Green Methanol Supply, 100 New Vessels, 7 M Ton Demand, and Korea’s $450/ton Cost Gap (2021 to 2025)

Green Methanol Adoption, Korea’s 100 New Vessels vs. Global Supply Scarcity

South Korea’s aggressive strategy to build and deploy methanol-fueled vessels created a significant supply-demand imbalance in 2025, as global green methanol production capacity has not kept pace with the rapidly growing order book.

- Between 2021 and 2024, the industry focused on planning and announcements; in 2025, this shifted to execution with the global delivery of over 100 new methanol dual-fuel vessels, a substantial portion built in Korean shipyards.

- This new fleet, combined with future orders, is projected to require approximately 7 million metric tons of renewable methanol annually by 2030, but anticipated global production is significantly lower, creating a clear supply bottleneck.

- The supply-demand gap presents a critical operational risk: without sufficient green methanol, these advanced dual-fuel vessels are forced to operate on conventional fuels, completely undermining the multibillion-dollar investment in decarbonization.

- Major global carriers solidified the demand signal in 2025, with companies like COSCO and Maersk placing large orders that, while validating the technology choice, further strained the nascent and underdeveloped green methanol supply chain.

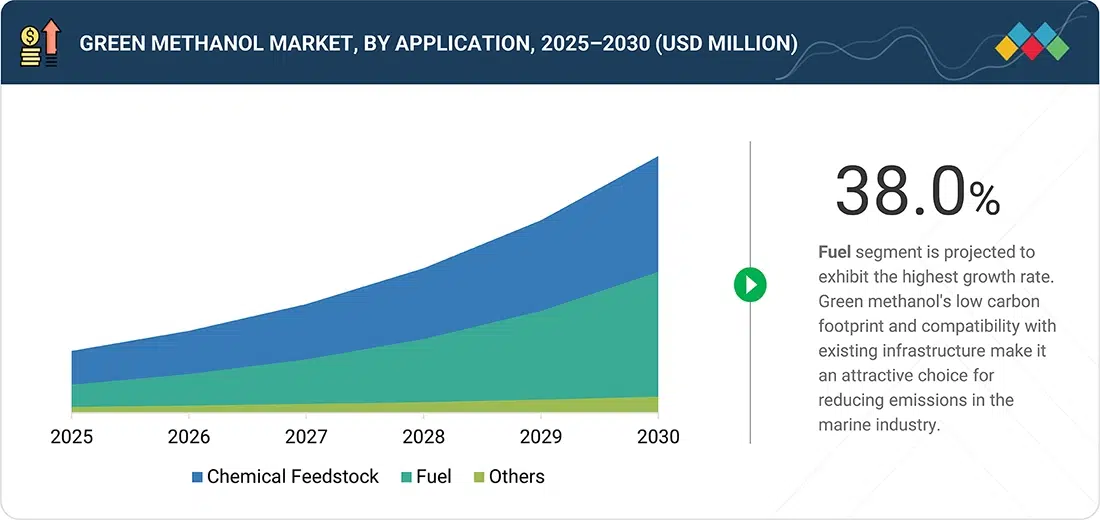

Marine Fuel to Drive Green Methanol Growth

This chart is selected for Section 0 because the section discusses Korea’s significant adoption of methanol-fueled vessels, which creates demand. The chart’s headline directly identifies the marine sector as the primary driver of green methanol growth, perfectly contextualizing the trend described.

(Source: MarketsandMarkets)

$1.75 B COSCO Order, Korean Shipbuilders’ Methanol Vessel Investments

While direct investment into South Korean green methanol production remained in early stages through 2025, massive capital flowed into the demand side through new vessel orders at Korean shipyards, creating a stark contrast with the high-risk, capital-intensive nature of upstream fuel production.

- The most significant investment signals were on the demand side, exemplified by COSCO‘s commitment of $1.75 billion to build 29 new ships, with a major focus on methanol-fuel technology from top-tier shipbuilders.

- Analysis in 2025 confirmed that green hydrogen is the primary production cost driver for e-methanol, accounting for 60% to 80% of the total cost, making new production facilities highly sensitive to the price of renewable electricity.

- The high capital expenditure for new green methanol plants and the significant price premium for the fuel created a classic investment standoff, as fuel producers remained hesitant to commit capital without binding long-term offtake agreements from shippers.

Green Methanol Ship Market Valued at $5.85B

Section 1 mentions a specific $1.75 billion order. This chart, valuing the total ‘Green Methanol Ship Market at $5.85B,’ provides crucial context to the reader, demonstrating the significant scale of the COSCO order within the overall market.

(Source: Fortune Business Insights)

Table: Strategic Investments in Methanol-Fueled Shipping (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| COSCO Newbuild Program | Oct 2025 | Commitment of $1.75 billion for 29 new ships, many featuring methanol dual-fuel technology. This validates the demand for methanol-powered vessels and directs significant capital to Korean and Chinese shipyards. | Breakbulk News |

| Maersk Fleet Expansion | 2025 | Took delivery of 10 large methanol-enabled vessels during 2025, bringing its total to 12. This action by an industry leader provides tangible proof of the move toward methanol and creates real-world demand for fuel. | Maersk Annual Report |

Korea-Europe GSC, 84 Global Corridor Initiatives, and Port Partnerships (2025)

South Korea is leveraging Green Shipping Corridors (GSCs) as its primary strategic tool to de-risk green methanol adoption, focusing on partnerships between ports, governments, and shipping lines to concentrate demand and coordinate infrastructure development.

- The Korea–Europe Green Shipping Corridor is the centerpiece of the nation’s strategy, with a 2025 proposal outlining an ambitious target of using 70% green methanol for vessels operating on this high-volume trade lane.

- The development of action plans for a Korea-U.S. GSC, involving the Port of Busan and the Northwest Seaport Alliance (Seattle/Tacoma), was a key focus in 2025, with methanol being the most widely considered fuel choice.

- These efforts are part of a global trend that saw the number of active GSC initiatives expand to 84 in 2025. Korea’s focus on methanol within these frameworks places it at the forefront of operationalizing the transition.

Chart Maps Methanol Shipping Ecosystem and Value Chain

Section 3 discusses global corridors, initiatives, and partnerships. This chart is the most appropriate match as it promises to visually map the very ‘ecosystem and value chain’ that these international collaborations help to build.

(Source: MarketsandMarkets)

Table: Key Green Shipping Corridor Partnerships Involving Korea (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Korea–Europe Green Shipping Corridor | Apr 2025 | A proposal to establish a GSC with a target of 70% green methanol fuel usage. The corridor is designed to aggregate demand and accelerate the development of bunkering and supply infrastructure between major Korean and European ports. | Solutions for Our Climate |

| Korea-U.S. Green Shipping Corridor | 2025 | Development and implementation of 2025 Action Plans involving the Port of Busan and U.S. West Coast ports like Seattle and Tacoma. Methanol is the most widely considered fuel, aiming to decarbonize a key trans-Pacific trade route. | Solutions for Our Climate |

Asia-Pacific vs. Europe, South Korea’s Green Methanol Shipbuilding Dominance

While regulatory drivers for decarbonization originate primarily in Europe, Asia-Pacific, led by South Korea’s formidable shipbuilding industry, solidified its role in 2025 as the global center for constructing the methanol-fueled fleet, creating a distinct geographical split between policy demand and physical supply.

- From 2021 to 2024, industry activity was characterized by global policy negotiations at the IMO and initial corridor announcements. The dynamic shifted in 2025 to concrete regional action.

- Europe’s Fuel EU Maritime regulation, which commenced on January 1, 2025, created a tangible and legally binding demand signal for low-carbon fuels on critical trade routes originating or terminating in the EU, including the Korea-Europe corridor.

- In response, South Korea’s industrial base, including shipbuilders HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean, captured the majority of the global order book for methanol-powered vessels, establishing the Asia-Pacific region as the dominant force in building the next generation of container ships.

- This industrial might, which includes not just shipbuilding but also global leaders in advanced manufacturing like SK Hynix, positions the country to execute complex technological transitions, though it remains dependent on international fuel supply chains.

Asia-Pacific Methanol Ship Market Growth Accelerates

Section 5 specifically focuses on the Asia-Pacific region and South Korea’s dominance. This chart is a perfect match because its headline explicitly refers to the accelerating growth of the ‘Asia-Pacific Methanol Ship Market,’ directly supporting the section’s regional analysis.

(Source: Fortune Business Insights)

Technology Readiness, Green Methanol’s TRL 9 vs. Ammonia’s Pilot Stage

Green methanol’s high Technology Readiness Level (TRL 9) for vessel engines confirmed its status in 2025 as the most pragmatic alternative marine fuel for immediate deployment, though its commercial maturity is now constrained by the still-developing green hydrogen and biogenic CO 2 supply chain.

- Throughout 2021-2024, methanol was evaluated alongside LNG and ammonia as a potential future fuel. By 2025, with over 100 methanol dual-fuel vessels in operation or being delivered, it decisively pulled ahead of ammonia, which remained at the pilot stage.

- The core technological challenge has pivoted away from the vessel engine, which is commercially available from major manufacturers, to the fuel production pathway itself, which remains economically immature.

- The critical barrier is the cost of green hydrogen, which requires renewable electricity prices below $20–$30/MWh to approach cost-competitiveness with fossil-based hydrogen, a price point rarely achieved at scale. The cost of power from grid operators like Dominion Energy is a key variable.

- The prevalence of dual-fuel engines acts as a crucial technological hedge, allowing ship owners to invest in new assets while mitigating the risk of fuel unavailability, albeit at the cost of undermining emissions reduction goals if fossil fuels are used.

Green Methanol Drastically Cuts Shipping Emissions

Section 6 discusses technology readiness. A chart showing that green methanol ‘Drastically Cuts Shipping Emissions’ provides a powerful justification for its TRL 9 readiness level and explains why it is being adopted over other, less-developed fuel options.

(Source: Green Fuel Journal)

SWOT Analysis, Korea’s Green Methanol Shipbuilding Strengths and Fuel Cost Weaknesses

South Korea’s 2025 green methanol strategy successfully leverages its world-class shipbuilding strengths to lead the hardware side of the maritime energy transition but remains highly exposed to external threats from volatile fuel costs and a lagging global supply chain.

- The nation has effectively built a dominant position in the construction of methanol-capable vessels, a key strength.

- However, this strength is offset by a critical weakness: the extreme cost premium of green methanol and the near-total lack of domestic production capacity.

- The primary opportunity lies in capturing a significant share of the rapidly growing market for green ships and fuels, projected to exceed $30 billion by the early 2030 s.

- The most significant threat is the failure of global green methanol production to scale, which would strand these advanced assets on conventional fuel and nullify the strategic push.

Table: SWOT Analysis for Korea’s Green Methanol Marine Initiative

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Established reputation in shipbuilding and LNG carriers. | Secured the majority of global orders for methanol dual-fuel vessels. Leadership in GSC planning (Korea-Europe, Korea-U.S.). | Korea validated its ability to pivot its shipbuilding dominance from LNG to methanol, moving from a theoretical capability to a market-leading position in the new order book. |

| Weakness | High dependency on imported energy and lack of domestic alternative fuel production. | The cost gap became starkly clear: green methanol costs $450-$650/ton vs. fossil methanol at under $250/ton. A domestic production strategy was not yet visible. | The abstract concern about fuel cost became a quantifiable, multi-hundred-dollar per ton barrier to adoption as the first large vessels were deployed. |

| Opportunity | Potential to be a first-mover in the green shipping transition. | Fuel EU Maritime regulation (Jan 2025) created a mandatory market for low-carbon fuels on the EU trade lane. The green methanol ship market is forecast to grow at a CAGR over 25%. | The opportunity shifted from a voluntary, “green premium” market to a compliance-driven market in key geographies, validating the strategic focus on the Korea-Europe corridor. |

| Threat | The “chicken-and-egg” problem of fuel availability vs. vessel orders was a known risk. | The “egg” was produced: over 100 new vessels were delivered in 2025, but the “chicken” (fuel production) lagged far behind, with projected demand at 7 million tons vs. minimal supply. | The theoretical “chicken-and-egg” problem became a tangible, near-term supply crisis. The risk is no longer conceptual but an immediate operational challenge for 2026 and beyond. |

2026 Outlook, Korea’s Green Methanol Strategy Hinges on Offtake Agreements

The success of South Korea’s green methanol strategy in 2026 will be determined by its ability to translate its Green Shipping Corridor frameworks into bankable, long-term offtake agreements that can finally de-risk and unlock investment in upstream fuel production.

- If this happens: Major Korean shipping lines, potentially with government backing, sign binding, multi-year offtake agreements for green methanol sourced for the Korea-Europe GSC, providing producers with the revenue certainty needed to secure project financing.

- Watch this: The price spread between green methanol and marine gas oil (MGO), and the effective carbon price under the EU’s Emissions Trading System. A narrowing of this gap, or a significant rise in the carbon price, would provide a powerful market-based incentive for adoption.

- These could be happening: Korean industrial and energy firms may take equity stakes in overseas green methanol production projects to secure a strategic supply. The challenges mirror those in other sectors, such as the push for Sustainable Aviation Fuel, where offtake agreements are critical to scaling new technologies.

Green Methanol Market to Exceed $11B by 2030

Section 9 provides a ‘2026 Outlook.’ The chart’s forecast that the market will ‘Exceed $11B by 2030’ offers a concrete, forward-looking data point that quantifies the potential of the market and substantiates the section’s strategic focus.

(Source: MarketsandMarkets)

The questions your competitors are already asking

This report covers one angle of the global green methanol supply-demand gap driven by South Korea’s maritime strategy. The questions that matter most depend on your work.

- What is actually happening with the 100+ methanol dual-fuel vessels delivered in 2025? Are they securing green methanol or running on conventional fuel?

- What is the outlook for green methanol supply meeting the projected 7 million ton demand from the new global fleet by 2030?

- What are the opportunities for green methanol producers and suppliers in the South Korean marine fuel market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.