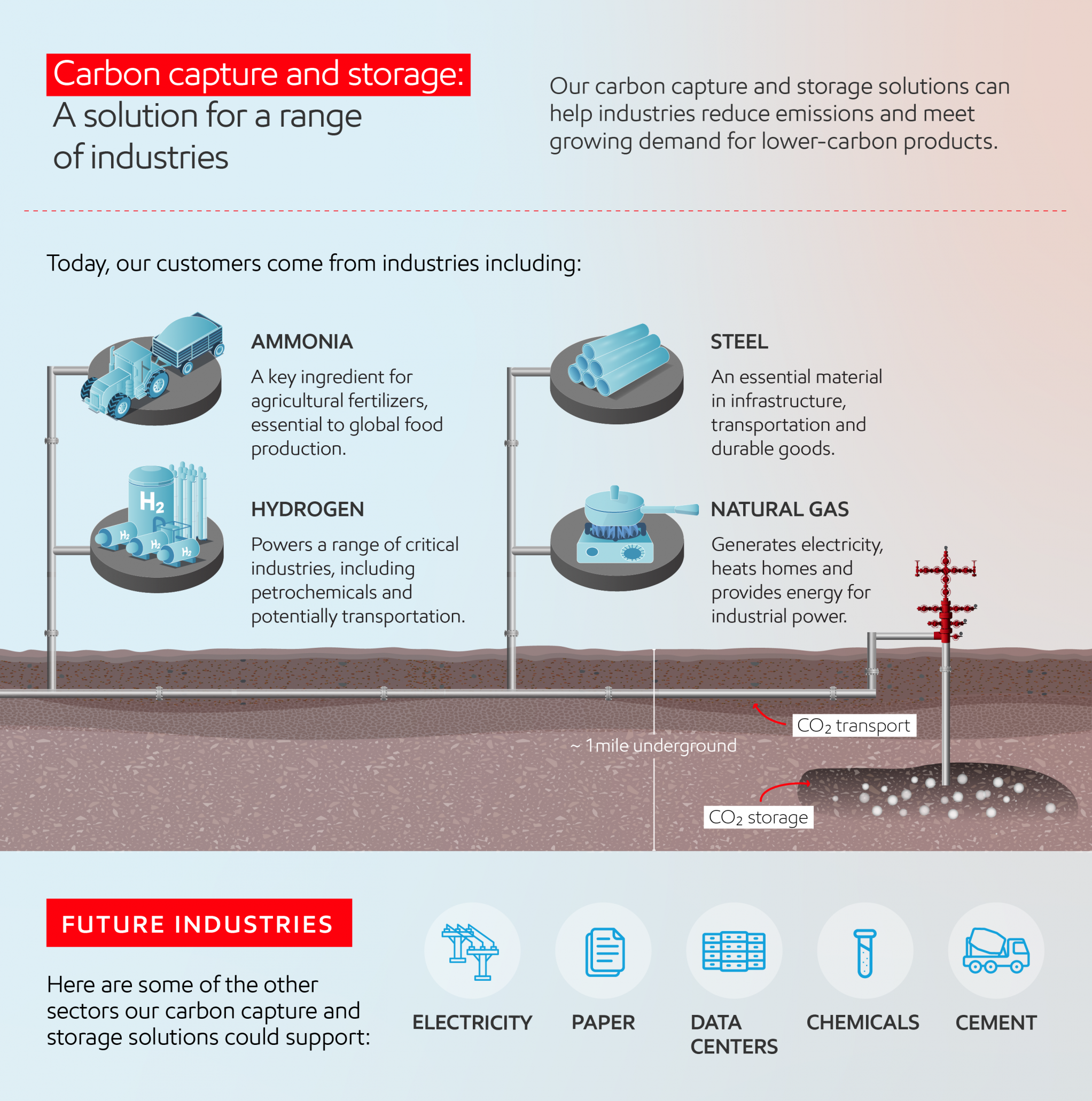

Exxon Mobil CCUS Strategy, $10 B Spending Cut, 2 MMTPA Calpine Deal, and 5 New Agreements (2021 to 2025)

CCUS Commercial Projects, Exxon Mobil Industrial Hub Strategy

In 2025, Exxon Mobil’s carbon capture strategy shifted from broad ambition to a concentrated commercial execution focused on building a carbon-management-as-a-service business, a departure from its more exploratory activities between 2021 and 2024. The company’s recent actions are designed to create a defensible economic moat in key industrial corridors, leveraging its geological and infrastructure expertise to serve third-party emitters.

- Prior to 2025, Exxon Mobil’s public strategy centered on large-scale concepts and capacity building. The period from 2025 to today is defined by the signing of tangible, large-volume offtake agreements that validate its “hub and spoke” business model.

- A key April 2025 agreement with power generator Calpine established a plan to transport and store up to 2 million metric tons of CO₂ per year, showcasing the model’s application to the power sector, which often relies on gas turbines from manufacturers like GE Vernova.

- This was followed by a September 2025 deal with Atmos Clear, its fifth such agreement in Louisiana, demonstrating significant commercial traction in building a regional network for industrial clients.

- The company also secured agreements with industrial players like the NG 3 Project for 1.2 million metric tons annually and CF Industries, diversifying its customer base beyond power generation into hard-to-abate sectors like ammonia production.

ExxonMobil Visualizes Its Carbon-as-a-Service Strategy

This section describes ExxonMobil’s industrial hub strategy. The chart, which visualizes a ‘Carbon-as-a-Service’ model, perfectly illustrates the business and operational framework behind that hub strategy.

(Source: ExxonMobil)

$10 B Spending Cut, Exxon Mobil Capital Reallocation

Exxon Mobil’s 2025 financial strategy for low-carbon initiatives is marked by a pragmatic recalibration, directly linking capital deployment to policy certainty and expected returns. This represents a more cautious investment posture compared to the broader commitments of previous years, signaling to the market that government incentives are a primary driver of project economics.

- In a pivotal announcement in December 2025, Exxon Mobil revealed a $10 billion reduction in its low-carbon spending plan through 2030, redirecting that capital toward traditional upstream oil and gas projects.

- The revised plan allocates approximately $20 billion for lower-emission investments between 2025 and 2030, with a significant portion, about 60%, aimed at reducing the company’s own operational emissions.

- This investment moderation highlights the profound influence of government policy, particularly the 45 Q tax credit, which provides up to $85 per metric ton for geologically stored CO₂ and underpins the financial viability of these projects.

- The potential delay or cancellation of the $7 billion Baytown clean hydrogen plant underscores this dependency, as its feasibility hinges on favorable interpretations of both the 45 Q and 45 V tax credits.

Charts Detail Sources of Industrial CO2 Emissions

This section discusses capital reallocation. The chart identifies the specific industrial sectors that are major sources of CO2, thereby explaining and justifying the strategic decision to reallocate capital towards CCUS solutions for these industries.

(Source: ExxonMobil)

Table: Exxon Mobil Low-Carbon Investment and Strategic Actions

| Project / Action | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Low-Carbon Spending Cut | Dec 11, 2025 | A $10 billion reduction in the planned low-carbon budget, with capital reallocated to higher-return upstream oil and gas business lines. | The Chemical Engineer |

| Revised Investment Plan | Dec 10, 2025 | Established a new $20 billion spending target for lower-emission projects for the 2025-2030 period, with 60% focused on internal emissions reduction. | S&P Global |

| Baytown Hydrogen Plant Risk | Aug 11, 2025 | Signaled that the $7 billion blue hydrogen facility in Baytown, Texas, faces potential delay or cancellation due to uncertainty over federal tax credit rules. | Energy Capital HTX |

Chart Shows Hydrogen Key to Lowering Net-Zero Costs

The section is a table of low-carbon investments and actions. The chart provides the strategic rationale for a key investment area—hydrogen—by illustrating its importance in reducing the overall cost of achieving net-zero emissions.

(Source: ExxonMobil)

Exxon Mobil 5 New Agreements, from Calpine to Atmos Clear (2025)

Partnerships in 2025 became the primary mechanism for Exxon Mobil to de-risk its CCUS infrastructure build-out and secure a foundational customer base. These collaborations span multiple industrial sectors, indicating a deliberate strategy to create diversified, high-volume carbon capture hubs rather than focusing on a single industry.

- The agreement with Calpine for 2 million metric tons per year is a cornerstone deal, anchoring Exxon Mobil’s services in the large-scale power generation sector.

- In September 2025, the company announced its fifth Louisiana-based CO₂ transport and storage agreement with Atmos Clear, confirming its success in aggregating multiple smaller emitters into a viable network.

- An offtake agreement with Marubeni for low-carbon ammonia, which relies on CCS for its “low-carbon” designation, directly links Exxon Mobil’s capture capabilities to the manufacturing of new energy products.

- The partnership with the NG 3 project adds another 1.2 million metric tons per year of capacity from an industrial source, further strengthening the economic case for its Louisiana pipeline infrastructure.

Carbon Capture Market to Reach $22B by 2032

This section details new partnership agreements. The chart’s forecast of a multi-billion dollar carbon capture market provides the clear commercial justification and long-term context for why ExxonMobil is forming these new agreements.

(Source: maximize market research)

Table: Exxon Mobil 2025 Carbon Capture Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ADNOC | Oct 30, 2025 | Endorsed the ‘Carbon Measures’ global coalition, signaling collaboration on developing a standardized, ledger-based carbon accounting system. | Journal of Petroleum Technology |

| Atmos Clear | Sep 22, 2025 | Selected by Atmos Clear for CO₂ transportation and storage services, marking the fifth customer agreement for Exxon Mobil in Louisiana. | PR Newswire |

| Marubeni | Aug 01, 2025 | Signed a long-term offtake agreement for approximately 250, 000 tonnes of low-carbon ammonia annually, with production dependent on CCS. | Oxford Institute for Energy Studies |

| Calpine Corporation | Apr 23, 2025 | Agreement to transport and store up to 2 million metric tons of CO₂ per year from Calpine’s power facility in Baytown, Texas. | Exxon Mobil Corporate |

Carbon Dioxide Utilization Market to Hit $18.3B

This section is a table of carbon capture partners. This chart, focusing on the ‘Utilization’ (the ‘U’ in CCUS) market, provides complementary context, highlighting a specific market segment that the listed partnerships aim to address.

(Source: Precedence Research)

US Gulf Coast Focus, Exxon Mobil CCS Hub Development

Exxon Mobil’s geographic strategy for carbon capture is heavily concentrated on the U.S. Gulf Coast, a region offering a unique combination of dense industrial emissions, favorable geology for storage, and existing pipeline infrastructure. While activities between 2021 and 2024 involved exploring global opportunities, the focus in 2025 has sharpened decisively on monetizing this specific corridor.

- The region from Houston, Texas, to the Mississippi River Delta in Louisiana is the epicenter of Exxon Mobil’s current CCS commercial activity, with all major 2025 agreements targeting facilities in this area.

- The selection of Baytown, Texas, for the Calpine project and the at-risk blue hydrogen plant leverages Exxon Mobil’s massive existing operational footprint and geological knowledge of the area.

- The string of five customer agreements in Louisiana, including those with Atmos Clear and the NG 3 Project, confirms the state as a parallel strategic hub where the company is aggregating multiple CO₂ streams.

- This geographic concentration is a strategic choice to achieve economies of scale. By building a shared pipeline and storage network, Exxon Mobil aims to lower the per-ton cost of CCS for all participants, creating a more attractive service offering.

ExxonMobil Details Gulf Coast Carbon Capture Hub

This is a direct and perfect match. The section topic is ExxonMobil’s CCS hub development on the US Gulf Coast, and the chart is a map that visually details that exact project and location.

(Source: CarbonCredits.com)

Technology Maturity, Exxon Mobil’s Mix of Pilot and Commercial Scale

Exxon Mobil’s technology strategy employs a two-pronged approach, deploying mature, commercially available capture systems for immediate revenue while simultaneously investing in next-generation technologies to drive down future costs. The period from 2021-2024 saw foundational work on these parallel tracks, while 2025 has brought both large-scale commercial deployment and key milestones for emerging tech.

- The agreements with Calpine, Atmos Clear, and others in 2025 rely on proven, post-combustion capture technologies that are at a high Technology Readiness Level (TRL 8-9) and can be deployed at scale.

- Simultaneously, Exxon Mobil is advancing its partnership with Fuel Cell Energy to pilot a novel carbonate fuel cell technology for carbon capture, with preparations in 2025 for a 2026 demonstration. This technology promises higher efficiency and a different cost structure.

- This dual strategy allows Exxon Mobil to build its commercial business and generate revenue today using established methods, while positioning itself to adopt more cost-effective solutions as they mature, protecting against technological obsolescence.

- The company’s investment in advanced methane detection via satellite and ground sensors is another critical technology play, focused on reducing its own operational emissions, which accounts for 60% of its revised low-carbon spending.

ExxonMobil Carbon Capture Capacity Growth to 2020

This section discusses technology maturity and scale. The chart’s depiction of historical capacity growth provides tangible evidence of the company’s experience and progression in scaling the technology from earlier stages to commercial operations.

(Source: OilNOW – Guyana’s)

SWOT Analysis, Exxon Mobil’s CCS Execution Risks

Exxon Mobil’s 2025 carbon capture initiatives are defined by a calculated commercial push into a nascent market, balanced by significant exposure to policy and regulatory risk. The company is successfully converting its inherent strengths into a tangible business, but its path to profitability is fragile and dependent on external support systems.

- Strengths: The company’s deep geological knowledge and extensive experience in large-scale project management have been validated by its ability to sign major offtake agreements with industrial partners like Calpine and Atmos Clear.

- Weaknesses: An overwhelming dependence on the 45 Q tax credit makes the entire business model vulnerable to policy shifts. The $10 billion spending cut is a direct admission that project economics are not self-sustaining without subsidies.

- Opportunities: By establishing itself as a first-mover in the CCS-as-a-service market, Exxon Mobil is positioning to capture a significant share of a market it projects could reach $4 trillion by 2050.

- Threats: Regulatory uncertainty, evidenced by the risk to the $7 billion Baytown hydrogen project, is the primary threat. A change in policy or unfavorable rule interpretations could stall momentum and lead to further capital reallocation back to fossil fuels.

ExxonMobil Maps Trillion-Dollar Low-Carbon Market Opportunities

This is a direct and perfect match. The section discusses a SWOT analysis, and the chart’s headline explicitly mentions ‘Opportunities,’ directly illustrating the ‘O’ component of the SWOT framework.

(Source: ExxonMobil)

Table: SWOT Analysis for Exxon Mobil’s CCUS Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical expertise in geology and project management; existing infrastructure footprint. | Demonstrated ability to sign multi-million-ton offtake agreements (Calpine, Atmos Clear, NG 3); first-mover advantage in CCS-as-a-service. | The company’s core competencies were validated as a bankable commercial offering, converting expertise into revenue-generating contracts. |

| Weaknesses | High cost of capture technologies; uncertain revenue models for a non-commodity (stored CO₂). | Explicit dependence on 45 Q/45 V tax credits for project viability; capital allocation is highly sensitive to policy shifts. | The weakness was quantified and made explicit; the $10 B spending cut confirmed that current project economics do not stand on their own. |

| Opportunities | Address a large potential market for industrial decarbonization; potential for a “hub and spoke” model. | Securing a diversified customer portfolio across power, ammonia, and other industrial sectors; linking CCS to new products like low-carbon ammonia (Marubeni). | The theoretical opportunity to build a service business was converted into a tangible project pipeline with a multi-sector customer base. |

| Threats | General regulatory uncertainty and political risk; competition from alternative decarbonization pathways. | Specific regulatory delays (45 Q/45 V rules) directly threatening a flagship $7 B project (Baytown); risk of capital flight back to upstream business. | The general threat of policy risk became an acute, project-specific threat, forcing the company to publicly moderate its investment plans. |

ExxonMobil GHG Emissions Trend Downward to 2024

The section is a SWOT analysis table. The chart showing declining GHG emissions serves as a key quantitative data point for the analysis, illustrating a ‘Strength’ (operational progress) or mitigation of a ‘Weakness’ (historical emissions).

(Source: CarbonCredits.com)

Exxon Mobil Baytown FID, Critical CCS Milestone

The single most critical factor for Exxon Mobil’s CCS strategy ahead is the final investment decision (FID) on the Baytown blue hydrogen plant, which will serve as a definitive market signal on the bankability of large-scale, policy-dependent decarbonization projects. If the project is approved, watch for an acceleration of similar integrated hydrogen-CCS projects. If it is canceled, these types of projects could be stalled across the industry.

- The fate of the $7 billion Baytown project is a bellwether for the entire U.S. low-carbon hydrogen and CCS sector. A positive FID would validate that the current incentive structure is sufficient to de-risk major private capital investment.

- Conversely, a cancellation or indefinite delay, as hinted at in August 2025, would confirm that even with enhanced tax credits, regulatory uncertainty remains too high for capital-intensive projects. This could impact related industries, including those developing new applications like hydrogen-powered aviation.

- Watch the pace of new commercial agreements. To reach its stated goal of 30 million metric tons per year of capture capacity by 2030, Exxon Mobil must continue to sign deals at or above the pace seen in 2025.

- Further guidance from the U.S. Treasury on 45 Q and 45 V implementation will be a key trigger. Clarity on rules for measurement, reporting, verification, and credit lifecycle will directly impact the financial models for all of Exxon Mobil’s planned projects.

ExxonMobil Leads in Announced Hydrogen Capacity

This section focuses on the Baytown FID, which is a critical milestone for a major blue hydrogen project. The chart, showing ExxonMobil’s leadership in announced hydrogen capacity, highlights the strategic importance of the Baytown project.

(Source: Enverus)

The questions your competitors are already asking

This report covers one angle of ExxonMobil’s carbon capture business. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the US Gulf Coast CCUS service market?

- ExxonMobil’s activities in Louisiana. Are the partnerships with Calpine and CF Industries progressing from signed agreements to operational CO₂ transport and storage?

- ExxonMobil’s low-carbon investments. Is the Louisiana CCUS hub project on track, considering the company’s broader capital spending cuts?

- What is the outlook for third-party CCUS deployment in the US Gulf Coast power generation and ammonia sectors by 2030?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.