Meta DAC Inaction: Strategic Risk as Microsoft Signs 315, 000-Ton Heirloom Deal and Market Nears $1.7 B (2021 to 2026)

Industry Adoption Risk, Meta Lacks DAC Offtakes Amidst Competitor Deals (2021-2026)

Meta’s lack of significant offtake agreements for Direct Air Capture (DAC) places it at a strategic disadvantage as competitors secure long-term carbon removal supply, exposing the company to future price volatility and supply constraints. While Meta has focused on renewable energy procurement, its inaction in the durable Carbon Dioxide Removal (CDR) market contrasts sharply with the proactive strategies of peers like Microsoft, which are actively shaping the market to address their own operational emissions from data centers and AI.

- Between 2021 and 2024, the DAC market was defined by pilot-scale projects, with most corporate engagement focused on small-volume credit purchases to test the technology and signal early demand.

- The period from 2025 to today marks a clear inflection point, with the industry moving toward commercial-scale deployment driven by large, multi-year offtake agreements. Key projects like 1 Point Five’s STRATOS facility, scheduled to begin operations in 2025, are predicated on this secured demand.

- Microsoft’s 10-year agreement with Heirloom to purchase up to 315, 000 tons of CO₂ removal, announced in July 2024, set a new benchmark for corporate procurement, providing the revenue certainty required for project financing.

- SAP followed this trend with a 37, 000-tonne multi-year agreement with Climeworks in July 2025, demonstrating a broadening base of corporate buyers locking in supply.

- Meta’s planned large-scale deployment of AI infrastructure starting in 2026 will substantially increase its carbon footprint, making its current absence from the durable CDR market a critical strategic vulnerability.

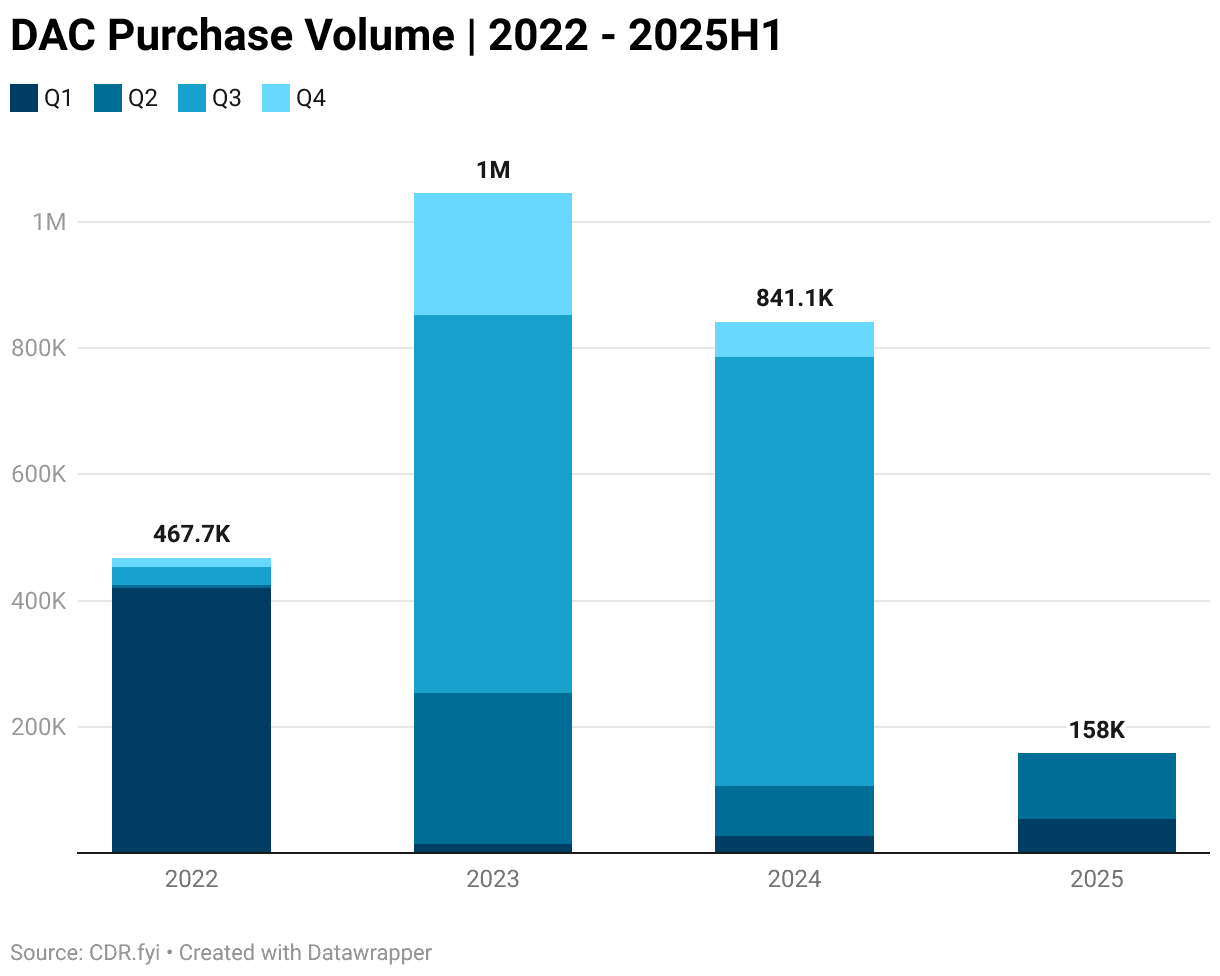

DAC Purchase Volume Peaks in 2023

This chart shows a surge in DAC purchase volume peaking in 2023, visually representing the market activity and competitor deals that Meta is not participating in, which supports the section’s focus on industry adoption risk within the 2021-2026 timeframe.

(Source: CDR.fyi)

$475 M for Heirloom, DAC Investment Surges Without Meta’s Participation

Capital is flowing into the Direct Air Capture market to fund the transition from pilot facilities to first-of-a-kind (FOAK) commercial plants, yet Meta has not been a visible participant in these crucial project-level investments. The significant capital expenditure required for DAC facilities means that project success is highly dependent on both corporate offtake commitments and direct equity investments, a domain where Meta’s competitors are increasingly active.

- In April 2026, Heirloom announced plans to develop two DAC facilities in Louisiana, backed by $475 million in investment, with the first plant targeting a capacity of 17, 000 tons per year.

- Modular DAC developer Aircapture secured a $50 million Series A funding round in June 2025, demonstrating investor confidence in technologies designed for faster, standardized deployment.

- These investments are critical for scaling production and driving down the industry’s high costs, which currently range from $600 to $1, 000 per tonne of CO₂ for commercial-scale operations.

- Microsoft’s Climate Innovation Fund acts as a catalyst, using offtake agreements to de-risk projects and attract the private capital necessary for construction, a strategic financial role Meta has yet to assume.

Table: Notable DAC Investments (2025-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Heirloom | Apr 2026 | Secured $475 Million to develop two DAC facilities in Louisiana. The investment funds the construction of commercial-scale plants, moving the technology from demonstration to industrial application. | Visible.vc |

| Aircapture | Jun 2025 | Raised $50 Million in a Series A funding round. This capital is designated to scale up the manufacturing of its modular DAC systems, enabling faster deployment and cost reductions. | Carbon Credits.com |

| Airhive | May 2025 | Completed a first investment round co-led by AP Ventures and Coca-Cola Europacific Partners. The funding supports the development of its novel fluidization-based DAC technology. | Global Venturing |

Meta Partnership Gap, Microsoft’s 10-Year Heirloom Deal Sets Benchmark (2024-2026)

Meta’s partnership activity in sustainability has been concentrated in renewable energy, failing to build the collaborative supply chain for durable carbon removal that its competitors are actively constructing. The DAC market is being built on a foundation of strategic partnerships between technology developers, energy providers, and corporate offtakers, which collectively de-risk projects and signal long-term market viability.

- Prior to 2024, partnerships were smaller and more exploratory. The period since has been defined by landmark, long-term agreements that provide the revenue certainty needed to finance multi-hundred-million-dollar facilities.

- The July 2024 deal between Microsoft and Heirloom for up to 315, 000 tons of CO₂ removal over 10 years is the primary example of a strategic partnership designed to catalyze commercial scaling.

- In March 2025, EDF Renewables North America partnered with DAC technology provider Skytree to develop a DAC park in Texas, integrating renewable energy generation directly with carbon capture operations.

- SAP’s July 2025 agreement with Climeworks for 37, 000 tonnes of removal highlights a growing trend of major corporations diversifying their CDR portfolios, a strategy Meta has not yet adopted.

Microsoft Dominates CDR Purchases; Meta Lags Far Behind

This chart directly illustrates the section’s headline by comparing Microsoft’s dominant purchasing volume to Meta’s lack thereof. It provides a clear, quantitative visualization of the ‘partnership gap’ and the benchmark set by a key competitor.

(Source: CDR.fyi)

Table: Benchmark DAC Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SAP / Climeworks | Jul 2025 | Multi-year offtake agreement for 37, 000 tonnes of CDR, including DAC. This deal demonstrates corporate demand for a portfolio of high-permanence removal solutions. | CDR.fyi |

| EDF Renewables / Skytree | Mar 2025 | Technology partnership to develop a DAC park in Texas. The collaboration aims to create a blueprint for integrating renewable energy with DAC, addressing the technology’s high energy requirements. | Carbon Herald |

| Microsoft / Heirloom | Jul 2024 | A 10-year offtake agreement for up to 315, 000 tons of CO₂ removal. This landmark contract provides long-term revenue certainty for Heirloom and helps secure financing for its commercial facilities. | Third Way |

US vs. Europe, Meta’s DAC Strategy Lags in Key Policy-Driven Markets

The global DAC market is overwhelmingly concentrated in North America, a direct result of strong policy incentives that Meta is not positioned to leverage due to its inaction. The geographic distribution of DAC projects highlights the critical role of government support in driving investment and deployment, creating a clear strategic imperative to engage in regions with favorable policy frameworks.

- By 2025, North America is projected to account for approximately 91% of global DAC capacity, with 517.7 kt CO₂ per year, compared to just 46.9 kt CO₂ in Europe.

- This dominance is fueled by the U.S. Inflation Reduction Act, specifically the 45 Q tax credit, which provides a direct incentive of up to $180 per ton for CO₂ captured via DAC and permanently stored.

- In the 2021-2024 period, Europe saw early leadership with projects like Climeworks’ Orca plant in Iceland. However, the scale and financial backing of U.S. policy have since shifted the industry’s center of gravity.

- The U.S. Department of Energy’s $3.5 billion investment in regional DAC Hubs further de-risks large-scale projects, creating prime opportunities for corporate partners to co-invest and secure offtake, an opportunity Meta is currently missing.

DAC Technology at Commercial Scale, Meta Sidelined as S-DAC and L-DAC Mature

Direct Air Capture technology is rapidly moving from Technology Readiness Level (TRL) 7 to 9, signifying the transition from pilots to commercially viable systems, yet Meta remains on the sidelines of this critical maturation phase. Both solid sorbent (S-DAC) and liquid solvent (L-DAC) pathways are now being deployed at a large scale, each with distinct operational profiles, cost curves, and leading developers.

- In the 2021-2024 period, the focus was on validating S-DAC technology through modular, pilot-scale plants like Climeworks’ Orca facility, demonstrating operational feasibility.

- Starting in 2025, the market is seeing the first commercial-scale L-DAC plant with 1 Point Five’s STRATOS project, which leverages Carbon Engineering’s technology acquired by Oxy. This project will provide the first real-world data on L-DAC’s costs and performance at scale.

- Heirloom is commercializing a novel S-DAC approach using limestone, which has attracted significant investment and a major offtake agreement from Microsoft, validating its accelerated mineralization process.

- While costs remain high at $600-$1, 000/t CO₂, the operational data from these first-of-a-kind commercial plants is essential for driving down the cost curve toward the industry’s target of under $200/t CO₂.

Infographic Outlines Economics of Flexible DAC Systems

As this section discusses the maturation of DAC technologies toward commercial scale, the infographic provides a specific example of the economic and technical progress being made, illustrating how DAC is becoming a commercially viable technology while Meta is sidelined.

(Source: CarbonCredits.com)

Meta’s Strategic Position, A SWOT Analysis of its DAC Inaction

Meta’s current stance on Direct Air Capture presents a complex mix of latent strengths and mounting external threats. While the company possesses the financial capacity to become a market-moving force, its delayed entry into the durable carbon removal sector creates significant strategic and reputational risks, especially as its operational footprint grows.

- Strengths: Substantial capital reserves for large-scale investments and offtake agreements; extensive experience in securing large-scale renewable energy projects that could be leveraged to power energy-intensive DAC operations.

- Weaknesses: No publicly announced offtake agreements or partnerships with leading DAC developers; a growing carbon footprint from AI data centers that is not yet matched with a credible, high-durability removal strategy.

- Opportunities: Partner with federally de-risked U.S. DAC Hubs to secure cost-advantaged supply; establish a climate innovation fund to accelerate technology and secure equity in promising startups; use its procurement power to help drive down the industry-wide cost curve.

- Threats: Competitors like Microsoft locking up the limited near-term supply of high-quality DAC credits; price inflation for carbon removal as more companies enter the market; policy instability surrounding key incentives like the 45 Q tax credit.

Table: SWOT Analysis for Meta’s DAC Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Massive capital reserves and a public net-zero commitment were key assets. Focus was on renewable energy procurement. | Capital remains a key asset. The 150 MW Sembcorp floating solar partnership shows capability in complex energy projects that could be applied to DAC. | The validation of large-scale renewable projects confirms Meta’s ability to execute energy infrastructure deals, a transferable skill for powering DAC. |

| Weaknesses | Lack of a durable CDR strategy was a minor gap as the market was nascent and peer activity was low. | The gap has become a critical weakness as competitors like Microsoft sign offtake deals for hundreds of thousands of tonnes, and Meta’s AI-driven emissions are set to rise. | Competitor actions and the imminent operational launch of large DAC plants (e.g., STRATOS) have transformed inaction from a passive stance to a clear strategic liability. |

| Opportunities | Opportunity to be an early mover in a small, developing market by signing pilot-scale offtake agreements. | Opportunity to partner with de-risked, large-scale projects like the U.S. DAC Hubs and secure significant volumes of removal credits. | The market has matured enough that Meta can now engage with commercially ready projects and developers like Climeworks and Heirloom, bypassing the earlier, riskier pilot phase. |

| Threats | Main threats were technological immaturity and high costs, with little risk of being left behind. | The primary threat is competitors locking up near-term DAC supply. With only a few megaton-scale projects coming online before 2030, capacity is finite. | The threat has shifted from technology risk to supply chain risk. The “wait and see” approach is no longer viable as the market’s supply becomes constrained by early buyers. |

$1.7 B Market by 2030, Meta’s Scenarios for DAC Engagement

If Meta aims to credibly address the emissions from its 2026 AI infrastructure expansion, it must enter the DAC market with a significant offtake agreement before year-end 2026. The key signal to watch for is a multi-year deal with an established developer like 1 Point Five, Climeworks, or Heirloom for a volume of at least 50, 000 tonnes, which would mark a decisive strategic shift from observer to active participant.

- If this happens, watch for Meta to follow up with a direct investment in a DAC project or the establishment of a dedicated climate fund to mirror Microsoft’s strategy of using capital to accelerate cost reductions and secure supply.

- Another signal could be Meta joining a corporate buyer coalition or announcing a partnership with one of the U.S. Department of Energy’s regional DAC Hubs, leveraging public funding to reduce its own investment risk.

- If Meta remains inactive through 2026, it suggests the company is betting that other, less mature CDR technologies will scale faster or that compliance markets will not mandate high-durability removal, a high-risk assumption given current regulatory trends.

DAC is 1% of a Rapidly Growing CDR Market

This chart provides essential context for the section’s market forecast. By showing DAC as a small but present fraction of the overall, growing CDR market, it effectively frames the ‘$1.7B by 2030’ figure as a significant growth opportunity, underscoring the potential scenarios for Meta’s engagement.

(Source: Carbon Removal Updates – Substack)

The questions your competitors are already asking

This report covers one angle of corporate competition for DAC offtake agreements. The questions that matter most depend on your work.

- Which tech companies are gaining or losing ground in the market for large-scale DAC offtake agreements?

- What is the outlook for DAC price and supply through 2026, following the 315,000-ton Microsoft-Heirloom deal?

- Which DAC suppliers, besides Heirloom and Climeworks, are positioned to fulfill multi-year corporate demand?

- Meta’s activities in durable CDR. Is the company’s procurement progressing fast enough to cover emissions from its large-scale AI deployment?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.