Advanced Reactor Do D Programs, 8 DIU Contractors, 9 Army Bases, and 2028 Deployment Target (2025 to 2026)

The U.S. Department of Defense (Do D) is executing a deliberate industrial strategy to create a commercial market for advanced nuclear microreactors by acting as a foundational first customer. Through programs like the Army’s Project Janus and specific Air Force pilot projects, the Do D is establishing bankable, long-term offtake agreements that de-risk the technology for private developers and investors. This military-led demand signal is the most significant catalyst for the sector, designed to solve the “first-of-a-kind” cost and regulatory hurdles that have historically stifled nuclear innovation. The success of these initial military deployments between 2025 and 2030 is intended to serve as the blueprint for wider commercial adoption, particularly for powering energy-intensive data centers and remote industrial operations.

Industry Adoption Shifts from Studies to 9 Do D Microreactor Deployment Contracts

The market for advanced microreactors has pivoted from early-stage design studies before 2025 to concrete deployment contracts and site-specific projects driven by the Do D’s demand for energy resilience. This shift is marked by firm timelines, named commercial partners, and a focus on operationalizing reactors on domestic military bases by 2030, moving the technology from the theoretical to the practical.

- Prior to 2025, industry activity was dominated by vendor-led development and efforts to engage with the Nuclear Regulatory Commission (NRC). The Do D’s involvement was largely in the form of research projects and studies, such as assessing the feasibility of mobile reactors.

- Beginning in 2025, this changed with the formal launch of procurement programs. The Army’s Project Janus selected nine domestic bases for microreactor deployment by 2030, and the Air Force selected Radiant to deliver its Kaleidos reactor to a base by 2028, creating the first firm, large-scale demand signal.

- The adoption model is primarily based on a contractor-owned, contractor-operated framework where the military signs long-term Power Purchase Agreements (PPAs). This transfers the capital and construction risk to developers like Oklo, Radiant, and Westinghouse, making the projects financeable.

- Applications are now clearly bifurcated between stationary power for base resilience (Janus) and transportable power for forward operations and disaster relief (Project Pele). This validates two distinct commercial use cases that can be expanded beyond defense.

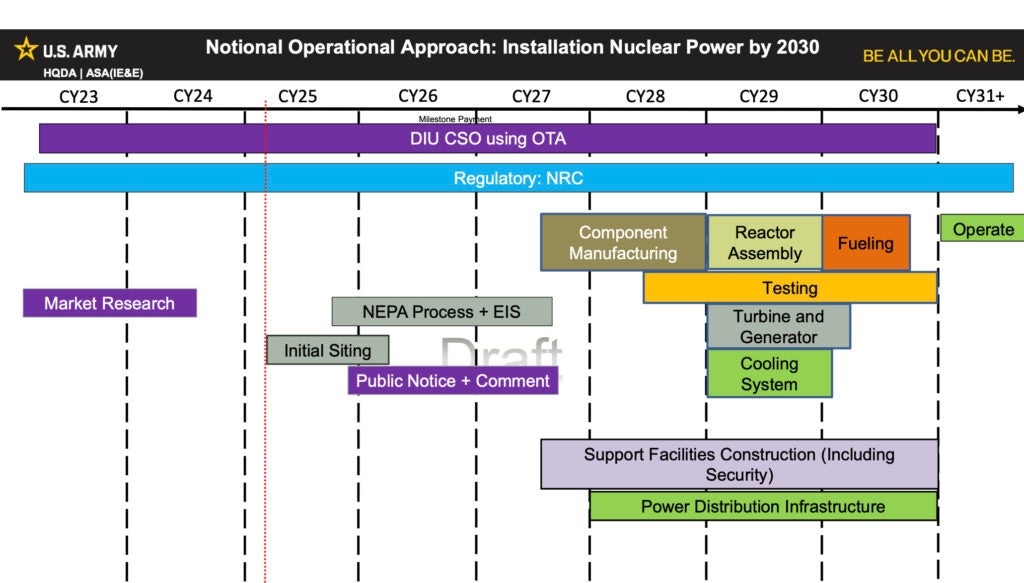

US Army Microreactor Deployment Timeline to 2030

This section discusses the shift to concrete deployment contracts with firm timelines targeting 2030. The Gantt chart directly illustrates this U.S. Army deployment timeline, showing the planned phases through 2030.

(Source: POWER Magazine)

$6.8 B Market Forecast, Do D Demand Underwrites Microreactor Commercialization

The Do D’s commitment to purchase power from multiple first-of-a-kind microreactors provides the revenue certainty needed to underwrite the market’s growth, with forecasts now projecting a surge from under $1 billion in 2025 to over $6.8 billion by 2034. This government-anchored demand is the critical factor attracting private capital and justifying investment in the supporting fuel and manufacturing supply chains.

- The nuclear microreactor market, valued at approximately $850 million in 2025, is projected to reach $6.8 billion by 2034, implying a compound annual growth rate of 26%. This growth is almost entirely predicated on the success of these initial Do D projects.

- In contrast, the broader Small Modular Reactor (SMR) and microreactor market was forecast by Grand View Research in early 2026 to grow more slowly, at a 6.8% CAGR. The accelerated growth in the microreactor-specific forecast reflects the direct impact of the Do D’s procurement programs.

- The PPA model is the key financial mechanism, providing a bankable revenue stream that mitigates the high financial risk of FOAK nuclear projects. This was a primary barrier that stalled projects prior to 2024.

- This strategy is intended to drive down costs through scale. The goal is to reduce the Levelized Cost of Electricity (LCOE) from an initial $150/MWh for a first unit to around $60/MWh for subsequent “nth-of-a-kind” reactors, making them competitive for commercial markets like data centers which have immense power needs, as seen in projects from firms like Bloom Energy.

Table: Nuclear Microreactor & SMR Market Projections

| Forecast Provider | Market Segment | 2025 Size ($B) | 2034 Forecast ($B) | Implied CAGR (%) | Source |

|---|---|---|---|---|---|

| PRNewswire / Cision | Nuclear Microreactor | $0.85 B | $6.8 B | 26.0% | PRNewswire |

| Market Intelo | Nuclear Microreactor & SMR | $4.8 B | $26.4 B | 19.3% | Market Intelo |

| Grand View Research | Small Modular Reactor (SMR) | $6.54 B | $10.69 B (by 2033) | 6.8% | Grand View Research |

Do D 8 Commercial Partners for Project Janus, Oklo, and Radiant (2025 to 2026)

The Department of Defense has structured its microreactor initiatives around a portfolio of commercial partnerships, selecting a diverse group of technology developers to ensure multiple pathways to success and foster a competitive industrial base. These partnerships, formalized since 2025, are the primary vehicle for executing the military’s energy resilience strategy.

- The most expansive partnership is the U.S. Army’s Project Janus, managed with the Defense Innovation Unit (DIU). In April 2025, the DIU selected eight companies as eligible developers: Westinghouse, X-energy, Ultra Safe Nuclear Corp. (USNC), Oklo, Radiant, NANO Nuclear Energy, General Atomics, and BWX Technologies (BWXT).

- The U.S. Air Force solidified its own partnerships, selecting Radiant in August 2025 for a project to deliver a 1 MWe microreactor to a U.S. military base by 2028. It also reaffirmed its selection of Oklo in June 2025 to provide a 5 MWe reactor for Eielson Air Force Base in Alaska.

- The Do D’s Strategic Capabilities Office (SCO) is leading Project Pele, a partnership focused on a transportable reactor. BWXT is the prime contractor and achieved a major milestone in December 2025 by delivering the first batch of advanced TRISO fuel for the prototype.

Table: Key Do D Microreactor Partnerships and Programs

| Program / Partnership | Lead Agency | Key Contractor(s) | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|---|---|

| USAF Microreactor Project | U.S. Air Force | Radiant | Aug 2025 | Agreement signed for Radiant to deliver its 1 MWe Kaleidos reactor to a USAF base by 2028, serving as a pathfinder for fixed installation power. | Neutron Bytes |

| Janus Program | U.S. Army / DIU | Multiple (8 selected) | Nov 2025 | Solicitation opened for commercial microreactors at nine selected domestic bases, aiming for deployment by 2030 to ensure 100% power for critical loads. | Hogan Lovells |

| Air Force Pilot (Eielson) | U.S. Air Force | Oklo | Jun 2025 | Oklo was retapped to provide a 5 MWe liquid metal-cooled reactor at Eielson AFB, Alaska, to provide clean power for a critical national security installation. | POWER Magazine |

| Project Pele | Do D Strategic Capabilities Office | BWX Technologies (BWXT) | Dec 2025 | BWXT delivered the first batch of TRISO microreactor fuel, a key milestone for demonstrating a transportable reactor for forward operating bases. | POWER Magazine |

US-Centric Deployment, Do D Selects Alaska and 9 Domestic Bases for Microreactors

The geographic focus of microreactor deployment has decisively centered on the United States, driven by the Do D’s strategy to fortify domestic military installations. While development activity before 2024 was geographically diffuse, events in 2025 have identified specific U.S. locations as the first real-world sites for these advanced energy systems.

- Prior to 2025, discussions of microreactor deployment were often generic, targeting “remote communities” or “industrial sites” without specific locations.

- In July 2025, Eielson Air Force Base in Alaska was confirmed as a primary site for the Air Force’s microreactor program, leveraging the technology for energy resilience in a strategic, arctic environment.

- In November 2025, the Army announced it had selected nine domestic bases for its Project Janus program. While the specific bases were not publicly named, the action concentrates deployment activity within the continental U.S. to address grid vulnerabilities.

- The selection of Idaho National Laboratory (INL) as the site for the MARVEL test bed in July 2025, involving companies like Radiant and Westinghouse, further cements the U.S. Intermountain West as a central hub for technology validation.

Technology Maturity Advances to Demonstration with Do D’s Project Pele and Janus

Do D programs are pushing microreactor technologies from the design and component-testing phase (TRL 5-6) into the operational demonstration phase (TRL 7-8). Milestones achieved in 2025, particularly the delivery of specialized fuel and the final selection of vendors for pilot projects, confirm that the technology is moving beyond simulations and into hardware-based validation.

- Before 2025, a key risk was the availability of High-Assay Low-Enriched Uranium (HALEU) fuel, which most advanced designs require. The successful delivery of the first TRISO fuel by BWXT for Project Pele in December 2025 was a critical milestone, proving the domestic supply chain can produce fuel for military needs.

- While companies had mature designs on paper, the Do D programs are forcing the first real-world integration and operational tests. The selection of Radiant’s helium-cooled design and Oklo’s liquid-metal reactor for Air Force projects provides validation for two different technological pathways.

- The creation of the MARVEL microreactor test bed at Idaho National Laboratory, announced in July 2025, provides a non-NRC regulated pathway for vendors like Westinghouse and Radiant to test their technology and collect operational data, accelerating the path to commercial readiness.

SWOT Analysis of the Do D’s Advanced Reactor Commercialization Strategy

The Do D’s strategy to act as an anchor customer for microreactors creates powerful strengths and opportunities, but it does not eliminate underlying weaknesses in the industrial base or external threats that could delay deployment. The primary change since 2024 is the mitigation of initial financial risk, shifting the focus to execution risk.

- Strengths: The strategy provides a clear, bankable demand signal and a non-commercial customer willing to absorb first-of-a-kind technology risk.

- Weaknesses: The domestic HALEU fuel supply chain is still nascent and dependent on government support, and the specialized nuclear workforce requires significant expansion.

- Opportunities: Successful Do D deployments will serve as a powerful case study for commercial markets, especially for powering AI data centers, and could position U.S. firms as global leaders in advanced nuclear exports.

- Threats: Even with streamlined DOE oversight, regulatory processes can cause delays. Potential cost overruns on these initial projects could diminish political support, and negative public perception remains a persistent challenge for any new nuclear project.

Table: SWOT Analysis of Do D Microreactor Strategy

| SWOT Category | State Before 2025 | State in 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | National security identified as a potential driver for nuclear; reliance on vulnerable grid was a known problem. | Formal programs (Janus, Pele) with timelines and budgets are established. PPA model is codified in solicitations. | The Do D’s strategic need for energy resilience was converted into a concrete, bankable procurement strategy. |

| Weaknesses | Developers faced immense financial risk with no clear first customer. HALEU fuel supply chain was a concept. | Financial risk is shifted to the government via PPAs, but supply chain and workforce bottlenecks are now the primary constraints. | The core challenge shifted from “Will anyone buy it?” to “Can we build it on time and on budget?”. |

| Opportunities | Potential for commercial spillover into markets like data centers was theoretical. | Soaring energy demand from AI has made the commercial case for microreactors urgent and explicit. | The convergence of military need and a massive commercial demand driver (AI/data centers) created a much larger total addressable market. |

| Threats | Regulatory uncertainty with the NRC was seen as a major barrier to any new nuclear project. | Use of DOE/DOW authority for military projects creates a parallel path, but NRC reform is still needed for mass commercialization. | The strategy partially bypasses the primary regulatory threat for initial deployments but does not solve it for the broader commercial market. |

Scenario Modelling: Watch Project Janus Progress for Commercial Data Center Signals

The most critical strategic variable for the advanced nuclear sector over the next two years is the tangible, on-schedule progress of the first military microreactor deployments. If the Do D, with partners like Radiant and the eventual winners of the Project Janus contracts, can meet early construction and licensing milestones, it will send a powerful signal to the commercial market, particularly data center operators, that the technology is ready for private-sector investment.

- If progress remains on track: Watch for the Army to announce the first specific base and commercial partner for a Project Janus reactor in late 2026 or early 2027. This would likely trigger a new wave of private investment into the selected developer and its supply chain partners. Also, expect to see the first firm commercial microreactor orders from a data center developer within 12 months of that announcement.

- If progress stalls: Watch for reports of delays in HALEU fuel delivery or unexpected issues at the MARVEL test bed. Any significant delay past the 2028 target for the first USAF reactor would be a negative signal, likely causing private investors and commercial customers to pause and re-evaluate the technology’s readiness.

- What could be happening: Behind the scenes, developers are likely using the validation from their Do D partnerships to finalize their manufacturing plans and secure long-lead-time components. The companies that can demonstrate a clear path from military deployment to a standardized, factory-producible model will be best positioned to capture the coming commercial demand.

The questions your competitors are already asking

This report covers one angle of the DoD’s industrial strategy to commercialize advanced microreactors. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the DoD microreactor market?

- What is the outlook for microreactor deployment on US military bases by 2030?

- Is the Army’s Project Janus on track for its 2028 deployment target?

- Which data center operators are adopting microreactor power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.