SOFC Data Center Deals, $7.65 B in Contracts, $7 B Tallgrass Investment, and Bloom Energy’s Crusoe Partnership (2025 to 2026)

SOFC Commercial Scale, Bloom Energy Projects Shift to Data Centers

Solid Oxide Fuel Cells (SOFCs) have pivoted from niche, high-reliability markets to become a primary power solution for data centers, driven by an urgent need to bypass grid connection delays that threaten the expansion of artificial intelligence. This transition is not an incremental change but a strategic market response to a severe power infrastructure bottleneck, where SOFCs’ rapid deployment time offers a decisive advantage over traditional power sources.

- Between 2021 and 2024, SOFC technology was validated in demanding maritime and military applications. These sectors proved the technology’s high efficiency and reliability under harsh conditions, but deployments were generally smaller-scale, such as pilot projects aimed at decarbonizing shipping or providing robust power for defense operations.

- Starting in 2025, the market dynamic shifted dramatically. The AI boom created a power demand crisis that existing infrastructure could not meet. The “time arbitrage” of SOFCs became the primary value proposition; systems can be deployed in under a year, while grid expansion takes five to seven years and order books for gas turbines are full through 2029.

- This shift is quantified by the surge in commercial activity. Bloom Energy, a leading provider, now supplies over 400 MW of power to data centers, and the industry saw $7.65 billion in data center fuel cell deals in the first 90 days of 2026 alone, indicating a full-scale commercial crossover into mission-critical digital infrastructure.

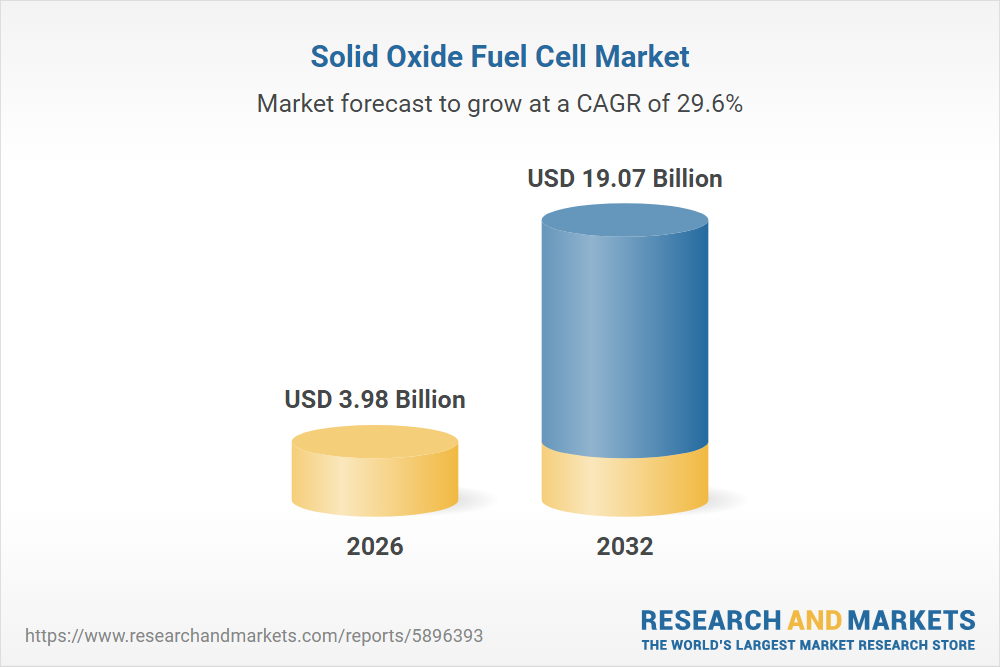

SOFC Market to Reach $19B by 2032

The section discusses SOFCs achieving ‘Commercial Scale’ through a shift to data centers. A chart projecting the market to reach a substantial size, such as $19 billion, provides a quantitative definition for this ‘scale’ and illustrates the magnitude of the commercial opportunity being pursued.

(Source: Research and Markets)

$7.65 B in Deals, SOFC Investment for AI Power Demand

The AI-driven power deficit has triggered a massive influx of capital into SOFC solutions, with investments now measured in the billions for single projects and infrastructure build-outs. This marks a transition from venture-style funding for technology development to large-scale project finance for mature, bankable assets.

- Prior to 2025, investments were largely directed toward research, development, and smaller pilot projects aimed at improving durability and reducing costs, often supported by government grants.

- The period from 2025 to 2026 saw a financial inflection point. The $7.65 billion in data center deals secured in early 2026 highlights the scale of capital now flowing into the sector to solve an immediate power shortage.

- A landmark deal involves Tallgrass funding $7 billion of power infrastructure for Crusoe‘s data centers, which will be powered in part by SOFCs from Bloom Energy. This demonstrates a new model where infrastructure funds directly back fuel cell deployments.

- However, project execution risk remains a material concern. The termination of Topsoe‘s 100 MW SOEC supply agreement with First Ammonia on March 26, 2026, due to missed project milestones, serves as a reminder that large-scale energy projects carry significant delivery risk.

Fuel Cells Pivot to AI and Data Centers

The section headline specifies that investments are being driven by ‘AI Power Demand’. The chart’s headline, ‘Fuel Cells Pivot to AI and Data Centers’, directly mirrors this theme, providing a clear visual confirmation of the strategic trend that is attracting billions in investment.

(Source: MarketsandMarkets)

Table: SOFC Investment and Cancellation Highlights (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Crusoe / Tallgrass / Bloom Energy | April 2026 | Tallgrass to fund $7 billion in power infrastructure for Crusoe‘s AI data centers, which will utilize Bloom Energy SOFCs. This validates SOFCs as a bankable, large-scale infrastructure asset class for institutional investors. | Substack |

| Topsoe / First Ammonia | March 2026 | Topsoe terminated its 100 MW SOEC supply agreements due to First Ammonia‘s failure to meet project milestones. This highlights project execution and counterparty risk in the clean energy sector. | decarbonfuse.com |

| Data Center Sector Deals | Q 1 2026 | Fuel cell providers secured $7.65 billion in data center deals in the first 90 days of 2026, demonstrating the extreme urgency for on-site power solutions to support AI growth. | Introl Blog |

Bloom Energy’s Crusoe and Centrica Alliances for Data Centers (2025 to 2026)

Strategic partnerships between SOFC manufacturers, infrastructure funds, and data center operators are forming to de-risk and accelerate the deployment of on-site power at scale. These new commercial ecosystems are designed to deliver complete, funded solutions rather than just technology components.

- Between 2021 and 2024, partnerships were often technology-focused, such as the former deal between Ceres Power and Bosch, which aimed at joint development and manufacturing scale-up. These were crucial for maturing the technology but were not direct commercial deployment vehicles.

- The 2025-2026 period is defined by vertically integrated commercial partnerships. The Crusoe / Tallgrass / Bloom Energy alliance is a prime example, combining a data center operator, a capital provider, and a technology supplier to deliver a full-stack, financed power solution.

- This trend is also visible in Europe. In April 2026, Centrica and Delta Electronics announced an infrastructure partnership to serve the data center market in the UK and Europe, leveraging SOFC technology to address similar power constraints.

- In December 2025, Power Cell entered an agreement with a US-based data center leader to pilot hydrogen fuel cell systems, showing that other fuel cell types are also competing for this market through strategic partnerships.

Fuel Cell Market to Exceed $18B by 2030

The section details specific strategic ‘Alliances’ being formed. This chart, showing the large size of the broader fuel cell market, provides the financial rationale and strategic context for why companies are forming partnerships to secure a position and capitalize on this significant market opportunity.

(Source: MarketsandMarkets)

Table: Key SOFC Strategic Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Centrica / Delta Electronics | April 2026 | Infrastructure partnership to serve the data center and other energy-intensive industries in the UK and Europe, leveraging SOFC technology to provide reliable power. | Datacenter-Technology |

| Crusoe / Tallgrass / Bloom Energy | April 2026 | A three-way partnership to build and power AI data centers. Crusoe operates, Tallgrass provides $7 billion in funding, and Bloom Energy supplies the SOFC power technology. | Substack |

| Power Cell / US Data Center Leader | December 2025 | Agreement to pilot hydrogen fuel cell systems for power solutions, with the pilot starting in Q 1 2026. This signals competition from other fuel cell chemistries in the data center market. | Fuel Cells Works |

| Fuel Cell Energy / MHB | March 2025 | Joint Development Agreement with Malaysia Marine and Heavy Engineering Holdings Berhad (MHB) to explore low-carbon fuel production using SOEC technology, showing continued activity in other sectors. | Hydrogen Technologies |

US vs. Europe, Bloom Energy SOFC Data Center Deployments

While SOFC development has been global, the United States has emerged as the unequivocal center of gravity for large-scale data center deployments, driven by the intense concentration of AI development and supportive, albeit volatile, policy incentives.

- From 2021 to 2024, market development was more distributed. Europe showed strong interest in SOFCs for maritime decarbonization, supported by EU targets, while Asian players like Doosan Fuel Cell focused on stationary power markets in their home regions.

- Since 2025, the United States has become the primary market for SOFCs in data centers. The extreme power demand from Silicon Valley and other tech hubs, combined with grid congestion, has made on-site generation a necessity. The financial incentives of the Investment Tax Credit (ITC) further strengthen the business case.

- The largest announced deals, including the Bloom Energy projects with Crusoe and others, are located in the US. This geographic concentration is a direct result of where the AI-driven power crunch is most acute.

- Europe is beginning to follow, as evidenced by the Centrica / Delta Electronics partnership. However, the scale and velocity of announced projects in the UK and EU currently lag behind the US market.

SOFC Technology Readiness, Bloom Energy Validates 99.999% Uptime

SOFC technology has crossed a critical maturity threshold, now proven capable of meeting the “five nines” reliability standard required for mission-critical data center primary power, transitioning it from a promising alternative to a commercially viable core solution.

- Between 2021 and 2024, SOFCs’ viability was established in marine and military settings. While these applications demanded high reliability, the operational profile differs from the 24/7, high-load factor requirements of data centers. Lingering questions remained around long-term degradation and capital cost.

- The period from 2025 to today has provided validation of the technology’s readiness for this new role. Companies like Bloom Energy have surpassed 1, 300 MW of installed stationary capacity, providing a deep well of operational data.

- The ability to meet “five nines” (99.999%) availability, a standard highlighted by Ceres Power, is what allows data center operators to trust SOFCs for primary power, not just as a replacement for diesel backup generators.

- Technical advantages like high electrical efficiency (50-60% for SOFCs vs. 35-45% for gas turbines) are now proven at scale. Remaining challenges related to high-temperature materials and rare earth supply chains are now being addressed as engineering and supply chain management problems, not fundamental research questions.

SOFC Market To Reach $12.5 Billion By 2032

The section focuses on ‘Technology Readiness’ and validated high uptime. This technical maturity is a key enabler for market adoption. The chart, forecasting a multi-billion dollar market, demonstrates the commercial success and scale that is predicated on the technology being reliable and ready for deployment.

(Source: Verified Market Research)

Bloom Energy SWOT, SOFC Market Strengths and Policy Risks

The market for Solid Oxide Fuel Cells is defined by a strong set of internal capabilities and external opportunities, particularly around the AI-driven power demand, but it also faces significant risks from policy uncertainty and technical execution challenges.

- Strengths: The primary strength of SOFCs is their unique combination of high electrical efficiency, fuel flexibility, and, most critically, rapid deployment capability (“time arbitrage”), which directly addresses the data center power bottleneck.

- Weaknesses: SOFCs still have a higher initial capital cost compared to some traditional technologies, and their high operating temperatures create material science challenges that impact long-term durability.

- Opportunities: The unprecedented power demand from AI and the slow pace of grid expansion create a massive market opportunity. US tax incentives, like the 30% ITC, provide a powerful financial tailwind.

- Threats: Policy volatility, such as the 2025 revocation of $7.5 billion in DOE funding by the Trump administration, creates significant uncertainty. Competition from other technologies and supply chain risks for critical materials also pose threats.

SOFC Market to Reach $32.14B by 2034

A SWOT analysis, as mentioned in the section heading, evaluates Strengths, Weaknesses, Opportunities, and Threats. This chart’s projection of a massive $32.14B market serves as a powerful and direct illustration of the ‘Opportunity’ aspect of the SOFC market’s SWOT profile.

(Source: Precedence Research)

Table: SWOT Analysis for SOFCs in the Data Center Market

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High efficiency and low emissions were key selling points in niche markets (marine, industrial CHP). Reliability was proven in pilots. | Rapid deployment (<1 year) becomes the dominant strength, offering "time arbitrage" over grid (5-7 years). High reliability is now validated at scale for data center uptime. | The value of deployment speed was validated as the primary driver for adoption in the time-sensitive AI infrastructure race. |

| Weaknesses | High capital cost (CAPEX) was a major barrier to widespread adoption. Concerns over long-term stack degradation and durability. | CAPEX remains higher than some alternatives, but is increasingly justified by the cost of grid delays. Material stability at high temperatures is an ongoing engineering challenge. | The urgency of the power crisis has reframed the cost calculation, making the higher CAPEX acceptable to avoid multi-year revenue delays. |

| Opportunities | Decarbonization goals and government R&D funding. Application in industrial and commercial sectors for grid stability. | The AI power crisis creates a massive, urgent demand for on-site power. The US Investment Tax Credit (ITC) provides a 30% credit, significantly improving project economics. | A massive, multi-billion dollar market (data centers) emerged that was willing to pay a premium for speed and reliability, validating the technology’s commercial potential. |

| Threats | Competition from other clean energy sources like batteries and PEM fuel cells. Slow development of hydrogen infrastructure. | Policy volatility, demonstrated by the Trump administration’s rollback of clean energy funding in October 2025. Supply chain risks for rare earth materials. | The threat of policy reversal became a tangible risk, highlighting the danger of depending solely on government incentives for long-term growth. |

SOFC 2026 Outlook, Bloom Energy’s Project Execution is Key

The central variable for the SOFC market in the next 18 months is execution, as the industry must now deliver on billions of dollars in signed contracts to maintain credibility and momentum. The conversation has decisively shifted from technological possibility to industrial delivery.

- If SOFC manufacturers like Bloom Energy successfully execute on the massive backlog of orders, such as the $7.65 billion in deals announced in early 2026, it will cement the technology’s role as a cornerstone of data center infrastructure and trigger another wave of investment.

- Watch for signals of manufacturing capacity expansion and supply chain de-risking from market leaders. The ability to produce and install systems at the promised speed and scale is the most critical metric.

- These could be happening now: project delays, cost overruns, or a failure to meet performance guarantees on these first large-scale deployments could quickly damage market confidence and open the door for competing technologies. The Topsoe / First Ammonia contract termination is a clear warning about the operational risks inherent in rapidly scaling new energy technologies.

SOFC Market to See 24.5% Annual Growth

The section discusses the future ‘Outlook’ for the SOFC market. A chart illustrating a strong compound annual growth rate (CAGR) of 24.5% directly quantifies this positive outlook and provides a clear visual for the market’s expected trajectory.

(Source: Research Nester)

The questions your competitors are already asking

This report covers one angle of the Solid Oxide Fuel Cell market’s pivot to data center primary power. The questions that matter most depend on your work.

- What is the outlook for SOFC deployment in AI data centers by 2030?

- Which data center operators are adopting on-site SOFC power?

- What is the status of the $7 B Tallgrass investment and the Bloom Energy-Crusoe partnership?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.