DAC CORSIA Compliance, IATA Alliance for 250 M Credits, $1.7 B Cost, and 10+ Airline Agreements (2021 to 2026)

DACCS Projects, IATA’s 250 M Credit Demand Signal for CORSIA

The market for Direct Air Carbon Capture and Storage (DACCS) is fundamentally shifting from a niche supported by voluntary corporate climate pledges to a critical compliance tool for the global aviation industry. The International Air Transport Association (IATA) has identified DACCS as an essential solution for meeting the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) targets, creating a powerful, non-negotiable demand signal that is reshaping the industry’s financial and operational trajectory.

- Between 2021 and 2024, the DACCS market was driven by early adopters, primarily tech companies like Microsoft, which signed multi-year offtake agreements with providers such as Climeworks and 1 Point Five. These deals validated the technology and provided revenue certainty for first-of-a-kind projects, but the demand remained voluntary and fragmented.

- Starting in 2025, the demand driver has pivoted to regulatory compliance. IATA projected a need for 225 to 250 million CORSIA-eligible credits for the 2024-2026 compliance period and forecast a cumulative supply shortfall of 202 million tonnes. This quantifiable gap represents a direct and urgent demand for high-integrity credits that only technologies like DACCS can supply.

- The market response to this compliance pressure materialized in June 2026 with IATA’s formation of the Supporting Alliance for CORSIA EEU Supply. This coalition of airlines and specialists was created specifically to unlock credit supply, serving as a unified demand signal that provides DACCS developers with the offtake confidence required for large-scale project financing.

- This shift is further validated by direct airline engagement. While earlier years saw general commitments, 2026 brought specific deals like Lufthansa Group’s partnership with Canadian developer Deep Sky for high-quality carbon removal credits, marking a direct link between airline compliance needs and DACCS project development.

Global Air Traffic Growth Fuels Offset Demand

This chart explains the fundamental driver (global air traffic growth) for the increasing ‘demand signal’ for carbon credits mentioned in the section, as airlines anticipate future CORSIA compliance needs.

(Source: IATA)

$20 B in UK CCUS Funding and US 45 Q Tax Credit De-Risk DACCS

Government policy has evolved from general support to targeted financial mechanisms that directly de-risk the high capital costs of DACCS projects, creating the necessary investment environment to meet emerging compliance demand. Early-stage R&D funding between 2021 and 2024 gave way to powerful, bankable incentives post-2025 that underpin the financial models for commercial-scale facilities.

- The U.S. Inflation Reduction Act (IRA) was a critical turning point, enhancing the 45 Q tax credit to provide a significant financial incentive for DACCS. This policy directly lowers the effective cost of carbon removal, making projects more attractive to investors and enabling developers like 1 Point Five to advance large-scale facilities such as the STRATOS plant in Texas.

- In April 2026, the U.S. Department of Energy restored crucial funding for carbon removal projects, reinforcing public-sector commitment and providing financial stability to an industry facing high upfront capital requirements.

- The UK government has committed up to £20 billion to support the Carbon Capture, Usage, and Storage (CCUS) sector, which includes DACCS. This long-term vision aims to establish a competitive market and provides a clear signal of sovereign support for the infrastructure required for permanent carbon storage.

- Canada established a clear compliance pathway in February 2025 by launching a federal offset protocol for DACCS. This regulation allows projects to generate credits within Canada’s carbon pricing system, creating a domestic market and financial incentive for developers like Deep Sky.

Table: Key Government Funding and Policy Enablers for DACCS

| Policy / Funding Program | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Department of Energy Funding Restoration | Apr 2026 | Restored funding for major carbon removal projects, providing critical public-sector support to de-risk and scale technology development. | Reuters |

| Government of Canada Federal Offset Protocol | Feb 2025 | Launched a formal compliance protocol for DACCS, allowing projects to generate credits under Canada’s carbon pricing system and creating a domestic market. | CDR.fyi |

| UK Government CCUS Vision | Dec 2023 | Announced up to £20 billion in funding to support the CCUS sector, signaling long-term commitment to building the necessary infrastructure for carbon removal and storage. | GOV.UK |

| U.S. Inflation Reduction Act (45 Q Tax Credit) | Aug 2022 | Significantly enhanced tax credits for carbon sequestration, providing a powerful financial incentive that underpins the economic viability of large-scale DACCS projects in the U.S. | World Resources Institute |

IATA Alliance for CORSIA, 10+ Offtake Deals, Lufthansa to Microsoft (2022 to 2026)

Strategic partnerships and long-term offtake agreements have become the primary commercial mechanism for scaling the DACCS market, providing developers with the revenue certainty needed to secure project financing. The nature of these partnerships has matured from speculative, voluntary purchases to strategic procurement by hard-to-abate industries like aviation to secure future compliance.

- Before 2025, landmark deals were dominated by technology companies. Microsoft’s agreements with Ørsted and 1 Point Five, and Airbus’s purchase of 400, 000 tonnes of removal credits from 1 Point Five, established bankable models for project financing based on corporate demand.

- The formation of demand aggregators like the Frontier Fund, backed by Stripe, Shopify, and Meta with a $1 billion+ commitment, signaled a coordinated effort to stimulate the supply of permanent carbon removals through advance market commitments.

- From 2025 onward, the focus shifted to direct aviation industry involvement. The Lufthansa Group’s agreement with Deep Sky for carbon removal credits is a primary example of an airline securing its own supply chain for CORSIA compliance, moving beyond reliance on third-party brokers.

- IATA’s creation of the Supporting Alliance for CORSIA EEU Supply in 2026 represents the most significant market development, institutionalizing the demand signal from the entire aviation sector and creating a platform for consortium-based offtake agreements with DACCS providers.

Table: Selected DACCS and Carbon Removal Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Lufthansa Group & Deep Sky | May 2026 | Partnership for the supply of high-quality carbon removal credits, signaling direct airline engagement to secure CORSIA-compliant offsets. | Sustainability Magazine |

| Microsoft & 1 Point Five | Sep 2024 | Offtake agreement for 500, 000 tonnes of carbon removal credits from the STRATOS DACCS facility, providing a key anchor customer for the large-scale project. | 1 Point Five |

| JPMorgan Chase & Multiple CDR Providers | Apr 2024 | Agreements valued at approximately $200 million to purchase over 800, 000 tonnes of carbon removal credits, including from Climeworks, diversifying its portfolio. | IEA |

| Airbus & 1 Point Five | Mar 2022 | Four-year agreement for 400, 000 tonnes of carbon removal credits, demonstrating early demand from the aerospace sector to address its value chain emissions. | 1 Point Five |

North America vs Europe, DACCS Project Development and Policy Support

The geographic landscape of DACCS development is concentrated in North America and Europe, where favorable geology for storage and robust government policy create a fertile ground for project deployment. While Europe was a first-mover with operational plants, North America is now positioned to lead in large-scale capacity additions, driven by superior financial incentives.

- Between 2021 and 2024, Europe led in operational capacity, with Climeworks launching its Orca and Mammoth plants in Iceland. These projects leveraged Iceland’s unique combination of renewable geothermal energy and basaltic rock formations ideal for permanent CO₂ mineralization.

- The United States emerged as a key development hub during this period, with Heirloom opening the first commercial DAC facility in the country in California in November 2023. This was largely enabled by state-level climate policies and venture funding.

- From 2025 onward, the U.S. is set to dominate large-scale deployment, primarily due to the 45 Q tax credit. Occidental’s STRATOS project in Texas, designed to capture up to 500, 000 tonnes annually, exemplifies this shift and leverages the region’s established oil and gas infrastructure and geological storage potential.

- Canada is solidifying its position as a strategic hub for DACCS. The federal government’s 2025 offset protocol created a clear financial pathway for projects, attracting developers like Deep Sky and positioning the country as a key supplier of high-integrity credits for both domestic and international compliance markets.

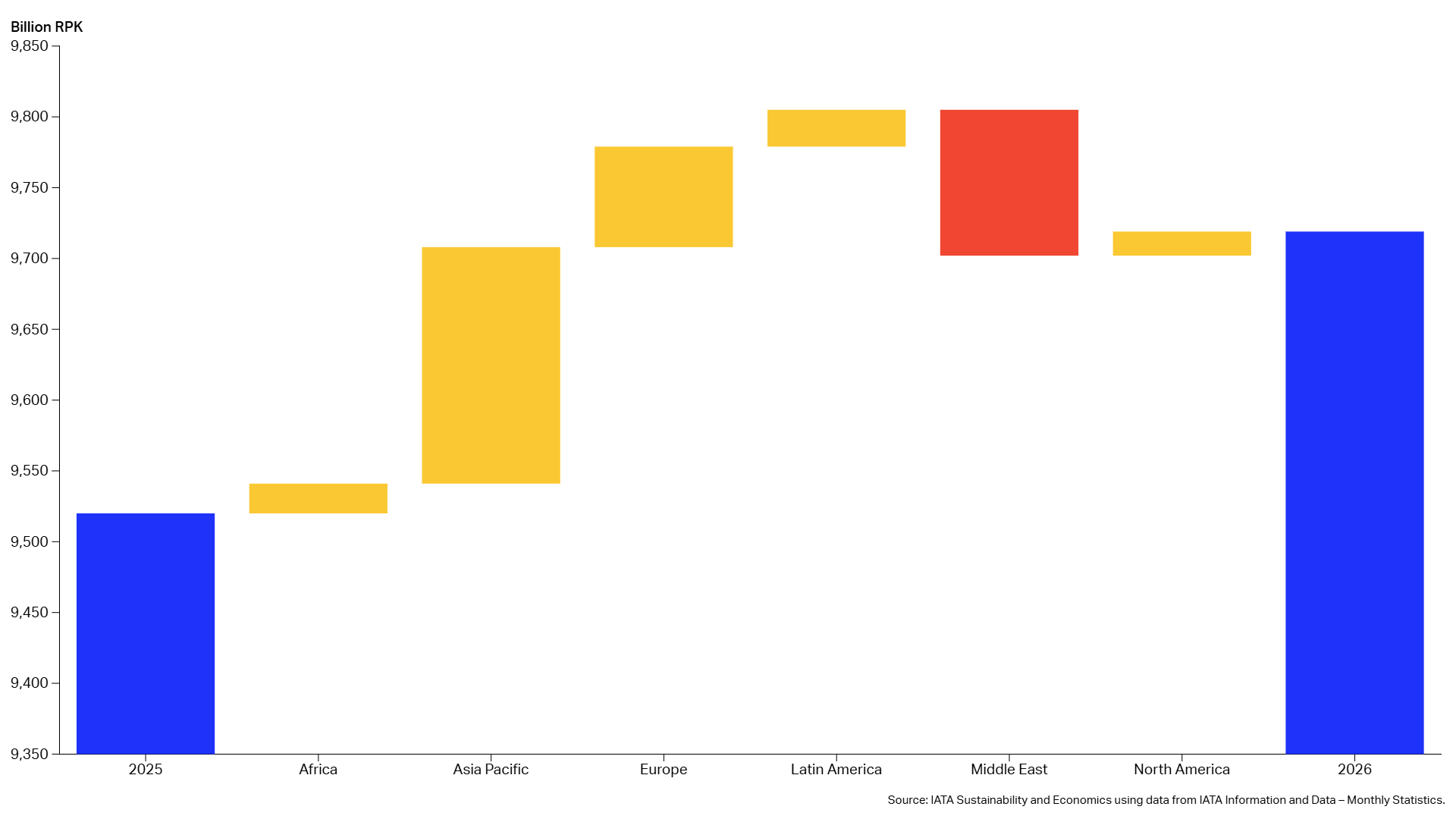

Asia Pacific to Lead Post-2025 Aviation Growth

This chart provides critical global context for the section’s comparison of North American and European policy. It shows that future aviation growth is concentrated in the Asia Pacific, highlighting the global scale of the emissions challenge that Western policies aim to address.

(Source: IATA)

$600/Tonne Costs, Climeworks’ Mammoth Plant and 1 Point Five STRATOS Project Scale

DACCS technology is progressing from small-scale, kiloton-level demonstration projects to the first generation of commercial, megaton-scale facilities, yet costs remain the primary barrier to widespread adoption. The period from 2021 to 2024 was defined by proving operational viability, while the period from 2025 to today is characterized by the race to scale production and drive down the cost curve in response to compliance-driven demand.

- Between 2021 and 2024, operational milestones were set by Climeworks. Its Orca plant (4, 000 tonnes/year) and subsequent Mammoth plant (36, 000 tonnes/year) demonstrated the viability of its solid-sorbent technology but at a high cost, estimated between $600 and $1, 000 per tonne.

- The market is now bifurcating between different technology pathways. While Climeworks and Heirloom focus on modular systems, Carbon Engineering (acquired by Occidental) is pursuing large-scale liquid-solvent plants, betting on economies of scale to reduce costs.

- As of 2026, cost estimates remain stubbornly high. Verified operational costs for net removal are reported in the $600 to $800 per tonne range, significantly above the sub-$100 per tonne target considered necessary for mass-market adoption. An ETH Zurich study projected costs will likely remain between $230 and $540 per tonne even by 2050.

- The primary technological challenge is moving from kiloton-scale operations to facilities capable of capturing over 500, 000 tonnes annually, such as 1 Point Five’s STRATOS project. Successfully commissioning these larger plants will be the definitive test of the technology’s scalability and its potential to meet the immense demand from sectors like aviation.

Charts Quantify CO₂ Removal Required for Climate-Neutral Aviation

This chart quantifies the total CO₂ removal required for climate neutrality, establishing the need for the large-scale projects like the Mammoth and STRATOS plants and their associated costs, which are the subject of the section.

(Source: Nature)

SWOT Analysis, IATA’s DACCS Demand and High Cost Constraints

The strategic position of DACCS has been transformed by the emergence of a large, mandatory compliance market in aviation, which magnifies both its strengths as a high-integrity solution and its weaknesses related to cost and scale. This shift has created new opportunities for market integration while exposing the threat of a severe supply-demand imbalance.

Global Airline Profits Recover After Pandemic Losses

This chart on recovering airline profits provides direct financial context for the section’s SWOT analysis. It informs the discussion on airlines’ financial capacity (‘Strength’ or ‘Weakness’) to invest in high-cost DACCS solutions and manage the ‘Constraints’ mentioned.

(Source: IATA)

Table: SWOT Analysis for DACCS in Aviation Compliance

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | High permanence and verifiability of carbon removal, attracting voluntary demand from corporations like Microsoft seeking high-quality offsets. | Durability and quantifiability are now essential for compliance markets. IATA’s endorsement validates DACCS as a preferred solution for meeting rigorous CORSIA standards. | The core value proposition of permanence shifted from a “nice-to-have” for voluntary markets to a “must-have” for regulated compliance. |

| Weaknesses | Prohibitively high costs ($600-$1, 000/tonne) and very limited operational capacity (under 10, 000 tonnes/year globally) confined it to a niche market. | Costs remain high ($600-$800/tonne), and a severe supply shortage of 202 million tonnes is now officially projected for the first CORSIA compliance period. | The weakness of limited supply has intensified into a critical bottleneck, threatening the functionality of the CORSIA market itself. |

| Opportunities | Emerging government incentives, such as the initial U.S. 45 Q tax credit and R&D grants, provided early-stage project support. | Formal compliance pathways are established (e.g., Canada’s offset protocol, ICAO program approvals), and alliances like IATA’s create structures for large-scale, multi-year offtake agreements. | The opportunity moved from speculative policy support to a structured, bankable offtake market driven by regulatory mandates. |

| Threats | Risk that the technology would remain too expensive for anything beyond niche corporate social responsibility budgets and fail to achieve commercial scale. | The massive gap between mandated demand and available supply could drive prices even higher, potentially making CORSIA compliance financially untenable for some airlines and jeopardizing the scheme’s goals. | The threat evolved from commercial failure due to high costs to a systemic market failure where demand exists but cannot be met at any viable price. |

IATA’s 2026 Outlook, CORSIA Compliance Driving Multi-Year Offtake Deals

The critical dynamic for the DACCS market in the year ahead will be the industry’s race to sign large-volume, multi-year offtake agreements to bridge the officially recognized supply gap for CORSIA compliance. If airlines and their consortiums can successfully secure these bankable contracts, it will unlock the project financing needed to build the next generation of megaton-scale facilities.

- If this happens: A wave of multi-year offtake agreements is announced between airline consortiums (mobilized by the IATA alliance) and leading DACCS developers like 1 Point Five and Climeworks.

- Watch this: The final investment decisions (FIDs) for large-scale projects like STRATOS and subsequent facilities. These decisions are contingent on securing long-term revenue streams, which these airline offtake agreements would provide.

- These could be happening: DACCS developers will accelerate M&A activity to acquire complementary technologies or enter joint ventures with energy majors to leverage balance sheets and geological expertise, mirroring Occidental’s acquisition of Carbon Engineering. The focus will be on building vertically integrated carbon management businesses capable of delivering removal credits at scale.

Chart Shows Aviation’s Growing CORSIA Compliance Gap

This chart directly visualizes the ‘growing CORSIA compliance gap,’ which is the central problem driving the 2026 outlook and the multi-year offtake deals discussed in the section.

(Source: Krungsri.com)

The questions your competitors are already asking

This report covers one angle of DACCS commercialization for aviation CORSIA compliance. The questions that matter most depend on your work.

- Which DACCS companies, like Climeworks or 1 Point Five, are gaining ground in the CORSIA compliance credit market?

- What is the outlook for DACCS deployment to meet the airline industry’s demand for 250 million CORSIA credits by 2026?

- What is actually happening with IATA’s Supporting Alliance for CORSIA EEU Supply since its formation in June 2026?

- Which airlines are adopting DACCS solutions to meet CORSIA targets?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.