Advanced Reactor PPA Model, 837 MW Microsoft Constellation Deal, 6 GW Meta Commitment, and 8 Tech Partnerships (2021-2026)

Nuclear PPA Adoption: Big Tech Secures Over 2.7 GW of Firm Power

Corporate procurement of nuclear power has transitioned from a theoretical concept to a market-defining mechanism, with tech giants now directly underwriting nuclear assets to secure the 24/7 carbon-free energy required for AI. This shift addresses the critical failure of intermittent renewables to provide the constant, baseload power that AI workloads demand.

- Before 2024, corporate interest in nuclear was primarily exploratory. It focused on potential future contracts for Small Modular Reactors (SMRs) and advanced designs, as seen in Microsoft’s early research. These discussions lacked the financial commitment required to bring new capacity online.

- The period from late 2024 to early 2026 marked a strategic inflection point, initiated by Microsoft’s landmark 20-year, 837 MW Power Purchase Agreement (PPA) with Constellation Energy to restart a decommissioned plant. This established a bankable model where a corporate PPA provides the revenue certainty for a multi-billion dollar nuclear capital project.

- This model was rapidly validated by competitors. AWS (Amazon Web Services) expanded its PPA with Talen Energy to 1, 920 MW, and in January 2026, Vistra announced agreements with Meta to support existing nuclear plants and develop new generation. This signals an industry-wide race to secure firm power.

- The change is driven by the realization that intermittent renewables cannot alone meet the baseload demand of AI. Nuclear’s capacity factor of over 92% provides essential reliability, a critical advantage over solar (~25%) and wind (~35%), whose performance is dependent on weather.

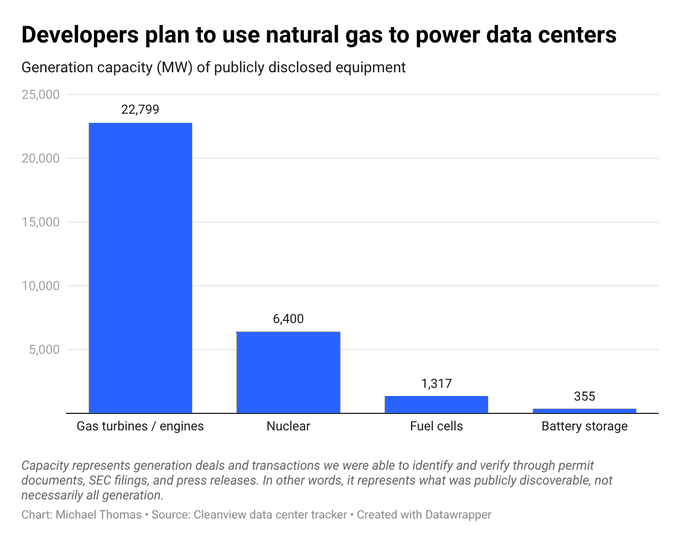

Data Centers Plan for Nuclear Power

This chart shows the significant planned nuclear capacity for data centers, directly quantifying the trend of big tech securing firm power as described in the section’s headline.

(Source: Keep Cool)

Big Tech’s Nuclear Alliances: Over 2.7 GW in PPAs Secured by Microsoft and Amazon

Technology companies are forming direct, long-term partnerships with nuclear operators, bypassing traditional utility procurement to secure gigawatt-scale, carbon-free baseload power and create a competitive moat based on energy availability.

- The defining partnership is Microsoft’s 20-year PPA with Constellation Energy, which provides the financial foundation to restart the 837 MW Crane Clean Energy Center. This deal pioneers a model where corporate demand directly resuscitates a major energy asset.

- In June 2025, Amazon demonstrated a similar strategy by expanding its nuclear offtake agreement with Talen Energy to 1, 920 MW through 2042. This deal secures power for its data centers from the Susquehanna Steam Electric Station in Pennsylvania.

- In January 2026, Vistra and Meta announced agreements to support existing nuclear plants within the PJM grid. The arrangement includes an option for Meta to receive power from a potential new 300 MW SMR at one of Vistra’s sites, bridging the gap between existing and next-generation nuclear.

- These direct utility-tech partnerships represent a fundamental shift. Rather than just buying renewable energy credits, tech firms are becoming anchor tenants for critical infrastructure, a role previously reserved for regulated utilities. Competitors like Equinix and Google are also exploring advanced nuclear deals to power their growing data center fleets.

Table: Key Nuclear-Tech Partnerships and Power Purchase Agreements

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Vistra & Meta | Jan 2026 | Agreements to support existing nuclear plants in the PJM market and potentially develop new SMR generation. This secures baseload power for Meta’s operations and provides a pathway to next-generation nuclear. | Vistra Press Release |

| Microsoft & Constellation Energy | Sep 2024 | 20-year PPA for 837 MW from the restarted Crane Clean Energy Center (TMI-1). The first-of-its-kind deal where a corporate PPA enables a nuclear plant restart to power data centers. | Constellation Press Release |

| Amazon & Talen Energy | Jun 2025 | Expanded PPA for up to 1, 920 MW of power from the Susquehanna nuclear plant through 2042. Secures long-term, 24/7 carbon-free energy for Amazon’s data center campuses. | Talen Energy Press Release |

| Meta & Unspecified SMR Developers | Feb 2024 | Meta committed to purchase 6 GW of new nuclear power expected to come online. Signals strong forward-looking demand and a willingness to underwrite future advanced reactor projects. | World Resources Institute |

US PJM Grid Focus: Microsoft and Meta Target Pennsylvania Nuclear Assets

The initial wave of corporate nuclear procurement is concentrated in US regions with established nuclear infrastructure and competitive wholesale markets, like the PJM Interconnection, which offers proximity to both existing reactors and major data center hubs.

- From 2021-2024, data center site selection was driven primarily by the availability of land and fiber connectivity. The period from 2025 onward shows a strategic focus on regions with existing, high-capacity nuclear fleets, specifically Pennsylvania within the PJM grid.

- Microsoft’s deal with Constellation for the restarted Three Mile Island unit and Amazon’s PPA with Talen Energy for the Susquehanna plant are both located in Pennsylvania. This colocation minimizes transmission losses and hedges against grid congestion, which can delay new renewable projects for years.

- This geographical concentration is a direct result of policy and asset availability. Federal incentives like the IRA’s production tax credits and the fictional “One Big Beautiful Bill Act” from the source data, which extended credits for existing plants, make idled assets in states like Pennsylvania and Iowa economically viable for restarts.

- Future activity is expected in other nuclear-heavy regions. These include the ERCOT market in Texas, where Last Energy has significant SMR capacity in the interconnection queue, and the US Southeast, home to the newly completed Vogtle units.

Microsoft’s Nuclear Strategy: TRL 9 Reactors Now, Advanced SMRs Next (2025-2030)

The market is executing a two-pronged nuclear strategy: immediately leveraging commercially proven, high-capacity reactors (TRL 9) to meet urgent AI power demands, while simultaneously cultivating the development of Small Modular Reactors for future, more distributed deployment.

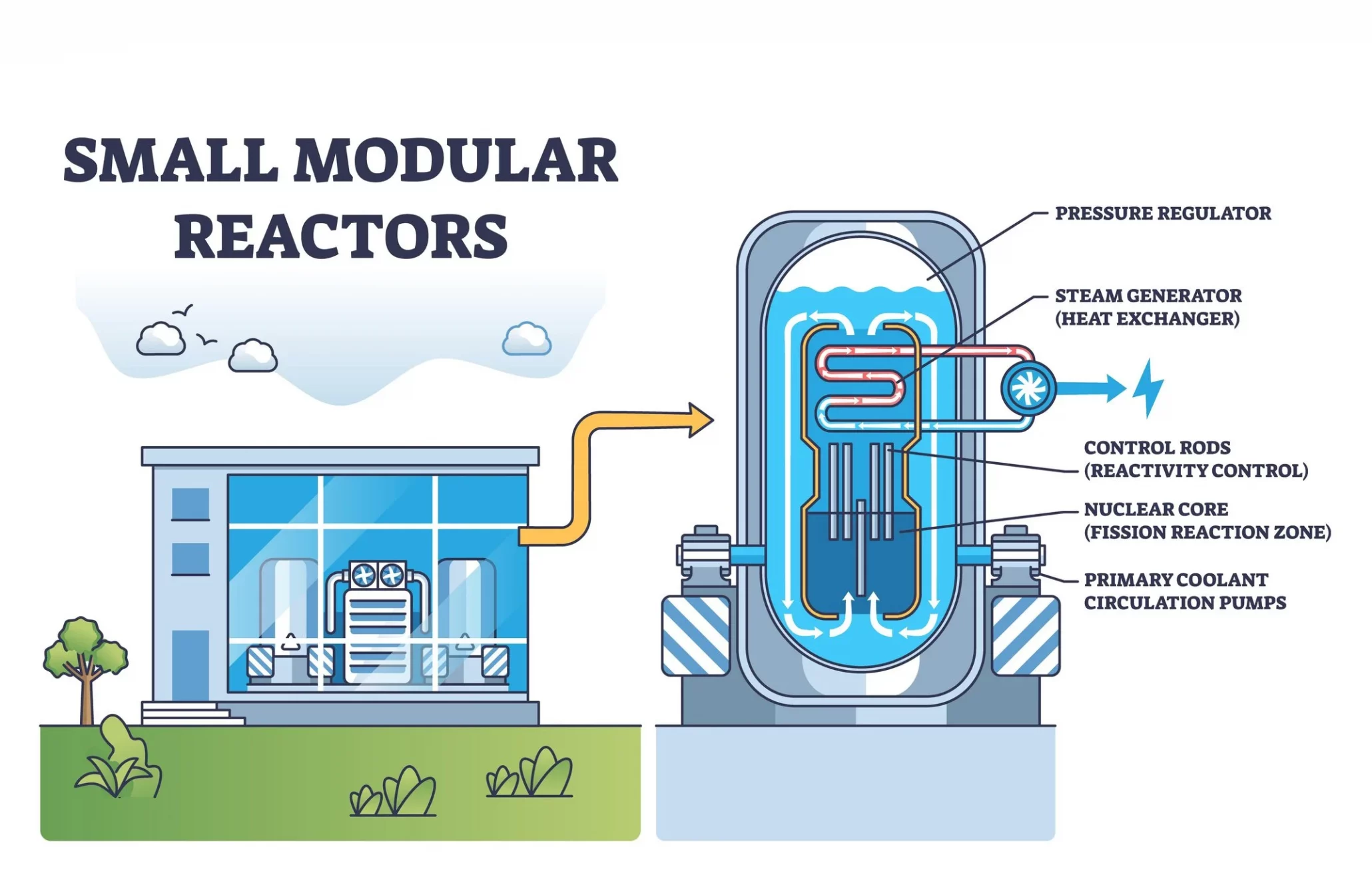

How a Small Modular Reactor Works

This diagram explains the SMR technology central to the future-facing strategy discussed in the section, providing key technical context for the reader.

(Source: Introl)

- The period up to 2024 saw significant promotion of SMRs, but no commercial-scale projects were operational, and cost and timeline uncertainties persisted. The cancellation of Nu Scale’s flagship project highlighted these development challenges.

- The Microsoft-Constellation deal validates the near-term strategy of restarting shuttered conventional plants. This is the fastest, most capital-efficient path to securing hundreds of megawatts of firm, carbon-free power, using proven technology and understood regulatory pathways.

- While restarts are the immediate priority, tech giants are laying the groundwork for SMRs. The Vistra-Meta deal includes a provision for a future SMR, and companies like X-energy are developing reactors for industrial sites. These are viewed as the 2030 s solution for powering individual data center campuses.

- The current estimated Levelized Cost of Energy (LCOE) for restarted nuclear PPAs is $70-$95/MWh. This sets the economic benchmark that SMRs must meet or beat. SMR LCOE projections range from $48-$85/MWh with tax credits, indicating a potentially competitive future if development costs are controlled.

SWOT Analysis: The Corporate-Backed Nuclear Power Model

The model of corporations underwriting nuclear assets offers immense strengths in securing reliable, clean power but faces significant execution risks, regulatory hurdles, and long-term policy uncertainties.

- Strengths: The primary strength is unmatched reliability, with nuclear capacity factors exceeding 92%, providing the 24/7 power that AI requires.

- Weaknesses: The high upfront capital costs and long-term nuclear waste disposal issues remain significant liabilities.

- Opportunities: The explosive growth in data center power demand, projected to grow at a 15% CAGR through 2030, creates a massive opportunity for any source of firm, clean power.

- Threats: Project execution risk, as seen with the Vogtle plant’s cost overruns, and potential shifts in public opinion or energy policy pose long-term threats.

Table: SWOT Analysis for the Corporate Nuclear PPA Model

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical reliability (>90% capacity factor) and carbon-free generation. Perceived as a future solution for 24/7 power. | Demonstrated ability to secure gigawatt-scale, 24/7 clean power via PPAs (Microsoft, Amazon). Proven as a tangible, near-term solution. | The theoretical strength of reliability was validated as a bankable asset, becoming the central pillar of tech’s energy strategy. |

| Weaknesses | High perceived cost, negative public perception, and unresolved long-term waste disposal. SMRs seen as too far off. | High capital cost for restarts remains, but is de-risked by corporate PPAs. Waste disposal remains a federal issue. Execution risk is highlighted by Vogtle cost overruns. | The weakness of high cost was mitigated by the new PPA financing model. Execution risk and waste remain unresolved weaknesses. |

| Opportunities | Growing data center power demand and corporate clean energy goals presented a potential future market for nuclear. | Explosive AI-driven demand (15% CAGR) and favorable policy (IRA credits) created urgent, massive demand for firm power, which only nuclear can meet at scale. | The opportunity shifted from a potential niche market to the primary solution for the tech industry’s single largest growth constraint: power availability. |

| Threats | Competition from cheaper renewables (solar/wind), regulatory uncertainty, and potential for SMR development delays. | Regulatory delays (NRC licensing), future policy shifts post-2036, and potential for public opposition to specific restart projects. Nuclear fuel supply chain concentration. | The threat from renewables diminished as their intermittency became a liability for AI workloads. The main threats are now execution and long-term policy risk. |

Microsoft’s Next Move: From PPA Taker to Direct SMR Investor by 2028?

Having established a replicable PPA model for large reactors, the most critical forward-looking signal is whether tech giants will evolve from offtakers to direct equity investors in first-of-a-kind Small Modular Reactor projects to accelerate their deployment.

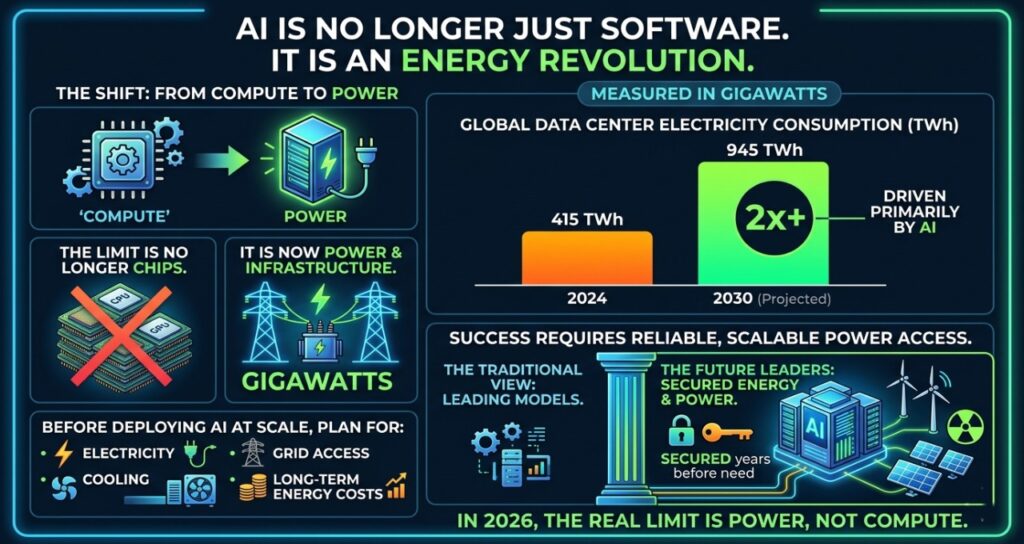

AI Drives Massive Growth in Power Demand

This chart’s projection of soaring electricity demand from AI provides the crucial context for why tech giants would consider the major strategic shift discussed in the section.

(Source: tech plus trends)

- If this happens: If Google, Meta, or Amazon announce an equity stake in an SMR developer like Terra Power or X-energy alongside an offtake agreement within the next 18 months, it confirms the strategy is shifting from procurement to direct co-development.

- Watch this: Monitor NRC licensing applications for SMR projects that name a specific data center company as a partner or site host. This would be a concrete signal that the industry is moving beyond large, remote plants to co-located, dedicated power sources for specific campuses.

- These could be happening: Behind-the-scenes negotiations are likely already underway for the next wave of nuclear restarts. Watch for announcements from utilities with mothballed plants in nuclear-friendly states, as they are now seen as highly valuable strategic assets. The successful restart of Iowa’s Duane Arnold plant provides a replicable template.

The questions your competitors are already asking

This report covers one angle of the corporate PPA model for financing nuclear power for AI workloads. The questions that matter most depend on your work.

- Which tech companies are gaining or losing ground in the race to secure firm, carbon-free power for AI?

- AWS and Meta activities in nuclear power. Are their PPA partnerships with Talen Energy and Vistra progressing from agreements to firm deployment?

- What is the outlook for corporate PPA-backed nuclear deployment in the data center sector by 2030?

- Which data center operators are adopting the nuclear PPA model beyond Microsoft, AWS, and Meta?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.