Blue Hydrogen’s 2026 Reality Check: Why Offtake Agreements Are Stalling Megaprojects

Blue Hydrogen Projects Stall in 2026 as Commercial Viability Falters

Large-scale blue hydrogen projects are failing to advance from planning to construction due to a critical lack of bankable offtake agreements, a significant shift from the ambitious project announcements that defined the 2021-2024 period. While companies like Equinor possess the technical expertise to produce low-carbon hydrogen, the market has not matured quickly enough to absorb the supply, leading to major strategic setbacks.

- Between 2021 and 2024, the industry saw a wave of ambitious announcements, including Equinor’s plans for 1.8 GW of production in the UK’s Humber region with its H 2 H Saltend and H 2 H Production 2 projects. These were framed as foundational elements of Europe’s new hydrogen economy.

- The period from 2025 to 2026 has delivered a harsh commercial reality. In February 2026, Equinor cancelled a flagship 1 GW EU-backed blue hydrogen project in the Netherlands, explicitly citing a failure to secure long-term buyers. This followed the September 2024 cancellation of a planned €3 billion pipeline to transport blue hydrogen from Norway to Germany.

- The consistent reason for these cancellations is an inability to secure offtake agreements. Potential industrial customers are unwilling to commit to long-term contracts for higher-priced low-carbon hydrogen without robust government subsidies and price stability, a risk producers are not willing to bear alone.

- Consequently, successful projects are now smaller test cases for market creation. The H 2 BE project in Belgium, launched in February 2026 with partner ENGIE, is designed to build a regional demand hub from the ground up, representing a tactical retreat from the earlier vision of supplying a vast, ready-made European market.

Uncontracted Hydrogen Projects Highlight Market Risk

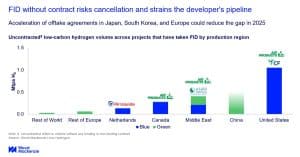

This chart perfectly illustrates the section’s main point that projects are stalling due to a lack of buyers by showing the high volume of project capacity lacking offtake agreements.

(Source: Carbon Credits)

Major Project Cancellations Signal Investor Caution in 2026

The cancellation of multi-billion-euro infrastructure projects signals a significant recalibration of investment risk, as the capital-intensive nature of blue hydrogen is proving unsupportable without guaranteed revenue streams. This has forced major players to pause or reverse significant capital allocation plans, indicating that investor confidence is now directly tied to the presence of firm customer commitments.

Major Blue Hydrogen Project Cancelled in 2025

The chart provides a direct, concrete example of the major project cancellations discussed in the section, specifically noting the withdrawal of BP from its large-scale blue hydrogen project.

(Source: Global Hydrogen Hub)

- The decision in September 2024 to scrap the planned €3 billion, 10 GW hydrogen pipeline from Norway to Germany was the first major signal that project economics were failing. The total supply chain cost was estimated in the “tens of billion euros, ” a figure that became untenable without clear demand signals from German industry.

- This was followed by the cancellation of the 1 GW H-vision project in the Port of Rotterdam in February 2026. Despite being backed by the EU, Equinor could not secure the necessary offtake agreements, demonstrating that even with policy support, projects cannot proceed on a speculative basis.

- These commercial failures have a direct impact on enabling infrastructure. In February 2026, Equinor announced it was scaling back near-term investment plans for Carbon Capture and Storage (CCS) expansion, a direct response to weakening market signals and a more cautious capital allocation strategy.

Table: Key Blue Hydrogen Project Cancellations and Investment Revisions (2025-2026)

| Project / Investment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| H-vision Blue Hydrogen Project | February 2026 | A 1 GW EU-backed blue hydrogen plant in the Netherlands was cancelled due to a lack of offtake demand and an inability to secure long-term purchase agreements. | Equinor Scraps EU-Backed 1 GW Blue Hydrogen Project |

| CCS Expansion Plans | February 2026 | Equinor scaled back near-term investment plans for CCS infrastructure, citing project economics and customer demand failing to mature at the expected pace. | Equinor Steps Back From CCS Expansion |

| Norway-Germany Hydrogen Pipeline | September 2024 | The ambitious €3 billion plan to transport up to 10 GW of blue hydrogen was scrapped due to unviable economics and insufficient demand from the German market. | Equinor scraps plan for hydrogen pipeline to Germany |

Partnerships Pivot from Production to Market Creation for Equinor’s Hydrogen Strategy

Strategic partnerships are evolving from purely production-focused alliances to collaborative efforts aimed at stimulating demand and de-risking the entire value chain. Faced with a hesitant customer base, Equinor and its peers are now using partnerships to create the commercial frameworks necessary for the hydrogen economy to function.

- The H 2 BE project with ENGIE, launched in February 2026, exemplifies this new model. Instead of just producing hydrogen, the partnership is focused on building a captive market by supplying a cluster of industrial users in Belgium, effectively creating demand where it was previously nascent.

- An innovative clause in the £20 bn natural gas supply deal with Centrica, signed in June 2025, creates a tangible offtake pathway. The agreement allows for the future swapping of natural gas volumes for blue hydrogen, de-risking future production by embedding a major utility as a potential anchor customer.

- Collaboration has also extended to policy advocacy. In March 2025, Equinor joined industrial gas giant Linde and other players to jointly lobby for new EU “incentive schemes.” This shows a recognition that without a favorable regulatory and subsidy framework, the market will not develop on its own.

Table: Equinor’s Strategic Hydrogen Partnerships Focused on Market Development

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ENGIE (H 2 BE Project) | February 2026 | Launched a project to develop low-carbon hydrogen production with CCS in Belgium, aiming to kick-start the regional market by supplying local industrial players. | ENGIE & Equinor launch the H 2 BE project |

| Centrica (Supply Agreement) | June 2025 | Signed a £20 bn gas deal that includes a novel clause to potentially swap natural gas volumes for blue hydrogen, creating a future commercial pathway to the UK market. | Hydrogen swaps | Blue H 2 offtake clause included in £20 bn gas deal |

| Linde (Policy Advocacy) | March 2025 | Jointly advocated for new EU “incentive schemes” to improve the economic viability of blue hydrogen, a partnership focused on shaping market rules. | EU Clean Industrial Deal in action |

UK’s Industrial Clusters Become Last Bastion for Equinor’s Blue Hydrogen Ambitions

While grand cross-border hydrogen plans for mainland Europe have faltered, the UK’s concentrated industrial clusters like the Humber region remain the most viable geographic focus for near-term blue hydrogen development. This geographic retrenchment reflects a pragmatic shift from broad, ambitious export strategies to a more targeted, demand-centric approach.

- The vision between 2021 and 2024 was expansive, envisioning a hydrogen network connecting Norway to major industrial centers in Germany, Belgium, and the Netherlands. This was underpinned by large-scale production and transport projects.

- The 2025-2026 reality is a dramatically smaller geographic footprint. The cancellation of the Norway-Germany pipeline and the failure of the 1 GW project in the Netherlands have effectively closed off the largest planned export markets for the near future.

- In contrast, the UK’s Humber region remains a strategic priority. Projects like the 600 MW H 2 H Saltend, which received planning permission in February 2024, and the proposed 1.2 GW H 2 H Production 2 are still advancing. Their viability is tied to the concentrated cluster of industrial offtakers in the immediate vicinity.

- Belgium remains a secondary point of interest with the H 2 BE project. However, this represents a single, localized industrial hub rather than a large-scale national market, reinforcing the new strategy of focusing on geographically contained, high-demand zones. The risk of a broader 2026 energy crisis has not yet been enough to compel governments to underwrite the large-scale infrastructure needed for a pan-European market.

Blue Hydrogen Technology Is Ready, but the Commercial Framework Lags in 2026

The core technologies for blue hydrogen production, such as Autothermal Reforming (ATR) and Carbon Capture and Storage (CCS), are mature and available. However, their deployment at scale is being blocked by economic and market-related barriers, not technical ones. The problem is no longer how to make blue hydrogen, but how to make it affordable for customers.

Fossil Fuels Dominate Current Hydrogen Market

This chart supports the section’s argument that the commercial framework is lagging by showing how current production is overwhelmingly fossil-fuel based, while new clean hydrogen uses are negligible.

(Source: Nature)

- In the 2021-2024 period, the technical path was clear. Companies focused on selecting technologies like ATR for its high carbon capture rates of over 95%. The advancement of the Northern Lights CCS project, which reached a final investment decision for its second stage in April 2025, demonstrated the technical feasibility of the required infrastructure.

- By 2025-2026, it became evident that technical readiness does not equate to commercial viability. The cancellation of the fully planned 1 GW Netherlands project was a clear signal that the high cost of production, even with mature technology, is a deal-breaker for customers without subsidies.

- This commercial roadblock for blue hydrogen stands in contrast to Equinor‘s ongoing venture investments in green hydrogen startups like Hystar and Electric Hydrogen. These investments target next-generation electrolyzers to drive down future production costs, an implicit acknowledgment that blue hydrogen’s current cost structure is a significant market weakness.

- The threat is compounded by projections that green hydrogen costs could fall to $2.5/kg by 2030, making it cheaper than blue hydrogen. This places immense pressure on blue hydrogen projects to secure customers and lock in revenue before their cost advantage disappears.

SWOT Analysis: Equinor’s Hydrogen Strategy at a Commercial Crossroads in 2026

Equinor‘s hydrogen strategy leverages its formidable strengths in natural gas and CCS, but it faces critical market-based weaknesses and external threats that have become acutely apparent in 2025-2026. The company’s technical capabilities are proven, but its ability to create a commercially viable market for its product remains the central challenge.

- Strengths in existing assets and technical expertise are being undermined by Weaknesses related to high costs and the inability to secure offtake agreements.

- Opportunities presented by government decarbonization policies are being tempered by the Threats of insufficient near-term demand and increasing competition from lower-cost green hydrogen.

Table: SWOT Analysis for Blue Hydrogen Commercial Viability

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Extensive natural gas reserves and deep expertise in Carbon Capture and Storage (CCS). Partnerships with major utilities like RWE. | FID reached on Northern Lights Stage 2 (CCS). Signed innovative gas/hydrogen swap deal with Centrica. Launched demand-creation project (H 2 BE) with ENGIE. | The technical capability to produce blue hydrogen and store carbon has been validated. The strategic focus has shifted to validating the commercial model through novel partnerships and contracts. |

| Weaknesses | High capital intensity of projects. Heavy reliance on future government subsidies and policy frameworks to be profitable. | Failed to secure offtake for major projects. High infrastructure costs (€3 B for one pipeline) proved prohibitive. Scaled back CCS investment due to weak demand. | The theoretical weakness of high cost and subsidy dependence was validated as a critical business constraint, leading directly to the cancellation of flagship projects. |

| Opportunities | EU and UK set ambitious decarbonization and hydrogen production targets, creating a large potential future market. | Pivoted to a more focused strategy targeting concentrated industrial hubs (Humber, Belgium). Deployed creative contract structures (Centrica deal) to seed future demand. | The strategy has shifted from relying on broad, top-down policy goals to a more pragmatic, bottom-up approach of creating localized, bankable markets. |

| Threats | Risk of policy delays or insufficient subsidies. Projections of green hydrogen becoming cheaper than blue by 2030. | Nascent demand proved insufficient to support large-scale investment. Pipeline economics failed commercial tests. Competition from green hydrogen ventures is accelerating. | The threat of immature demand has materialized, proving to be the single biggest obstacle to growth. The long-term threat from green hydrogen is becoming more acute as blue hydrogen projects stall. |

Forward Outlook: Will Industrial Hubs and Policy Rescue Blue Hydrogen’s Future?

The survival of large-scale blue hydrogen projects now depends on the success of a more focused, hub-based strategy and the materialization of government-backed incentives to bridge the commercial viability gap. The industry is watching to see if this tactical pivot can succeed where grander strategies have failed.

Ambitious Hydrogen Project Pipeline Faces Uncertainty

This chart visualizes the large pipeline of announced hydrogen projects, providing context for the section’s forward-looking question of whether these ambitious plans can be rescued from stalling.

(Source: Net Zero Technology Centre)

- If Equinor and its partners secure binding offtake agreements for the Humber projects, watch for Final Investment Decisions (FIDs) in late 2026 or early 2027. A positive FID on H 2 H Saltend would be the first major validation of the industrial hub model in Europe and could unlock further investment.

- If offtake demand remains weak despite a more focused approach, watch for further project delays and a potential strategic pivot by major players to allocate more capital toward their green hydrogen portfolios and smaller, more manageable blue hydrogen initiatives.

- The most critical external signal is government action. The structure and funding of UK subsidy schemes and the results of the EU’s Hydrogen Bank auctions are essential. Without these mechanisms to close the cost gap, the commercial case for blue hydrogen will remain broken, and private capital will remain on the sidelines.

Frequently Asked Questions

Why are major blue hydrogen projects being cancelled in 2026?

Large-scale blue hydrogen projects are being cancelled primarily due to a lack of bankable offtake agreements. Potential industrial customers are not willing to commit to long-term contracts to purchase higher-priced low-carbon hydrogen without robust government subsidies, making the multi-billion-euro projects commercially unviable for producers like Equinor.

What is Equinor’s new strategy for blue hydrogen after these cancellations?

Equinor has pivoted from large, cross-border export plans to a more focused, hub-based strategy. Instead of trying to supply a vast European market, it is now concentrating on creating demand within specific industrial clusters, such as the Humber region in the UK and through its H2BE project in Belgium, aiming to build a customer base from the ground up.

Is the technology for blue hydrogen the reason these projects are failing?

No, the technology is not the problem. The article states that the core technologies for blue hydrogen production, like Autothermal Reforming (ATR) and Carbon Capture and Storage (CCS), are mature and technically ready. The failure is commercial; the high cost of production makes it unaffordable for customers without subsidies, blocking the projects from proceeding.

How are partnerships in the hydrogen sector changing?

Partnerships are evolving from being purely production-focused to being centered on market creation and de-risking. For example, Equinor’s H2BE project with ENGIE aims to build a regional demand hub, its gas deal with Centrica includes a clause to swap gas for hydrogen in the future, and its collaboration with Linde involves lobbying for government incentives to make the market viable.

What needs to happen for blue hydrogen to become successful in the future?

For blue hydrogen to succeed, two key things must happen. First, the new ‘industrial hub’ strategy must prove successful by securing firm, binding offtake agreements from concentrated clusters of industrial users. Second, governments must introduce effective and well-funded subsidy schemes and incentives, like the EU’s Hydrogen Bank, to bridge the price gap and make blue hydrogen commercially attractive for customers.