SMR Maritime Adoption, $7.14 B Market by 2030, 1 HD Hyundai Pilot, and 5-Year Allseas Goal (2021 to 2026)

SMR Maritime Projects, Allseas 5-Year Pilot and HD Hyundai Design Approval

The maritime industry’s interest in Small Modular Reactors (SMRs) has advanced from conceptual discussions before 2025 to active design and development projects today, driven by stringent decarbonization mandates. However, commercial adoption remains over a decade away, constrained by immature technology, high costs, and the absence of a global regulatory framework.

- Before 2025, nuclear propulsion was largely a theoretical solution discussed in industry papers. Post-2025 activity shows a clear shift, with offshore services company Allseas announcing a plan to deploy a marine-compatible SMR on a vessel within five years.

- Major shipbuilders are now committing resources to specific designs. HD Hyundai is designing a container ship powered by a 100 MW reactor, signaling a move toward integrating SMRs into high-value commercial vessels.

- Early adopters are focusing on advanced reactor types with enhanced safety profiles. Tanker operator Scorpio Tankers is actively exploring Molten Salt Reactors (MSRs), indicating a preference for Generation-IV technologies over scaled-down traditional designs for commercial use.

- The broader SMR market momentum, supported by demand from data centers run by firms like Microsoft and AWS, provides the industrial base necessary for maritime developers to leverage.

$7.14 B SMR Market Forecast, Maritime Sector Eyes High CAPEX vs. OPEX Gains

While the overall SMR market shows steady growth projections, direct investment in maritime nuclear projects is limited to early-stage design and feasibility studies, as high capital expenditure remains the primary deterrent to near-term financing. The business case for shipping lines is entirely dependent on a future with high carbon pricing and a significant cost reduction in reactor manufacturing.

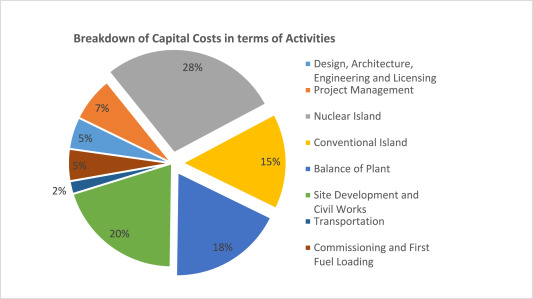

SMR Capital Costs Breakdown Visualized

The section highlights high capital expenditure (CAPEX) as a primary deterrent. This chart perfectly illustrates the major components of SMR capital costs, directly supporting the article’s point about financial hurdles.

(Source: ScienceDirect.com)

- Market forecasts indicate a growing industrial capacity for SMRs, with projections from Marketsand Markets showing growth from $6.00 billion in 2024 to $7.14 billion by 2030. This expansion is a critical enabler for niche applications like shipping.

- The primary financial barrier is the high upfront capital cost. Estimates place the CAPEX for a single-unit SMR at $5, 715/k W, meaning a 100 MW reactor for a large container ship would cost over $570 million before vessel integration.

- Economic viability hinges on total cost of ownership calculations in a carbon-constrained world. As carbon taxes rise, the high CAPEX of nuclear becomes more competitive against the volatile operational costs of bunker fuel and the high projected prices of green alternatives like ammonia.

- The first projects are unlikely to be financed without significant government support, such as loan guarantees or contracts for difference, to de-risk the investment for first-of-a-kind (FOAK) vessels.

Table: SMR Market Size Projections (2024-2034)

| Forecast Provider | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Marketintelo | 2025 – 2034 | Projects the Nuclear Microreactor & SMR market to grow from $4.8 billion in 2025 to $26.4 billion by 2034, reflecting a high-growth scenario of a 19.3% CAGR. This outlook is based on rapid technology maturation and adoption in various sectors. | Marketintelo |

| Datam Intelligence | 2025 – 2033 | Forecasts the SMR market to expand from $6.42 billion in 2025 to $12.24 billion by 2033 at an 8.65% CAGR. This reflects steady demand for carbon-free power from heavy industry and remote applications. | Datam Intelligence |

| Marketsand Markets | 2024 – 2030 | Provides a conservative forecast, with the SMR market growing from $6.00 billion in 2024 to $7.14 billion by 2030 (3.0% CAGR). This projection highlights the impact of regulatory hurdles and long development timelines. | Marketsand Markets |

Global vs. Regional, SMR Maritime Regulation Blocks Port Access and Routes

Maritime SMR development is geographically concentrated in nations with strong shipbuilding industries and existing nuclear expertise, but global deployment is stalled by the lack of a harmonized international regulatory framework for port access, liability, and safety. Without a global solution, nuclear-powered commercial vessels will be confined to limited point-to-point routes between specially prepared ports.

Raw Material Supply is Geographically Concentrated

The section discusses global versus regional challenges, including regulatory fragmentation. This chart highlights a related dependency, showing how the raw material supply for nuclear fuel is also concentrated in a few nations.

(Source: Information Technology and Innovation Foundation (ITIF))

- Development activity is centered in established nuclear and maritime nations. The United Kingdom’s Generic Design Assessment (GDA) for the Rolls-Royce SMR and South Korean shipbuilder HD Hyundai’s design work are prime examples of regional leadership.

- The single greatest barrier to deployment is regulatory fragmentation. Maritime law is governed by the International Maritime Organization (IMO), while nuclear safety is overseen by the International Atomic Energy Agency (IAEA) and national regulators, with no integrated treaty for mobile marine reactors.

- Port access is a critical unresolved issue. Without international agreements, nuclear-powered ships face the risk of being denied entry to ports due to national security concerns, liability questions, or public opposition, rendering global trade routes unviable.

- The creation of a dedicated global network of nuclear-ready ports is a prerequisite for widespread adoption. This requires massive investment in specialized infrastructure for refueling, maintenance, waste handling, and emergency response, a task no single entity can undertake.

Maritime SMRs, 5 Reactor Designs Remain at TRL 3-5 (2021 to 2026)

While the foundational Pressurized Water Reactor (PWR) technology is mature from decades of naval use, the advanced Generation-IV SMR designs favored for commercial shipping remain at low Technology Readiness Levels (TRL 3-5). This indicates that prototypes are still in lab or simulation phases, with commercial readiness not expected before 2035.

Explainer on Advanced SMR Reactor Designs

This section details the various SMR designs under development and their readiness levels. The chart provides a clear visual guide to these different reactor technologies, directly complementing the text.

(Source: Information Technology and Innovation Foundation (ITIF))

- From 2021 to 2024, most maritime SMR concepts were at TRL 2-3. By 2025, several designs have advanced to TRL 4-5, signifying prototype demonstration in a lab environment, but they are still far from commercial deployment (TRL 8-9).

- Pressurized Water Reactors (PWRs), scaled-down versions of naval reactors, are the most mature at TRL 6-7. However, the industry is trending toward safer, more efficient Generation-IV designs like Molten Salt Reactors (MSRs), which are at a lower TRL of 3-4.

- Lead-Cooled Fast Reactors (LFRs), another Gen-IV design, offer a long core life that could last a vessel’s entire lifespan but are also at a low maturity level of TRL 3-4, with developers like Westinghouse and Seaborg Technologies still in early development stages.

- A critical dependency for many advanced reactors, including those from developers like X-energy and Terra Power, is the supply of High-Assay Low-Enriched Uranium (HALEU) fuel. The current global supply chain for HALEU is insufficient to support a large fleet of SMRs.

SWOT Analysis, Maritime SMR Strengths vs. Regulatory & Cost Hurdles

The primary strengths of maritime SMRs are their unmatched energy density and zero-emission operation, which directly solve the shipping industry’s decarbonization challenges. However, these are currently offset by weaknesses in economic viability and significant external threats from regulatory fragmentation and a lack of critical fuel supply infrastructure.

Nuclear Power’s High Reliability Factor

The section summarizes a SWOT analysis, citing operational advantages as a key strength. This chart quantifies that strength by showing nuclear’s leading capacity factor, demonstrating its superior reliability.

(Source: Information Technology and Innovation Foundation (ITIF))

Table: SWOT Analysis for Maritime SMR Adoption

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical zero-emission power with high energy density. Potential for longer voyages and higher speeds. | Validated ability to provide >100 MWe power for large vessels in design studies. No refueling needs confirmed as a key operational advantage. | The operational benefits of endurance and power density have been validated in conceptual designs for large container ships, moving them from theory to concrete engineering plans. |

| Weaknesses | High hypothetical CAPEX. Unproven commercial-grade reactor designs. Lack of specialized crew. | Specific CAPEX estimates ($5, 715/k W) confirm extreme upfront cost. Most designs remain at low TRL (3-5). | The economic weakness has been quantified, confirming that SMRs are not financially viable without heavy subsidies or extreme carbon pricing. The technology gap between naval and commercial designs is now clearly defined. |

| Opportunities | Meeting future IMO GHG targets. Potential for new Arctic trade routes. Powering onboard systems. | The IMO adopted a Net-Zero Framework by 2050, creating a firm regulatory driver. “Cold ironing” (supplying power to ports) emerged as a viable secondary revenue stream. | The regulatory push for decarbonization has become a concrete mandate, solidifying the market opportunity for zero-emission propulsion. New use cases like port-side power supply have been validated. |

| Threats | Fragmented regulatory landscape. Negative public perception. Lack of port infrastructure. | The dual regulatory problem (IMO vs. IAEA) remains unresolved. HALEU fuel supply chain insufficiency identified as a major strategic bottleneck. | The regulatory threat has intensified as pilot projects near, with no clear path to international licensing. The dependency on a non-existent HALEU supply chain has emerged as a critical, near-term threat to deployment. |

2035 SMR Commercialization, 1 st Pilot Vessel Hinges on IMO Regulation

The most likely scenario for maritime SMR adoption involves the first commercial pilot vessel launching around 2035, a timeline entirely contingent on the successful establishment of a harmonized international regulatory framework by the IMO and IAEA within the next five to seven years. Without this, technological progress will be irrelevant for global trade.

Aging Global Fleet Drives Need for SMRs

This section looks toward the future commercialization timeline. The chart provides crucial context by showing the advanced age of the current global nuclear fleet, highlighting the long-term need for new reactor technology.

(Source: World Nuclear Industry Status Report)

- If this happens: A unified IMO/IAEA regulatory framework is established by 2030. Watch this: A rapid increase in bilateral “green corridor” agreements between nations to permit nuclear vessel transit and investment in a small number of nuclear-ready “super-ports” in key trade hubs like Singapore and Rotterdam.

- If this happens: SMR costs continue to escalate, following the trend seen in some land-based projects, while green ammonia production costs fall faster than expected. Watch this: Major shipping lines like Maersk and CMA CGM will solidify their commitment to ammonia/methanol-powered newbuilds, delaying significant investment in nuclear-powered vessels until the post-2040 period.

- These could be happening now: The clearest signals of progress are non-technical. Watch for the formation of a dedicated IMO working group for mobile marine reactors, the publication of formal “rules for nuclear ships” by classification societies like DNV and ABS, and an increase in joint development agreements between reactor vendors and major shipbuilders.

The questions your competitors are already asking

This report covers one angle of SMR commercial adoption in the maritime sector. The questions that matter most depend on your work.

- What is the outlook for SMR deployment in commercial shipping by 2035?

- What is actually happening with the Allseas five-year SMR pilot since its 2021 announcement?

- How do Molten Salt Reactors (MSRs) compare to scaled-down Pressurized Water Reactors (PWRs) for commercial shipping?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.