Green Hydrogen Infrastructure, Germany’s €220 M Fund for 400 Trucks, and the Persistent Utilization Gap (2026)

Germany’s Hydrogen Infrastructure Risk: The Utilization Gap at Commercial Scale

Germany’s €220 million funding program, launched in January 2026 to deploy 400 hydrogen trucks and 40 refueling stations, directly confronts the industry’s “chicken-and-egg” problem but fails to solve the critical issue of long-term station utilization. The program creates a subsidized, self-contained ecosystem that improves initial project economics but leaves a significant gap between the initial fleet size and the capacity required for a station to reach its breakeven point, posing a substantial risk of creating stranded assets.

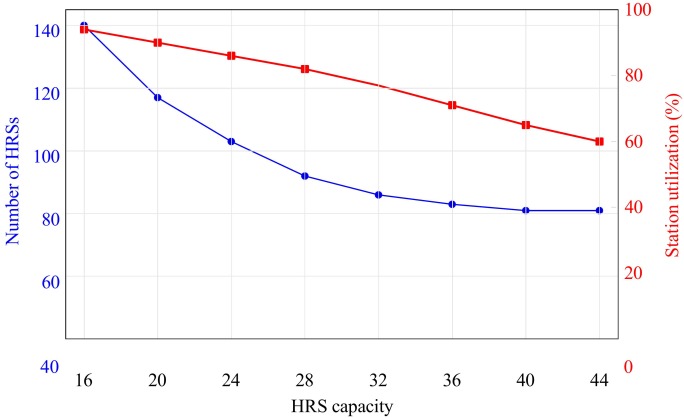

- Between 2021 and 2024, Germany’s hydrogen refueling network, primarily built for passenger cars, experienced a contraction, with the number of stations declining from a peak of around 110 to nearly 65. This was due to extremely low utilization, making the stations financially unviable and costly to maintain.

- The 2026 policy shift focuses exclusively on the heavy-duty vehicle market, aiming to create anchor demand by linking truck and station funding. The program establishes an average fleet of 10 trucks per new station, a marked improvement over the passenger car model.

- A new heavy-duty station, like the one in Lübeck, is designed with a capacity to refuel up to 50 trucks per day. The guaranteed demand from 10 trucks represents a baseline utilization of only 20%, a figure that improves initial bankability but remains well below the levels needed for standalone profitability.

- This persistent utilization gap means that without a rapid, unsubsidized expansion of the hydrogen truck fleet beyond the initial 400 units, these new stations will face the same adverse economics that led to the closure of earlier passenger-focused stations.

Station Utilization Gap Threatens Profitability

This chart illustrates the “utilization gap” risk by showing that as hydrogen station capacity increases, utilization drops, a core problem for Germany’s infrastructure plan.

(Source: ScienceDirect.com)

€220 M in CAPEX Subsidies, Germany’s Hydrogen Market De-risking

Government funding is successfully de-risking the high initial capital expenditure (CAPEX) for early movers in Germany’s hydrogen transport sector, but the lack of a corresponding long-term operational subsidy creates a significant “subsidy cliff.” While direct grants make initial projects financially viable by improving metrics like Net Present Value (NPV) and shortening payback periods, they do not address the high ongoing cost of green hydrogen, which remains the primary barrier to sustainable, market-driven adoption.

Capital Costs Drive Hydrogen Project Economics

This chart highlights the significant capital and truck costs that Germany’s €220M CAPEX subsidies are designed to de-risk for early hydrogen projects.

(Source: ScienceDirect.com)

Table: Germany’s Key Hydrogen Funding and Policy Mechanisms (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ks NI Program (German Federal Ministry for Digital and Transport) | Jan 2026 | €220 million in grants for up to 400 hydrogen trucks and 40 public refueling stations to create linked supply and demand. | electrive.com |

| Hydrogen Acceleration Act (German Government) | Feb 2026 | Designates hydrogen infrastructure of “overriding public interest” to shorten permitting and approval timelines, reducing pre-construction costs and risks. | Argus Media |

| H 2 Global Joint Tender (Australia-Germany) | Jan 2026 | Uses government funds via the HINT.CO instrument to purchase green hydrogen from international producers and sell it to German consumers, absorbing the price difference to secure supply. | DCCEEW |

| Canadian Hydrogen Imports (German Government) | Jan 2026 | A €200 million German scheme approved to support renewable hydrogen production in Canada for export to Germany, with auctions scheduled for 2027. | Enlit World |

OEM Partnerships, Daimler Truck and Cellcentric Fuel Cell Collaboration

Major truck original equipment manufacturers (OEMs) are forming strategic alliances to standardize fuel cell technology and reduce costs, a critical prerequisite for scaling the market beyond initial subsidized deployments. These collaborations, such as the cellcentric joint venture, signal a long-term commitment to hydrogen technology independent of short-term government incentives, focusing on the core challenge of making hydrogen trucks commercially competitive at scale.

OEMs Benchmark Fuel Cell Truck Efficiency

This chart shows the current fuel efficiency of trucks from major OEMs, providing context for the technology standardization goals of their strategic partnerships.

(Source: ScienceDirect.com)

Table: Key OEM Partnerships and Deployments in Germany’s Hydrogen Truck Market (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Daimler Truck / cellcentric | Late 2026 | Plans small-series production of 100 units of the Mercedes-Benz Next Gen H 2 truck, which uses liquid hydrogen (s LH 2) to achieve a range over 1, 000 km. This provides a clear technology pathway for long-haul trucking. | Automotive World |

| Toyota / cellcentric | Apr 2026 | Toyota joined the cellcentric joint venture with Daimler Truck and Volvo Group to accelerate the development and mass production of fuel cell systems, aiming to lower unit costs through shared scale. | Trucking Info |

| Hyundai / XCIENT Fleet | 2021-2026 | The Hyundai XCIENT Fuel Cell fleet has accumulated over 20 million km of real-world driving in Europe, demonstrating high technology readiness and providing critical operational data on durability and performance. | Hyundai News |

| MAN / Bavarian Fleet | Early 2026 | Began delivering its first hydrogen combustion engine trucks (MAN h TGX) to customers in Bavaria, representing a different technological approach within the hydrogen vehicle space. | Fuel Cells Works |

Germany’s National Strategy vs. European Hydrogen Infrastructure Gaps

Germany is positioning itself as Europe’s lead market for hydrogen-powered heavy transport by combining direct domestic subsidies with international procurement strategies, yet its national ambitions remain constrained by broader European infrastructure gaps. While Germany’s policy provides a clear demand signal, its effectiveness depends on the development of a coherent, cross-border refueling network and the availability of affordable, imported green hydrogen, highlighting the country’s dependence on factors outside its direct control.

Long-Haul Hydrogen Trucks Emerge

This chart visualizes the emergence of long-range hydrogen trucks, directly supporting the section’s data on new models designed for over 1,000 km.

(Source: ScienceDirect.com)

- Between 2021 and 2024, hydrogen policy in Europe was fragmented, focusing more on national strategies than on creating a unified, pan-European logistics network. This led to isolated infrastructure projects with limited interoperability.

- In 2026, Germany’s strategy acknowledges its role as a major hydrogen importer. It is actively funding production abroad, including a €200 million scheme for Canadian imports and the H 2 Global mechanism for Australian supply, to bridge the gap left by lagging domestic production.

- The European policy goal of having a hydrogen refueling station every 200 km along major transport corridors (TEN-T) provides a framework, but Germany’s plan to build only 40 stations is a small first step. The success of these stations depends on their integration into a wider network that allows for cross-border freight.

- The “Hydrogen Acceleration Act” streamlines permitting within Germany, but project developers still face inconsistent regulatory and permitting processes in neighboring countries, creating a significant bottleneck for establishing the crucial international logistics routes needed for a viable market.

SWOT Analysis for Germany’s Green Hydrogen Trucking Initiative

The strategic analysis of Germany’s hydrogen trucking policy reveals a strong foundation of government support and technological readiness, but significant threats from high operational costs and dependency on subsidies persist. The 2026 initiatives successfully address initial CAPEX and regulatory hurdles but have not yet created a clear path to a self-sustaining market free from government support.

Table: SWOT Analysis of Germany’s Hydrogen Truck Infrastructure Program

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong political will for decarbonization; established automotive OEMs (Daimler, MAN). | A €220 M grant program is launched; the Hydrogen Acceleration Act passes, shortening permit times; high TRL of fuel cell trucks is proven. | Policy has translated into tangible financial support and regulatory relief, directly addressing key project development barriers. |

| Weaknesses | Chicken-and-egg problem stalls investment; very low utilization of passenger car H 2 stations; high cost of green hydrogen. | The cost gap for green hydrogen remains vast (€70-€275/MWh); domestic production lags; station utilization for the 400-truck fleet will still be low. | The core weakness shifted from a lack of any demand to insufficient demand to make subsidized infrastructure profitable on its own. The high cost of fuel remains unresolved. |

| Opportunities | Potential to lead Europe in heavy-duty decarbonization; leverage OEM strength. | First-mover advantage for funded projects; creation of strategic refueling hubs; activation of the component supply chain (fuel cells, tanks, electrolyzers). | The 2026 program creates a defined, de-risked market entry point, turning theoretical opportunities into concrete projects for a select group of companies. |

| Threats | Competition from battery-electric trucks; lack of cost-competitive green hydrogen supply. | A “subsidy cliff” when grants end; fuel price volatility from import dependency; technology standardization risk (liquid vs. gaseous H 2); continued competition from improving battery-electric trucks. | The threat has become more specific: the risk is no longer market inaction but the potential for a market collapse after the initial subsidies are exhausted. |

Scenario Modelling: The Risk of Stranded Assets Without Operational Subsidies

If Germany does not introduce a long-term operational support mechanism, such as a Contract for Difference (Cf D), by the time the initial 400-truck fleet is deployed, the new hydrogen refueling stations are at high risk of becoming stranded assets. The prohibitive cost of unsubsidized green hydrogen will make it impossible for fleet operators to run the trucks economically, destroying the demand that the stations were built to serve. The critical signal to watch is whether policymakers shift their focus from CAPEX grants to OPEX support to ensure long-term viability.

- The current policy framework successfully ignites the market but does not provide the fuel to keep it running. The cost of green hydrogen remains double that of useful energy from battery-electric alternatives, an unsustainable gap for any commercial operator.

- Industry groups like BDEW are already warning that the hydrogen ramp-up is at risk without an integrated policy package that includes long-term price security. Their advocacy for Cf Ds will be a key indicator of market pressure on policymakers.

- The progress of Germany’s international procurement efforts, such as the H 2 Global auctions, will be a critical variable. If these mechanisms fail to secure green hydrogen at a price that can be passed on to consumers competitively, the entire domestic transport strategy is undermined.

- Watch for follow-on announcements from the German Federal Ministry for Digital and Transport (BMV). The absence of a successor program to the €220 million fund or a new policy addressing the green hydrogen price gap by 2027 would be a strong negative signal for investors.

The questions your competitors are already asking

This report covers one angle of the utilization risk in Germany’s heavy-duty hydrogen infrastructure strategy. The questions that matter most depend on your work.

- What is the outlook for heavy-duty hydrogen refueling station profitability in Germany beyond the 2026 subsidy program?

- What is actually happening with Germany’s H2 station network since the 2026 policy shift to heavy-duty trucks?

- Germany’s €220M investment. Is the program’s target of 10 trucks per station sufficient to avoid creating stranded assets?

- Which fleet operators and logistics companies are participating in Germany’s 2026 hydrogen truck program?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.