Top 10 SOFC Manufacturers: Bloom’s $20 B Backlog, Oracle 2.8 GW Deal & Data Center Demand (2024-2026)

The Solid Oxide Fuel Cell (SOFC) market is undergoing a rapid and decisive transition from pilot-scale projects to commercially robust, gigawatt-scale deployments. This shift is overwhelmingly driven by the insatiable power demands of the artificial intelligence and data center sectors. Analysis of commercial activity from 2024 to 2026 reveals a clear market consolidation around manufacturers that have achieved significant production scale and secured multi-billion-dollar order backlogs. Bloom Energy has cemented its leadership with a staggering $20 billion total backlog and projected 2026 revenue of approximately $3.6 billion. The dominant theme for 2025 is the bifurcation of the market between vertically integrated system providers meeting massive data center demand and capital-light technology licensors whose partners are now entering mass production.

The competitive landscape is intensifying, as highlighted by Fuel Cell Energy’s strategic exit from the SOFC market after taking a $64.5 million impairment charge. This move underscores the high barriers to entry and the immense capital required to compete at scale. Meanwhile, Ceres Power‘s licensing model is gaining validation as its partner, Doosan Fuel Cell, initiated mass production in July 2025, marking a crucial shift toward recurring royalty revenues. Below is a breakdown of the key commercial activities signaling this market maturation.

Key Commercial Activities (2024-2026)

The following activities demonstrate the transition from pilot projects to significant, recurring commercial revenue across the SOFC sector.

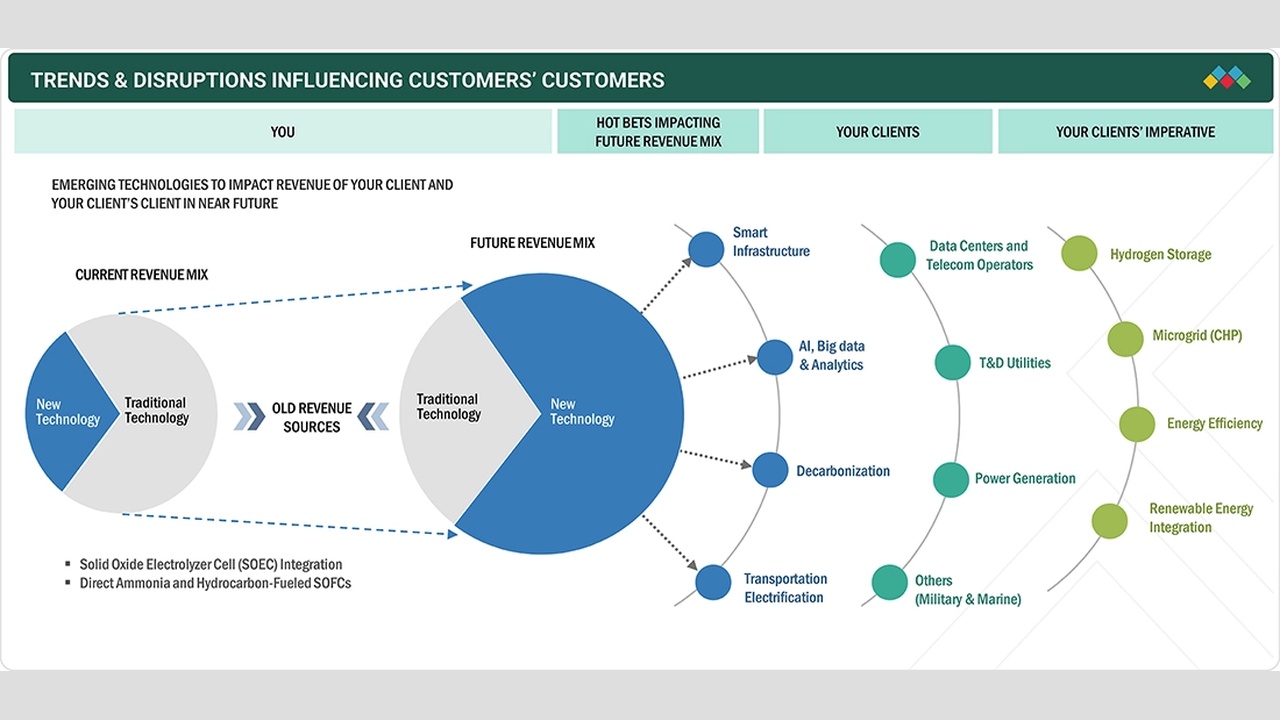

SOFC & SOEC Tech Shift Drives Revenue

This infographic provides a high-level overview of the revenue shift driven by SOFC and SOEC technologies, perfectly introducing the commercial activities detailed in the following sections.

(Source: MarketsandMarkets)

1. Bloom Energy Secures Landmark Data Center Deals

Company: Bloom Energy

Activity: Expanded a strategic partnership with Oracle to deploy up to 2.8 GW of capacity and raised its 2026 revenue growth guidance to approximately 80% year-over-year.

Application: Providing primary, on-site power for AI data centers.

Source: Bloom Energy, Oracle expand deal to 2.8 GW

2. Ceres Power Monetizes Licensing Model

Company: Ceres Power

Activity: Achieved approximately £45 million in contracted revenue for 2026 as its manufacturing partners begin commercial production.

Application: Technology licensing for SOFC stacks used in stationary power and maritime systems.

Source: Final results for the year ended 31 December 2025

3. Doosan Fuel Cell Initiates Commercial Production

Company: Doosan Fuel Cell

Activity: Began mass production of SOFC stacks in July 2025 and secured its first commercial order for 9 MW in December 2025.

Application: Manufacturing SOFC systems under license from Ceres Power for data centers and maritime applications.

Source: Mass production of Ceres Power fuel cell technology begins in Korea

4. Sunfire Refocuses on Electrolysis

Company: Sunfire Gmb H

Activity: Spun off its fuel cell business in 2024 to concentrate on its Solid Oxide Electrolyzer Cell (SOEC) business, despite holding a combined backlog of over 800 MW.

Application: Strategic pivot toward the green hydrogen production market.

Source: Sunfire Year in Review 2024

5. Fuel Cell Energy Exits the SOFC Market

Company: Fuel Cell Energy

Activity: Abandoned its SOFC platform in June 2025, resulting in a $64.5 million impairment charge.

Application: Restructuring to focus on its core carbonate fuel cell and electrolysis technologies.

Source: Fuel Cell Energy: Poor Prospects Result In Further Restructuring

Top SOFC Manufacturers by Projected 2026 Revenue

| Rank | Company | Projected 2026 Revenue | End-of-Year 2025 Backlog | Key Commercial Highlights |

|---|---|---|---|---|

| 1 | Bloom Energy | Approx. $3.6 B | $20 Billion (total), $6 Billion (SOFC) | Product sales, installations, and long-term service agreements for the AI data center market. |

| 2 | Ceres Power | ~£45 Million (contracted) | Not reported as backlog | Technology licensing and royalty model; recurring revenue from partners’ commercial production. |

| 3 | Doosan Fuel Cell | Growing | 9 MW order (Dec 2025) | Transitioning from R&D to commercial production via Ceres license. |

| 4 | Mitsubishi Power | Not specified | Not specified | Sells complete SOFC systems for industrial and utility-scale power. |

| 5 | Robert Bosch Gmb H | Not specified | Not specified | Investing heavily in mass production for stationary and mobility applications. |

| 6 | Sunfire Gmb H | Not specified | >800 MW (SOFC/SOEC, end of 2024) | Spun off fuel cell business in 2024 to focus on electrolysis. |

| 7 | Topsoe | Not specified | DKK 5.73 Billion (H 1 2025, company-wide) | Primarily a catalyst and technology provider with strong SOEC business. |

| 8 | Aisin Seiki | Not specified | Not specified | Major Japanese manufacturer of residential/commercial SOFC CHP systems. |

| 9 | Cummins Inc. | Not specified | Not specified | Integrating SOFC technology into its broader hydrogen solutions portfolio. |

| 10 | Fuel Cell Energy | $0 (SOFC platform abandoned) | $0 (SOFC) | Exited the SOFC market in June 2025, taking a $64.5 M impairment charge. |

SOFC Adoption: Data Centers Drive Gigawatt-Scale Demand

The diversity of applications reveals a market at a critical inflection point. While established residential combined-heat-and-power (CHP) applications from companies like Japan’s Aisin Seiki demonstrate the technology’s long-term reliability in niche segments, the explosive growth is now concentrated in the power-hungry data center market. Bloom Energy’s partnerships with technology and finance giants like Oracle and Brookfield have validated SOFCs as a bankable, scalable solution for providing clean, reliable, grid-independent baseload power. This shift from government-subsidized pilots to commercially driven, multi-gigawatt deployments for critical digital infrastructure is the single most important trend defining the industry. The success of this high-volume application provides a halo effect, de-risking the technology for other industrial uses and creating a robust supply chain that benefits all players.

Bloom Energy Focuses on Data Center Market

This chart directly supports the section’s theme, as it explicitly identifies data centers as Bloom Energy’s largest and fastest-growing market, validating the claim that data centers are driving SOFC adoption.

(Source: Arya’s Substack)

North America Leads as Asia-Pacific Ramps Up SOFC Production

Geographically, North America has emerged as the undisputed leader in commercial SOFC deployment, almost exclusively due to Bloom Energy‘s success in the U.S. data center market. The scale of its order backlog confirms the region as the primary revenue generator for the foreseeable future. However, the manufacturing and technology development landscape is more globally distributed. Asia-Pacific is a crucial hub for production and future growth. South Korea’s Doosan Fuel Cell has begun mass-producing SOFC systems based on technology from the UK’s Ceres Power. In Europe, industrial powerhouses like Germany’s Robert Bosch Gmb H are making significant investments to establish volume production, signaling a strategic push to capture a share of the burgeoning market for decentralized energy.

China Poised to Lead Future Market Growth

This chart complements the section’s geographic analysis by forecasting future growth rates. It supports the text’s assertion that Asia-Pacific is ramping up by showing that China and South Korea are projected to lead market growth post-2026.

(Source: Future Market Insights)

Bloom Energy’s $20 B Backlog Signals SOFC Commercial Maturity

The recent commercial activities reveal a clear bifurcation in technological and commercial maturity. Bloom Energy stands alone in the “Commercially Scaled” category, with over a decade of deployment experience, a vertically integrated manufacturing process, and a deep backlog providing years of revenue visibility. Its ability to offer long-term service agreements creates a predictable, recurring revenue stream that is highly attractive to both customers and investors. In the next tier, companies like Ceres Power and its partner Doosan Fuel Cell are transitioning from R&D to commercial reality. The start of mass production in 2025 was a pivotal moment, shifting Ceres‘s model from one-off license fees to high-margin, recurring royalties. At the other end of the spectrum, Fuel Cell Energy’s exit from the SOFC space demonstrates the immense technical and financial challenges of competing, thereby validating the significant competitive moat built by the market leaders.

Bloom Energy Profitability Surges into 2026

This chart provides the financial data to back up the section’s claim of Bloom Energy’s commercial maturity. The projected growth in margin and positive EPS serves as direct evidence of the company’s financial strength and successful scaling.

(Source: LongYield – Substack)

SOFC Market Outlook: AI Demand versus Green Hydrogen Integration

The critical path for SOFC leaders in the year ahead involves balancing execution on massive data center backlogs with the strategic integration of green hydrogen as a fuel source to meet long-term decarbonization goals.

- The model of providing on-site, grid-independent power for data centers is accelerating. Watch for more multi-gigawatt agreements from hyperscale operators beyond the landmark 2.8 GW Oracle deal. Bloom Energy‘s projection of ~80% revenue growth in 2026 is the primary signal of this momentum.

- The technology licensing model is proving its viability. Monitor for announcements from Ceres Power regarding new licensees or significant follow-on orders for its partners like Doosan, which would indicate broader market adoption beyond a single manufacturer’s dominance.

- While data centers are the main event, watch for SOFCs to gain traction in other industrial applications requiring high-efficiency, reliable power, such as maritime and heavy industry. The scale achieved in the data center market will drive down costs, making the technology more competitive elsewhere.

- An emerging signal is the convergence of SOFC technology with the green hydrogen economy. Companies with expertise in both SOFC (power generation) and SOEC (hydrogen production), such as Topsoe and Sunfire, are uniquely positioned to capitalize on this future trend as customers demand a path to zero-carbon operations.

SOFC Market to Reach $12.5 Billion by 2032

A market forecast is the ideal chart for this outlook section. This chart quantifies the significant long-term growth potential of the SOFC market, aligning with the section’s discussion of AI-driven demand and future opportunities.

(Source: Verified Market Research)

The questions your competitors are already asking

This report covers one angle of commercial revenue and market consolidation in the SOFC sector. The questions that matter most depend on your work.

- Which SOFC manufacturers are gaining or losing ground based on order backlogs and projected 2026 revenue?

- What is the outlook for SOFC deployment in the AI and data center sector through 2026?

- What is actually happening with Ceres Power’s licensing model? Is the partnership with Doosan Fuel Cell progressing from pilot to recurring revenue?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.