Hess CCUS Strategy Pivot, $1 B Chevron Acquisition, $750 M Guyana Credit Deal, and Capa Project Suspension (2025)

Corporate M&A as a Primary Risk for Standalone CCUS Project Timelines

Corporate acquisitions are a primary execution risk for mid-scale, standalone Carbon Capture, Utilization, and Storage (CCUS) projects, as demonstrated by Chevron’s acquisition of Hess, which caused a strategic pivot from regional project development to integration within a supermajor’s global portfolio. This M&A-driven disruption highlights how parent company capital allocation can override the project-level economics of individual carbon capture initiatives, even in a supportive policy environment.

- Between 2021 and 2024, Hess’s public carbon management strategy focused primarily on operational efficiency and methane reduction through its membership in the ONE Future coalition, with no major capital commitments to physical CCUS infrastructure.

- In early 2025, Hess signaled a clear financial strategy by purchasing 37.5 million jurisdictional carbon credits from the Government of Guyana for $750 million, favoring a large-scale offset approach over direct capital expenditure on capture technology.

- The completion of the Chevron acquisition on July 18, 2025, immediately subordinated Hess’s strategy to Chevron’s global infrastructure goals, which prioritize developing large-scale carbon capture hubs and achieving $1 billion in cost synergies.

- By September 2025, the direct result of this integration was the suspension of engineering activities for the Capa Gas Plant in North Dakota, a tangible project designed for the Bakken shale play, as capital was redirected toward assets with greater perceived strategic importance within Chevron’s portfolio.

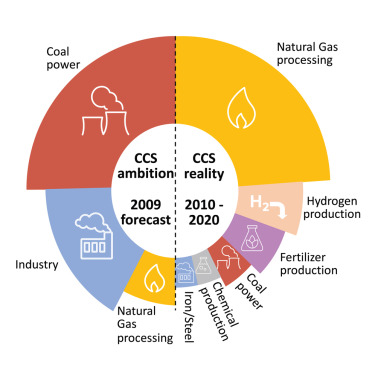

CCS Reality Diverges from 2009 Forecast

This chart highlights the inherent difficulties and underperformance of large-scale CCS projects, establishing a baseline of project risk. The section then argues that M&A activity, like the Chevron-Hess deal, introduces a significant additional layer of risk and uncertainty to project timelines.

(Source: ScienceDirect.com)

$750 M Credit Purchase, Hess Pivots After Capa Project Suspension

Hess’s 2025 capital allocation in carbon management was defined by two opposing actions: a major $750 million investment in carbon credits followed by the suspension of a key infrastructure project, illustrating the strategic conflict between market-based offset strategies and capital-intensive direct capture projects. The sequence of events shows a clear shift in priorities driven by new ownership, prioritizing portfolio-level synergies over pre-existing, regional project pipelines.

- The pre-acquisition purchase of 37.5 million carbon credits from Guyana represented a significant, immediate move to address emissions on the balance sheet, leveraging the established market for high-integrity, nature-based offsets.

- The post-acquisition suspension of the Capa Gas Plant, a planned 125 MMSCFD natural gas processing facility with CCUS potential, removed a major capital-expenditure item from Hess Midstream’s forecast, leading to a lowered capital outlook for 2026 and 2027.

- This decision aligns with Chevron’s broader strategy of consolidating capital toward its own large-scale, established low-carbon projects, such as the Bayou Bend CCS hub, rather than funding smaller-scale projects from an acquired entity’s pipeline.

Historical CO2 Emissions from ‘Carbon Majors’ Skyrocket

This chart illustrates the immense and growing pressure on major energy companies to address their carbon footprint. This context explains the urgency behind Hess’s strategy and why, after suspending the Capa infrastructure project, the company immediately pivoted to a large-scale credit purchase to continue managing its emissions liability.

(Source: InfluenceMap)

Table: Hess Carbon Strategy Investments & Cancellations (2025)

| Project / Investment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Capa Gas Plant | Sep 2025 | Suspension of early engineering for a 125 MMSCFD gas plant in North Dakota. The move was a direct result of the Chevron acquisition and a realignment of capital priorities. | Hess Midstream |

| Guyana Carbon Credits | Feb 2025 | Purchase of 37.5 million jurisdictional carbon credits for $750 million. This was Hess’s primary carbon mitigation strategy prior to the completion of the Chevron deal. | Weil, Gotshal & Manges LLP |

Hess 1 Major Acquisition, Chevron Deal Reshapes Carbon Strategy

The most significant partnership activity for Hess in 2025 was its acquisition by Chevron, a transaction that completely absorbed its independent carbon strategy and realigned its assets within a supermajor’s global low-carbon framework. This event superseded all other collaborative efforts, demonstrating how M&A can serve as the ultimate form of strategic partnership, dictating all subsequent project and investment decisions.

- The acquisition, completed on July 18, 2025, integrated all Hess assets, including its valuable positions in Guyana and the Bakken shale, into Chevron’s portfolio. Chevron’s stated goal is to lower the carbon intensity of the combined operations.

- As a result, Hess’s standalone carbon capture ambitions have been folded into Chevron’s established low-carbon business unit, which focuses on developing large-scale CCUS hubs and offset markets.

- While Hess continued its participation in the ONE Future coalition to reduce methane emissions, this operational-level initiative was overshadowed by the comprehensive strategic realignment mandated by the Chevron acquisition.

M&A Activity Reshapes Low-Carbon Sector

The chart shows a broad industry trend where mergers and acquisitions are a key lever for strategic change in the low-carbon space. The section provides a specific, high-profile example of this trend: the Chevron-Hess acquisition and its profound impact on Hess’s carbon strategy.

(Source: S&P Global)

Table: Hess Strategic Alliances and Corporate Actions (2025)

| Partner / Action | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Chevron Corporation | Jul 2025 | Acquisition of Hess Corporation. This transaction effectively ended Hess’s independent strategy and integrated its assets and carbon initiatives into Chevron’s global framework. | Chevron |

| ONE Future Coalition | Ongoing in 2025 | Continued participation in an industry group focused on voluntarily reducing methane emissions to less than 1% of gross production, representing an ongoing operational efficiency effort. | Hess Corporation |

North Dakota vs. Guyana, Hess Geographic Focus Shifts Post-Acquisition

Hess’s carbon management geographic focus shifted dramatically in 2025, from a dual interest in North Dakota’s physical infrastructure and Guyana’s jurisdictional credits to a complete consolidation under Chevron’s global portfolio strategy. The change illustrates how M&A can centralize and redirect the geographic priorities of an acquired company’s decarbonization efforts.

- Prior to the acquisition, Hess maintained two distinct geographic nodes for its carbon strategy: North Dakota, where the proposed Capa Gas Plant would have addressed emissions from its Bakken operations, and Guyana, the source of its $750 million carbon credit purchase.

- Following the acquisition, the North Dakota project was indefinitely suspended, removing the Bakken region as a near-term focus for new CCUS infrastructure development under the legacy Hess plan.

- The interest in Guyana remains through the ownership of the carbon credits, but their strategic use is now determined by Chevron. These credits can be applied across Chevron’s global operations, delinking them from the specific emissions of the Guyana oil production assets.

- The future of decarbonization for legacy Hess assets in the U.S. now depends on their proximity and integration potential with Chevron’s large-scale hubs, such as the Bayou Bend project on the Gulf Coast, rather than localized, bespoke solutions.

CO2 EOR Market Sees Steady Global Growth

This chart explains the business case for Hess’s previous CCUS focus in North Dakota, where a growing market for CO2 in Enhanced Oil Recovery (EOR) exists. This makes the post-acquisition strategic shift in geographic focus toward Guyana, which lacks a similar EOR market, all the more significant.

(Source: Future Market Insights)

Offsets vs. Infrastructure, Hess Shows Split in CCUS Tech Paths

Hess’s 2025 actions highlight a critical split in CCUS adoption pathways: leveraging the mature, financially-driven market for carbon offsets versus navigating the high-cost, long-timeline development of physical post-combustion capture facilities. The company’s pre- and post-acquisition strategies serve as a case study for the competing demands of immediate, scalable offsetting and long-term, capital-intensive infrastructure.

- The $750 million purchase of Guyanese carbon credits represented a strategic choice to use a mature, market-based instrument for immediate and large-scale emissions mitigation. This approach relies on established verification standards and financial markets, not technology development.

- In contrast, the proposed Capa Gas Plant represented a commitment to physical infrastructure for post-combustion capture. While the technology is commercially available, its deployment requires significant upfront capital, complex engineering, and a long development horizon, posing substantial project execution risk.

- The suspension of the Capa project after the Chevron acquisition suggests that for an acquired entity, such standalone projects are often deemed less strategically valuable or more economically risky compared to the parent company’s flagship initiatives, even with financial incentives like the 45 Q tax credit.

Absorber Unit Dominates Carbon Capture Plant Costs

The section discusses the strategic split between investing in physical infrastructure versus purchasing carbon offsets. This chart provides a clear financial rationale for this split by detailing the high capital costs associated with carbon capture plants, making the alternative path of offsets more financially flexible or attractive.

(Source: CSIS)

SWOT Analysis for Hess and its 2025 Carbon Capture Strategy

The acquisition by Chevron in 2025 fundamentally altered Hess’s SWOT profile regarding carbon capture, trading the agility and focused strategy of an independent operator for the scale, capital access, and systemic complexity of a supermajor. The shift exchanged project-level execution risk for portfolio-level integration risk.

- Strengths transitioned from financial flexibility to access to Chevron’s vast capital reserves and advanced technology portfolio.

- Weaknesses shifted from a lack of large-scale CCUS project experience to a loss of strategic independence and the de-prioritization of regional projects.

- Opportunities evolved from monetizing Bakken gas via a single plant to integrating assets into global low-carbon value chains.

- Threats moved from the execution risk of the Capa project to the integration challenges and internal capital competition within Chevron’s global portfolio.

World’s Largest Corporate Carbon Emitters Ranked

This chart provides essential context for the SWOT analysis by ranking major corporate emitters. This positions Hess and its new parent Chevron among the cohort of companies facing the most significant pressure (a Threat or Weakness) to develop and execute a viable carbon capture strategy.

(Source: InfluenceMap)

Table: SWOT Analysis for Hess CCUS Strategy (Pre- vs. Post-Acquisition 2025)

| SWOT Category | Pre-Acquisition (Jan – Jul 2025) | Post-Acquisition (Jul – Dec 2025) | What Changed / Validated |

|---|---|---|---|

| Strength | High-value assets in Guyana and the Bakken. A clear, financially-driven offset strategy via the $750 M Guyana credit deal. | Access to Chevron’s deep capital resources, global project portfolio (e.g., Bayou Bend), and established low-carbon technology division. | The value of Hess’s assets was validated by the acquisition. Its standalone financial strategy was replaced by the strength of a supermajor’s balance sheet and technical expertise. |

| Weakness | Lack of operational experience in developing and running large-scale, physical CCUS projects. Reliance on a single planned project (Capa). | Loss of strategic autonomy. Legacy Hess projects (Capa) are subject to de-prioritization in favor of Chevron’s existing flagship initiatives. | The weakness in project execution capacity became moot as the decision-making power shifted to Chevron, which has a more experienced carbon management team. |

| Opportunity | Leverage the 45 Q tax credit to build the Capa Gas Plant and decarbonize Bakken operations. Establish leadership in the high-integrity jurisdictional credit market. | Integrate Bakken and Guyana assets into Chevron’s global hydrogen and carbon capture value chains. Utilize Chevron’s scale to drive down costs. | The opportunity shifted from a single-project focus to a broader, portfolio-wide integration play with potentially greater long-term value but less near-term certainty for specific assets. |

| Threat | Project execution risk and potential capital overruns on the Capa Gas Plant. Market volatility for carbon credits. | Integration risk with Chevron’s corporate culture and systems. Capital starvation for legacy Hess projects amid competition within Chevron’s vast portfolio. | The primary threat changed from external project failure to internal corporate politics and capital allocation decisions. The suspension of Capa immediately validated this new threat. |

Hess Integration, Watch for Chevron’s Capa Plant Decision

The primary signal to monitor for the legacy Hess carbon strategy is Chevron’s decision-making regarding the suspended Capa Gas Plant and the broader plan for integrating Hess’s Bakken assets into its decarbonization framework. This will be the first major test of how Chevron values and intends to manage the carbon footprint of its newly acquired onshore assets.

- If Chevron revives the Capa project or announces an alternative CCUS solution in the Bakken, it will signal a strong commitment to decarbonizing these specific assets at the source, potentially validating the original project’s economics under a new owner.

- If the Capa plant remains suspended indefinitely, watch for commentary on whether the associated emissions will be managed through operational efficiencies or covered by retiring offsets, such as the 37.5 million credits acquired from Guyana.

- The disposition of the Guyana credits is a key indicator. If Chevron retires them to meet its own corporate climate targets, it confirms their value as an internal compliance tool. If it sells them on the voluntary market, it suggests a strategy of monetizing acquired carbon assets.

- Future capital expenditure announcements from Hess Midstream will provide definitive financial proof of the new strategic direction. Budgets that confirm lower spending for 2026 and 2027 will validate the long-term impact of the Capa project’s suspension.

ExxonMobil’s Carbon Capture Capacity Growth Over Time

As Chevron integrates Hess and re-evaluates the Capa plant, this chart provides critical competitive context. It benchmarks the aggressive carbon capture growth of its primary rival, ExxonMobil, framing the Capa decision as a key strategic move in the competitive landscape of energy supermajors.

(Source: OilNOW – Guyana’s)

The questions your competitors are already asking

This report covers one angle of CCUS project risk driven by corporate M&A. The questions that matter most depend on your work.

- What is the status of the Capa Gas Plant CCUS project in North Dakota following the Chevron acquisition?

- Hess’s carbon management activities. Is the $750M Guyana credit purchase a strategic pivot away from capital investment in physical CCUS infrastructure?

- What is the outlook for standalone CCUS project development in the Bakken shale after the Hess-Chevron deal?

- In the wake of the Chevron-Hess acquisition, which players are gaining ground in CCUS: supermajors with integrated global portfolios or regional project developers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.