Exxon Mobil BESS Supply Chain, $20 B Investment, Superior Graphite Acquisition, and 2 Key Projects (2025)

Lithium Supply Chain Risk, Exxon Mobil’s Upstream Focus and Midstream Gap

In 2025, Exxon Mobil executed a strategic pivot into the battery materials market by focusing on upstream production, a move that leverages its core competencies but exposes the vulnerability of the entire U.S. supply chain due to a critical gap in midstream processing. This strategy shifts the company from a position of observation prior to 2024 to an active participant aiming to establish a domestic supply of critical battery inputs, yet its success is inextricably linked to the development of a national refining infrastructure that does not yet exist at scale.

- Prior to 2025, Exxon Mobil’s involvement in the battery sector was minimal. The significant shift occurred in 2025 with the establishment of the Mobil Lithium brand and a clear focus on developing lithium resources from the Smackover Formation in Arkansas, targeting a 2027 production start.

- The company further solidified its upstream position in September 2025 by acquiring Superior Graphite. This transaction secured technology and U.S.-based assets to produce synthetic graphite for battery anodes, another critical raw material, with a goal for commercial production by 2029.

- The primary industry risk is the lack of domestic midstream refining capacity. Raw lithium extracted via Direct Lithium Extraction (DLE) must be converted into battery-grade lithium carbonate or hydroxide. With current infrastructure, this processing largely occurs in Asia, undermining the strategic goal of a resilient domestic supply chain.

- This strategic entry is driven by immense market demand, with the global EV market projected to hit 25 million units in 2025. Exxon Mobil’s goal is to secure a share of this market and reduce reliance on China, which currently controls approximately 70% of global lithium battery production.

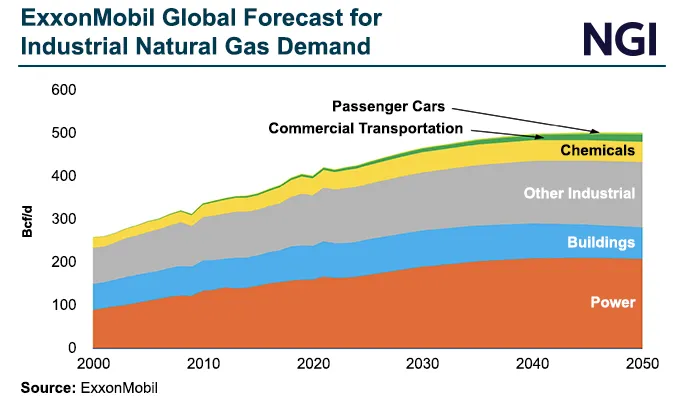

ExxonMobil Sees Natural Gas Demand Growing to 2050

The section heading refers to ExxonMobil’s ‘Upstream Focus.’ This chart, showing the company’s bullish projection for natural gas, directly illustrates and justifies its continued investment in its core upstream business.

(Source: Natural Gas Intelligence)

$20 B Low-Carbon Plan, Exxon Mobil Investment Strategy and Policy Dependence

Exxon Mobil’s financial commitment to its energy transition strategy is substantial, but its economic viability remains heavily dependent on supportive government policy, particularly the tax incentives provided by the Inflation Reduction Act (IRA). The company’s 2025 investment plans reveal a disciplined approach to funding new ventures like battery materials through cost savings and efficiency, rather than a blank-check expansion, making the stability of federal credits a critical factor for future growth.

- In December 2025, Exxon Mobil confirmed plans to allocate approximately $20 billion toward lower-emission investments between 2025 and 2030. This capital is designated for a portfolio including carbon capture, hydrogen, biofuels, and its new battery materials business.

- The company’s updated corporate plan, also announced in December 2025, aims to generate an additional $5 billion in earnings and cash flow growth by 2030 without increasing overall capital expenditures. This highlights a strategy of funding new ventures through structural cost reductions, which reached $1.4 billion year-to-date as of September 2025.

- Company executives have explicitly stated that these low-carbon investments are contingent on the continuation of federal support mechanisms like the 45 Q and 45 V tax credits. This policy dependence makes the projects vulnerable to political shifts and potential legislative changes to the IRA.

ExxonMobil’s Low-Carbon Solutions Portfolio Visualized

This chart directly visualizes the components of ExxonMobil’s low-carbon business (CCS, Hydrogen, Biofuels), which is the core subject of the section discussing the company’s $20 billion low-carbon investment plan.

(Source: ExxonMobil)

Table: Exxon Mobil Strategic Investments and Financial Plans (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Low-Carbon Solutions | 2025-2030 | Allocation of $20 billion in capital for lower-emission projects, including CCS, hydrogen, and battery materials like lithium. This is a reduction from a previous $30 billion target but remains a significant commitment. | edie |

| Corporate Plan Growth | By 2030 | Strategy to increase earnings and cash flow by an incremental $5 billion compared to the prior plan, with no increase in total capital spending, funding new ventures through operational efficiency. | Exxon Mobil |

| Structural Cost Savings | YTD 2025 | Achieved $1.4 billion in year-to-date structural cost savings, on track for a cumulative $18 billion. These savings free up capital for strategic investments in growth areas like battery materials. | Financial Content |

| Superior Graphite | Sep 2025 | Acquisition of technology and U.S.-based assets to establish a domestic supply chain for synthetic graphite for EV battery anodes, targeting commercial production by 2029. | Exxon Mobil |

Exxon Mobil 2025 Alliances, Next Era and Calpine CCS Deals

In 2025, Exxon Mobil focused its partnership activity on its more mature low-carbon businesses, particularly carbon capture, rather than on new battery material joint ventures. These collaborations with major energy players like Next Era Energy demonstrate a consistent strategy of leveraging large-scale infrastructure partnerships to build out its energy transition portfolio, a model it will likely apply to its lithium business as it matures.

- On December 8, 2025, Exxon Mobil announced a partnership with Next Era Energy Resources to develop carbon-abated, gas-fired power generation projects. This alliance combines Exxon Mobil’s carbon capture and storage (CCS) capabilities with Next Era’s power generation portfolio to create lower-emission baseload electricity.

- The acquisition of Superior Graphite in September 2025 represents a different kind of partnership, one of vertical integration. By purchasing the company’s technology and assets, Exxon Mobil brought critical anode material expertise in-house to build a domestic supply chain.

- While not a direct partnership, the competitive environment in the Smackover Formation was highlighted in January 2025 when the U.S. Department of Energy awarded a grant to a joint venture between Standard Lithium and Equinor for DLE development in the same region, signaling strong federal interest and intensifying regional activity.

ExxonMobil Details Path to Lower GHG Intensity

The section discusses specific Carbon Capture and Storage (CCS) deals. This chart illustrates the strategic goal of those alliances—lowering greenhouse gas intensity—thereby connecting the specific actions to the broader objective.

(Source: ExxonMobil)

Table: Exxon Mobil Energy Transition Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Next Era Energy | Dec 2025 | Collaboration to develop carbon-abated, gas-fired power generation, integrating CCS with power infrastructure. | Next Era Energy |

| Superior Graphite | Sep 2025 | Acquisition of technology and key U.S. assets to become a domestic supplier of synthetic graphite for battery anodes. | Exxon Mobil |

| Standard Lithium (Competitor) | Jan 2025 | A Department of Energy grant was awarded to a competitor’s joint venture for DLE development in the same Smackover region where Exxon Mobil operates, validating the area’s strategic importance. | Standard Lithium |

Arkansas vs. Global Supply, Exxon Mobil’s US-Centric Lithium Focus

Exxon Mobil’s 2025 strategy for battery materials is geographically concentrated in the United States, specifically Arkansas, representing a decisive move to onshore a critical part of the EV supply chain. This domestic focus contrasts sharply with the pre-2025 period of global resource evaluation and marks a deliberate effort to build a North American-centric business, though it remains exposed to the globalized nature of midstream refining.

- From 2021 to 2024, Exxon Mobil’s public activity in battery materials was negligible. The year 2025 marked a clear geographical pivot to the U.S. with the announced development of lithium resources in the Smackover Formation in southern Arkansas.

- This U.S. focus was reinforced by the acquisition of Superior Graphite’s domestic assets, ensuring that its planned synthetic graphite production will also be based in the United States, further strengthening its “Made in America” supply chain narrative.

- The primary geographic challenge is the disconnect between domestic upstream extraction and the global midstream market. With most battery-grade lithium refining capacity located in Asia, particularly China, the raw materials extracted in Arkansas face a long and geopolitically sensitive journey before they can be used in U.S. battery plants. Addressing this gap is critical for the long-term viability of the ASEAN grid and other regional power systems.

Battery Demand to Surge with Renewables Growth

This chart provides the essential market rationale for ExxonMobil’s US-centric lithium focus by showing that the demand for batteries (and thus lithium) is surging due to the growth of renewables.

(Source: Springer Nature)

Commercial Scale DLE, Exxon Mobil’s Technology Readiness and Hurdles

The technological foundation of Exxon Mobil’s battery materials strategy is Direct Lithium Extraction (DLE), a technology that moved from pilot phases to a central pillar of corporate strategy in 2025. The company’s success now depends on its ability to scale DLE from demonstration to a commercially viable and cost-competitive industrial process, a significant technical and economic hurdle.

- Prior to 2025, DLE was considered an emerging technology largely in pilot stages across the industry. In 2025, Exxon Mobil fully committed to DLE for its Arkansas project, classifying it at a high level of technology readiness (TRL 7-8) and leveraging its extensive subsurface engineering and fluid management expertise.

- DLE offers a more efficient and environmentally smaller footprint compared to traditional hard-rock mining or evaporation ponds by selectively extracting lithium from brine. This allows Exxon Mobil to utilize its century-long experience in managing underground resources.

- The critical challenge is achieving cost-competitiveness at an industrial scale. With competitor operating costs for lithium carbonate averaging around $4, 500 per tonne, Exxon Mobil must prove it can meet or beat this benchmark to succeed commercially.

- Alongside DLE, the company announced a novel synthetic graphite molecule in September 2025. This innovation, backed by the Superior Graphite acquisition, is designed to improve battery performance and signals a dual-pronged technological push into both anode and cathode material supply chains.

SWOT Analysis, Exxon Mobil’s Battery Materials Pivot Strengths and Risks

Exxon Mobil’s 2025 strategic entry into battery materials is built upon its formidable strengths in capital allocation and project execution, but it faces significant market weaknesses and external threats related to policy dependence and supply chain gaps. The year 2025 was pivotal in crystallizing both the opportunity and the inherent risks of this diversification.

- Strengths: The company is leveraging its vast capital resources and deep technical expertise in subsurface engineering, turning legacy oil and gas skills into a competitive advantage for lithium extraction.

- Weaknesses: A primary weakness is the current lack of a complete domestic supply chain, particularly for midstream refining, which forces reliance on foreign processing.

- Opportunities: The strategy positions Exxon Mobil to capture growth in the booming EV and energy storage markets while capitalizing on U.S. government incentives for onshoring critical supply chains.

- Threats: The most significant threats are the project’s stated dependence on the Inflation Reduction Act, making it vulnerable to political shifts, and the intense cost competition from established global lithium producers.

Fossil Fuels Must Decline For Paris Climate Goals

This chart perfectly visualizes the primary ‘Threat’ in a SWOT analysis for an oil and gas major. It shows the external pressure that necessitates Exxon’s strategic pivot into battery materials.

(Source: Carbon Tracker Initiative)

Table: SWOT Analysis for Exxon Mobil’s Battery Materials Initiative

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Vast capital and subsurface expertise existed but were not applied to batteries. | Leveraged core competencies for DLE in Arkansas. Acquired Superior Graphite for anode expertise. | The company validated its ability to translate oil and gas skills directly to the battery materials upstream sector. |

| Weaknesses | No experience in the battery market or with key materials like lithium and graphite. | Entered the market under the Mobil Lithium brand; however, the lack of midstream refining capacity in the U.S. became a clear strategic weakness. | The 2025 strategy confirmed that while Exxon Mobil can manage upstream extraction, it cannot single-handedly solve the midstream processing gap. |

| Opportunities | The EV and energy storage markets were growing, and onshoring was a political goal. | Announced the Arkansas lithium project to directly target the EV market. The $20 B low-carbon plan is designed to capitalize on IRA incentives. | The company formally committed to capturing the onshoring opportunity, moving from concept to a concrete project plan. |

| Threats | Risks included commodity price volatility and competition from established low-cost producers. | Dependence on IRA tax credits was explicitly confirmed. The challenge of competing with producers at $4, 500/tonne cost basis was quantified. | The economic model for the new ventures was validated as being highly sensitive to both policy stability and global market prices. |

Exxon Mobil 2026 Outlook, Offtake Agreements and DLE Scaling

The most critical near-term signal for Exxon Mobil’s battery materials strategy will be the announcement of its first binding offtake agreements. Securing contracts with major automotive or battery manufacturers would serve as the primary commercial validation of its multi-billion-dollar DLE venture, de-risking the project ahead of its planned 2027 production start.

- If Exxon Mobil secures offtake agreements for Mobil Lithium, watch for the partners involved. Deals with major U.S., European, or Korean automakers would signal strong market confidence in its ability to deliver battery-grade material at scale.

- These could be happening: pilot plant results from the Arkansas site. Monitor for any announcements regarding the operational efficiency, lithium recovery rates, and projected cost per tonne from its DLE demonstration facility, as this data will determine its future cost-competitiveness.

- Watch for any further moves in vertical integration, particularly investments or partnerships aimed at closing the midstream refining gap. An investment in a U.S.-based lithium conversion facility would be a major strategic development. Continued investment in carbon capture, such as projects with Deep Sky, will also signal its commitment to the broader low-carbon portfolio.

Exxon’s 2025 Outlook on Global Energy Demand

This chart is a perfect match, as it details Exxon’s specific outlook on energy demand, providing the direct market context for the company’s 2026 outlook and scaling plans discussed in the section.

(Source: ExxonMobil)

The questions your competitors are already asking

This report covers one angle of ExxonMobil’s upstream investment in the battery supply chain. The questions that matter most depend on your work.

- ExxonMobil activities in the battery supply chain. Is the Mobil Lithium initiative progressing from announcement to commercial production?

- ExxonMobil investments and funding. Is the lithium project in the Smackover Formation on track for its 2027 production target?

- Which companies are gaining or losing ground in the U.S. lithium supply chain with ExxonMobil’s entry?

- What are the opportunities for midstream refiners to process lithium from ExxonMobil’s Smackover Formation?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.