Top 10 SOFC Data Center Players: Bloom’s 2.8 GW Oracle Deal, 9 New Agreements, and $5 B in Financing (2024-2026)

The immense power demand from artificial intelligence and slow grid upgrades are forcing a strategic pivot to on-site generation, with solid oxide fuel cells (SOFCs) emerging as the primary solution for rapid deployment. This shift is validated by multi-gigawatt agreements, such as Bloom Energy’s expanded partnership with Oracle for up to 2.8 GW, and Fuel Cell Energy’s pivot to the data center market, which now constitutes over 80% of its proposal pipeline. The dominant trend for 2025 and beyond is the adoption of fuel cells as a primary “bridge power” source, enabling data center operators to bypass multi-year grid interconnection queues and achieve critical “time to power.” These developments are central to understanding the top fuel cell projects for AI data centers.

1. Bloom Energy and Nebius Partner for 328 MW AI Cloud Power

Company: Bloom Energy & Nebius

Installation Capacity: 328 MW (first project)

Applications: Primary power for AI cloud infrastructure

Source: Nebius and Bloom Energy partner to power AI infrastructure build-out

2. Bloom Energy and Oracle Expand Partnership for 2.8 GW

Company: Bloom Energy & Oracle

Installation Capacity: Up to 2.8 GW

Applications: Primary power for Oracle’s AI data centers

Source: Bloom Energy and Oracle Expand Strategic Partnership…

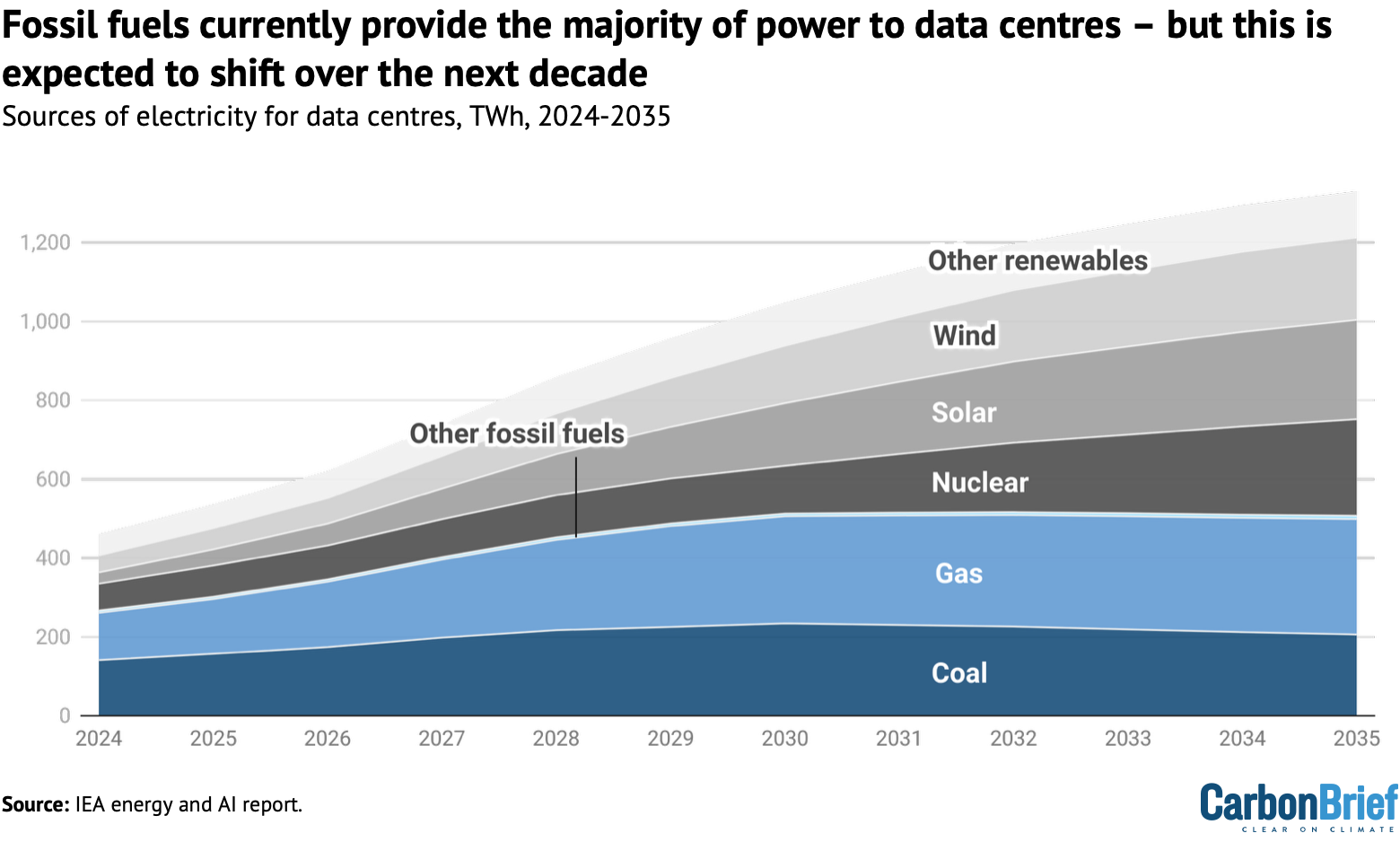

Data Center Power Demand to Triple by 2035

The section highlights an exceptionally large 2.8 GW deal with Oracle. The chart’s aggressive forecast that power demand will triple by 2035 justifies the massive scale of Oracle’s power procurement strategy.

(Source: Carbon Brief)

3. Fuel Cell Energy and SDCL Forge 450 MW Data Center Collaboration

Company: Fuel Cell Energy & SDCL

Installation Capacity: Up to 450 MW

Applications: Deployment of fuel cell systems for data centers

Source: Sustainable Development Capital LLP and Fuel Cell Energy Forge …

Data Center Growth Drives Natural Gas Demand

The section covers a large fuel cell data center deal. The chart connects the macro trend of data center growth directly to increased demand for natural gas, the primary fuel for these fuel cell installations.

(Source: Enverus)

4. Brookfield and Bloom Energy Announce $5 Billion AI Infrastructure Partnership

Company: Bloom Energy & Brookfield

Installation Capacity: Not Specified ($5 Billion financing partnership)

Applications: Financing AI data center infrastructure using Bloom’s fuel cell technology

Source: Brookfield and Bloom Energy Announce $5 Billion Strategic AI …

5. Fuel Cell Energy and Inuverse Target 100 MW Korean Data Center

Company: Fuel Cell Energy & Inuverse

Installation Capacity: 100 MW

Applications: MOU for data center power development in South Korea

Source: Fuel Cell Energy and Inuverse sign MOU…

Stationary Fuel Cell Market to Grow Significantly

This section discusses a Fuel Cell Energy deal in the Korean market. The chart, showing significant growth in the global stationary fuel cell market, contextualizes this international project as part of a broader industry trend.

(Source: Global Market Insights)

6. Fuel Cell Energy Partners to Supply 360 MW to Virginia Data Centers

Company: Fuel Cell Energy, Diversified Energy, & TESIAC

Installation Capacity: Up to 360 MW

Applications: Power three data centers in Virginia leveraging natural gas and coal mine methane

Source: Diversified, Partners to Supply Electricity to Data Centers

7. Bloom Energy Surpasses 100 MW Deployed with Equinix

Company: Bloom Energy & Equinix

Installation Capacity: Over 104 MW

Applications: Primary on-site power for 19 U.S. data centers

Source: Bloom Energy Expands Data Center Power Agreement with Equinix …

Strong YoY Revenue Growth Projected Through 2025

The section marks a deployment milestone with a key customer, Equinix. The chart projecting strong revenue growth illustrates the business momentum and financial success resulting from such ongoing deployments and partnerships.

(Source: Beth Kindig – Medium)

8. AEP and Bloom Energy Sign 1 GW Procurement Agreement

Company: American Electric Power (AEP) & Bloom Energy

Installation Capacity: Up to 1 GW

Applications: “Bridge power” for data centers and other large customers in AEP’s service territory

Source: Bloom Energy Announces Gigawatt Fuel Cell Procurement …

US Power Capacity Additions Soar to New Highs

The section details a 1 GW procurement agreement with US utility AEP. The chart showing soaring US power capacity additions provides the macro context, positioning this deal as a significant contributor to national energy expansion.

(Source: National Center for Energy Analytics)

9. Caterpillar and Microsoft Demonstrate 3 MW Hydrogen Backup Power

Company: Caterpillar & Microsoft

Installation Capacity: 3 MW

Applications: Technology demonstration for long-duration (48+ hours) hydrogen fuel cell backup power

Source: Caterpillar Demonstrates Viability of Using Hydrogen Fuel Cell …

Table: Major Fuel Cell for Data Center Commercial Activity (2024-2026)

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Bloom Energy & Nebius | 328 MW | Primary power for AI cloud | Nebius/Bloom PR |

| Bloom Energy & Oracle | Up to 2.8 GW | Primary power for AI data centers | Bloom/Oracle PR |

| Fuel Cell Energy & SDCL | Up to 450 MW | Data center power collaboration | FCEL/SDCL PR |

| Bloom Energy & Brookfield | $5 Billion Financing | Financing for AI data center power | Bloom/Brookfield PR |

| Fuel Cell Energy & Inuverse | 100 MW | Data center development in Korea | FCEL/Inuverse PR |

| Fuel Cell Energy & Partners | Up to 360 MW | Power for Virginia data centers | Hart Energy |

| Bloom Energy & Equinix | Over 104 MW | Primary power for 19 data centers | Bloom/Equinix PR |

| AEP & Bloom Energy | Up to 1 GW | Utility-procured data center power | Bloom/AEP PR |

| Caterpillar & Microsoft | 3 MW Demo | Hydrogen backup power validation | CAT/Microsoft PR |

Datacenter Power Redundancy Costs Rise With Unit Size

The section describes a demonstration of hydrogen backup power. The chart explains the economic motivation, showing that rising redundancy costs drive the search for alternative backup solutions like hydrogen.

(Source: SemiAnalysis)

Data Center Power, Fuel Cell Energy’s 910 MW Pivot

The pattern of adoption shows a definitive industry shift from using fuel cells for niche backup power to deploying them as primary, baseload energy sources. Data center REIT Equinix is a key example, having already deployed or contracted over 104 MW of SOFC capacity from Bloom Energy for primary power across its portfolio. This trend is expanding beyond data center operators to include utilities themselves. American Electric Power’s (AEP) agreement to procure up to 1 GW of fuel cells for its data center customers is a landmark move, establishing a new model where utilities act as facilitators for on-site power to retain large industrial loads. The strategic pivot by Fuel Cell Energy, underscored by recent agreements totaling over 910 MW, confirms this is now an industry-wide movement driven by the urgent need for scalable and rapidly deployable power.

Fuel Cell Market to Reach $18B by 2030

This summary section highlights Fuel Cell Energy’s strategic 910 MW pivot. The chart quantifies the total addressable market, showing the $18 billion opportunity that FCE is targeting with this significant shift.

(Source: MarketsandMarkets)

North America Leadership, AEP’s 1 GW Bloom Energy Deal

Geographically, North America is the undisputed leader in adopting fuel cells for AI data centers. The intense concentration of hyperscale development and severe grid congestion in U.S. data center alleys, particularly in states like Virginia, create the ideal conditions for this trend. The 360 MW project targeted by Fuel Cell Energy and its partners in Virginia is a direct response to these regional pressures. The proactive strategy from major U.S. utilities like AEP, which serves a large data center cluster in Ohio, further solidifies North American dominance. However, nascent signs of global replication are appearing. Fuel Cell Energy’s MOU for a 100 MW project in South Korea suggests that the model for using fuel cells to bypass grid constraints is starting to gain traction in other power-constrained, high-growth digital economies.

Data Center Power Ecosystem Players Identified

This analysis section frames the AEP deal as a mark of leadership for Bloom Energy. The chart identifying key ecosystem players allows for the visualization of Bloom’s competitive positioning and leadership role.

(Source: MarketsandMarkets)

Bloom Energy’s 2 GW SOFC Scale-Up (2024-2026)

The announced projects reveal a clear hierarchy in technology maturity and commercial scale. Bloom Energy’s SOFC technology stands out as the most mature and scalable solution, capable of supporting multi-gigawatt deals with hyperscalers like Oracle. The company’s ability to execute is backed by an existing 1 GW of annual manufacturing capacity, which is on track to expand to 2 GW. In contrast, hydrogen-based PEM fuel cells for stationary power remain in the advanced validation stage, as shown by the successful but smaller-scale 3 MW backup power demonstration by Caterpillar and Microsoft. Fuel Cell Energy is aggressively moving to close the gap on the leader, announcing plans for a five-fold manufacturing expansion to 500 MW annually and launching a standardized, pre-packaged 12.5 MW power block specifically engineered for faster data center deployment.

Data Center Power Market to Exceed $50B by 2030

The section focuses on Bloom Energy’s 2 GW production scale-up. The chart, showing the data center power market exceeding $50 billion, provides the rationale by demonstrating the massive market size that justifies such a large investment.

(Source: MarketsandMarkets)

2.8 GW, Oracle’s SOFC Strategy Signals Broader Hyperscaler Shift

The single most critical strategic development to watch is other hyperscale cloud providers following Oracle’s lead to secure gigawatts of dedicated, off-grid power, effectively making on-site fuel cells a standard component for any major AI infrastructure build-out. This is no longer a niche or experimental play; it is becoming a core part of the deployment strategy to de-risk AI capacity expansion from grid availability.

- The April 2026 expansion of the Oracle-Bloom Energy partnership to 2.8 GW has established a new benchmark for the scale of behind-the-meter power procurement in the data center industry.

- The partnership between AI cloud provider Nebius and Bloom Energy, announced in May 2026 for an initial 328 MW project, demonstrates that this strategy is being adopted by a broader range of AI-focused companies beyond the largest U.S. hyperscalers.

- Fuel Cell Energy’s disclosure in March 2026 that data centers now drive 80% of its new business proposals confirms that market-wide demand has fundamentally and rapidly shifted toward this model.

- The $5 billion strategic financing partnership between Brookfield and Bloom Energy in October 2025 provides a crucial, repeatable financial template for funding these capital-intensive projects, removing a key barrier to widespread adoption.

Data Center Power Market Pivots to New Technologies

The section analyzes the Oracle deal as a signal of a broader hyperscaler shift. The chart’s headline perfectly encapsulates this central argument, visually representing the market’s pivot to new power technologies.

(Source: MarketsandMarkets)

The questions your competitors are already asking

This report covers one angle of the fuel cell market’s pivot to power AI data centers. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the fuel cell data center market?

- What is the outlook for SOFC deployment in the AI data center sector by 2026?

- How do solid oxide fuel cells (SOFCs) compare to natural gas generators for AI data center bridge power?

- Which data center operators, besides Oracle and Nebius, are adopting on-site fuel cell power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.