Eni BESS Manufacturing Pivot, >8 GWh FIB Partnership, €3 Billion Divestment, and 5.5 GW Target (2021 to 2025)

Industry Adoption Risks: Eni’s Strategic Pivot to Battery Manufacturing

In 2025, Eni executed a strategic pivot from a traditional energy producer to a vertically integrated manufacturer in the energy storage supply chain, a fundamental shift from its pre-2025 position as primarily a deployer and operator of energy assets. This move is designed to capture value further upstream and secure control over a critical component for its renewable energy expansion, directly challenging the market structure dominated by established Asian producers.

- Prior to 2025, major energy companies, including Eni, focused their storage strategy on deploying third-party battery systems to support their renewable projects and participate in grid services.

- The launch of Eni Storage Systems on September 24, 2025, marked a decisive change. This joint venture with battery specialist FIB aims to build a domestic Italian manufacturing hub, moving Eni from a technology consumer to a technology producer.

- This vertical integration strategy aims to mitigate supply chain risks and cost volatility associated with relying on external suppliers, particularly from China, which controls nearly 85% of global battery cell production capacity.

- The initiative directly supports the rapid growth of Eni’s renewable arm, Plenitude, by creating a captive offtake market for its manufactured batteries, ensuring a baseload demand for the new factory and de-risking the substantial capital investment. This contrasts with its other transition strategies, like its Pengerang Biorefinery project for Sustainable Aviation Fuel.

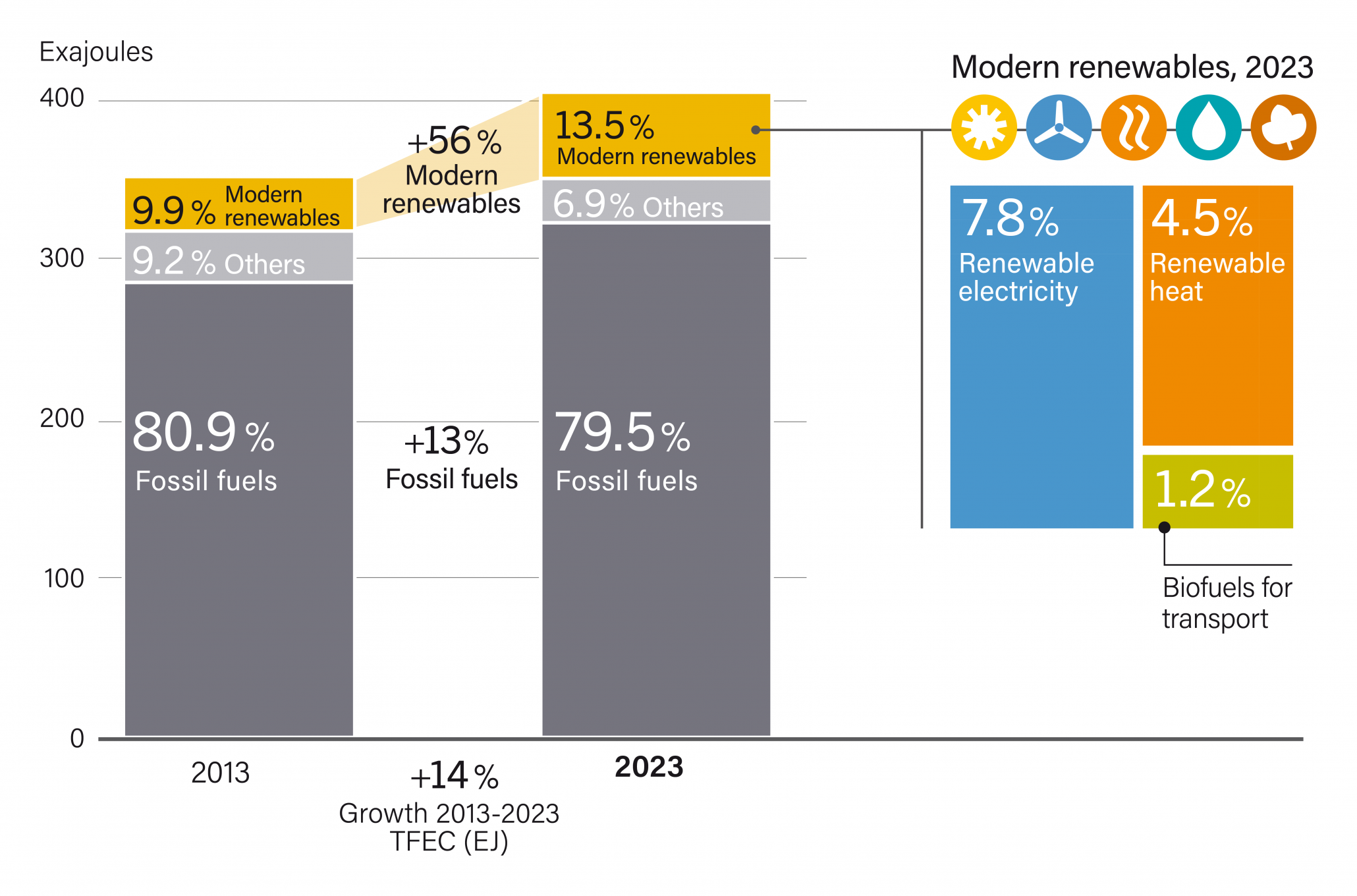

Renewable Energy Share Grows, Fossil Fuels Still Dominate

This chart directly visualizes the core challenge and ‘Adoption Risk’ for Eni. It shows the opportunity (growing renewables) but also the risk posed by the incumbency of fossil fuels, which is the market Eni is pivoting away from.

(Source: REN21)

Investment: €3 B Asset Sale Funds Eni’s 8 GWh Manufacturing Ambitions

Eni is financing its entry into battery manufacturing through a disciplined capital recycling strategy, divesting legacy assets to fund investments in high-growth energy transition sectors. This financial maneuver allows the company to undertake significant new capital projects, such as the Brindisi gigafactory, without compromising its overall financial stability, demonstrating a clear reallocation of capital from traditional to new energy business lines.

- The centerpiece of Eni’s 2025 investment is the development of the Brindisi battery gigafactory, planned to have a production capacity exceeding 8 GWh per year of Lithium Iron Phosphate (LFP) batteries.

- To fuel this transition, Eni accelerated its asset divestment program, with analysts in January 2025 projecting the company would generate an additional €3 billion in sales by the end of the year to fund strategic priorities.

- These investments are symbiotic with the continued capital expenditure into Plenitude, which reached 4.8 GW of installed renewable capacity by Q 3 2025 and is on track for its 5.5 GW year-end target, creating the pull-through demand for the new battery output.

- This contrasts with the investment model of competitors, like the $135 million financing secured by SMT Energy in March 2025 for a 160 MW BESS project in Texas, which focuses on asset deployment rather than manufacturing.

Eni Outlines Capex and Cashflow Strategy

The section discusses the funding of Eni’s manufacturing ambitions. A chart detailing the company’s Capex (Capital Expenditure) and cash flow strategy provides a direct look into the financial mechanisms enabling this large-scale investment.

(Source: Investing.com)

Table: Eni Strategic Investments and Funding (2025)

| Project / Initiative | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| LFP Battery Gigafactory | Sep 2025 | Development of a battery manufacturing plant in Brindisi, Italy, with over 8 GWh/year capacity to secure a domestic supply chain for stationary storage systems. | Eni |

| Plenitude Renewables Expansion | Q 3 2025 | Reached 4.8 GW of installed renewable capacity, progressing toward the 5.5 GW year-end target. This expansion creates the internal, captive market for the gigafactory’s output. | Eni |

| Asset Divestment Program | Jan 2025 | An accelerated program targeting an additional €3 billion in asset sales by year-end 2025 to generate capital for reinvestment into energy transition projects like battery manufacturing. | Yahoo Finance |

Eni Financial Forecast for 2025 Strategic Pivot

This section heading describes a table of financial data. A chart forecasting Eni’s finances for its 2025 pivot contains precisely the data that would populate such a table, making it a perfect match.

(Source: Yahoo Finance)

Partnership Data: Eni and FIB Launch Eni Storage Systems JV

Eni’s entry into battery manufacturing was enabled by a critical joint venture with FIB, a subsidiary of the Italian industrial group Seri, which possesses the specialized technical expertise in battery production that Eni lacks. This partnership structure allows Eni to de-risk its entry into a new industrial sector by leveraging an experienced partner while providing the industrial scale, market access, and financial backing required for a gigafactory project.

- The joint venture, named Eni Storage Systems, was formally launched on September 24, 2025, with the stated objective of developing and producing stationary lithium-ion battery systems in Italy.

- FIB brings its technological know-how in battery cell and system manufacturing, providing the core competency for the project’s success.

- Eni contributes its project management experience on large industrial sites, financial strength, and a guaranteed internal market through its renewables subsidiary, Plenitude.

- This strategic alliance is designed to create a significant European player in the battery sector, directly aligning with the EU’s policy goals of re-shoring critical clean energy supply chains.

Table: Eni Key Strategic Partnership (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| FIB (Seri Industrial) / Eni Storage Systems JV | Sep 2025 | Formation of a joint venture to establish a battery manufacturing hub in Brindisi, Italy. The goal is to produce over 8 GWh/year of LFP batteries, combining FIB’s technical expertise with Eni’s scale and market access. | Energy Storage News |

Geography: Italy as the Hub for Eni’s European Battery Ambitions

Eni’s decision to center its manufacturing ambitions in Italy is a strategic choice driven by strong domestic market signals and supportive national and continental policy. The favorable environment in its home market provides a stable foundation and a clear path to commercialization for the Brindisi factory’s output, reducing the risks associated with a new large-scale industrial venture.

- Italy has emerged as one of Europe’s most attractive markets for battery energy storage, supported by a national target of 50 GWh of battery capacity by 2030. This creates a substantial and predictable domestic demand pipeline.

- The Italian government and grid operator Terna have established clear market mechanisms for BESS participation, including capacity market auctions like the MACSE auction in 2025, which procured nearly 10 GWh of capacity, ensuring revenue streams for new projects.

- The project benefits from the broader European Union policy framework, including the EU Batteries Regulation. Starting in 2025, this regulation began introducing carbon footprint declaration requirements, which can favor locally produced batteries with a lower transport-related carbon footprint over imports.

European Battery Storage Market Growth Projected to 2029

This chart provides the essential context for the ‘Geography’ section. It demonstrates the significant projected growth in the European battery storage market, which justifies Eni’s strategy to establish Italy as a central manufacturing hub.

(Source: LinkedIn)

Technology Maturity: LFP Chemistry as the Low-Risk Choice for Stationary Storage

Eni’s selection of Lithium Iron Phosphate (LFP) chemistry for its first gigafactory is a deliberate, risk-averse decision that prioritizes the specific needs of the stationary storage market over the higher energy density chemistries used in electric vehicles. LFP is a mature, commercially proven technology (TRL 9) that offers the best balance of performance, cost, safety, and longevity for grid-scale applications.

- In the period before 2025, much of the battery industry focus was on high-energy-density chemistries like Nickel Manganese Cobalt (NMC) for the EV market.

- By 2025, LFP has become the dominant chemistry for stationary storage due to its superior safety profile, longer cycle life, and avoidance of ethically and price-volatile materials like cobalt. Its lower cost, with LFP core equipment from China reaching $75/k Wh in 2025, is a primary driver.

- Utility-scale project developers prioritize long-term reliability and a low levelized cost of storage (LCOS) over a battery’s weight or volume, making LFP the optimal choice for these applications.

- By choosing a proven technology, Eni avoids the technical and commercial risks associated with nascent battery chemistries, focusing its efforts on the challenges of manufacturing at scale rather than on fundamental technology development.

LMFP Battery Market Forecast to Reach $6.79B

The section highlights LFP as a ‘low-risk’ technology choice. This chart supports the argument by showing a strong market forecast for LMFP, a promising and related variant, indicating technological maturity and commercial viability.

(Source: Towards Automotive)

SWOT Analysis of Eni’s Battery Manufacturing Strategy

Eni’s 2025 pivot into battery manufacturing is a calculated move to build a resilient, vertically integrated position in the energy transition. The strategy leverages the company’s financial strengths to address a critical supply chain gap, but also exposes it to new operational and competitive risks outside its traditional expertise.

- The core strength of the strategy is the creation of a closed-loop system where its renewables arm, Plenitude, provides a captive market for its new manufacturing arm, Eni Storage Systems.

- The primary weakness is Eni’s inexperience in high-volume, high-precision manufacturing, a significant operational risk that it seeks to mitigate through its partnership with FIB.

- The opportunity lies in capturing a share of the rapidly expanding European BESS market, which is supported by strong policy and demand, while building a new, sustainable revenue stream.

- The main threat comes from established, high-volume Asian competitors who can leverage economies of scale to exert significant price pressure.

Eni Balance Sheet Strengthens Amid Strategic Pivot

A SWOT analysis requires evaluating internal strengths. This chart, showing a strengthening balance sheet, provides direct evidence of Eni’s financial ‘Strength,’ a critical enabler for a capital-intensive strategy.

(Source: Investing.com)

Table: SWOT Analysis for Eni’s Energy Storage Initiatives

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Strong cash flow from legacy oil and gas operations. Extensive experience in large-scale energy project management. | Creation of a vertically integrated model (Plenitude + Eni Storage Systems). Secured manufacturing expertise via FIB JV. | The company validated its ability to use its financial strength to enter new, strategic industrial sectors beyond its core business. |

| Weaknesses | High dependence on fossil fuel revenue. Lack of in-house expertise in battery technology and manufacturing. | Execution risk on a multi-billion euro gigafactory project. New exposure to manufacturing-specific challenges like raw material sourcing and quality control. | The shift exposes a new weakness: a lack of historical competency in manufacturing, which now becomes a critical factor for success. |

| Opportunities | Growing demand for renewable energy and grid services. Early-stage investments in storage asset deployment. | EU policy push for domestic supply chains (EU Batteries Regulation). Massive growth in the Italian BESS market (50 GWh target by 2030). | The opportunity crystallized from a general “growth in renewables” to a specific, actionable market entry into manufacturing, driven by policy. |

| Threats | Policy risk for fossil fuels and market volatility. Early competition in renewable project development. | Intense price competition from established Asian battery manufacturers with massive economies of scale. Potential volatility in lithium and phosphate supply chains. | The competitive threat shifted from other energy majors to specialized, low-cost global technology manufacturers in the battery sector. |

Global Battery Storage Capacity Surged in 2024

This section title indicates a table format for a SWOT analysis. This chart serves as a key data point for the ‘Opportunities’ quadrant of that table, quantifying the massive market expansion Eni is targeting.

(Source: REN21)

Scenario Modelling: Eni’s Brindisi Factory Execution as a Key 2026 Signal

The single most critical action to monitor in the coming year will be Eni’s execution of the Brindisi gigafactory project, as its success is the lynchpin of the company’s entire vertical integration strategy. Progress or delays on this front will serve as the primary indicator of Eni’s ability to transform itself into a significant player in the clean energy hardware supply chain.

- If this happens: Eni announces a final investment decision (FID) for the Brindisi plant in the first half of 2026. Watch this: The announcement should be followed by the signing of long-term offtake agreements, both internally with Plenitude and with third-party customers. This could be happening: This would validate the commercial viability of the project and signal that Eni is successfully de-risking its investment.

- If this happens: News emerges of significant raw material supply agreements for lithium and phosphate. Watch this: Look for deals with suppliers outside of the traditional Chinese-dominated sphere to assess progress on building a resilient, diversified supply chain. This could be happening: This would indicate that Eni is proactively mitigating one of the biggest risks in battery manufacturing.

- If this happens: Delays are announced for the factory’s construction timeline. Watch this: The reasons cited for the delay, whether related to permitting, financing, or partner disagreements, will be crucial. This could be happening: This could signal that the operational and financial challenges of entering a new industrial sector are proving more difficult than anticipated.

Energy Storage Pipeline Growth Accelerates Through 2025

Scenario modeling relies on forward-looking data. This chart showing an accelerating pipeline of energy storage projects is a key input for modeling the potential market and success of Eni’s Brindisi factory.

(Source: Enverus)

The questions your competitors are already asking

This report covers one angle of Eni’s commercial pivot into battery manufacturing. The questions that matter most depend on your work.

- Which energy majors are gaining or losing ground in the European battery manufacturing market?

- Eni’s investments and funding. Is the >8 GWh manufacturing scale-up on track for its 2025 targets?

- Which European energy operators are adopting a vertical integration strategy for battery storage?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.