PEM Fuel Cell Military Procurement, 450 SFC Energy Systems for India, 2 TKMS Submarines for Norway (2021 to 2026)

Military Fuel Cell Adoption, GM Defense & SFC Energy Secure 3 Major Procurement Deals

Military adoption of fuel cells has transitioned from niche development projects between 2021 and 2024 to strategic procurement contracts in 2025-2026, driven by confirmed operational advantages in endurance and stealth. This shift marks the technology’s move from a promising alternative to a fielded strategic enabler for ground, air, and sea domains.

- In the 2021 to 2024 period, activity was characterized by R&D contracts and prototypes designed to prove operational concepts. Examples include Advent Technologies securing a $2.2 million U.S. Department of Defense contract for its “Honey Badger” portable fuel cell systems and the French Armed Forces unveiling their RAPACE hydrogen drone, signaling national investment in building sovereign capabilities.

- The period from 2025 to today demonstrates a clear shift to procurement and fleet-level integration, confirming the technology’s value. Norway signed a contract for two additional Thyssen Krupp Marine Systems (TKMS) Type 212 CD submarines with fuel cell Air-Independent Propulsion (AIP), and the Indian Defence Forces placed a major order for 450 portable methanol fuel cell systems from SFC Energy for high-altitude operations.

- Application diversity has expanded significantly, validating fuel cells as a platform technology rather than a point solution. Deployments now include not only UAVs (Intelligent Energy, Heven Drones) but also AIP submarines (TKMS, Hanwha Ocean), unmanned ground drones (First Hydrogen), and resilient stationary power for forward operating bases being developed by companies like Ceres Power.

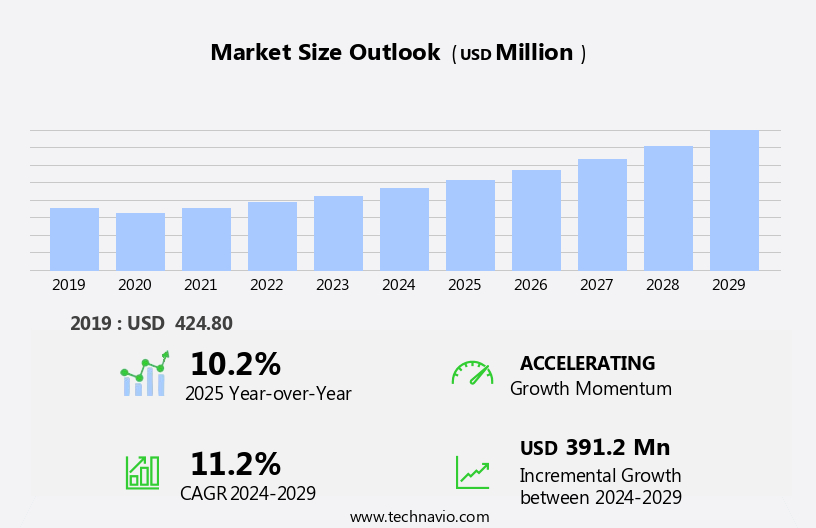

Military UAV Fuel Cell Market Growth

This chart quantifies the military adoption trend discussed in the section, showing significant market growth for fuel cells in the UAV (air) domain, which is mentioned as a key example.

(Source: Technavio)

$79 M in Funding, Mach Industries & Do D Investment in Hydrogen Platforms

Investment in military fuel cell technology has matured from foundational government R&D grants to include significant venture capital and large-scale defense contracts, signaling commercial viability and strategic urgency among defense planners. This funding progression confirms that the technology has successfully crossed the initial valley of death and is now seen as a bankable asset for both private investors and government procurers.

- The 2021-2024 timeframe was defined by government-led, early-stage funding programs designed to foster innovation and de-risk the technology for defense applications. The U.S. Army’s Direct to Phase II SBIR program, announced in March 2023, offered up to $1.8 million per company to develop clean hydrogen technologies, creating a pipeline of potential suppliers.

- Targeted production contracts began bridging the gap between R&D and fielding. In September 2023, Advent Technologies secured a $2.2 million Do D award specifically to advance higher production volumes of its wearable fuel cell systems, a clear signal of intent to move from prototype to at-scale deployment.

- A critical validation point was the entry of tier-one venture capital, which acts as a powerful market signal. In October 2023, defense startup Mach Industries, which is developing hydrogen-powered platforms, closed a $79 million Series A funding round at a $335 million valuation with participation from Sequoia Capital.

Table: Military Fuel Cell Investment Milestones

| Entity / Program | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Mach Industries | Oct 2023 | Closed a $79 million Series A funding round to develop hydrogen-powered platforms and munitions. The investment from prominent VCs like Sequoia signals strong private market confidence in the defense-tech application of hydrogen. | Tech Crunch |

| Advent Technologies | Sep 2023 | Secured a $2.2 million contract with the U.S. Do D to scale production of its “Honey Badger” portable HT-PEM fuel cell systems. The purpose is to move from prototype to higher-volume manufacturing for soldier-worn power. | Advent Technologies |

| U.S. Army | Mar 2023 | Announced up to $1.8 million per company via a Direct to Phase II SBIR program for clean hydrogen fuel technologies. This grant program is designed to accelerate innovation and broaden the industrial base for military hydrogen applications. | U.S. Army |

Rheinmetall 1 Strategic Partnership & GM Defense 2 Do D Agreements (2023 to 2026)

Strategic partnerships have evolved from technology-specific collaborations to ecosystem-building alliances, pairing fuel cell specialists with large defense integrators and energy providers. This trend indicates the market is maturing beyond point products and is now focused on creating complete, deployable “power-on-demand” solutions that address the entire hydrogen value chain from production to consumption.

- Between 2021 and 2024, partnerships were primarily focused on integrating fuel cell technology into specific platforms. For example, GM Defense partnered with the United Arab Emirates to explore hydrogen-based vehicle technologies, and Intelligent Energy worked directly with the UK Ministry of Defence to extend drone flight times.

- The 2025-2026 period shows a strategic shift toward solving the hydrogen logistics problem, which is the primary barrier to widespread adoption. The April 2026 partnership between German defense prime Rheinmetall AG and PEM electrolyzer manufacturer ITM Power aims to develop decentralized green hydrogen and e-fuel production networks specifically for defense applications.

- The ecosystem now extends to civil infrastructure players whose technology is directly applicable to military needs. The March 2026 partnership between Ceres Power and utility owner Centrica to deploy SOFCs for high-demand users provides a commercial model for powering energy-intensive military bases and command centers.

Table: Key Military Fuel Cell Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Rheinmetall AG & ITM Power | Apr 2026 | Strategic collaboration to develop decentralized green hydrogen and e-fuel production facilities for defense. This partnership aims to solve the hydrogen supply chain challenge for military operations. | Fuel Cells Works |

| Ceres Power & Centrica | Mar 2026 | Partnership to deploy SOFC technology to meet multi-gigawatt demand from high-consumption users like data centers. This has direct applicability for powering resilient microgrids at military installations. | Reuters |

| GM Defense & Do D | Jun 2023 | Contracted to prototype the Scalable Tactical Edge Power (STEEP) energy storage system for the Do D. The system is designed to integrate with hydrogen generators to create intelligent tactical microgrids. | GM Defense |

| SFC Energy & Indian Defence Forces | Mar 2023 | Received a major order to supply 450 portable methanol fuel cell systems. The partnership provides power for soldiers in remote and high-altitude environments, reducing reliance on conventional batteries. | Fuel Cells Works |

Europe vs. Asia, Thyssen Krupp and Hanwha Ocean Lead Submarine AIP Race

While North America leads in R&D funding and venture-backed startups for fuel cell applications, Europe and Asia are dominating large-scale procurement and deployment, particularly in the high-value naval sector. This geographic divergence highlights a global split where the U.S. funds innovation while its allies and competitors are the first to field the resulting capabilities in operational hardware.

- North America: The U.S. and Canada are epicenters of fuel cell R&D and early-stage commercialization, driven by Do D programs like the ONR’s H-Ta RP hydrogen generator and GM Defense‘s STEEP microgrid project. Canada represents a major procurement opportunity with its pending $20 billion Canadian Patrol Submarine Project (CPSP), attracting bids from global suppliers.

- Europe: Germany, through Thyssen Krupp Marine Systems (TKMS), is the undisputed leader in deploying hydrogen AIP submarines, setting the global standard with its Type 212 class and securing follow-on orders from allies like Norway in February 2026. The UK shows strength in UAV fuel cells through Intelligent Energy and is developing large autonomous submarines like the Herne with hydrogen propulsion.

- Asia: South Korea and India are rapidly emerging as key players. South Korea’s Hanwha Ocean and Hyundai are aggressively marketing their KSS-III AIP submarine for export, while its Agency for Defense Development (ADD) has developed its own methanol-reforming technology. India is both a major procurer, with its large order for SFC Energy portable units, and a developer, with its DRDO pursuing an indigenous AIP system for delivery by 2026.

PEM vs. SOFC Maturity, Intelligent Energy and Ceres Power Target Different Segments

Proton Exchange Membrane (PEM) fuel cells have achieved commercial maturity for military mobility applications that require high power density and rapid response, while Solid Oxide Fuel Cells (SOFC) are being commercialized for stationary power where high efficiency and fuel flexibility are the primary requirements. This bifurcation of the technology landscape shows the market is effectively matching the right type of fuel cell to the specific operational need.

Solid Oxide Fuel Cell (SOFC) Market

As the section directly compares PEM and SOFC technologies, this chart provides specific market forecast data for the SOFC segment, illustrating its commercial growth and validating a key part of the text.

(Source: MarketsandMarkets)

- PEM Fuel Cells are now the default technology for mobile defense applications. They are being fielded in UAVs (Intelligent Energy), man-portable power systems (Advent Technologies, SFC Energy), and submarine AIP systems (TKMS). The technology is considered field-ready, with challenges shifting from technical performance to manufacturing scale, cost reduction, and hydrogen logistics.

- Solid Oxide Fuel Cells (SOFC) are gaining traction for stationary and auxiliary power, where their superior efficiency and ability to run on various fuels (including hydrogen, natural gas, or JP-8 with reforming) is a significant advantage. The Ceres Power partnership with Centrica to power data centers provides a direct commercial analogue for providing resilient, efficient power to forward operating bases.

- Hydrogen Generation & Storage remains the least mature part of the military fuel cell ecosystem and represents the most significant adoption risk. The focus is shifting to on-demand, on-site generation to eliminate vulnerable liquid fuel convoys. The U.S. Navy’s H-Ta RP project and Rheinmetall‘s partnership with ITM Power are critical initiatives aimed at solving this logistical challenge, which is the final barrier to widespread fuel cell deployment.

1 SWOT Analysis, GM Defense & Thyssen Krupp Strategic Positions

Military fuel cell adoption is driven by strong operational advantages in stealth and endurance, creating new tactical possibilities. However, the technology’s growth faces significant threats from the logistical complexities of hydrogen supply and persistent competition from incremental improvements in advanced battery technology.

- Strengths: The primary strength is the confirmed ability to provide a tactical advantage through stealth (low acoustic/thermal signature) and extended mission endurance.

- Weaknesses: The main weakness remains the hydrogen supply chain, which is complex and requires new infrastructure for production, storage, and distribution at the tactical edge.

- Opportunities: The opportunity lies in creating energy-independent forces and becoming the default power source for the military’s broad electrification push across all domains.

- Threats: The primary threat comes from rapid advancements in alternative energy storage, particularly solid-state batteries, which could eventually narrow the energy density gap.

Table: SWOT Analysis for Military Fuel Cell Adoption (2021-2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated extended endurance for UAVs in prototypes. Low acoustic signature was a theoretical benefit for submarines. | Endurance and stealth are now specified requirements in major procurement contracts, such as the TKMS Type 212 CD submarines and UAVs capable of 13+ hour flights. | The operational advantages have been validated and are now driving billion-dollar acquisition programs, moving from theory to practice. |

| Weaknesses | Hydrogen logistics were identified as a major barrier. High upfront costs of fuel cell systems compared to diesel generators. | Hydrogen logistics remain a key challenge, but major defense primes like Rheinmetall are now forming partnerships (with ITM Power) to build dedicated military hydrogen networks. | The weakness is being actively addressed through strategic partnerships, indicating the problem is seen as solvable and the benefits of fuel cells are worth the investment in solving it. |

| Opportunities | The concept of “silent watch” for vehicles and man-portable power for soldiers were key opportunity areas. AIP for submarines was an emerging niche. | The opportunity has expanded to full electrification of military bases (Ceres Power) and ground fleets (GM Defense). AIP is now a standard requirement for new conventional submarines. | The scope of opportunity has broadened from niche applications to becoming a foundational technology for achieving energy resilience and independence across the entire military. |

| Threats | Competition from improving lithium-ion battery technology. Geopolitical risks associated with platinum group metal (PGM) supply chains for PEM catalysts. | Advanced battery technology remains a competitor, but the energy density gap for long-endurance missions is still significant. PGM supply risk persists. | The threat from batteries has not materialized for long-endurance missions, validating the unique role of fuel cells. The market is accepting the PGM risk in exchange for the performance gains. |

Future Scenarios, Rheinmetall & ITM Power On-Site Hydrogen Generation

The critical variable for 2026 and beyond is the successful deployment of tactical, on-site hydrogen generation, which will determine whether fuel cells remain a niche capability for specialized units or become the backbone of mainstream military energy infrastructure.

Hydrogen Fuel Cell Powertrain Explained

This diagram illustrates the core technology whose future is debated in the section, providing essential technical context for the scenario of on-site hydrogen generation.

(Source: ScienceDirect.com)

- If this happens: If partnerships like Rheinmetall–ITM Power successfully pilot and scale deployable PEM electrolyzer networks capable of producing hydrogen from available water sources in the field…

- Watch this: …watch for a rapid increase in procurement contracts for fuel-cell powered ground vehicles and a fundamental shift in military construction budgets toward building tactical microgrids instead of fortified fuel depots.

- This could be happening: This would signal the final transition from simply using hydrogen-powered equipment to building entire hydrogen-based energy ecosystems at the tactical edge, a move that would fundamentally alter military logistics, reduce casualties associated with fuel convoys, and deliver true energy independence. The operational success of the U.S. Navy’s H-Ta RP prototype will be a leading indicator of this shift.

The questions your competitors are already asking

This report covers one angle of fuel cell deployment across global armed forces. The questions that matter most depend on your work.

- Which companies are gaining ground in the military fuel cell market, from SFC Energy in portable power to TKMS in submarine AIP?

- What is the outlook for fuel cell AIP adoption in non-nuclear submarine fleets by 2030?

- How do PEM fuel cells, like Advent’s ‘Honey Badger’ system, compare to direct methanol fuel cells (DMFCs) for soldier-portable applications?

- Which armed forces are actively testing or procuring fuel cell UAVs for reconnaissance roles, following the French RAPACE program?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.