent technology while capturing value from the growing demand for clean energy.

- The high cost of DAC, with estimates ranging from $600 to $1, 000 per ton of captured CO₂, presents a significant investment hurdle that discourages direct technology ownership for many utilities.

- EDF‘s March 2025 Term Sheet to supply renewable power to the Texas DAC park is a capital-light investment strategy, creating a guaranteed revenue stream for its energy assets while enabling a partner’s project.

- This model is heavily reliant on policy incentives like the U.S. 45 Q tax credit, which provides $85 per metric ton for stored CO₂, making large-scale projects financially viable for developers who can secure a reliable source of clean power.

- While overall investment in carbon projects declined from a 2021 peak, announced capital for 2025 is projected at $2.0 billion, indicating a sustained, albeit fluctuating, pipeline for which energy supply is critical.

Utility-Scale Solar Installations Surge Dramatically

This section discusses de-risking DAC investments with Power Purchase Agreements (PPAs). DAC is highly energy-intensive, and the viability of PPAs depends on the availability of low-cost, reliable electricity. The surge in utility-scale solar provides a growing source of cheap renewable energy that can be secured via PPAs, making the entire strategy feasible.

(Source: EDF Innovation Lab)

Table: Announced Capital for Carbon Projects by Type (2021-2025)

| Project Type / Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Nature Restoration | 2021-2025 | Represents the largest segment of funding, attracting 46% of total capital. This indicates strong investor preference for nature-based solutions with perceived lower costs and ecological co-benefits. | Carbon Credits |

| REDD+ (Reducing Emissions from Deforestation) | 2021-2025 | Secured 25% of announced capital, further highlighting the market’s focus on forest-related carbon projects over engineered solutions in the near term. | Carbon Credits |

| Carbon Engineering (DAC) | 2021-2025 | As a proxy for technology-heavy projects, this segment captured 12% of capital. This smaller share reflects the higher capital intensity and perceived technology risk compared to nature-based alternatives. | Carbon Credits |

DOE Budgets $910M for Carbon Management

The section heading refers to a table of ‘Announced Capital for Carbon Projects’. This chart provides a major, specific data point for such a table: a $910M budget from the U.S. Department of Energy. This government funding represents a significant source of the capital being deployed in the sector.

(Source: EDF Innovation Lab)

Partnership Models, EDF’s 50/50 Shell JV Signals Broader Energy Collaboration

Strategic partnerships in 2025 have evolved from single-project agreements to broader alliances, indicating a move towards building integrated clean energy ecosystems where carbon removal is one of several interconnected components. These collaborations pool specialized expertise to manage the complexity of large-scale decarbonization projects.

- The dominant partnership model for DAC now involves a triad: a technology provider (Skytree), a project developer (Return Carbon), and a renewable energy supplier (EDF Renewables), allowing each to focus on its core competency.

- This specialized model accelerates deployment and mitigates risk by distributing financial and execution burdens across the value chain, making ambitious projects more feasible.

- Beyond DAC, EDF Renewables’ 50/50 joint venture with Shell New Energies, established in August 2025, points to higher-level strategic alignment on new energy initiatives, creating a platform for future integrated carbon management collaborations.

Flowchart Outlines Voluntary Carbon Market Structure

A partnership between major energy players like EDF and Shell to develop carbon capture would need to monetize the results. This flowchart illustrates the structure of the voluntary carbon market, the primary ecosystem where credits from such a project would be sold, providing essential context for the partnership’s business model.

(Source: Springer Nature)

Table: EDF Carbon Capture and Competitor Partnerships (2025)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| EDF Renewables & Shell New Energies | Aug 2025 | Formation of a 50/50 joint venture for clean energy initiatives. This high-level collaboration establishes a framework for potential future co-investment in carbon management and other decarbonization technologies. | Holland & Knight |

| EDF Renewables, Return Carbon, & Skytree | Mar 2025 | Execution of a Term Sheet for EDF to supply renewable power to a 500, 000 tonnes/year DAC park in Texas. This establishes the enabler model for EDF in the carbon removal market. | Carbon Capture Magazine |

| Occidental (Competitor) | 2025 | The STRATOS DAC plant, with a capacity of up to 1 million tons/year, is expected to begin operations. This project represents a competitive, vertically integrated approach to DAC development. | Oxy |

Electricity and Heat Dominate European Energy Demand

This section discusses EDF’s partnerships and competitors. This chart shows the massive scale of the European energy market that needs to be decarbonized. This context explains the ‘why’ behind the partnerships: the challenge is so large that it necessitates collaboration among major players to address this dominant energy demand.

(Source: Nature)

US vs. Europe, EDF’s Texas Focus Highlights Policy-Driven Geography

North America, particularly the United States, has solidified its position as the epicenter for large-scale DAC development due to superior and more direct financial incentives, causing capital and projects to concentrate there while European activity remains comparatively limited.

- EDF‘s decision to enable a major DAC project in Texas is a direct response to the U.S. policy environment, where the 45 Q tax credit provides a clear, bankable subsidy for carbon removal and storage.

- This contrasts sharply with the European market, where total CCS capture capacity was only around 4 million tons per year in 2025, indicating a slower and more complex development pathway.

- The U.S. is projected to host 8.71 million tonnes of DAC capacity in planning or construction, vastly outpacing Europe, where France and the UK have 0.20 and 0.05 million tonnes planned, respectively.

- This geographic divergence demonstrates that near-term DAC deployment is currently dictated less by geological suitability and more by the strength and certainty of regional government subsidies.

Inflation Reduction Act Drives Deeper Emission Cuts

The section heading explicitly points to ‘policy-driven geography’ and EDF’s ‘Texas Focus’. The U.S. Inflation Reduction Act (IRA) is the single most important policy creating financial incentives for carbon capture in the US. This chart directly visualizes the impact of the policy that is driving investment to locations like Texas.

From Pilot to Utility-Scale, DAC Maturity Hinges on Energy Integration

In 2025, Direct Air Capture technology crossed a critical maturity threshold from isolated pilots to integrated, utility-scale projects, with its commercial viability now intrinsically linked to the availability of low-cost, large-volume renewable power. The technology’s path to widespread deployment is now a systems integration challenge, not just a chemical one.

- Between 2021 and 2024, DAC projects primarily focused on demonstrating the chemical and mechanical viability of CO₂ capture at a small scale, often with capacities of a few thousand tons per year.

- The year 2025 marks the beginning of commercial-scale operations, with projects like Occidental‘s 1 million ton/year plant and the EDF-enabled 500, 000 ton/year park proving the technology can be planned at an industrially relevant capacity.

- The primary challenge to maturity has shifted from the capture mechanism itself to its massive energy consumption. This elevates the role of energy suppliers like EDF from peripheral vendors to critical-path partners for any large-scale deployment.

Renewables Grew 56%, Yet Fossil Fuels Dominate

The section discusses scaling DAC to ‘utility-scale’ and the critical role of ‘energy integration’. This chart perfectly illustrates the core challenge of that integration. While renewables are growing, the energy system is still dominated by fossil fuels, highlighting the complex reality that large-scale DAC must navigate as a major new energy consumer.

(Source: REN21)

SWOT Analysis of DAC Enablement Strategy for EDF in 2025

EDF‘s capital-light, energy-provider strategy for DAC leverages its core strengths and aligns with external opportunities in the U.S. market, but it also creates dependencies on nascent technology partners and shifting policy landscapes. This positions the company to benefit from the growth of carbon removal without bearing the full risk of technology development.

Survey Shows Strong Public Support for Carbon Removal

A SWOT analysis evaluates external opportunities and threats. Strong public support for carbon removal, as shown in this survey, is a key ‘Opportunity’. It indicates a favorable social license to operate and political tailwinds that strengthen the business case for EDF’s DAC strategy.

(Source: Carbon Removal Updates – Substack)

Table: SWOT Analysis for EDF’s DAC Enablement Strategy

| SWOT Category | 2021 – 2024 | 2025 and Forward | What Changed / Validated |

|---|---|---|---|

| Strengths | Established portfolio of renewable energy assets and project development expertise in North America. | Leverages its 23 GW renewables portfolio as a key enabler for energy-intensive DAC projects, creating a new demand stream for existing assets. | The 2025 Texas DAC deal validates a business model where renewable power is the core offering, not a secondary element. |

| Weaknesses | Limited direct experience and no proprietary technology in the carbon capture sector. | Dependence on the technological and execution success of partners like Skytree and Return Carbon; lack of control over the core capture technology. | The partnership model adopted in 2025 formalizes this weakness as a strategic choice, mitigating it by avoiding direct R&D investment. |

| Opportunities | Emerging corporate net-zero targets and early-stage U.S. policy support for carbon removal. | Strong financial incentives from the U.S. 45 Q tax credit ($85/ton) make large-scale DAC projects bankable. The 50/50 JV with Shell opens avenues for broader energy collaborations. | The 2025 policy environment in the U.S. became a primary driver, turning a theoretical opportunity into a concrete, project-based one. |

| Threats | High cost and unproven scalability of DAC technology posed a significant risk to direct investment. | Competition from vertically integrated players like Occidental who own the full technology stack. The high cost ($600-$1, 000/ton) could limit the market size if it does not decrease. | EDF‘s 2025 strategy mitigates the direct technology risk but increases exposure to competitive and market-pricing threats in the broader carbon removal sector. |

Scenario for EDF: From PPA Enabler to Infrastructure Owner

The most critical strategic development for EDF in the next 12-18 months will be converting its Texas DAC park Term Sheet into a binding PPA, a move that would serve as a blueprint for a scalable new business model as a premier energy provider to the carbon removal industry.

- If the Texas DAC park successfully moves to a final investment decision, watch for EDF Renewables to announce similar PPA-based enablement deals for other DAC or CCS projects across North America.

- This could be happening as a way for EDF to build a defensible market position, creating a portfolio of long-term contracts that supply its renewable energy to a new, high-growth industrial sector.

- Another signal to monitor is the activity within the EDF–Shell JV; any joint investment in CO₂ transport or storage infrastructure would indicate a strategic evolution from being a power supplier to a more integrated carbon management player.

EDF Models Future CO₂ Emissions Caps

This section outlines a future ‘Scenario for EDF’. A strategic shift to becoming an ‘Infrastructure Owner’ would be based on long-term projections. This chart, showing EDF’s own modeling of future CO₂ caps, is a direct example of the forward-looking analysis required to justify such a strategic evolution.

The questions your competitors are already asking

This report covers one angle of EDF’s strategy for enabling utility-scale Direct Air Capture. The questions that matter most depend on your work.

- Which companies are gaining ground in the DAC market: energy enablers like EDF or vertically integrated owner-operators like Occidental?

- EDF and Return Carbon’s activities in Texas. Is the 500,000 tonne DAC park progressing toward its 2025 deployment?

- What are the opportunities for energy companies to leverage their renewable power portfolios in the carbon removal market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.