Advanced Reactor PPAs, Kairos Power’s Google Deal, $303 M Award, and Talen Energy’s 960 MW AWS Project (2021 to 2026)

Nuclear Project Bankability: From Government Support to Corporate PPAs

The commercial model for new nuclear projects has fundamentally shifted from a near-total reliance on government subsidies and utility rate-basing to a new structure anchored by direct, bankable power purchase agreements (PPAs) with large corporations, particularly data center operators. This change mitigates the financing risk that stalled previous projects by providing a guaranteed revenue stream from credit-worthy offtakers willing to pay a premium for reliable, carbon-free power.

- Between 2021 and 2024, the viability of new nuclear hinged on government programs like the U.S. Department of Energy’s Advanced Reactor Demonstration Program (ARDP) and tax credits from the Inflation Reduction Act. The commercial failure of Nu Scale Power’s Carbon Free Power Project (CFPP) in late 2023, which was canceled after failing to secure enough utility subscribers amid rising costs, exposed the weakness of the traditional utility-centric model for first-of-a-kind (FOAK) projects.

- The landscape transformed in 2025 with a landmark PPA involving Kairos Power, the Tennessee Valley Authority (TVA), and Google. This agreement, the first in the U.S. for a Generation IV reactor, established a new template where a utility acts as an intermediary to supply advanced nuclear power directly to a corporate customer. This structure provides the revenue certainty that was missing from earlier projects.

- This model was reinforced by direct-sourcing agreements. In May 2026, Talen Energy announced it would provide up to 960 MW of power from its Susquehanna nuclear plant to an adjacent data center campus for Amazon Web Services (AWS). This co-location strategy physically and contractually links a nuclear asset to a specific large-scale energy user, creating a self-contained, highly reliable energy ecosystem.

- The new U.S. policy environment, shaped by the 2025 “One Big Beautiful Bill Act” (OBBBA), further supports this trend by preserving key production tax credits for nuclear energy while streamlining the licensing process. This provides a stable policy foundation for developers to secure long-term corporate contracts.

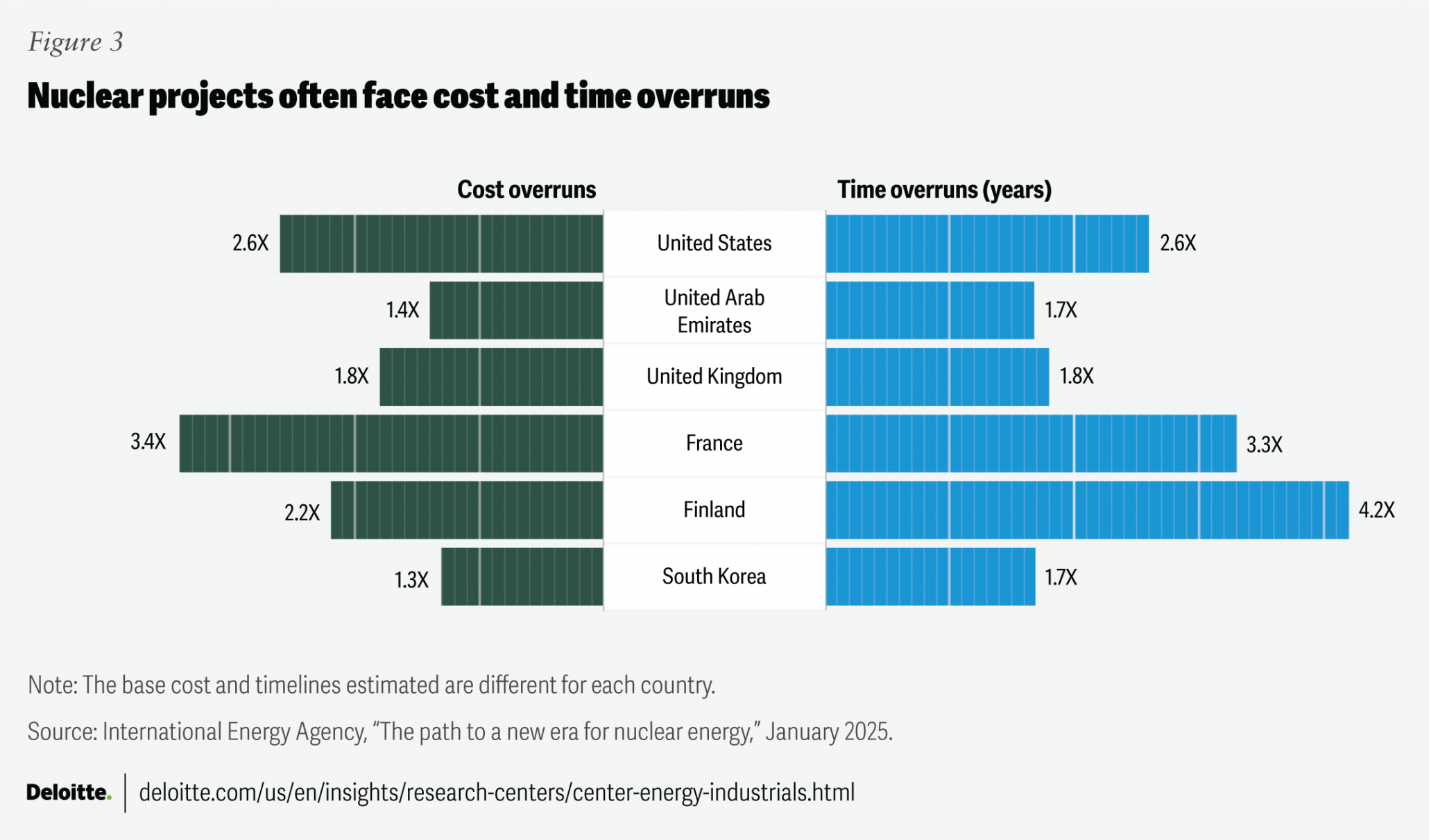

Nuclear Projects Suffer Major Cost and Time Overruns

This chart directly illustrates a primary obstacle to project bankability—significant cost and time overruns. This supports the section’s focus on the financial viability and investment risks of new nuclear projects.

(Source: Deloitte)

$610 M in New Funding: Radiant, Hadron, and Kairos Power Secure Capital

Targeted investments are flowing into advanced reactor companies that demonstrate a clear and viable path to commercialization, either through innovative technology applications or by securing project sites and offtake agreements. This shift from broad R&D funding to focused project-level financing signals growing investor confidence in the new commercial models for nuclear energy.

- In December 2025, Radiant, a developer of portable microreactors, announced it had raised over $300 million in new funding. This capital is aimed at mass-producing its 1 MW Kaleidos high-temperature gas-cooled reactor, targeting off-grid industrial, remote community, and military applications, a different market segment from grid-scale power.

- Project development firm Hadron Energy completed a $7.5 million pre-IPO equity financing round in April 2026. The investment, coupled with a multi-project MOU with Smartland, is intended to advance development at sites including the V.C. Summer location in South Carolina, indicating a strategy focused on preparing pre-licensed sites for future reactor deployments.

- Kairos Power received a $303 million federal award from the DOE, a key development announced in August 2025. This government funding serves as a crucial de-risking tool that complements private investment by covering a portion of the high upfront costs associated with FOAK reactor construction, making the project more attractive for private financing and corporate offtakers like Google.

Table: Key Nuclear Power Investments and Awards (2025-2026)

| Company / Project | Time Frame | Value and Strategic Purpose | Source |

|---|---|---|---|

| Hadron Energy / Smartland | Apr 2026 | Secured $7.5 million in pre-IPO equity and a multi-project MOU to advance development at nuclear-ready sites. This model focuses on site preparation to reduce lead times for future reactor projects. | Yahoo Finance |

| Radiant | Dec 2025 | Raised over $300 million in new funding to mass-produce its Kaleidos portable microreactor. The capital supports a factory-based production model for military and commercial markets. | Radiant |

| Kairos Power / TVA / Google | Aug 2025 | Received a $303 million federal award to support the construction of its Hermes demonstration reactor. This government funding was critical for de-risking the project and enabling the landmark PPA with TVA and Google. | POWER Magazine |

US vs. China: A Diverging Path to Nuclear Deployment and Commercialization

While China continues to dominate global nuclear expansion through a state-led strategy of deploying large-scale, standardized reactors, the United States is pioneering a market-driven commercialization model for advanced reactors fueled by private sector demand from the AI and data center industries. This divergence reflects two distinct approaches to achieving energy security and decarbonization goals.

- Between 2021 and 2024, China’s state-owned enterprises like CNNC and CGN consistently added new reactors to the grid, primarily their indigenous Hualong One design. During the same period, the U.S. focused on completing the long-delayed and costly Vogtle Units 3 & 4, the only new large-scale reactors to come online in the country in decades.

- The period from 2025 to today highlights the new U.S. approach. Private-sector demand is driving projects like Kairos Power’s Hermes reactor in Tennessee, Talen Energy’s data center project in Pennsylvania, and X-energy’s planned SMR for Dow’s Texas facility. This contrasts with China’s ongoing, state-financed construction pipeline of over 20 reactors.

- Canada is pursuing a similar path to the U.S., with Ontario Power Generation (OPG) advancing the Darlington SMR project, which aims to be North America’s first commercial, grid-scale SMR. The selection of GE Hitachi’s BWRX-300 for this site demonstrates a North American focus on leveraging SMR technology for grid modernization.

- Meanwhile, the United Kingdom’s experience with the Hinkley Point C and Sizewell C projects, which have faced significant delays and financing challenges, underscores the difficulties of executing large-scale nuclear builds in Western markets without the direct offtake agreements now emerging in the U.S.

China Dominates Future Nuclear Power Construction

This chart visually represents the ‘diverging path’ mentioned in the section title by showing China’s massive lead in new construction, a core element of its deployment strategy compared to the US.

(Source: Visual Capitalist)

Advanced Reactor Commercialization: From Demonstration to Bankable Projects

Advanced reactor technology is making a critical transition from the government-funded demonstration phase to the initial stage of commercialization, validated by the first bankable PPAs from corporate buyers. This progression confirms that while the technology is maturing, its commercial viability is ultimately determined by its ability to secure long-term revenue contracts.

- The 2021-2024 period was defined by regulatory progress and federal support. Key milestones included Nu Scale Power receiving the first-ever SMR design approval from the U.S. Nuclear Regulatory Commission and companies like Terra Power and X-energy securing ARDP funding. However, the technology was not yet commercially bankable, as proven by the cancellation of the Nu Scale UAMPS project due to cost concerns and a lack of firm subscribers.

- The definitive validation point arrived in 2025 with the Kairos Power PPA for its fluoride salt-cooled high-temperature reactor (KP-FHR). This agreement demonstrated that a Generation IV reactor design could secure a commercial contract, shifting the conversation from technical feasibility to economic reality.

- Other designs are also moving toward commercial application. X-energy is progressing with its Xe-100 high-temperature gas-cooled reactor (HTGR) to provide process heat for Dow, and Radiant’s recent $300 million funding round advances its portable HTGR for specialized industrial markets. These projects show a diversification of applications beyond just grid electricity.

- Although the unsubsidized Levelized Cost of Energy (LCOE) for FOAK SMRs remains high at a projected $180/MWh, tech companies’ willingness to pay a premium for 24/7 carbon-free power is creating a viable market. This demand effectively subsidizes the higher cost of initial projects, paving the way for future cost reductions through scaled production.

Nuclear Market to Reach $44.71B by 2029

This chart provides a forward-looking market size projection, quantifying the commercial potential discussed in the section. It connects the concept of commercialization to a tangible financial forecast.

(Source: MarketsandMarkets)

SWOT Analysis: AI Demand Drives Nuclear Growth Amid Cost and Supply Chain Risks

A surge in electricity demand from AI, coupled with supportive policy shifts, has created strong tailwinds for nuclear power, but persistent challenges in cost-competitiveness, supply chain capacity, and project execution risk remain significant threats. The industry’s ability to capitalize on new opportunities depends on its capacity to mitigate these long-standing weaknesses.

- Strengths have been reinforced as nuclear’s value proposition of reliable, carbon-free baseload power is now highly sought after by data centers.

- Weaknesses around high costs and long construction timelines persist, but the new commercial models with corporate PPAs are providing a path to overcome them.

- Opportunities have expanded dramatically with the AI electricity boom and new policy support, creating a powerful demand-pull for new reactor technologies.

- Threats are intensifying in the supply chain, as a global build-out could create bottlenecks, while new rules on fuel sourcing add geopolitical complexity.

Nuclear Fuel Shows Drastically Lower CO2 Emissions

This chart highlights a key ‘Strength’ in the SWOT analysis: the low carbon footprint of nuclear power. This environmental advantage is a primary driver for the ‘Opportunity’ of meeting AI-driven energy demand, as mentioned in the section heading.

(Source: Tema ETFs)

Table: SWOT Analysis for Nuclear Power Commercialization

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Provided 24/7 carbon-free power. Existing fleet seen as a key decarbonization asset. | High capacity factor and reliability are now seen as essential for powering AI and data centers, creating a “premium” product attribute. | The inherent reliability of nuclear power shifted from a grid-level benefit to a bankable commercial advantage sought by specific high-demand customers like Google and AWS. |

| Weaknesses | High LCOE ($141-$221/MWh) compared to renewables. Long, uncertain construction timelines (e.g., Vogtle project delays). | FOAK SMR costs remain high (est. $180/MWh). Financing is still dependent on government de-risking and long-term contracts. | The core weakness of high cost was not eliminated but was successfully bypassed in specific projects where customers are willing to pay a premium for firm power, as seen in the Kairos Power PPA. |

| Opportunities | Government incentives like the Inflation Reduction Act (IRA) provided tax credits. DOE’s ARDP funded demonstration projects. | Massive electricity demand growth from AI (projected 1, 050 TWh globally by 2026). New policy support via the OBBBA and streamlined NRC licensing. | The primary opportunity shifted from being policy-driven (supply-push) to market-driven (demand-pull), with tech companies actively seeking nuclear power solutions. |

| Threats | Project cost overruns and cancellations (Nu Scale’s CFPP). Supply chain bottlenecks for specialized components. Reliance on Russian enriched uranium. | Intensifying supply chain constraints for forgings and components. OBBBA’s “Foreign Entity of Concern” (FEOC) rules create new fuel sourcing risks after 2027. | Geopolitical risk became codified in U.S. policy via the OBBBA, forcing a strategic realignment of the nuclear fuel supply chain and favoring Western suppliers like Orano. |

Kairos Power 2026 Outlook: The Race to Replicate the Google PPA Model

The critical test for the U.S. nuclear renaissance in the next 12-24 months is whether the landmark Kairos Power-TVA-Google PPA can be replicated by other advanced reactor developers and corporate offtakers. Success would validate a new, market-driven financing model for advanced nuclear, while failure would suggest it was a one-off deal, pushing the industry back toward a reliance on government subsidies.

- If this happens, other major technology and industrial companies will sign firm, long-term PPAs for advanced nuclear power, creating a visible and competitive project pipeline.

- Watch this: Announcements from developers like X-energy or Terra Power securing a firm commercial contract for their first commercial units, moving beyond government-funded demonstrations to fully bankable projects. The structure of these deals will reveal whether the three-way utility-developer-customer model becomes the industry standard.

- Watch this: The reaction of financial markets. A second or third major PPA could unlock significant private capital from infrastructure funds and institutional investors, reducing the sector’s dependence on government loan guarantees and demonstrating a clear path to profitability for advanced nuclear technologies.

- These could be happening: Utilities may begin to structure and market “green data center” tariffs or dedicated power blocks. These new products would blend firm nuclear power with intermittent renewables, offering large tech customers a complete, reliable, and carbon-free energy solution that addresses the high costs of grid firming services, a growing challenge for operators like the National Grid.

The questions your competitors are already asking

This report covers one angle of the commercial model for new nuclear projects. The questions that matter most depend on your work.

- Which advanced nuclear companies are gaining or losing ground in the new PPA-driven market?

- What is the outlook for advanced reactor deployment in the data center sector by 2030?

- What is actually happening with Talen Energy’s 960 MW project for the AWS data center campus?

- Which data center operators, besides Google and Amazon, are adopting nuclear power solutions?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.