Green Hydrogen Project Viability, $3/kg 45 V Credit, 52 Project Cancellations, and the Offtake Gap (2021 to 2026)

52 Cancellations, Green Hydrogen Projects Face Offtake Uncertainty

The Section 45 V tax credit has made green hydrogen production economics viable on paper, but a severe shortage of bankable offtake agreements is preventing a majority of announced projects from reaching final investment decision (FID). While the incentive effectively reduces production costs to be competitive with conventional hydrogen, the inability to secure long-term revenue contracts remains the single largest barrier to converting project pipelines into operational assets.

- Between 2021 and 2024, the market was characterized by project announcements and feasibility studies that were contingent on future policy. The lack of clarity around the 45 V credit’s implementation stalled major investment commitments, with developers unable to model reliable financial returns.

- The finalization of the 45 V regulations in January 2025 and the subsequent extension of the “commence construction” deadline to January 1, 2028, provided essential regulatory certainty. However, this clarity immediately exposed the market’s underlying weakness on the demand side.

- The period of uncertainty had tangible consequences. In the 18 months leading up to September 2025, approximately 52 commercial-scale clean hydrogen projects were publicly cancelled, with developers for 38% of these projects citing policy uncertainty as a primary factor. Even major energy firms like Exxon Mobil have faced headwinds with DOE funding for large-scale projects.

- The core issue is that project financing for high-CAPEX hydrogen facilities requires revenue certainty. While the $3/kg credit makes the Levelized Cost of Hydrogen (LCOH) attractive, financiers are unwilling to back projects without binding, long-term purchase agreements from credible offtakers.

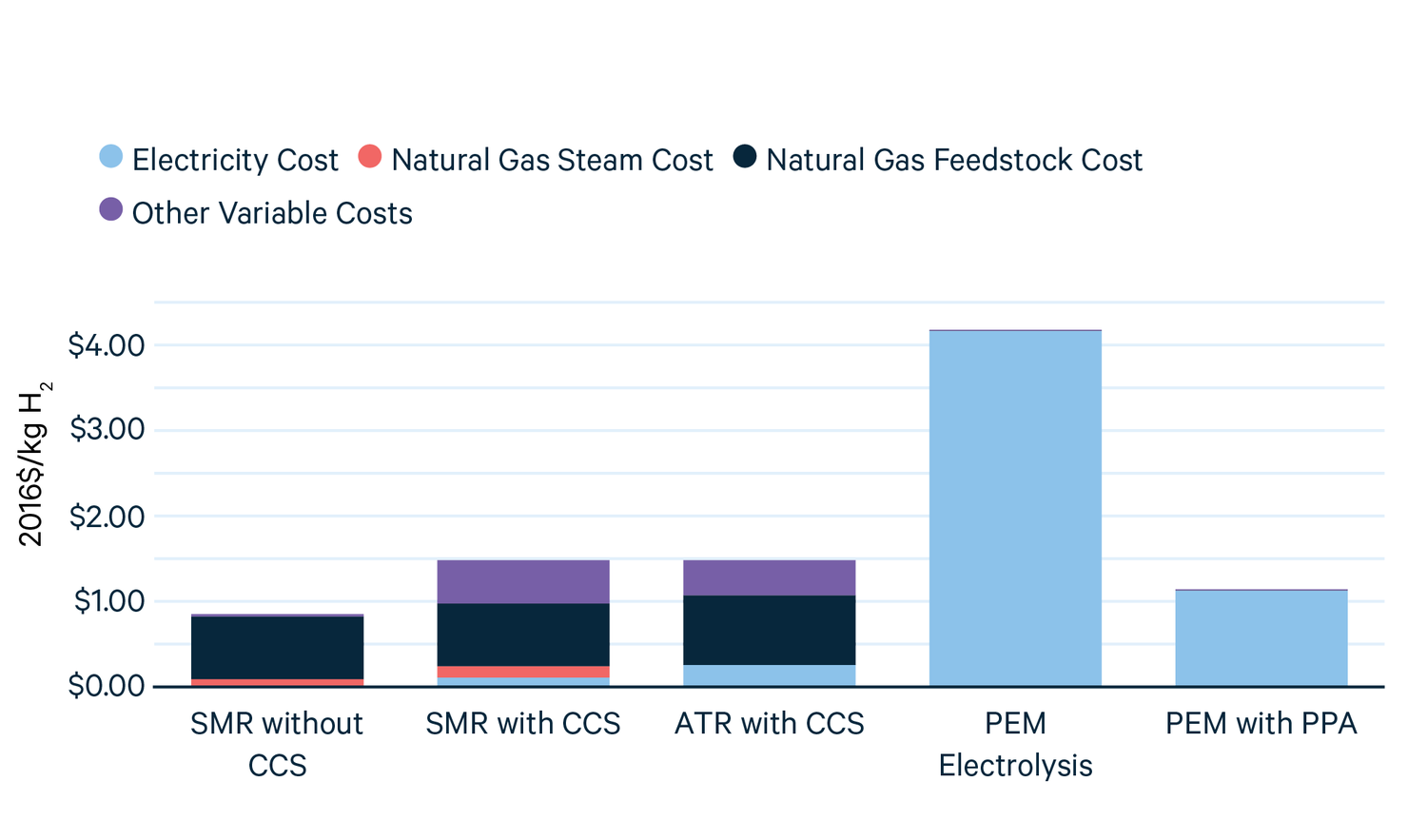

Hydrogen Production Cost Breakdown by Technology

The section’s focus on project cancellations and offtake uncertainty relates directly to project economics. This chart, by breaking down hydrogen production costs, visually explains the high expenses that challenge project viability and lead to the cancellations mentioned.

(Source: Resources for the Future)

Green Hydrogen Developers’ 4 M tpa Capacity at Risk from Cancellations (2024 to 2025)

Project cancellations accelerated in the period of regulatory limbo leading up to the final 45 V rules, wiping out millions of tons of potential annual production capacity and demonstrating extreme investor sensitivity to policy risk. This trend confirms that supply-side incentives, while powerful, are insufficient to de-risk investments without corresponding demand-side commitments.

- The cancelled capacity, estimated at 4 million metric tons per annum (mtpa), represents a significant setback for the industry’s growth targets. It underscores the financial community’s requirement for clear rules before deploying capital into long-cycle energy infrastructure projects.

- The primary driver for these cancellations was the inability of developers to model reliable returns without clear guidance on the “three pillars” of incrementality, temporal matching, and deliverability, which dictate eligibility for the maximum tax credit.

- The subsequent extension of the “commence construction” deadline to 2028 created a new window of opportunity for the development pipeline. However, the fundamental need for binding offtake agreements to secure project financing remains the primary hurdle to reaching FID.

- While some developers like Plug Power have successfully monetized tax credits through sale-leaseback transactions, such deals are often predicated on existing offtake agreements with major partners like Amazon, a luxury most standalone projects do not have.

Table: Clean Hydrogen Project Cancellations and Delays

| Entity / Trend | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Commercial-Scale Project Cancellations | 2024 – 2025 | 52 commercial-scale clean hydrogen projects were cancelled in the 18 months leading to September 2025. This represented 4 million metric tons per annum (mtpa) of potential capacity. | [PDF] Global Hydrogen Compass 2025 |

| Stated Reason for Cancellations | 2024 – 2025 | For 38% of the cancelled projects, developers explicitly cited policy and regulatory uncertainty as a primary contributing factor for halting development. | [PDF] Global Hydrogen Compass 2025 |

| Commence Construction Deadline Risk | 2025 | An analysis by Wood Mackenzie warned that 75% of US green hydrogen projects were at risk of missing the original 45 V tax credit deadline before it was extended, highlighting the long lead times for development. | 75% of US Green Hydrogen Projects at Risk, Says Wood Mac |

US Policy, Green Hydrogen Projects Hinge on 45 V Credit Viability

The United States, through the Inflation Reduction Act’s 45 V credit, has established itself as the most attractive global destination for clean hydrogen investment, but the actual realization of this project pipeline is now contingent on navigating state-level permitting and critical infrastructure bottlenecks. The focus of risk has shifted from federal policy uncertainty to on-the-ground execution challenges.

- Between 2021 and 2024, hydrogen policy announcements were globally dispersed, with Europe and Asia promoting significant initiatives. However, the scale of the US incentive post-IRA shifted the focus of global capital and development activity decisively toward North America.

- Since 2025, the US has become the clear leader in new project announcements. The $3.00/kg credit, which can reduce the LCOH of green hydrogen from over $4.00/kg to less than $1.50/kg, makes projects economically competitive with grey hydrogen produced from unabated natural gas.

- Project development is now concentrating in regions with abundant renewable resources, such as Texas (wind and solar), and existing industrial infrastructure, like the Gulf Coast. This geographic focus creates localized development challenges.

- These regional risks include long grid interconnection queues for the new renewable power required by the “incrementality” rule, a lack of midstream hydrogen transport and storage infrastructure, and complex, time-consuming state and local permitting processes. These factors now represent the next major hurdle for project developers.

Grid Carbon Intensity Determines Hydrogen’s Emissions

The section discusses project viability under the 45V credit, which is tied to carbon intensity. This chart illustrates a critical dependency for that viability: how the emissions of grid-powered hydrogen are determined by the grid’s carbon intensity, a key factor for credit qualification.

(Source: Center on Global Energy Policy – Columbia University)

$1, 500/k W, PEM Electrolyzer Costs Face Scaling Pressure

While electrolysis technologies like Proton Exchange Membrane (PEM) and Alkaline are commercially mature, the 45 V credit is creating unprecedented demand pressure on the manufacturing supply chain. Scaling production to meet the announced project pipeline without sacrificing quality or increasing costs remains a key execution risk for the entire industry.

- During the 2021–2024 period, the industry’s primary focus was on improving electrolyzer efficiency and demonstrating system performance in small-scale pilot projects. Manufacturing capacity was limited and tailored to a nascent market.

- From 2025 onward, the focus has shifted abruptly to industrial-scale manufacturing. Global annual electrolyzer manufacturing capacity is now estimated at 61 GW, with an additional 16 GW under construction, a massive oversupply compared to the volume of projects that have actually reached FID.

- The strict “three pillars” of the 45 V rules favor projects that co-locate new renewable energy sources with electrolyzers. This puts a premium on flexible technologies like PEM electrolysis, but their current capital costs of $1, 500–$2, 000/k W remain a significant component of overall project CAPEX.

- This dynamic has created a market imbalance. Manufacturers are scaling rapidly based on policy-driven forecasts, but project FIDs are stalled by the offtake shortage. If projects continue to be delayed, the electrolyzer sector could face significant consolidation or a sharp pullback in planned capacity expansions.

Clean Tech Costs Decrease as Deployment Scales

The section addresses electrolyzer costs and scaling pressure. This chart, a classic learning curve, directly visualizes the principle that technology costs decrease as deployment scales up, perfectly illustrating the dynamic described in the heading.

(Source: Center on Global Energy Policy – Columbia University)

SWOT Analysis, Green Hydrogen Project Economics Under 45 V

The 45 V credit provides a powerful, direct solution to the high production cost of green hydrogen, creating a clear strength. However, this is significantly counteracted by a critical weakness in demand-side maturity and an overarching threat from potential policy instability and infrastructure gaps that could derail the market’s trajectory.

45V Credit Can Make Green Hydrogen Cost-Competitive

The section calls for a SWOT analysis of project economics under 45V. This chart illustrates a primary ‘Opportunity’ in that analysis by showing how the tax credit can make green hydrogen economically competitive, a key factor for investment.

(Source: Resources for the Future)

Table: SWOT Analysis for Green Hydrogen Project Economics

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Green hydrogen offered a theoretical pathway to decarbonize hard-to-abate sectors, but production costs were prohibitive ($4.00-$6.00/kg). | The $3.00/kg tax credit directly addresses the cost barrier, making green hydrogen cost-competitive with grey hydrogen ($1.50-$2.50/kg) in many scenarios. | The primary economic barrier to production (high LCOH) was directly addressed by a powerful, bankable federal incentive, transforming project economics. |

| Weakness | The lack of offtake agreements was a known issue but was secondary to the fundamental problem of high production costs and policy uncertainty. | With production costs subsidized, the lack of bankable offtake agreements has become the primary bottleneck preventing projects from reaching FID. | Solving the production cost problem exposed the immaturity of the demand side as the new critical path risk for the entire industry. |

| Opportunity | Opportunity was focused on technology development and demonstrating electrolyzer performance at the pilot scale. | A surge in bankable projects, driven by the 45 V credit, has the potential to catalyze economies of scale in the electrolyzer supply chain and reduce CAPEX. | The incentive created a massive market signal, accelerating investment in manufacturing capacity and creating the potential for a virtuous cycle of cost reduction. |

| Threat | The main threat was regulatory uncertainty, specifically whether robust incentives would materialize and what the final rules would look like. | The primary threats are now political risk (repeal/modification of the IRA), the January 1, 2028 “commence construction” deadline, and physical infrastructure bottlenecks (grid, pipelines). | Regulatory risk shifted from “will the rules be good?” to “will the rules last?” while execution risks like permitting and grid access became more prominent. |

Green Hydrogen FID Momentum Depends on Offtake and Policy Stability

The critical variable for the US green hydrogen market in the next 12-24 months is the conversion rate of project announcements to final investment decisions. This rate hinges almost entirely on developers’ ability to secure bankable offtake agreements and the perceived stability of federal energy policy through a potential change in administration.

- If this happens: One or more major industrial players (e.g., in steel, ammonia, or refining) or a large utility signs a multi-year, fixed-price offtake agreement for a significant volume of green hydrogen. Watch this: Such a deal would provide a powerful de-risking signal to financial markets, triggering a wave of FIDs for the most advanced projects and validating the 45 V incentive model.

- If this happens: The January 1, 2028, “commence construction” deadline is not extended further and state-level permitting bottlenecks for both renewable generation and hydrogen facilities persist. Watch this: A significant portion of the current project pipeline will be at high risk of cancellation, as developers may run out of time to complete all necessary pre-development work and secure financing.

- These could be happening: The market may bifurcate. A small number of well-capitalized, vertically integrated projects with captive offtakers (e.g., industrial gas companies like Air Products supplying their own existing customers) move forward successfully. Meanwhile, the majority of speculative, standalone projects remain stalled, leading to a much slower and more fragmented market build-out than optimistic forecasts suggest.

Hydrogen Capacity Hinges on Demand, Policy Scenarios

This section connects investment momentum (FID) to offtake and policy stability. The chart directly mirrors this by showing how projected hydrogen capacity (the result of FIDs) is dependent on different demand (offtake) and policy scenarios.

(Source: RFF.org)

The questions your competitors are already asking

This report covers one angle of the gap between policy incentives and final investment decisions in the green hydrogen market. The questions that matter most depend on your work.

- What is actually happening with the US clean hydrogen project pipeline since the finalization of the 45V tax credit rules?

- What is the outlook for commercial-scale green hydrogen deployment by the 2028 ‘commence construction’ deadline?

- Which industrial sectors are signing bankable offtake agreements for clean hydrogen, and which are holding back?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.