ENOC CCUS Under UAE Climate Law, Emirates SAF Mo U, and $11 B ADNOC Financing (2021-2025)

CCUS Adoption, ENOC and ADNOC Projects Under New UAE Climate Law

The 2025 UAE Federal Climate Law has fundamentally shifted Carbon Capture, Utilization, and Storage (CCUS) from a voluntary, niche activity into a mandatory compliance requirement for national oil companies, forcing a clear divergence in strategy between first movers and strategic evaluators. This new regulatory pressure has created a distinct split between companies accelerating large-scale deployment and those taking a more measured, preparatory approach.

- Between 2021 and 2024, CCUS in the region was primarily defined by pioneering projects like the Al Reyadah facility, operated by Abu Dhabi National Oil Company (ADNOC). For other state-owned enterprises like Emirates National Oil Company (ENOC), large-scale carbon capture was not a publicly stated priority, with activities focused on core business operations.

- The strategic landscape changed decisively in 2025 with the enactment of the UAE Federal Law on the Reduction of Climate Change Effects on May 30, 2025. This legislation mandates that major entities report their greenhouse gas emissions and formulate concrete reduction plans, creating an immediate and powerful driver for CCUS investment.

- ENOC’s most significant public initiative in 2025 was a Memorandum of Understanding (Mo U) signed in November with Emirates airline to conduct feasibility studies on Sustainable Aviation Fuel (SAF). This move represents a cautious, low-capital entry point into the carbon management value chain, positioning captured CO₂ as a potential future feedstock for e-fuels rather than committing to immediate point-source capture.

- In stark contrast, ADNOC demonstrated an aggressive investment posture in 2025 by securing a landmark $11 billion structured financing deal for its Hail and Ghasha gas development, a project integral to its low-carbon strategy that incorporates CCUS. This highlights a commitment to immediate, large-scale infrastructure deployment.

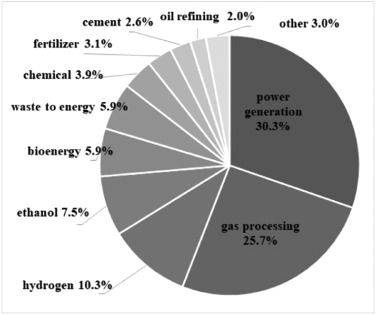

Power and Gas Sectors Dominate CCUS Projects

The section discusses CCUS projects by ENOC and ADNOC, both operating in the oil and gas sector. This chart provides essential context by showing that the power and gas industries are the leading developers of CCUS projects, validating the strategic focus of these UAE-based companies.

(Source: ScienceDirect.com)

$500 M per Mtpa, ENOC CCUS Project Cost Dynamics in MENA

While ENOC announced no direct capital investments in CCUS projects in 2025, the well-defined cost environment in the region and the significant spending by its national counterpart, ADNOC, provide a clear rationale for its cautious, asset-light approach. The substantial capital expenditure required for new projects explains the company’s current focus on strategic evaluation and partnership exploration before committing to multi-billion-dollar infrastructure.

- The established benchmark for new, large-scale CCUS projects in the Middle East and North Africa (MENA) region is approximately $500 million in CAPEX per million tonnes per annum (Mtpa) of CO₂ captured, with operational expenditures running at about 5% of CAPEX.

- Competitor spending in 2025 underscored the high-cost nature of these commitments. ADNOC not only secured $11 billion in project financing for its Hail and Ghasha development but its subsidiary, TA’ZIZ, also awarded a $1.7 billion EPC contract for a new methanol plant, a key industrial process for CCUS application.

- ENOC’s capital allocation in 2025 remained focused on its core retail business, including the opening of three new service stations in Dubai in February. This signals a deliberate strategy to observe market developments and technology cost curves before diverting significant capital to CCUS.

- Lifecycle costs for advanced carbon capture technologies are becoming more competitive, with some solvent-based systems targeting a range of $35-40 per tonne. This improving economic outlook likely informs ENOC’s decision to wait, potentially allowing it to deploy more advanced, lower-cost technology in the future.

Cost Analysis of Urea Production via Direct Air Capture

The section focuses on the cost dynamics of CCUS projects in MENA. This chart offers a specific example of a cost analysis for a process that utilizes captured carbon (Direct Air Capture to Urea), illustrating the type of economic evaluation that underpins the investment figures mentioned in the section.

(Source: Carbon Removal Updates – Substack)

Table: Regional Energy Transition Investments and Projects (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ADNOC / Hail and Ghasha Project | Dec 2025 | Secured up to $11 billion in structured financing for a key gas development project that integrates CCUS as part of ADNOC‘s low-carbon growth strategy. | Europétrole |

| TA’ZIZ (ADNOC JV) / SAMSUNG E&A | Feb 2025 | Awarded a $1.7 billion (AED 6.2 billion) EPC contract for the construction of the first methanol production facility in the UAE, a prime candidate for future CCUS integration. | Europétrole |

MENA Renewables Share to Double by 2030

The section, a table on regional energy transition investments, is complemented by this chart. It visualizes a key macro trend of this transition—the rapid growth of renewables in MENA—providing a high-level context for the specific projects and investments detailed in the table.

(Source: Middle East Institute)

ENOC 1 SAF Mo U with Emirates, ADNOC Alliances (2025)

In 2025, ENOC’s partnership strategy in the decarbonization space was characterized by a single, foundational agreement focused on future fuel supply chains. This stands in contrast to the multi-billion-dollar EPC and financing agreements executed by its competitors, clearly establishing a “follower versus leader” dynamic in the race to build out the UAE’s low-carbon infrastructure.

- ENOC’s primary partnership was a Memorandum of Understanding signed with Emirates airline on November 19, 2025. This pre-commercial agreement focuses on studying the feasibility of SAF supply in Dubai, representing an exploratory step into a value chain where captured CO₂ is a critical feedstock for synthetic e-fuels.

- By comparison, ADNOC‘s joint venture TA’ZIZ moved decisively from study to execution by awarding a $1.7 billion Engineering, Procurement, and Construction (EPC) contract to SAMSUNG E&A for a world-scale methanol plant, a project with clear synergies for CCUS.

- The ecosystem around these large projects is also solidifying. In October 2025, SAMSUNG E&A and Honeywell signed their own Mo U to collaborate on projects using advanced solvent carbon capture technologies, indicating that technology providers are aligning with major capital projects.

- ADNOC’s ability to secure an $11 billion financing package for its Hail and Ghasha project demonstrates its capacity to attract significant international capital, a critical enabler for its large-scale, integrated energy transition strategy.

Global Transport GHG Emissions Reached 8.9 Gt in 2019

The section details a strategic Memorandum of Understanding (MoU) for Sustainable Aviation Fuel (SAF). This chart provides the critical rationale for such an agreement by quantifying the massive scale of greenhouse gas emissions from the global transport sector, underscoring the urgency for solutions like SAF.

Table: ENOC and Competitor Decarbonization Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ENOC / Emirates | Nov 2025 | Mo U to conduct feasibility studies for SAF supply opportunities in Dubai. This is an indirect, low-capital entry into the carbon value chain via e-fuels. | Oil Price.com |

| SAMSUNG E&A / Honeywell | Oct 2025 | Mo U to collaborate on projects utilizing Honeywell‘s advanced solvent carbon capture (ASCC) technology, aiming to improve efficiency in the energy sector. | Europétrole |

Oil & Gas Companies Ranked by Gas Flaring

The section is a comparative table of decarbonization partnerships. This chart provides a competitive benchmark by ranking oil and gas companies on gas flaring, a key decarbonization metric. It visualizes the peer pressure on companies like ENOC to improve environmental performance and pursue decarbonization efforts.

(Source: Clean Air Task Force)

MENA vs Global, ENOC’s Role in UAE’s CCUS Hub Strategy

In 2025, the UAE solidified its position as a central hub for CCUS development within the MENA region, propelled by a new national climate policy and the strategic imperative for its state-owned oil companies, including ENOC, to actively decarbonize their operations. This pivot is transforming the country into a key growth market within the expanding global CCUS landscape.

- While the UAE had flagship CCUS projects prior to 2025, the country’s new climate law and its national target to build 5 million tons per annum (Mtpa) of CCUS capacity by 2030 have significantly accelerated strategic planning and investment.

- Globally, the CCUS project pipeline expanded rapidly in 2025, with the number of operational projects rising by 54% year-over-year to 77 projects. The UAE’s national ambition is a key contributor to this global momentum.

- The UAE’s strategy is centered on developing carbon capture hubs in defined geographic clusters to enhance efficiency and achieve economies of scale. This framework ensures that ENOC‘s future projects will not exist in isolation but will be integrated into this national infrastructure.

- While ADNOC leads development in Abu Dhabi, ENOC’s operations in Dubai, particularly its SAF partnership with Emirates, position it to play a crucial role in decarbonizing the aviation sector, a vital economic engine for both the emirate and the nation.

Global CO2 Storage Capacity Accelerates Significantly

The section compares MENA’s CCUS strategy to the global context. This chart directly supports the ‘MENA vs Global’ theme by illustrating the accelerating worldwide trend in CO2 storage capacity, setting the stage to analyze how the UAE’s and ENOC’s ambitions fit within this global momentum.

(Source: Carbon Removal Updates – Substack)

Technology Evaluation, ENOC’s Indirect Path via SAF and E-fuels

In 2025, ENOC strategically bypassed direct investment in mature point-source capture technologies, opting instead for a calculated entry into the Sustainable Aviation Fuel value chain. This approach positions the company to capitalize on future, more advanced CCUS technologies required for e-fuel production, avoiding the risk of being locked into current-generation assets.

- Prior to 2025, the primary focus of regional CCUS was on established post-combustion capture from large industrial sources, a technology proven by ADNOC‘s Al Reyadah project.

- ENOC‘s 2025 feasibility study on SAF represents an indirect but strategic bet on the next generation of CCUS. The production of e-SAF requires large volumes of captured CO₂ and green hydrogen, linking ENOC‘s future to the successful scale-up of these technologies.

- This “wait-and-see” approach allows ENOC to benefit from continued innovation in the sector. For instance, advanced solvent technologies from providers like Honeywell are targeting a competitive cost range of $35-40 per tonne of CO₂, making future project economics more favorable.

- While still far too expensive for this application, the development of Direct Air Capture (DAC), with costs ranging from $400 to $1, 500 per tonne, demonstrates the broad spectrum of innovation. ENOC‘s strategy allows it to observe this technological maturation from a distance before committing capital.

GCC Algae Biofuel Market Eyes $231M by 2031

The section evaluates technology paths, specifically SAF and e-fuels. This chart provides a tangible data point for this evaluation by showing the market projection for algae biofuel, a potential SAF feedstock, within the GCC. It offers a specific market-based insight into a relevant production technology.

(Source: Mordor Intelligence)

SWOT Analysis, ENOC CCUS Strategy and Market Position

ENOC‘s 2025 CCUS position is defined by the strength of its government mandate, offset by its status as a latecomer in large-scale deployment. This creates a critical opportunity to leverage competitor lessons but also a significant threat from falling behind on compliance and market share in the UAE’s rapidly evolving energy transition.

GCC Leads MENA Energy Demand Growth

The section is a SWOT analysis of ENOC’s strategy. This chart highlights a core market driver, showing that rising energy demand in the GCC presents both an Opportunity (a growing market for an energy provider) and a Threat (increasing pressure to decarbonize that growing supply), which are fundamental inputs for a SWOT analysis.

(Source: Middle East Institute)

Table: SWOT Analysis for ENOC CCUS Strategy (2025)

| SWOT Category | 2021 – 2024 (Pre-Law) | 2025 (Post-Law) | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong downstream and retail network; government ownership. | Clear mandate from new Federal Climate Law; strategic partnership with key offtaker (Emirates). | The 2025 climate law transformed government backing from implicit support to an explicit, legally binding driver for decarbonization. |

| Weaknesses | No public-facing CCUS projects or stated strategy. | Lack of large-scale operational CCUS projects; public perception as a follower to ADNOC; capital still focused on core retail business. | ADNOC’s multi-billion-dollar announcements in 2025 validated ENOC‘s position as a strategic follower, not a first mover. |

| Opportunities | Potential to learn from early movers and adopt more efficient technologies later. | Leverage competitor learnings (ADNOC‘s projects); develop a niche in SAF/e-fuels; utilize new national carbon credit market. | The establishment of the National Carbon Credit Registry in 2025 created a new market-based mechanism that did not exist previously. |

| Threats | Reputational risk from inaction on climate change. | Compliance risk and potential penalties under the new climate law; losing competitive ground to ADNOC in technology, talent, and prime storage assets. | The threat shifted from reputational to legal and financial with the enforcement of the UAE Climate Law in May 2025. |

ENOC 2026 Outlook, SAF Study Triggering CCUS Investment

The most critical signal to watch for ENOC in 2026 is the announcement of a pilot project or joint venture for CCUS or e-fuel production. Such a move would be a direct consequence of its 2025 SAF feasibility study and its first mandatory emissions reports under the new UAE climate law, marking a definitive shift from evaluation to execution.

- If this happens: The feasibility study with Emirates concludes with a positive business case for local SAF production.

- Watch this: ENOC announces a firm investment decision or a joint venture for a pilot-scale e-fuel production facility. This would almost certainly trigger a parallel investment in a carbon capture source to secure the necessary CO₂ feedstock.

- These could be happening: ENOC begins to actively participate in the UAE’s new National Carbon Credit Registry, either as a buyer to meet initial compliance obligations or as a developer of projects to generate credits. The government’s decision to extend 0% corporate tax to carbon credit trading makes this an attractive option.

- Signal Failure: A failure by ENOC to announce any concrete decarbonization projects or capital allocation shifts in its 2026 budget would signal a significant strategic lag, indicating that the company is falling further behind its national peers and increasing its compliance risk under the new federal law.

The questions your competitors are already asking

This report covers one angle of ENOC’s strategic positioning in the UAE’s carbon management market. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the UAE CCUS market under the new Federal Climate Law?

- ENOC activities in carbon management. Is the Emirates SAF partnership progressing from a feasibility MoU to a pilot project?

- ADNOC investments and funding. Is the $11B financing accelerating CCUS deployment beyond the Al Reyadah project?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.