Data Center Project Cancellations, 7 GW Capacity Gap, 300 State Bills, and Tax Incentive Rollbacks (2025 to 2026)

The race to deploy 100 k W per rack AI infrastructure has collided with an immovable barrier: the physical and political limits of the power grid. The primary constraint on AI expansion is no longer the ability to cool high-density hardware, but the inability to secure power and permits in a timely fashion. This has triggered widespread project cancellations and a wave of regulatory and community backlash, creating a systemic risk that threatens to derail billions in planned investment. The data center industry’s long-standing playbook of securing favorable tax treatment in exchange for development is now being actively challenged, fundamentally altering the economics and geography of digital infrastructure.

Data Center Project Delays, 7 GW Capacity Gap, and 300 State Bills

The rapid escalation of data center power demand has outpaced grid capacity and public acceptance, leading to widespread project delays, cancellations, and a wave of new state-level regulations that now pose the primary risk to AI infrastructure growth.

- Between 2025 and 2026, a new crisis emerged where nearly half of all planned AI data center projects in the U.S. were either delayed or canceled, creating a potential capacity gap of 7 GW. This contrasts sharply with the pre-2025 environment, where development was constrained primarily by supply chain and construction timelines, not systemic power and regulatory blockades.

- The political landscape shifted dramatically in early 2026, with over 300 state bills related to data centers filed across more than 30 states. This legislative activity marks a decisive pivot from the incentive-driven policies of 2021-2024 to a new era of regulatory scrutiny focused on energy consumption and tax equity.

- Community opposition became a primary driver of project failure, with the number of data center projects canceled due to local resistance quadrupling in 2025. At least 25 planned projects were halted, signaling that gaining local social license is now as critical as securing power from utilities like Dominion Energy.

- Globally, estimates for 2026 suggest that 30% to 50% of all large data center projects will be delayed. This is a direct result of power constraints from grid operators like PJM and shortages of essential electrical equipment, including transformers and switchgear.

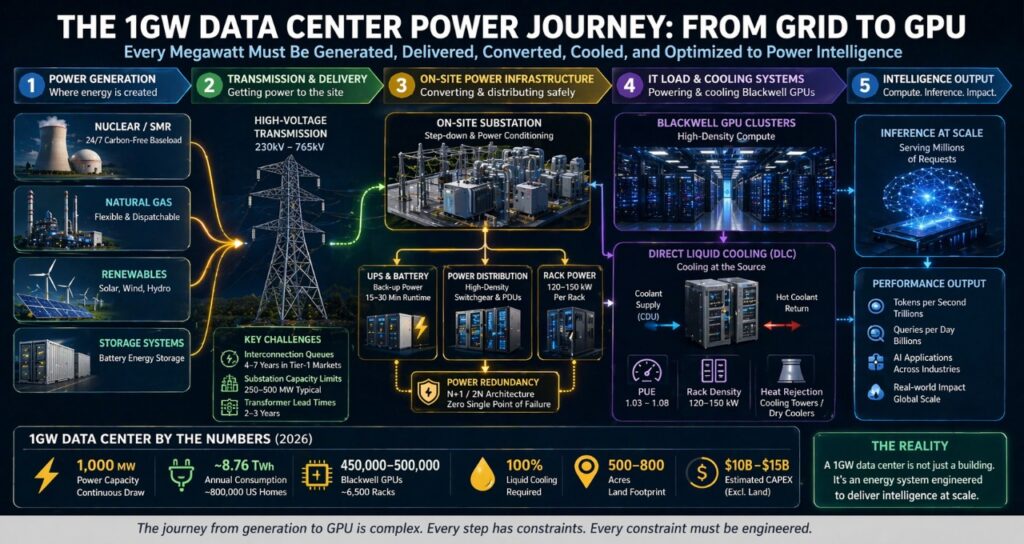

The Scale of a 1GW AI Data Center

The section discusses a ‘7 GW Capacity Gap.’ The chart provides critical context for this number by illustrating the immense scale of a single large data center, helping the reader visualize the magnitude of the capacity shortfall.

(Source: tech plus trends)

Data Center Cancellations, 25 Projects Halted, and Quadrupled Local Opposition (2025 to 2026)

A surge in community opposition and regulatory friction caused data center project cancellations to quadruple in 2025, representing a new, significant source of financial and development risk for investors and operators.

- In 2025, at least 25 data center projects were canceled specifically because of community opposition, a fourfold increase from the prior year. This trend indicates that grassroots resistance to the noise, water, and energy impacts of large-scale facilities has become a material risk to project development pipelines.

- The high rate of cancellations and delays has significant financial consequences, as developers often invest millions in site acquisition, engineering, and permitting before a project is halted. This rising risk of stranded capital is forcing a re-evaluation of site selection criteria and investment models across the industry.

- Global data from 2026 reinforces the scale of this problem, with multiple analyses projecting that up to half of all large data center projects scheduled to come online in the year face delays. This bottleneck is not isolated to specific markets but reflects a worldwide strain on power grids and supply chains.

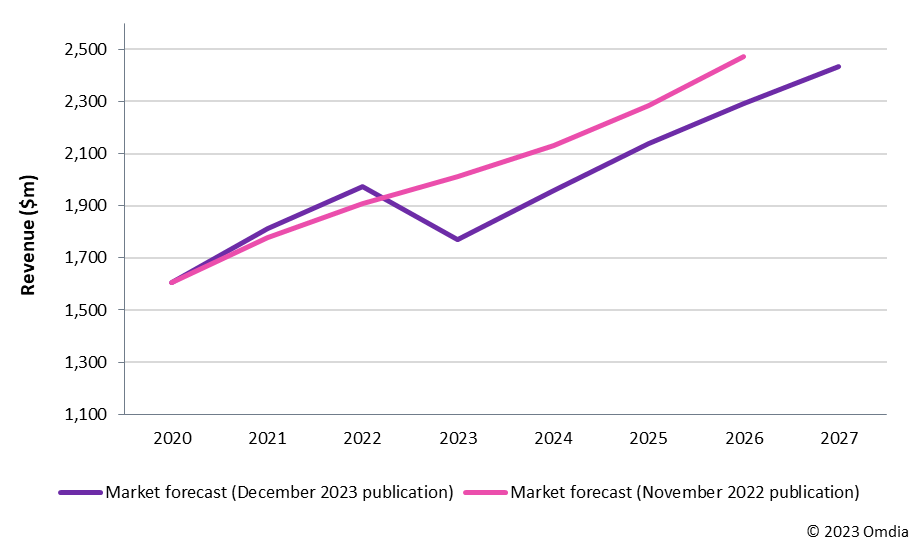

Data Center Rack Market Forecasts Revised Downward

The section focuses on project cancellations and halts. The chart directly illustrates a key economic consequence of these negative developments, showing how halted projects translate to a weaker market outlook for essential hardware like racks.

(Source: Omdia – Informa)

Table: Data Center Project Delays and Cancellations (2025-2026)

| Event / Trend | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Project Delays | 2026 | Nearly half of planned U.S. AI data center builds were delayed or canceled, creating a 7 GW capacity gap due to shortages of power and infrastructure. | Tom’s Hardware |

| Global Project Delays | 2026 | An estimated 30% to 50% of large data center projects scheduled to come online globally are expected to be delayed due to power and equipment shortages. | Semafor |

| Community Opposition | 2025 | The number of data center projects canceled due to community opposition quadrupled, with at least 25 projects being halted by local resistance. | Gizmodo |

| Long-Term Project Failure | 2026 | Analysis indicates that projects are being canceled long after initial planning due to unresolved power, zoning, and community issues that were present from the outset. | Medium |

US Regulatory Backlash, Virginia’s $1.6 B Tax Fight, and Illinois Incentive Suspension

The United States, particularly long-standing data center hubs like Virginia, has become the epicenter of regulatory backlash, with state governments now actively reconsidering the economic trade-offs of massive data center energy consumption.

- Virginia’s “Data Center Alley, ” the world’s largest concentration of data centers, is now a political battleground. The state’s sales tax exemption cost the commonwealth an estimated $1.6 billion in forgone revenue in fiscal year 2025, prompting intense debate over the policy’s future and the strain on the Dominion Energy grid.

- In a significant policy reversal, Illinois Governor Pritzker announced a two-year suspension of state tax incentives for new data center developments, effective July 1, 2026. This move reflects a growing concern among policymakers about the impact of data centers on grid stability and electricity prices for other consumers.

- The trend is widespread, with legislators in at least 28 states introducing bills in 2026 to roll back or re-evaluate existing tax incentives for data centers. This marks a fundamental shift from just a few years ago when states competed to offer the most generous incentive packages.

- However, the legislative landscape is fragmenting. While some states are pulling back, others like Pennsylvania are moving forward with new incentives. The Shapiro administration proposed new tax breaks to support a planned $20 billion investment by Amazon Web Services, highlighting the diverging state-level strategies for attracting digital infrastructure.

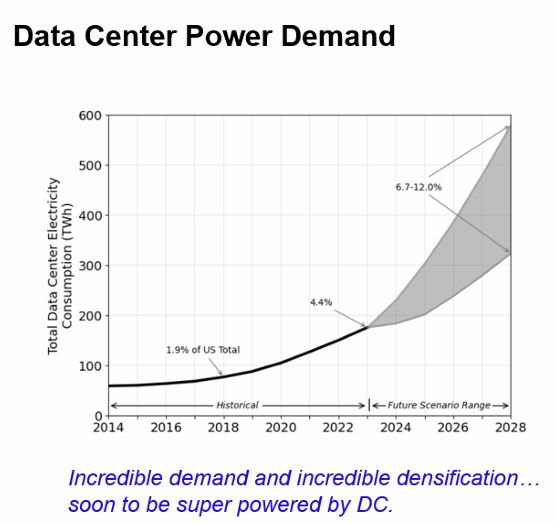

Data Center Power Demand Projected to Spike

This section details regulatory and tax backlash. The chart illustrates the underlying cause of this backlash—the overwhelming spike in power demand that strains public resources and prompts governmental action.

(Source: LinkedIn)

AI Data Center Power Procurement, 10-Year PPAs, and Grid Interconnection Queues

The technological and physical maturity of high-density data centers is now directly constrained by the immaturity of supporting grid infrastructure, forcing operators to adopt new, long-term power procurement strategies like multi-decade PPAs to bypass 3-to-5-year grid interconnection queues.

- The primary bottleneck for deploying mature, 100 k W rack technology is no longer internal data center design but external grid availability. Developers face waits of three to five years just to get a new project connected to the grid, rendering traditional development timelines obsolete.

- In response to these delays, a key strategic shift between 2025 and 2026 has been the move away from conventional utility contracts toward long-term Power Purchase Agreements (PPAs). Operators are now signing 10- to 25-year deals to guarantee capacity and stabilize pricing, effectively bypassing the uncertainty of public grid expansion.

- Google’s 21-year PPA in Malaysia to power its data center operations is a prime example of this emerging procurement model. Hyperscalers are increasingly acting as their own energy developers to secure the massive, reliable power blocks their AI infrastructure requires. This is also seen with Meta‘s strategic moves to secure power.

- This procurement evolution confirms that the problem is not a lack of viable server and cooling technology. Instead, the inability of the grid to keep pace has forced the data center industry into the energy sector, fundamentally changing its business model and capital requirements. The high-density hardware from companies like NVIDIA is ready, but the power infrastructure is not.

AI Rack Power Demand to Grow 5x by 2027

The section covers long-term power procurement strategies like 10-year PPAs and grid interconnection queues. The chart quantifies the specific, forward-looking AI demand that necessitates these complex and long-term planning efforts.

(Source: Data Gravity)

SWOT Analysis, Data Center Power Demand vs. Regulatory and Grid Constraints

While insatiable AI-driven demand creates a massive market opportunity for high-density data centers, this strength is directly threatened by grid power limitations and mounting regulatory hostility, which represent the most significant execution risks.

- The core tension for the industry is that its greatest strength, the exponential growth in demand for AI compute, is the direct cause of its greatest threats.

- The analysis shows a clear shift between the two periods. The challenges in 2021-2023 were largely internal and operational, while the challenges of 2024-2025 are external, systemic, and political.

- Opportunities now lie in vertical integration with the energy sector and geographic diversification into regions with less constrained power and more favorable regulatory environments.

AI to Drive Massive Data Center Capacity Growth

This section presents a SWOT analysis. The chart effectively represents the primary ‘Opportunity’ and driving force in the analysis—the massive growth fueled by AI—which must be weighed against regulatory and grid threats.

(Source: Roland Berger)

Table: SWOT Analysis for Data Center Infrastructure Deployment

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong demand for cloud computing; established development models in key markets like Northern Virginia. | Explosive, non-discretionary demand for AI and high-density compute (100 k W+ racks); significant investor appetite from private equity. | Demand shifted from a strong tailwind to an overwhelming force, creating both the market opportunity and its primary constraints. |

| Weaknesses | Long construction timelines; supply chain delays for some components; high water usage effectiveness (WUE). | Extreme dependency on a constrained power grid; development cycles (5+ years) are out of sync with AI hardware cycles (18-24 months). | The critical weakness shifted from construction logistics to the fundamental inability to secure power at the required scale and speed. |

| Opportunities | Securing land in primary markets; improving Power Usage Effectiveness (PUE) through new cooling technologies. | Develop “behind-the-meter” power generation; secure long-term PPAs; geographic diversification to emerging markets with power surplus. | Opportunities shifted from optimizing within the data center to controlling the external energy supply chain. |

| Threats | Competition for land and labor; rising electricity costs in some markets. | Regulatory moratoria and suspension of tax incentives (Illinois); quadrupling of project cancellations from community opposition; grid connection queues of 3-5 years. | Threats evolved from manageable business risks to existential political and infrastructure barriers that can halt projects entirely. |

Data Center Site Selection 2026: If Grid Delays Persist, Watch for On-Site Generation

Given that nearly half of planned U.S. AI data centers are already delayed, the most critical strategic development to watch in the next 12-18 months will be a pivot from grid-dependent projects to those with integrated, behind-the-meter power generation.

- If this happens: Grid interconnection queues remain at 3-5 years, and states like Virginia continue to erect regulatory hurdles and challenge tax exemptions.

- Watch this: A marked increase in announcements for data center projects that explicitly include co-located power generation as a central feature. This will manifest as more partnerships between developers and energy firms and a rise in demand for on-site solutions like the fuel cells offered by Bloom Energy.

- These could be happening: A geographic fragmentation of data center development away from constrained regions like Northern Virginia toward states with more favorable power and regulatory climates. Investors will increasingly favor projects with secured power contracts or integrated generation over those with speculative grid access, changing the risk profile and valuation of development assets.

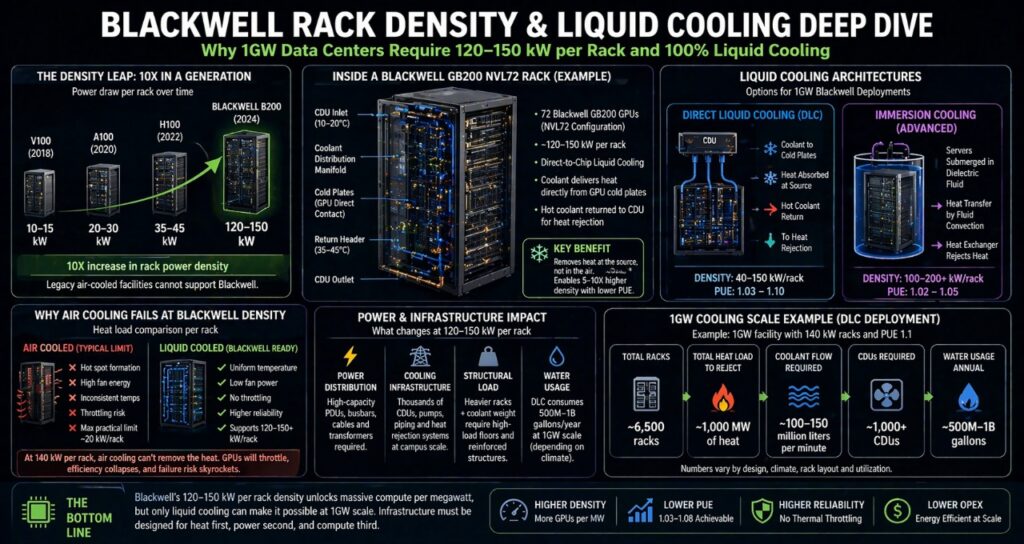

AI Server Racks See 10X Power Density Jump

The section suggests on-site generation as a future solution for grid delays. The chart explains the technical reason why, as the 10x jump in power density at the rack level is what makes traditional grid connections insufficient, justifying radical solutions like on-site power.

(Source: tech plus trends)

The questions your competitors are already asking

This report covers one angle of the systemic risks now blocking high-density AI data center deployment. The questions that matter most depend on your work.

- What is the status of the 7 GW of delayed or canceled AI data center projects?

- What is the outlook for AI data center capacity growth through 2026 amid power grid constraints and 300+ new state bills?

- Which hyperscalers and developers are gaining or losing ground as tax incentives are rolled back?

- Which data center operators are adopting on-site power strategies to bypass grid interconnection queues?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.