Top 10 Sustainable Aviation Fuel Deals: IAG’s 785 k Ton Buy and Air France-KLM’s 1.5 M Ton Agreement (2024-2026)

The Sustainable Aviation Fuel (SAF) market is rapidly maturing, shifting from small, voluntary purchases to massive, multi-year offtake agreements that are essential for financing new production. Analysis of the top deals between January 2024 and June 2026 reveals that European airline groups are aggressively securing supply ahead of upcoming mandates, with two agreements alone—Air France-KLM‘s 1.5 million metric ton deal with Total Energies and International Airlines Group‘s (IAG) 785, 000 metric ton commitment to Twelve—accounting for a substantial portion of future supply. The dominant theme for 2025 is a strategic bifurcation: airlines are locking in huge volumes of conventional bio-SAF to meet immediate regulatory needs while simultaneously placing large, long-term bets on next-generation e-SAF technologies to ensure long-term scalability.

1. Loganair and Clima Htech Green Flight

Buyer: Loganair

Offtake Volume: Not Specified

Application: Decarbonizing UK regional aviation with advanced SAF.

Source: Loganair signs 15-year SAF offtake agreement with Clima Htech …

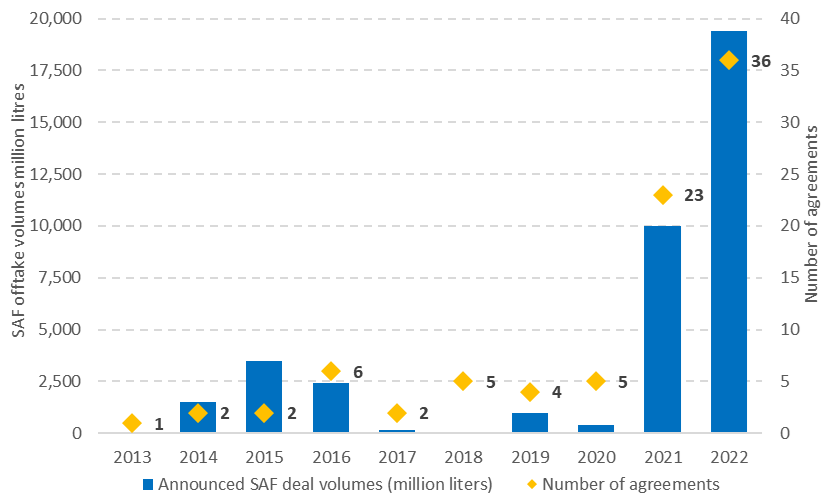

SAF Offtake Agreements See Explosive Growth

The chart contextualizes the Loganair deal, showing it as part of an industry-wide explosive growth in SAF offtake agreements.

(Source: CAPA – Centre for Aviation)

2. DHL Express and SAF One

Buyer: DHL Express

Offtake Volume: 250, 000 metric tons

Application: Securing SAF for global air cargo operations over ten years.

Source: DHL Express signs ten-year offtake deal with SAF One

3. American Airlines and Aemetis

Buyer: American Airlines

Offtake Volume: 341, 600 metric tons

Application: Long-term physical SAF supply for US domestic and international flights.

Source: Mass balance or book and claim? Capacity allocation of sustainable …

SAF Offtake Agreements Peaked Sharply in 2021

This chart provides historical context for the American Airlines agreement, showing it follows a sharp peak in deal-making activity in 2021.

(Source: Iba.aero)

4. Syzygy Plasmonics and Trafigura

Buyer: Trafigura

Offtake Volume: Entire production volume of Nova SAF-1 plant

Application: Global commodities trader securing next-generation e-SAF supply for the broader market.

Source: News Roundup January 2026 – Green Air News

SAF Market to Reach $78.8B by 2034

The chart frames the strategic importance of the Syzygy and Trafigura technology partnership by quantifying the massive projected market value they are targeting.

(Source: Market.us News)

5. Eco Ceres and British Airways (IAG)

Buyer: British Airways

Offtake Volume: Implied >150, 000 metric tons

Application: Multi-year supply to reduce lifecycle carbon emissions for the UK flag carrier.

Source: Eco Ceres, British Airways sign SAF supply agreement – Argus Media

SAF Market Projected to Exceed $40B by 2034

This market projection illustrates the financial scale of the SAF industry that the Eco Ceres and British Airways deal is contributing to.

(Source: Fortune Business Insights)

6. Qantas/Sydney Airport and Ampol

Buyer: Qantas and Sydney Airport

Offtake Volume: 1, 360 metric tons

Application: Australia’s largest single SAF import to advance local SAF availability.

Source: Sustainable Aviation Fuel Market Size & Growth Analysis 2033

US to Lead Potential SAF Feedstock Supply

This chart provides global context for the Australian-based Qantas deal by highlighting the geographic concentration of potential feedstock supply in the US, underscoring global supply chain dynamics.

(Source: Klimatic Group – Substack)

7. Phillips 66 and United Airlines

Buyer: United Airlines

Offtake Volume: Up to 24, 400 metric tons

Application: Short-term supply agreement with potential for significant expansion in 2025.

Source: Phillips 66 and United Airlines sign SAF supply agreement

United Airlines Leads in SAF Offtake Agreements

This chart directly complements the section by putting the specific Phillips 66 deal into the broader context of United Airlines’ leadership position in the number of SAF agreements.

(Source: SkiesFifty – Sustainable Aviation)

8. International Airlines Group (IAG) and Infinium

Buyer: IAG

Offtake Volume: Not Specified

Application: Securing future supply of e-SAF from green hydrogen and captured CO 2.

Source: IAG continues to go big on e-SAF as it inks 10-year offtake …

Jet Fuel Price Spike Narrows SAF Cost Gap

The chart provides crucial economic context for the IAG and Infinium e-fuel deal, showing how conventional fuel price volatility makes the economics of SAF increasingly viable.

(Source: Cleantech Group)

9. Air France-KLM and Total Energies

Buyer: Air France-KLM

Offtake Volume: 1, 500, 000 metric tons

Application: One of the industry’s largest volume commitments to secure SAF over a 10-year period.

Source: Air France-KLM ramps up its SAF offtake agreement with Total

Announced SAF Production to Exceed 60M Tonnes by 2030

This chart frames the significance of the large-scale Air France-KLM deal by comparing it to the total announced global SAF production capacity expected by 2030.

(Source: SkiesFifty – Sustainable Aviation)

10. International Airlines Group (IAG) and Twelve

Buyer: IAG

Offtake Volume: 785, 000 metric tons

Application: Landmark 14-year deal for e-SAF, signaling strong airline confidence in power-to-liquids technology.

Source: Twelve’s historic sustainable aviation fuel deal with IAG is… – DCVC

Table: Top 10 SAF Offtake Agreements (Jan 2024 – Jun 2026)

| Buyer | Offtake Volume (Metric Tons) | Application | Source |

|---|---|---|---|

| Loganair | Not Specified | Decarbonizing UK regional aviation | Loganair Agreement |

| DHL Express | 250, 000 | Securing SAF for global air cargo | DHL Express Deal |

| American Airlines | 341, 600 | Long-term supply for US flights | American Airlines Agreement |

| Trafigura | Entire plant volume | Securing e-SAF for commodities market | Trafigura Deal |

| British Airways | >150, 000 (Implied) | Multi-year supply for carbon reduction | British Airways Agreement |

| Qantas & Sydney Airport | 1, 360 | Australia’s largest single SAF import | Qantas Import |

| United Airlines | Up to 24, 400 | Short-term supply with expansion option | United Airlines Agreement |

| IAG | Not Specified | Future supply of e-SAF | IAG e-SAF Deal |

| Air France-KLM | 1, 500, 000 | Largest volume commitment over 10 years | Air France-KLM Agreement |

| IAG | 785, 000 | 14-year deal for e-SAF technology | IAG & Twelve Deal |

SAF Investment Soars, Peaking Near $3B

The chart shows the investment surge driving new technologies in the SAF space, providing context for the IAG partnership with a technology innovator like Twelve.

(Source: Cleantech Group)

SAF Adoption, IAG and Air France-KLM Lead With 2.2 M+ Ton Agreements

The diversity of buyers demonstrates SAF’s widening adoption across the logistics and energy sectors, not just within airlines. The involvement of cargo giant DHL Express with a 250, 000 metric ton deal and commodities trader Trafigura buying the entire output of a plant signals that SAF is becoming an integrated part of the broader energy and supply chain economy. These agreements, characterized by long durations of 10 to 15 years, are crucial financial instruments. They provide the demand certainty that producers like Aemetis and Clima Htech Green Flight need to secure project financing for capital-intensive production facilities, transforming SAF from a corporate social responsibility initiative into a core, bankable business strategy.

United Airlines Leads in SAF Offtake Volume

The chart provides a contrasting, data-driven market overview, showing that while European airlines are making large agreements, United Airlines currently leads the pack in total offtake volume.

(Source: QS Newsletters)

European Leadership, IAG and Air France-KLM Dominate SAF Offtake

A clear geographical pattern shows European airline groups leading the procurement charge. IAG and Air France-KLM are by far the most aggressive offtakers, a direct reaction to looming regional mandates like the Re Fuel EU Aviation regulation, which requires a 2% SAF blend starting in 2025. This regulatory stick provides the market certainty needed to justify multi-million-ton commitments. While US carriers like American Airlines and United Airlines have also signed significant deals, they are generally smaller in total volume or shorter in duration. Meanwhile, the global nature of the supply chain is evident, with production facilities in Bahrain (SAF One) and Hong Kong (Eco Ceres) being developed to meet this surging European-led demand. The Qantas deal highlights a different regional dynamic, where a lack of local production makes importing SAF the only current viable option.

Global Policies Drive SAF Adoption Targets

The chart explains a key driver behind the European leadership discussed in the section, illustrating how strong policy mandates in regions like the EU are compelling airlines to secure SAF.

(Source: World Energy)

Twelve’s e-SAF Tech, A 785, 000 Ton Bet by IAG on Scalability

These agreements reveal a market operating on two distinct technology tracks. The first track involves commercially mature, HEFA-based bio-SAF, exemplified by the massive 1.5 million ton deal between Air France-KLM and energy major Total Energies. This is the pragmatic, low-risk path to meeting near-term 2025 mandates. The second, more forward-looking track is the strategic investment in e-SAF (also known as power-to-liquids). IAG‘s landmark 785, 000 metric ton, 14-year agreement with Twelve is a powerful signal of confidence in this nascent technology. While less mature, e-SAF’s use of captured CO 2 and green hydrogen as feedstocks promises greater long-term scalability without the constraints of biomass availability. IAG’s parallel deal with Infinium and Trafigura’s with Syzygy Plasmonics reinforce that the industry’s largest players are using long-term offtakes to finance and de-risk the next generation of SAF technology.

Market Map Highlights 10 Key SAF Startups

This market map visually situates Twelve, the focus of the section, within the broader ecosystem of key technology startups pioneering SAF production.

(Source: NatureTech Memos)

1.5 M Tons, Air France-KLM Signals A SAF Supply Squeeze

For airlines and fuel suppliers, the primary strategic imperative for the year ahead is to secure long-term SAF supply or risk being exposed to significant price volatility and supply shortages as binding mandates take effect in 2025. The scale of recent offtake agreements indicates that proactive players are already locking up a large portion of the world’s projected near-term SAF output.

- If the reported gap between announced deal volumes and actual SAF production volumes continues to widen, watch for a scramble for supply that could see airlines paying steep premiums or non-compliance penalties. This would intensify M&A activity as larger players look to acquire smaller SAF producers to secure their supply chains.

- If e-SAF producers like Twelve and Infinium meet their production timelines for deliveries beginning around 2028, this could signal an accelerated cost-down curve for synthetic fuels. This would put significant pressure on conventional bio-SAF producers to compete on both price and feedstock sustainability.

- If more logistics and trading firms like DHL and Trafigura continue to enter the offtake market, watch for increased competition for a limited SAF pool. This could drive up the base cost of SAF for all end-users, especially airlines that have not secured fixed-price, long-term contracts.

Announced SAF Supply Projected to 2030

The chart visually demonstrates the ‘supply squeeze’ mentioned in the headline by showing the total projected supply, providing a scale against which large offtake deals can be judged.

(Source: RMI)

The questions your competitors are already asking

This report covers one angle of the emerging market for SAF offtake agreements. The questions that matter most depend on your work.

- Which airlines are gaining or losing ground in securing both conventional bio-SAF and next-generation e-SAF supply?

- What is the outlook for e-SAF deployment in the aviation sector by 2030?

- How does conventional bio-SAF (HEFA) compare to e-SAF for scalability and cost-reduction pathways?

- Which major airline groups, beyond Air France-KLM and IAG, are actively seeking large-volume SAF offtake agreements?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.