Aramco Flow Battery Integration, $11 B GIP Deal, 1 MW Pilot, and Ma’aden Lithium Venture (2025 to 2026)

Aramco Storage Projects Signal Shift from Procurement to Ownership

Saudi Aramco’s initiatives in 2025 marked a strategic evolution from procuring third-party energy storage systems to developing proprietary technology and controlling the associated value chain.

- Prior to 2025, the Kingdom’s strategy was dominated by large-scale procurement of established technologies to meet ambitious grid targets. This approach shifted in 2025 toward building internal capabilities and intellectual property.

- The commissioning of a 1 MW Iron-Vanadium (Fe/V) flow battery in May 2025 at the Wa’ad Al-Shamal gas facility provides concrete evidence of this change. This patented, in-house technology is now being used to directly power Aramco‘s core hydrocarbon operations, demonstrating a move to create bespoke solutions.

- The company advanced further into vertical integration through its joint venture with Ma’aden to extract lithium from brine. This positions Aramco not just as a technology consumer, but as a future controller of critical raw materials for the battery industry.

- This long-term strategy runs parallel to massive short-term procurement needed for national goals, such as the February 2025 contract for BYD to supply 12.5 GWh of battery storage. This dual approach meets immediate demand while building sustainable, long-term competitive advantages.

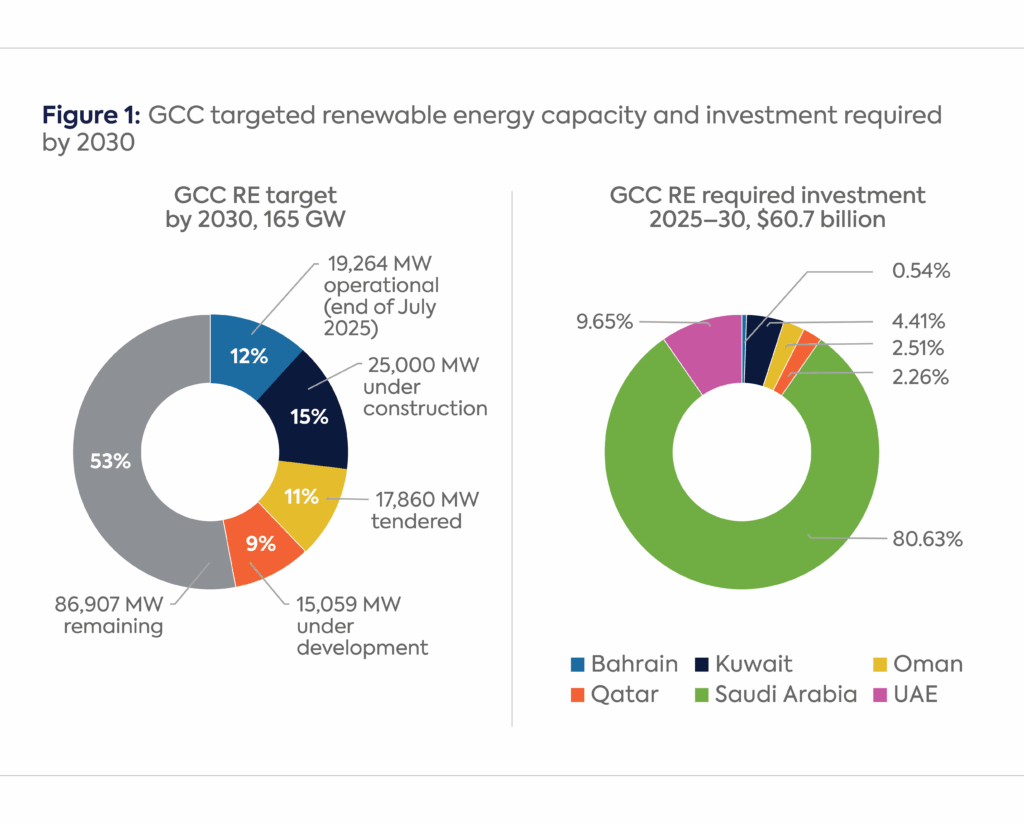

Saudi Arabia to Dominate $60.7B GCC Renewables Investment

The massive projected investment in GCC renewables, led by Saudi Arabia, provides the core economic rationale for Aramco’s strategic shift from procuring storage to owning assets. This allows Aramco to capture a larger share of the value chain created by this renewables boom.

(Source: Center on Global Energy Policy – Columbia University)

$11 B Aramco Capital Recycling Funds Energy Storage Transition

In 2025, Saudi Aramco executed a sophisticated capital recycling strategy, monetizing legacy assets to generate a dedicated funding stream for its pivot into energy storage and related transition technologies.

- The cornerstone of this financial strategy was the $11 billion lease-and-leaseback agreement for its midstream gas pipeline network, finalized in August 2025 with a consortium led by Global Infrastructure Partners.

- This transaction unlocked significant capital, explicitly intended to fund strategic initiatives and long-term growth projects, including the company’s energy diversification and manufacturing goals.

- These funds support national R&D investment, which was projected to reach $150 million in 2024, aimed at developing advanced battery technologies and improving domestic manufacturing processes.

- The investment extends beyond direct capital expenditure to include the development of proprietary intellectual property, such as the patented Fe/V flow battery, which represents a long-term value creation strategy independent of commodity cycles.

BESS Market to Reach $110B by 2035

A forecast showing the Battery Energy Storage Systems (BESS) market will grow to $110 billion provides the macro-level justification for Aramco’s significant $11 billion capital allocation, framing it as a strategic investment in a massive future market.

(Source: SNS Insider)

Table: Aramco Strategic Capital Allocation (2025-2026)

| Project / Initiative | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Corporate Bond Issuance | Mar 2026 | Successfully issued $5.0 billion in international bonds to raise capital for general corporate purposes, including strategic projects and long-term growth investments. | [PDF] Aramco | Results and performance |

| Midstream Asset Monetization | Sep 2025 | An $11 billion agreement with a Global Infrastructure Partners-led consortium to recycle capital from midstream gas assets to fund strategic initiatives, including renewables and energy storage. | Monthly Review: U.S.-Saudi Business Deals (August 2025) – USSBC |

| New Project Execution Plan | Sep 2025 | Announced plans to execute 85 new, expansion, and upgrade projects over the next three years to support strategic diversification, including into new energy markets. | Aramco plans to execute 85 projects in next three years – MEED |

| Battery R&D Investment | Jan 2025 | Total national investment in battery R&D was projected to reach $150 million in 2024, supporting efforts to develop advanced technologies and manufacturing processes within the Kingdom. | KSA Battery Manufacturing Market Outlook to 2030 – Ken Research |

Aramco 4 Key Partnerships for Technology and Supply Chain (2025)

Saudi Aramco‘s 2025 partnerships reveal a calculated strategy focused on acquiring technology, securing raw materials, and leveraging financial expertise to accelerate its energy transition.

- The joint venture with mining company Ma’aden is a critical move to establish a domestic lithium supply chain. The project aims to process brine to produce enough lithium for approximately 500, 000 electric vehicle batteries annually, directly tackling upstream supply risk.

- A technology-focused collaboration with Siemens Energy to pilot Saudi Arabia’s first Direct Air Capture (DAC) unit in Dhahran demonstrates a commitment to mitigating emissions from existing operations while building expertise in carbon removal technologies.

- The $11 billion financial partnership with Global Infrastructure Partners for midstream assets was not just a sale, but a strategic move to bring in external capital and expertise in infrastructure management, freeing up internal resources for new energy ventures.

- The company’s agreement with SLB and Linde to develop a carbon capture and storage (CCUS) hub further supports decarbonization efforts, which are directly linked to the broader clean energy transition that necessitates energy storage.

Saudi Li-Ion Market Segmented by Chemistry

This chart illustrates the specific battery chemistries within the Saudi market. It provides direct context for why Aramco would form strategic partnerships to secure technology and supply chains for these specific, in-demand chemistries like LFP and NMC.

(Source: Ken Research)

Table: Aramco Strategic Partnerships (2024-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Siemens Energy | Oct 2025 | Piloted the Kingdom’s first Direct Air Capture (DAC) unit in Dhahran to gain leadership in carbon removal technologies and address operational emissions. | [PDF] STAYING THE COURSE – Global CCS Institute |

| Global Infrastructure Partners | Sep 2025 | Signed an $11 billion lease-and-leaseback agreement for its gas pipeline network to recycle capital for strategic initiatives, including energy transition projects. | Monthly Review: U.S.-Saudi Business Deals (August 2025) – USSBC |

| Ma’aden | May 2025 | Formed a joint venture for domestic lithium production, with production planned by 2027, to build a secure supply chain for battery manufacturing. | [PDF] Localizing Renewable Energy Supply Chains in the Gulf |

| SLB, Linde | Oct 2024 | Entered a joint development agreement to establish a CCUS hub, supporting decarbonization efforts that enable the clean energy transition. | [PDF] global status of ccs 2024 – collaborating for a net-zero future |

Saudi Arabia: Aramco Builds a Protected Domestic Storage Market

Saudi Arabia is the clear epicenter of Aramco‘s energy storage strategy, with the company leveraging national policy and its own market power to create a large, protected, and rapidly growing domestic market for storage technologies.

- From 2025 onward, Saudi Arabia’s Vision 2030 and its target of deploying 48 GWh of battery storage by 2030 provide a massive, state-backed demand signal that de-risks investment. This contrasts with the more fragmented and commercially-driven markets seen before this period.

- Aramco is anchoring this domestic market with its own projects, such as the Wa’ad Al-Shamal flow battery, and by facilitating giga-scale procurements, including the 12.5 GWh BYD deal and annual tenders for 2 GW/8 GWh of BESS capacity.

- The strategy is heavily focused on localization. The establishment of the Kingdom’s first BESS manufacturing facility by ZOE Energy Storage (6 GWh annual capacity) and Aramco‘s own lithium JV are designed to build a self-sufficient ecosystem within Saudi Arabia.

- While international activity, such as the joint venture in China with Panjin Xincheng, secures demand for traditional products, it also provides the financial foundation to aggressively fund the energy transition and technology localization at home.

Saudi Battery Storage Imports Soared Pre-2025

The chart showing a pre-2025 surge in battery imports directly illustrates the problem Aramco’s strategy aims to solve. Building a ‘protected domestic market’ is a direct response to this import dependency, justifying the move to localize production.

(Source: 6Wresearch)

Aramco Flow Battery Pilot Moves from R&D to Commercial Use

In 2025, Saudi Aramco validated its long-term technology strategy by successfully moving its proprietary Iron-Vanadium flow battery from the research phase directly into a live commercial application, powering its own industrial operations.

- Prior to 2025, Aramco‘s involvement in storage was primarily as a large-scale procurer of mature Lithium-ion technology, while its own alternative chemistry research remained in development.

- The commissioning of the 1 MW/hour Fe/V flow battery at the Wa’ad Al-Shamal gas facility in May 2025 marked a pivotal transition from R&D to operations. The system is now powering up to five gas wells, proving its viability in a harsh, real-world industrial environment.

- The technology is specifically engineered to withstand Saudi Arabia’s hot climate and offers a projected 25-year lifespan, demonstrating a focus on developing solutions that overcome the limitations of standard battery technologies in the region.

- While Li-ion remains the dominant technology for immediate, large-scale grid projects, such as the 2.5 GW grid-forming BESS commissioned in 2026, Aramco‘s successful Fe/V pilot creates a viable path for a technologically diversified storage portfolio, particularly for long-duration applications.

Electrochemical Storage to Dominate Growing Market

As Aramco moves a flow battery pilot to commercial use, this chart provides context by showing that the broader category of electrochemical storage is the dominant market segment. This validates investing in new electrochemical alternatives to lithium-ion.

(Source: Polaris Market Research)

SWOT Analysis of Aramco’s Vertically Integrated Storage Strategy

Saudi Aramco‘s 2025 energy storage strategy combines immense financial strength and project execution capability with the inherent risks of pioneering new technologies and building nascent supply chains from the ground up.

Key Factors Driving Energy Storage Market

This chart directly complements a SWOT analysis by outlining market ‘Opportunities.’ The factors listed—such as grid modernization and renewable integration—are the external drivers that support Aramco’s vertically integrated storage strategy.

(Source: Coherent Market Insights)

Table: SWOT Analysis for Aramco’s Energy Storage Initiatives

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Access to state capital; world-class project management expertise in giga-projects. | All previous strengths, plus now holds proprietary IP with the patented Fe/V flow battery; executing a clear vertical integration strategy (lithium). | The company validated its ability to move from funding R&D to deploying its own patented technology in a commercial setting. |

| Weaknesses | High reliance on foreign technology and supply chains for batteries (e.g., from China, South Korea). | Execution risk for its new, unproven technology at scale; developing a lithium supply chain from scratch carries significant geological and processing risk. | The weakness shifted from reliance on others to the internal challenge of executing a complex, multi-stage industrial strategy. |

| Opportunities | Meet domestic renewable energy targets under Vision 2030; diversify revenue away from oil. | Become a global technology provider for hot-climate energy storage; control a regional battery supply chain from materials to manufacturing. | The opportunity expanded from being a large customer to becoming a technology and materials leader in the new energy economy. |

| Threats | Global competition on BESS pricing; supply chain disruptions for key components. | Competing flow battery or long-duration storage technologies maturing faster; failure of its own Fe/V technology to scale economically; geopolitical risks impacting lithium processing. | The threat evolved from market-based risks (prices) to more fundamental technology and execution risks tied to its own strategy. |

Aramco 2026: Watch for Flow Battery Scale-Up Post 1 MW Pilot

The most critical indicator to watch in 2026 will be whether Saudi Aramco scales its proprietary Iron-Vanadium flow battery technology beyond the initial pilot phase into larger grid or industrial applications.

- If this happens: An announcement of a multi-megawatt or grid-scale Fe/V flow battery project would validate the technology’s commercial readiness and signal a serious challenge to the dominance of Lithium-ion for long-duration storage, especially in hot climates.

- Watch this: Monitor announcements related to the Saudi Power Procurement Company’s annual 2 GW/8 GWh BESS tenders. A specific carve-out or requirement for non-lithium, long-duration storage would be a strong policy signal supporting Aramco‘s technology.

- These could be happening: Internally, Aramco is evaluating performance data from the Wa’ad Al-Shamal pilot to identify the next optimal use case. This could be for expanded industrial operations or integration into one of the Kingdom’s large-scale renewable energy projects. Watch for new patent filings or targeted hiring of battery and material science engineers.

Saudi Solar Storage Market to Hit $728M by 2033

This chart provides a specific, tangible domestic market opportunity ($728M) that justifies Aramco’s plan to scale up its flow battery technology. Solar+storage is a key application for flow batteries, making the scale-up commercially logical.

(Source: openPR.com)

The questions your competitors are already asking

This report covers one angle of Saudi Aramco’s vertical integration strategy in the energy storage market. The questions that matter most depend on your work.

- Aramco activities in flow batteries. Is the 1 MW Iron-Vanadium pilot progressing from pilot to utility-scale deployment?

- Aramco investments and funding. Is the Ma’aden lithium extraction venture on track to support the Kingdom’s battery manufacturing targets?

- How does Aramco’s proprietary Iron-Vanadium flow battery compare to the BYD lithium-ion systems it is also procuring for grid-scale applications?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.