Halliburton CCUS Projects, 2 Major Deals with NEP & In Capture, $30 B Aramco Mo U, and 5 Tech Partnerships (2024-2026)

CCUS Project Execution, Halliburton’s Shift to Commercial Scale Services

By 2025, Halliburton crystallized its Carbon Capture, Utilization, and Storage (CCUS) strategy around providing critical enabling services, positioning itself as a technology provider rather than a project owner to mitigate direct capital risk. This “picks and shovels” model leverages its core subsurface and wellbore expertise to de-risk complex storage projects for major energy clients, a significant shift from the industry’s earlier focus on smaller-scale pilot programs between 2021 and 2024.

- Before 2025, the CCUS market was characterized by feasibility studies and small-scale pilot projects, with service companies providing generalized support. Halliburton‘s role was less defined within the emerging low-carbon segment.

- In 2025, the market began a phase of “industrial hardening, ” with major projects moving toward execution. Halliburton secured a key contract in August 2025 with the Northern Endurance Partnership (NEP), a consortium including bp, Equinor, and Total Energies, for the UK’s first commercial offshore CCS system, validating its service-led approach.

- This strategic pivot allows Halliburton to capitalize on a market projected to grow from $5.82 billion in 2025 to $17.75 billion by 2030 without the high capital exposure of owning capture facilities. The company targets high-margin services like completions and downhole monitoring, essential for project bankability.

- The launch of the specialized XTR™ CS injection system in February 2026 further solidified this strategy, offering a purpose-built technology for the unique challenges of CO₂ injection wells and demonstrating a direct response to the market’s move toward commercial deployment.

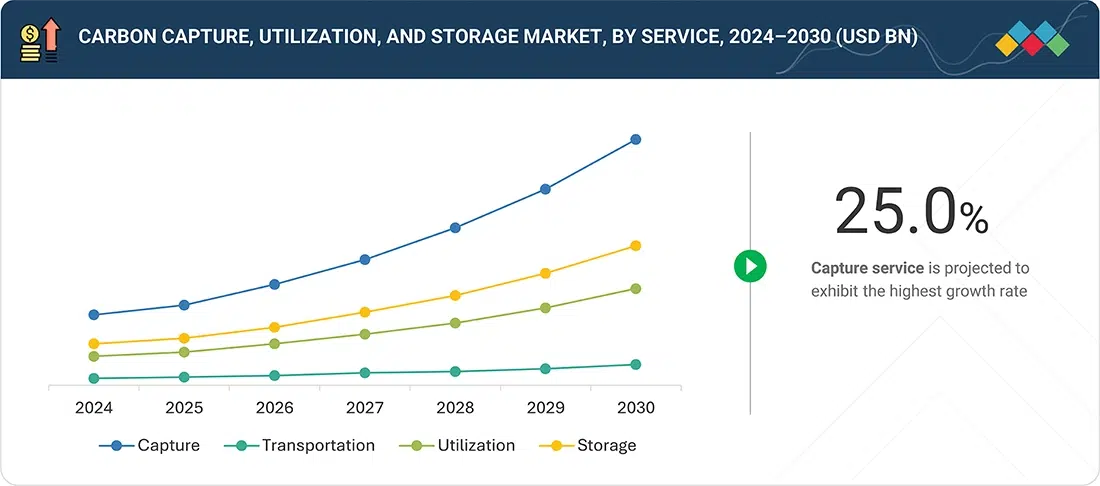

CCUS Services Market Forecasted for Strong Growth

The section details Halliburton’s strategic shift to providing commercial-scale CCUS services. This chart directly supports the narrative by quantifying the significant growth forecast for the CCUS services market, validating the business opportunity Halliburton is targeting.

(Source: MarketsandMarkets)

Halliburton 4 Key CCUS Alliances with NEP, Aramco, and In Capture (2024-2026)

Halliburton’s commercial strategy in the CCUS sector is built on forging strategic partnerships that embed its technology and services into large-scale, international projects from their early stages. These collaborations, established between 2024 and 2026, secure a pipeline of high-value work and position the company as an indispensable technical partner for energy majors and national oil companies navigating the energy transition.

- The most significant partnership is the August 2025 service contract with the Northern Endurance Partnership. This agreement makes Halliburton a core service provider for completions and monitoring on a flagship project that will define the UK’s CCS industry.

- In March 2025, Halliburton announced a collaboration with the In Capture joint venture in Australia. This early-stage involvement in identifying and maturing a commercial-scale CCS project allows Halliburton to influence technical decisions and secure future service contracts.

- A broad Memorandum of Understanding (Mo U) signed with Aramco in November 2025, part of a larger set of agreements potentially worth over $30 billion, includes collaboration on lower-carbon initiatives, opening a path for Halliburton to support Saudi Arabia’s decarbonization goals.

- Through its Halliburton Labs accelerator, the company onboarded five new clean tech companies in December 2024, including Cella, which focuses on innovative CO₂ storage. This provides Halliburton with low-cost access to next-generation technologies and market intelligence.

Energy Majors Lead Carbon Capture Market Share

This section highlights Halliburton’s key alliances with companies like Aramco. The chart illustrates that energy majors are the dominant players in the carbon capture market, which provides the strategic context for why Halliburton is partnering with these specific entities to secure market access.

(Source: Global Market Insights)

Table: Halliburton CCUS Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Aramco | Nov 2025 | Signed an Mo U as part of a potential $30 bn+ agreement package to collaborate on energy services and lower-carbon solutions, positioning Halliburton for future CCUS work in the Middle East. | Aramco |

| Northern Endurance Partnership (bp, Equinor, Total Energies) | Aug 2025 | Awarded a service contract for well completions and downhole monitoring for the UK’s first commercial offshore CCS system, a cornerstone project for the European market. | Halliburton |

| In Capture Joint Venture (with SK earthon) | Mar 2025 | Established a collaboration to provide expertise on a commercial-scale CCS project in Australia, securing an early-stage role in project maturation and design. | World Oil |

| Cella (via Halliburton Labs) | Dec 2024 | Onboarded Cella, a startup developing novel CO₂ storage solutions, into its accelerator program to foster innovation and gain access to emerging technologies. | Halliburton |

UK and Australia, Halliburton Secures Foothold in Key Offshore CCS Hubs

In 2025, Halliburton concentrated its CCUS commercial efforts on emerging offshore storage hubs in the UK and Australia, securing roles in nationally significant projects that serve as beachheads into these critical growth markets. This geographic focus aligns with its expertise in complex deepwater environments and targets regions with strong regulatory support for decarbonization.

- The UK North Sea became a primary focus with the Northern Endurance Partnership contract. This project leverages existing North Sea infrastructure and geological knowledge, making it a logical and strategic entry point for Halliburton to prove its CCUS service model in Europe.

- Offshore Western Australia represents another key market, with the collaboration on the In Capture G-15-AP project. Australia’s vast saline aquifers and history of large-scale gas projects provide an ideal setting for developing commercial CCS, and Halliburton‘s involvement positions it to capture future work in the Asia-Pacific region.

- While the US remains a large market driven by the 45 Q tax credit, Halliburton‘s marquee wins in 2025 were international. This signals a strategy to diversify its CCUS portfolio beyond North America and target first-mover opportunities in regions with clear, large-scale offshore storage potential. The broader EU carbon capture framework, with its ambitious targets and funding mechanisms, further validates the focus on the European market.

1 New Product Launch, Halliburton’s CCUS Technology Reaches Commercial Readiness

Halliburton’s technology strategy matured from adapting existing oil and gas tools to launching purpose-built CCUS solutions, signaling the market’s transition to commercial-scale operations that require specialized and reliable equipment. The company’s focus on well integrity and long-term monitoring directly addresses the primary technical risks and regulatory hurdles associated with permanent CO₂ sequestration.

- Between 2021 and 2024, Halliburton primarily marketed its existing portfolio of subsurface characterization software and well construction services for CCUS applications, with few dedicated product launches.

- The key validation point came in February 2026 with the launch of the XTR™ CS injection system. This wireline-retrievable safety valve was specifically engineered for the corrosive and high-pressure environment of CO₂ injection wells, moving beyond adaptation to genuine innovation.

- The company’s digital offerings, such as the LOGIX™ Automated Cementing System, became a cornerstone of its CCUS value proposition. This technology ensures the long-term integrity of the wellbore, a critical factor for securing regulatory permits and public acceptance for storage projects.

- Through its Halliburton Labs partnership with startups like Cella, the company maintains a pipeline of future technologies, ensuring it can address next-generation storage challenges without bearing all the R&D costs internally.

Carbon Capture Materials Market to See Explosive Growth

As this section discusses a new product launch and Halliburton’s technology reaching commercial readiness, this chart provides context on the innovation happening at a foundational level. The explosive growth in the materials market underscores the rapid technological advancement and market demand for new CCUS solutions.

(Source: Polaris Market Research)

SWOT Analysis, Halliburton’s Service Model vs. Market Risks

Halliburton’s strategic positioning in the CCUS market leverages its core strengths while navigating significant external uncertainties, creating a resilient but dependent business model. The shift from a nascent, theoretical market before 2024 to one defined by large-scale project execution in 2025 has both validated its approach and highlighted its key vulnerabilities.

- Strengths: Deep subsurface expertise and a capital-light service model reduce direct financial exposure.

- Weaknesses: Revenue is contingent on clients’ final investment decisions (FIDs), which are sensitive to policy and economic shifts.

- Opportunities: The massive projected growth of the CCUS market and securing contracts on flagship projects establish market leadership.

- Threats: Intense competition from rivals like SLB and the risk of widespread project delays or cancellations due to regulatory or funding issues.

Global CCUS Market to Reach $32B by 2035

The section presents a SWOT analysis of Halliburton’s strategy. This chart perfectly illustrates the ‘Opportunity’ aspect of the analysis by showing a large and rapidly expanding total addressable market, which is the primary external factor justifying Halliburton’s investment and strategic focus on CCUS.

(Source: openPR.com)

Table: SWOT Analysis for Halliburton CCUS Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Leveraged existing oil and gas subsurface expertise and strong balance sheet. | Secured contracts for major commercial-scale projects (NEP, In Capture) using core competencies in well construction and monitoring. | The market’s move to commercial-scale projects validated that Halliburton‘s core expertise is directly transferable and highly valuable for CCUS. |

| Weakness | CCUS was a nascent, non-core part of the business with an unclear revenue model. | Revenue remains dependent on client FIDs, which are subject to policy volatility like the potential erosion of the US 45 Q tax credit value due to inflation. | The reliance on client capital deployment was confirmed. The service model works but is a lagging indicator of market health, not a leading one. |

| Opportunity | The CCUS market was projected to grow, but commercial projects were scarce. | Capitalized on the “industrial hardening” of CCUS, winning work on projects aiming to store millions of tons of CO₂. Launched dedicated tech like the XTR™ CS system. | The opportunity shifted from theoretical to tangible. Halliburton proved it could convert market growth into specific, high-value contracts. |

| Threat | Competition from other oilfield service companies and the risk that CCUS would not scale commercially. | Direct competition with SLB on the NEP project, where SLB won a broader scope. Broader market risk from project delays and funding cuts. | The competitive threat materialized, with clients splitting work scopes. The market’s sensitivity to policy and execution risk was confirmed as a primary threat to the entire service sector. |

Halliburton’s 2026 Outlook, NEP Execution and New Contract Wins

Looking ahead, Halliburton’s success in the CCUS market hinges on its ability to execute flawlessly on its flagship contracts and convert the growing pipeline of global projects into secured revenue. The primary focus will be demonstrating that its specialized services can be delivered on time and on budget for complex, first-of-a-kind commercial storage facilities.

- If this happens: The Northern Endurance Partnership project progresses toward its 2027 first-injection target without significant delays or technical issues. Watch this: Milestone announcements related to well drilling, completion, and the installation of monitoring equipment. This would serve as the ultimate proof point for Halliburton‘s service model.

- If this happens: Halliburton secures at least one more major international CCUS service contract in 2026, particularly in a new geographic market like Southeast Asia or the Middle East. Watch this: Company announcements following major industry events and quarterly earnings calls for new contract wins.

- These could be happening: Increased market adoption of the XTR™ CS injection system and other digital CCUS solutions. Watch for client testimonials or case studies highlighting the performance of these technologies, as this would signal a strengthening competitive advantage over rivals offering more generalized solutions.

Oil & Gas Dominates 2025 CCUS Market

This section focuses on Halliburton’s 2026 outlook and contract wins. The chart directly supports this outlook by showing that the oil and gas sector—Halliburton’s traditional customer base—is the dominant segment of the CCUS market. This indicates a strong, existing client pool for their new CCUS services.

(Source: IMARC Group)

The questions your competitors are already asking

This report covers one angle of Halliburton’s commercial strategy for CCUS services. The questions that matter most depend on your work.

- Which oilfield service companies are gaining or losing ground in the CCUS market as it shifts to commercial scale?

- Halliburton activities in CCUS. Is the Northern Endurance Partnership (NEP) project progressing from planning to deployment?

- Halliburton investments and funding. Is the $30B Aramco MoU on track for definitive agreements?

- Which major energy operators are adopting a service-led model for their large-scale CCUS projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.