Green Hydrogen Market Correction, $22 B Cancellations, Air Products NY Project Exit, and 59 FIDs (2021 to 2026)

Project Attrition Signals Green Hydrogen Market Correction After 2025

The global green hydrogen sector is undergoing a necessary market rationalization, shifting from a period of hype-driven announcements between 2021 and 2024 to a phase of execution-focused discipline in 2025. This correction is characterized by a significant wave of project cancellations that are filtering out speculative or commercially unviable ventures, forcing the industry to prioritize projects with secured offtake agreements and sound economics. While long-term growth forecasts remain exceptionally strong, the market in 2025 is defined by the clash between this potential and the immediate challenges of cost, demand, and policy stability.

- In the first half of 2025 alone, $22 billion worth of clean energy projects, including many in hydrogen, were cancelled in the U.S., resulting in the loss of an estimated 16, 500 jobs.

- This trend was exemplified by high-profile cancellations, such as Air Products abandoning its $500 million green hydrogen facility in New York in February 2025, citing unfavorable economics and policy uncertainty.

- Analysis of the low-carbon hydrogen project pipeline, which shrank by 25% in 2025, revealed that 48% of cancelled capacity was due to strategic pivots by developers, underscoring a shift away from speculative projects.

- Despite the high rate of attrition, the market is not stalled. The International Energy Agency (IEA) reported that 59 clean hydrogen projects successfully began construction in 2025, indicating that well-structured projects with secured financing and demand are advancing.

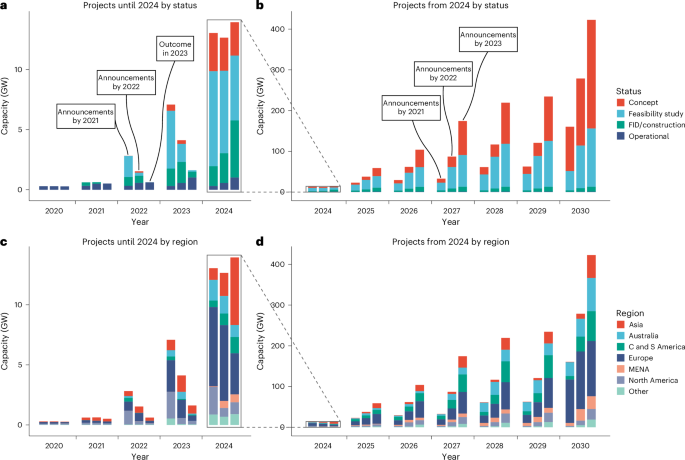

Chart Shows Gap Between Hydrogen Ambition and Reality

The section heading discusses ‘Project Attrition’ and a ‘Market Correction,’ which points to a discrepancy between planned projects and actual execution. This aligns perfectly with the chart’s headline about the ‘Gap Between Hydrogen Ambition and Reality.’

(Source: Nature)

$110 B in Committed Capital, Green Hydrogen Investment Navigates Volatility

Despite a turbulent 2025 marked by project cancellations and policy shifts, the clean hydrogen sector continues to attract and retain significant capital for mature projects, though the criteria for new investment have become far more stringent. The landscape now clearly differentiates between speculative projects, which are being abandoned, and bankable projects with secured offtake and clear economics, which continue to secure financing. This bifurcation signals an investor pivot toward de-risked assets, a trend expected to define the market moving into 2026.

- As of July 2025, over $110 billion in committed investment supports more than 500 global clean hydrogen projects that have passed the Final Investment Decision (FID) stage, forming the first wave of large-scale deployment.

- This committed capital stands in stark contrast to the more than $10 billion in hydrogen projects that were cancelled in July 2025 alone, highlighting the market’s severe correction.

- Strategic reassessments by major players, such as Fortescue Metals Group‘s decision in July 2025 to abandon key hydrogen initiatives as part of a $150 million strategic pivot, illustrate the pressure on companies to focus on core, profitable operations.

- However, overall investment in the clean hydrogen technology space was projected to increase by 70% in 2025 to nearly $8 billion, demonstrating that capital is flowing toward technology development and more viable projects even as the broader pipeline is rationalized.

Table: Key Green Hydrogen Project Cancellations (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fortescue Metals Group | July 2025 | Cancelled key hydrogen projects as part of a $150 million strategic pivot to refocus on its core iron ore business, reflecting shareholder pressure and market challenges. | Discovery Alert |

| Global Project Pipeline | H 1 2025 | Over $22 billion in clean energy projects, including hydrogen, were cancelled in the first half of the year in the U.S., resulting in the loss of 16, 500 jobs. | E 2.org |

| Air Products | February 2025 | Cancelled a planned $500 million green hydrogen production facility in New York, citing a lack of economic viability and policy support. | E&E News |

Green Hydrogen Joint Ventures, Plug Power and Olin Corp Start Production in 2025

In a market where solo ventures face significant hurdles, strategic partnerships that vertically integrate the value chain or secure demand are proving to be a critical success factor. The contrast between cancelled projects and operational joint ventures in 2025 demonstrates that collaborative models are more resilient, effectively de-risking development by combining technological expertise, financial resources, and guaranteed offtake.

- A key success story in 2025 is the joint venture between Plug Power and Olin Corporation, which began producing 15 tons of green hydrogen per day. This partnership leverages Olin‘s chemical production expertise with Plug Power‘s hydrogen technology.

- The Transhydrogen Alliance, a consortium including Proton Ventures, Trammo DMCC, and Varo Energy, announced a $2 billion investment in green hydrogen production facilities, pooling resources to achieve scale.

- The bankability of large-scale projects increasingly relies on such alliances, as lenders require strong, creditworthy partners and long-term offtake agreements, which are often established through these multi-party structures.

Grey Hydrogen Dominates 2025 Market Share

This section discusses new green hydrogen production starting up. The chart provides essential context by showing the incumbent, grey-hydrogen-dominated market that these new green hydrogen ventures are entering and aiming to displace.

(Source: Global Market Insights)

Table: Green Hydrogen Strategic Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power & Olin Corp | October 2025 | A joint venture began operations, producing 15 tons of green hydrogen per day. The partnership creates a secure supply chain and operational efficiency. | Decarbonfuse |

| Transhydrogen Alliance | December 2025 | Consortium of Proton Ventures, Trammo DMCC, and Varo Energy to invest $2 billion in green hydrogen production, combining expertise across the value chain. | Ammonia Energy Association |

US vs. EU, Green Hydrogen Policy Divergence and Market Impact in 2025

Divergent policy approaches in the U.S. and Europe created a complex and uncertain global landscape for green hydrogen investment in 2025. While the U.S. Inflation Reduction Act (IRA) aimed to spur supply through generous tax credits, subsequent legislative changes introduced significant risk. Meanwhile, the EU’s ambitious production targets are running ahead of demand-side policy, creating the potential for a future supply glut.

- The U.S. Section 45 V production tax credit, offering up to $3.00/kg, was the market’s most powerful incentive. However, the passage of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, shortened the eligibility window, injecting significant uncertainty for projects with long development cycles.

- The EU is targeting 10 million metric tons of domestic green hydrogen production by 2030. Yet, demand is projected to be only 3.7 to 7.0 million metric tons by then, creating a risk of oversupply and underutilized assets.

- Germany’s €9 billion National Hydrogen Strategy and India’s $60 billion incentive ecosystem demonstrate that nations are actively competing to establish production hubs, though the lack of coordinated global demand remains a key challenge.

Electrolyzer TRL, Green Hydrogen Focuses on Mature ALK and PEM Tech

The green hydrogen market in 2025 and 2026 is heavily reliant on commercially mature electrolyzer technologies to move projects from announcement to operation. While emerging technologies promise future cost reductions, the current wave of projects reaching FID is built on proven Alkaline (ALK) and Proton Exchange Membrane (PEM) systems, both of which are at Technology Readiness Level (TRL) 9.

- ALK and PEM electrolysis are considered fully commercialized (TRL 9), providing the technological backbone for projects currently under construction. ALK offers lower capital costs, while PEM provides greater operational flexibility to pair with variable renewables.

- Solid Oxide Electrolysis (SOE), such as the technology developed by Bloom Energy, is also at a high readiness level (TRL 8-9) and is being deployed in early commercial projects, valued for its high electrical efficiency, especially when integrated with industrial heat sources.

- Anion Exchange Membrane (AEM) electrolysis remains at a lower readiness level (TRL 4-6) but is a key area of research. It aims to combine the low-cost materials of ALK with the high performance of PEM, representing a critical pathway for future cost reductions.

- The primary barrier to widespread adoption remains the levelized cost, which ranges from $3.00 to $6.00 per kg for green hydrogen, compared to just $1.00 to $2.00 per kg for grey hydrogen. This cost gap underscores the industry’s dependence on subsidies and technological advancement.

Wind Power Leads Green Hydrogen Production in 2025

While the section focuses on electrolyzer technology (TRL, ALK, PEM), the chart complements this by illustrating the primary energy source (‘Wind Power’) for production. The energy source is a critical component of the overall green hydrogen production technology stack.

(Source: Precedence Research)

SWOT Analysis of the Green Hydrogen Market in 2025

The green hydrogen market’s fundamental strength lies in its alignment with global decarbonization mandates, backed by substantial policy support in key regions. However, this is significantly undermined by a persistent cost gap with fossil-fuel alternatives and a critical lack of guaranteed offtake, creating a high-risk environment that led to the market correction of 2025.

- Strengths are rooted in policy, with incentives like the U.S. IRA and the EU Green Deal providing a powerful financial backstop for the industry.

- Weaknesses are commercial, primarily the high production cost and the difficulty for projects to secure the bankable, long-term offtake agreements needed to obtain project financing.

- Opportunities for growth are tied to technological breakthroughs that lower costs and the successful creation of new demand centers in hard-to-abate sectors like shipping and aviation.

- Threats are largely external, including the risk of policy reversal due to political shifts and continued price volatility for the renewable electricity that underpins production costs.

Green Hydrogen Market Forecasts Explosive Growth

A SWOT analysis framework includes ‘Opportunities.’ A chart forecasting ‘Explosive Growth’ is a direct and powerful visual representation of the significant market opportunity discussed in such an analysis.

(Source: Mordor Intelligence)

Table: SWOT Analysis for the Global Green Hydrogen Market

| SWOT Category | 2021 – 2024 (Hype Phase) | 2025 – Today (Correction Phase) | What Changed / Validated |

|---|---|---|---|

| Strengths | Massive project announcements and ambitious government targets. High investor enthusiasm based on long-term potential. | Strong policy incentives (IRA $3/kg credit) are now codified in regulations. A core of well-structured projects (59) have reached FID and started construction. | The strength shifted from announcements to tangible, albeit fewer, projects backed by real policy mechanisms. |

| Weaknesses | High projected costs were often downplayed. The challenge of securing offtake agreements was underestimated. | High production costs ($3.50-$12/kg) became a primary reason for project cancellations. The lack of bankable offtake is now cited as the main barrier to FIDs. | The weakness of project economics without subsidies or guaranteed demand was validated by the wave of cancellations. |

| Opportunities | The narrative focused on replacing all grey hydrogen and expanding into all energy sectors simultaneously. | Focus is narrowing to high-value applications (refining, ammonia) where hydrogen is an existing feedstock and a premium can be justified. | The opportunity has become more focused and pragmatic, prioritizing applications with a clearer business case over broad, aspirational goals. |

| Threats | Policy risk was a known but distant concern. Permitting and grid connection were seen as procedural hurdles. | Policy risk became reality with the U.S. OBBBA legislation altering IRA timelines. Project delays and cancellations are now directly attributed to these external factors. | The threat of political and regulatory instability has been validated as an immediate and material risk to project viability. |

The 2026 Outlook, Green Hydrogen Shifts to Bankable Offtake Agreements

The defining metric for the green hydrogen market’s health moving into 2026 will be the velocity and volume of long-term, bankable offtake agreements. Following the market correction of 2025, the industry has shifted from a supply-push model, driven by production targets, to a demand-pull model, where project viability is dictated by secured revenue streams. The ability to lock in these contracts will be the primary determinant of which projects advance to FID.

- If developers can successfully negotiate more “take-or-pay” contracts for green hydrogen and its derivatives, watch for an increase in projects reaching FID, particularly those that have already completed permitting.

- If policy instability persists, especially around the U.S. IRA credits, watch for continued investment hesitation and a potential flight of capital to regions with more stable, long-term regulatory frameworks.

- If the cost of key technologies, particularly next-generation electrolyzers like AEM, demonstrates a faster-than-expected reduction curve in pilot projects, this could accelerate timelines for cost parity and trigger a new wave of investment.

Green Hydrogen Pipeline Swells with Speculative Projects

The section discusses a future ‘shift to bankable offtake agreements.’ The chart, which highlights a pipeline of ‘speculative projects,’ perfectly illustrates the current market state that necessitates this strategic shift, providing the ‘before’ to the section’s ‘after’.

(Source: Nature)

The questions your competitors are already asking

This report covers one angle of the commercial realities shaping the 2025 green hydrogen project pipeline. The questions that matter most depend on your work.

- Which developers are gaining ground by securing offtake, and which are losing ground amid the 2025 green hydrogen market correction?

- What is the status of the 59 green hydrogen projects that reached FID in 2025, and what separates them from the projects that were cancelled?

- After Air Products’ exit from its $500 million New York facility, what are the new economic and policy benchmarks for a viable green hydrogen investment?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.