Base Power BESS VPP Model, $1.2 B Valuation Target, Lennar Partnership, and Austin Energy Deal (2023-2026)

BESS Adoption, Base Power’s 100 MWh Deployed and the Shift to Energy-as-a-Service

The residential energy storage market is moving from high-cost, one-time hardware sales to integrated, service-based models that reduce upfront costs and aggregate homes into grid assets. This shift is validated by the rapid scaling of companies like Base Power, which lowers the financial barrier for homeowners and creates a new revenue stream from grid services, a model that gained significant traction between 2025 and 2026 through key utility partnerships.

- Between 2021 and 2024, residential battery adoption was primarily driven by consumers seeking backup power, with high upfront costs of $15, 000 or more limiting the market to affluent households. VPP participation through programs like Tesla‘s was an optional add-on rather than the core business model.

- Starting in 2024, Base Power launched its disruptive model in Texas, offering a 20 k Wh battery for a $2, 000-$3, 000 installation fee by bundling it with a retail electricity plan. This turned the home into a grid-interactive asset from the outset.

- By 2025 and 2026, this model achieved commercial validation. Base Power sold over 100 MWh of storage in Texas and secured a landmark partnership with municipal utility Austin Energy in April 2026 to use its aggregated home batteries for grid stability.

- The growth in demand from data centers, as seen with Microsoft, is a major driver for new power solutions. The industry is exploring various options, including advanced nuclear reactors, to meet this load growth, highlighting the need for flexible resources like VPPs.

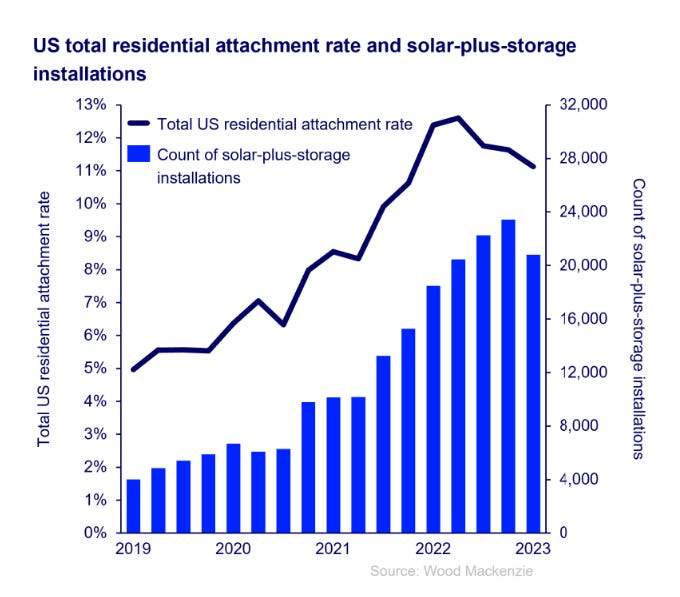

US Residential Solar+Storage Adoption Surges

The section focuses on ‘BESS Adoption’ and the broader shift in the energy market. This chart, showing a surge in ‘Residential Solar+Storage Adoption,’ provides direct evidence for the market trend that enables Base Power’s business model.

(Source: Worth Overdoing – Substack)

$1.2 B Valuation, Base Power Investment Signals and Market Growth

Investment is flowing into vertically integrated VPP operators, recognizing the model’s potential to capture value across the energy supply chain, from customer acquisition to wholesale market participation. Base Power‘s reported funding talks at a $1.2 billion valuation in May 2026 confirm investor confidence in this capital-efficient approach to deploying grid infrastructure.

- The overall market for distributed energy resources is expanding rapidly, with one forecast projecting growth from $48.7 billion in 2026 to $61.48 billion by 2035, creating a substantial tailwind for VPP aggregators.

- Unlike traditional utility capital expenditures on centralized power plants or large-scale grid modernization plans like Sempra’s $48 B initiative, the VPP model leverages private capital and customer acquisition to build grid assets, offering a faster and more scalable solution.

- Base Power’s approach contrasts with the asset-heavy strategy of building new dispatchable generation, such as natural gas peaker plants from providers like Baker Hughes, by instead monetizing underutilized residential capacity.

- This investment trend is underpinned by the dramatic fall in lithium-ion battery prices, which declined from $780/k Wh in 2013 to $139/k Wh in 2023, making the economics of residential battery-as-a-service viable at scale.

Base Power Secures $1B in Series C Funding

The section discusses Base Power’s ‘$1.2B Valuation’ and ‘Investment Signals.’ The chart, announcing a ‘$1B in Series C Funding’ round, directly corroborates the theme of significant investment and high valuation for the company.

(Source: LinkedIn)

Table: Base Power and DER Market Financials

| Entity / Market | Time Frame | Financial Metric and Strategic Purpose | Source |

|---|---|---|---|

| Base Power | May 2026 | Reportedly in talks to raise funding at a $1.2 billion valuation. This capital would be used to scale its VPP operations and expand its customer base in Texas and beyond. | Forbes |

| Austin Energy | 2026-2036 | Announced a 10-year, $735 million investment plan for grid resilience. The partnership with Base Power is a key component, enabling the utility to leverage DERs instead of relying solely on its own capital-intensive projects. | KXAN |

| Residential Lithium-ion BESS Market | 2023-2033 | Forecasted to grow to $68.9 billion by 2033 at a CAGR of 28.3%. This explosive growth reflects the increasing economic viability and consumer demand for home storage. | Market.us |

| Distributed Energy Resources Market | 2026-2035 | Projected to reach $61.48 billion by 2035. This broader market trend validates business models focused on aggregating and controlling distributed assets for grid services. | Business Research Insights |

Base Power Partnerships, Austin Energy and Lennar Deals Accelerate VPP Scale

Strategic partnerships with utilities and homebuilders are proving to be the primary mechanism for scaling residential VPPs, solving customer acquisition challenges and ensuring assets are concentrated in strategically valuable grid locations. Base Power‘s alliances with Lennar and Austin Energy create a blueprint for rapid, targeted deployment that standalone hardware sales cannot match.

- In April 2026, Austin Energy’s city council approved a partnership with Base Power, enabling the utility to dispatch the startup’s fleet of residential batteries to enhance local grid reliability. This represents a critical validation of the VPP model by a municipal utility.

- Beginning in 2024, a partnership with major homebuilder Lennar allowed Base Power to embed its battery and energy service directly into new home construction. This provides a highly efficient channel for acquiring thousands of customers in concentrated geographies.

- An earlier partnership with Guadalupe Valley Electric Cooperative (GVEC), announced in May 2024, demonstrated the model’s applicability to rural and co-op utility territories, expanding the addressable market beyond dense urban centers.

Table: Base Power Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Austin Energy | Apr 2026 | Partnership to integrate Base Power‘s residential VPP into Austin Energy‘s grid operations. This provides the utility with a dispatchable, non-wires alternative for managing grid constraints and enhancing local reliability. | Austin American-Statesman |

| Lennar (via Len X) | 2024 – Ongoing | Collaboration to offer Base Power‘s battery and energy plan to new homebuyers. This strategy creates entire communities of grid-interactive homes, providing concentrated capacity for the VPP. | Housing Wire |

| Guadalupe Valley Electric Cooperative (GVEC) | May 2024 | Partnership to offer the Base Power system to GVEC members. This expands Base Power‘s reach into a co-op service territory and provides GVEC with a tool for managing its local grid. | Business Wire |

Texas Grid, Base Power Focus and ERCOT Instability

Texas has become the primary geography for VPP model innovation due to the unique combination of its isolated, energy-only ERCOT market, extreme weather vulnerability, and rapid demand growth. These factors create both an urgent need for flexible grid resources and a lucrative opportunity for services like energy arbitrage and demand response, unlike more stable grid regions.

- The ERCOT grid’s isolation and fragility, exposed during Winter Storm Uri in 2021, created a strong market and regulatory driver for reliability solutions. Post-Uri, consumer demand for backup power surged, creating a receptive customer base.

- ERCOT forecasts potential supply shortfalls as early as summer 2026, driven by population growth and industrial electrification, particularly from data centers. This projected scarcity increases the value of dispatchable resources like VPPs.

- While Texas has rapidly deployed grid-scale storage, reaching 13.9 GW by early 2026, interconnection delays for new generation and transmission upgrades are creating bottlenecks. VPPs offer a way to add capacity without requiring major transmission projects.

- The price volatility in ERCOT’s wholesale market creates significant revenue opportunities for VPP operators who can perform energy arbitrage. This dynamic is less pronounced in other U.S. markets, such as the ISO-NE grid, making Texas a uniquely fertile ground for this business model.

Texas Grid Storage Capacity Explodes Past 10,000 MW

The section heading is ‘Texas Grid, Base Power Focus and ERCOT Instability.’ The chart’s headline showing that ‘Texas Grid Storage Capacity Explodes’ directly quantifies the growth and scale of the market Base Power is targeting within the Texas/ERCOT grid.

(Source: Reddit)

Commercial Scale VPP, Base Power Technology and Business Model Maturity

The core innovation driving residential VPPs is the maturation of the vertically integrated business model, not a breakthrough in battery hardware. By combining a retail electricity provider license with VPP aggregation software, companies like Base Power can control the entire value stack, a strategy that has now progressed from concept in 2023 to a commercially validated, utility-integrated solution in 2026.

- Between 2021-2024, VPPs were typically operated by third-party software companies that had to partner with multiple retail electricity providers and hardware vendors, creating a fragmented value chain and complex customer experience.

- Base Power‘s model, launched in 2024, integrated these functions. By becoming the retail provider, it directly accesses wholesale market revenue streams to subsidize the battery cost for consumers, solving the core economic challenge.

- The partnership with Austin Energy in 2026 marks a key maturity milestone. It moves the VPP from a pure merchant model (playing the wholesale market) to a contracted grid services provider for a utility, signaling a more stable, long-term revenue structure.

- The technology stack combines mature lithium-ion battery hardware with proprietary software for VPP aggregation, market bidding, and dispatch. The model’s success validates the software and market integration as the key differentiator.

Battery Market Booms as Costs Plummet

The section discusses ‘Commercial Scale VPP’ and ‘Business Model Maturity.’ The chart showing that the ‘Battery Market Booms as Costs Plummet’ explains the fundamental economic driver that makes commercial-scale VPPs a mature, viable business model.

(Source: Not Boring by Packy McCormick)

SWOT Analysis, Base Power Model and Texas Market Entry

The integrated VPP model pioneered by Base Power possesses distinct strengths in customer acquisition and a clear opportunity to address grid reliability gaps, but it faces threats from market volatility and potential regulatory shifts. The evolution from 2024 to 2026 has validated its core strengths while bringing market risks into sharper focus.

- Strengths: The low upfront cost for consumers is a powerful competitive advantage that dramatically expands the addressable market for home energy storage.

- Weaknesses: The business model’s profitability is sensitive to wholesale electricity price spreads, which can be volatile and are influenced by weather and regulatory actions.

- Opportunities: ERCOT’s looming capacity shortfalls and transmission constraints create a clear, high-value role for distributed, dispatchable resources like VPPs.

- Threats: Changes in ERCOT market rules or the introduction of new capacity market structures could alter the economics of energy arbitrage and ancillary services, impacting revenue.

Table: SWOT Analysis for Base Power’s Integrated VPP Model

| SWOT Category | 2023 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | The business model’s primary strength was its disruptive customer proposition: a low-cost battery in exchange for signing up for an electricity plan. This was largely theoretical at launch in 2024. | The model’s ability to drive rapid customer acquisition was validated through the sale of over 100 MWh of storage and the scalable Lennar partnership. | The core strength of the low-cost acquisition model was proven to work at scale, moving from a hypothesis to a demonstrated market advantage. |

| Weakness | A key weakness was the reliance on a merchant revenue model (energy arbitrage) in the volatile ERCOT market, posing a risk to financial stability. | The model’s financial structure began to de-risk through the Austin Energy partnership, which introduces a more predictable, service-based revenue stream from a utility. | The weakness of pure merchant risk was partially mitigated by securing a utility partner, validating a path towards more stable, contracted revenues. |

| Opportunity | The opportunity was defined by post-Uri consumer demand for resilience and the general need for more flexible resources on the Texas grid. | The opportunity became more acute with ERCOT’s official forecast of a potential supply shortfall by summer 2026 and Austin Energy’s own transmission upgrade delays. | The market need for VPPs shifted from a general concept to a specific, quantifiable, and near-term grid requirement, increasing the urgency and value of the solution. |

| Threat | The main threat was competition from established hardware providers like Tesla and the risk that the integrated model would not be economically viable. | Threats now include potential changes to ERCOT’s market design and increased competition from other VPP aggregators entering the Texas market. | The competitive landscape matured from legacy hardware sellers to include other service-based competitors, while regulatory risk became a more prominent factor. |

Scenario Modelling: Base Power, Utility Partnerships and VPP Replication

The most critical strategic development to watch in the coming year is the replication of the Austin Energy–Base Power partnership model by other utilities, both within Texas and in other states facing grid constraints. If other municipal utilities or cooperatives sign similar deals to use VPPs as non-wires alternatives, it will confirm a systemic shift in how utilities plan and procure grid capacity.

- If this happens: More utilities will issue RFPs specifically for VPP capacity and DER aggregation, creating a new, formalized market for companies like Base Power.

- Watch this: Pay close attention to regulatory dockets in states like Illinois and New Jersey, which have already mandated utilities to develop VPP programs. The structure of these programs will indicate the size of the opportunity outside of Texas.

- This could be happening: We may see established energy providers and utilities attempting to acquire VPP startups to vertically integrate these capabilities, rather than partnering. A move by a major utility to buy, rather than partner with, a company like Base Power would signal a major strategic validation.

The questions your competitors are already asking

This report covers one angle of Base Power’s commercial trajectory and its residential VPP model. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the Texas residential VPP market?

- Is Base Power a good investment at its $1.2B valuation target?

- What is actually happening with the Austin Energy partnership since the April 2026 announcement?

- Which Texas utilities and homebuilders are adopting residential BESS-as-a-service models?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.