Shell Green Hydrogen, 100 MW REFHYNE 2 Project, £14 M Supercritical Deal, and 2 European PPAs (2025)

Green Hydrogen Offtake Risk, Shell’s 100 MW Captive Demand Strategy

In 2025, the central challenge for green hydrogen projects shifted from production feasibility to demand certainty, compelling major players like Shell to adopt a de-risked strategy centered on captive offtake. This pivot reflects a market-wide recalibration where the speculative ambition of the 2021-2024 period collided with the economic reality that few third-party buyers are willing to sign long-term, bankable offtake agreements. Shell‘s actions demonstrate that securing an internal, guaranteed customer is currently the most viable path to advancing commercial-scale projects.

- The company’s most significant progress was on the 100 MW REFHYNE 2 project in Germany, which will produce up to 16, 000 tonnes of green hydrogen annually, primarily to decarbonize Shell‘s own Energy and Chemicals Park. This captive demand model solves the offtake uncertainty that plagues the broader market, where developers struggle to secure buyers for more than 10-15% of planned output.

- This focused approach in Europe contrasts sharply with Shell‘s decision in January 2025 to pause a green hydrogen pilot at Brazil’s Port of Açu. The move was explicitly framed as a strategic refocus on higher-return projects with clearer demand, underscoring the shift away from speculative, market-building activities.

- The underlying driver for this strategic pivot is the persistent cost gap. Green hydrogen production costs in 2025 range from $4 to $12 per kilogram, significantly higher than the $1-$3/kg for grey hydrogen, making projects economically unviable without both subsidies and a guaranteed buyer.

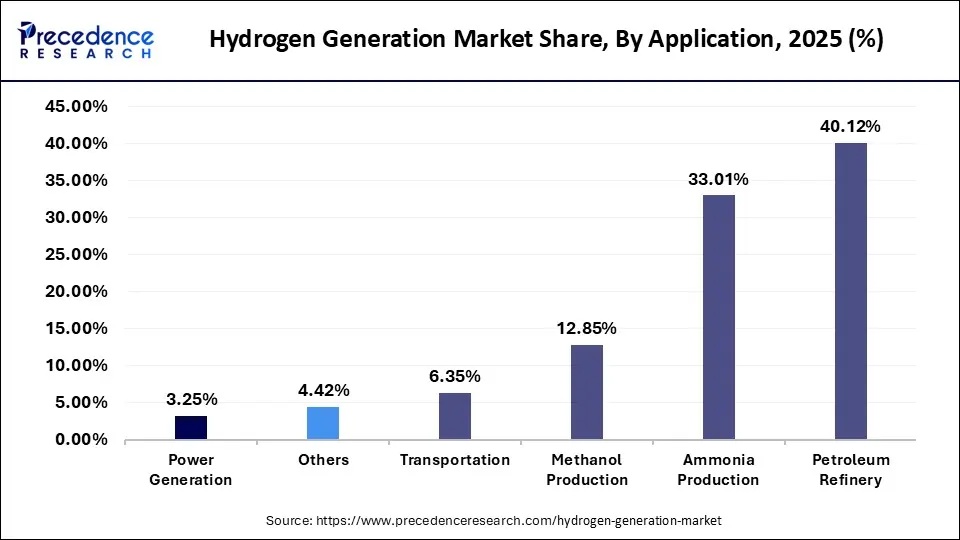

Refineries and Ammonia Dominate 2025 Hydrogen Demand

The chart directly supports Shell’s captive demand strategy by showing that refineries—a core part of Shell’s business—are a dominant source of hydrogen demand. This validates the strategy of producing hydrogen for its own use to mitigate offtake risk.

(Source: Precedence Research)

£14 M Venture Deal, Shell’s Green Hydrogen Investment Pivot

Shell‘s 2025 investment activities reveal a disciplined capital allocation strategy, pivoting away from large-scale renewable generation projects toward targeted venture investments in cost-reduction technologies. This dual approach allows the company to reduce its near-term capital exposure to high-cost projects while maintaining a strategic position in the technologies needed for long-term cost parity. This marks a significant change from the preceding years, which were characterized by larger, more expansive greenfield announcements.

- In March 2025, Shell Ventures co-led a £14 million investment in Supercritical, a UK startup developing a novel, high-efficiency electrolyzer. This move directly targets the industry’s primary barrier, high production costs, by backing a technology that could make green hydrogen more competitive.

- The venture investment occurred alongside a broader strategic update in March 2025 where Shell announced plans to halve green investments and boost natural gas sales. This highlights a clear prioritization of shareholder returns and operational integration over expansive, high-risk green energy development.

- This investment pivot was further solidified by the decision to pause the Brazil green hydrogen pilot. By deferring capital expenditure on a project with an uncertain offtake market, Shell preserved capital for its core European projects and low-cost technology bets.

Green Hydrogen Market to Reach $242B by 2035

This chart provides the essential market context for Shell’s investment pivot. The massive projected market size of $242B justifies significant venture deals and strategic shifts towards green hydrogen, framing the £14M deal as a move to capture a share of a lucrative future market.

(Source: Market Research Future)

Table: Shell’s Key Hydrogen Investment and Divestment Activities (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Green Investment Program | March 2025 | Announced a plan to more than halve its exposure to wind and solar farms, signaling a major reduction in capital allocation for the renewable generation required for green hydrogen. | The Telegraph |

| Supercritical | March 2025 | Co-led a £14 million investment in a high-efficiency electrolyzer startup. This is a low-capital move to secure a stake in technology that could lower future hydrogen production costs. | Supercritical |

| Port of Açu Pilot | January 2025 | Paused a planned green hydrogen pilot in Brazil, citing a strategic refocus on higher-return projects in Europe with more stable market conditions and clearer internal demand. | Fuel Cells Works |

Key Players in Green Hydrogen for 2025

This chart complements a table of Shell’s investment activities by providing the competitive landscape. It helps to position Shell’s actions relative to other key players in the green hydrogen space, offering a broader context for its strategic decisions.

(Source: LinkedIn)

Europe vs. Global Projects, Shell’s Geographic Green Hydrogen Focus

In 2025, Shell deliberately consolidated its green hydrogen ambitions into a tight geographic focus on Europe, specifically Germany and the Netherlands. This regional concentration is driven by a combination of stable regulatory frameworks, proximity to Shell‘s existing industrial assets, and access to mature renewable energy markets. The strategy involves building integrated energy hubs where renewable power generation, hydrogen production, and industrial consumption are co-located.

- The epicenter of Shell‘s strategy is Germany, where the company secured two critical Power Purchase Agreements (PPAs) in November 2025 to supply its REFHYNE 2 project. These include a deal with Nordsee One for offshore wind power and another with Solarkraftwerk Halenbeck-Rohlsdorf for solar power, ensuring a supply of renewable electricity.

- This European focus is further demonstrated by the continued development of the 200 MW Holland Hydrogen I project in Rotterdam. Like REFHYNE 2, this facility is designed to supply green hydrogen directly to Shell‘s own nearby refinery, reinforcing the captive demand model.

- This consolidation in Europe occurred at the direct expense of projects in other regions. The pausing of the Brazilian pilot project in January 2025 was a clear signal that Shell is prioritizing markets with established policy support, such as the EU’s Renewable Energy Directive, over regions with higher perceived risk or less-developed market structures.

Europe Leads 2025 Low Carbon Hydrogen Market

The chart is a perfect match for the section’s heading, which focuses on Shell’s geographic priorities. It visually confirms that Europe is the leading market, explaining why Shell has a strong geographic focus on the region for its green hydrogen projects.

(Source: maximize market research)

Electrolyzer Technology, Shell’s Focus on Cost and Commercial Scale

While the core technology for water electrolysis is commercially mature, its high capital and operational costs remain the single largest impediment to the widespread adoption of green hydrogen. Shell‘s 2025 strategy addresses this by deploying existing technology at scale to gain operational expertise while simultaneously investing in next-generation solutions designed to bring down the long-term cost curve. This dual-track approach acknowledges that today’s technology is not yet sufficient for cost-competitive production.

- Projects like Holland Hydrogen I and REFHYNE 2 are being built using established Proton Exchange Membrane (PEM) electrolysis technology. While reliable, this technology results in a production cost of $4-$12/kg, making it dependent on government subsidies and high carbon prices to compete with incumbent grey hydrogen.

- The £14 million investment in Supercritical represents Shell‘s effort to break this cost dependency. Supercritical’s technology aims to improve electrolyzer efficiency, which is a critical lever for reducing the levelized cost of hydrogen and achieving the industry’s long-term target of below $2/kg.

- By operating the 10 MW REFHYNE 1 project, advancing the 100 MW REFHYNE 2, and investing in disruptive technology, Shell is building a comprehensive understanding of electrolysis. This covers everything from the practical challenges of integrating electrolyzers with intermittent renewables to the fundamental science of next-generation materials and designs.

PEM Electrolysis to Lead Hydrogen Tech Growth

The section discusses Shell’s focus on electrolyzer technology for commercial scale, and this chart highlights the projected growth of a leading technology, PEM electrolysis. This directly relates to the technological considerations and investment direction Shell would be exploring.

(Source: MarketsandMarkets)

SWOT Analysis, Shell’s 2025 Green Hydrogen Strategy

Shell‘s 2025 green hydrogen strategy leverages its core strengths as an integrated energy producer to exploit the clear opportunity of decarbonizing its own assets. However, this approach remains vulnerable to fundamental market weaknesses, such as high production costs, and external threats from volatile energy policies. The key change from prior years is the validation that a self-contained, de-risked approach is necessary in the current market.

Green Hydrogen Market To See 32.7% CAGR

This chart quantifies the ‘Opportunity’ aspect of a SWOT analysis. The specific and high Compound Annual Growth Rate (CAGR) of 32.7% provides a powerful data point to illustrate the market’s rapid expansion, which is a key external factor influencing Shell’s strategy.

(Source: Evolvance Market Research)

Table: SWOT Analysis for Shell’s Green Hydrogen Initiatives in 2025

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Broad global footprint and engineering capabilities were seen as strengths for deploying projects anywhere in the world. | Integrated assets, particularly refineries and chemical parks in Europe, provide a ready-made source of captive demand for green hydrogen. | The definition of strength narrowed from a global operational reach to the specific value of co-located industrial assets that can act as guaranteed offtakers. |

| Weakness | The high cost of green hydrogen was acknowledged as a long-term challenge to be solved with scale. | The high production cost ($4-$12/kg) is an immediate barrier, making projects unbankable without subsidies and captive offtake, limiting scalable deployment. | The weakness shifted from a future problem to a present-day constraint that actively forced the strategic pivot away from speculative projects like the one in Brazil. |

| Opportunity | The opportunity was seen as building a new global market for traded hydrogen and establishing first-mover advantage. | The primary opportunity is to use green hydrogen to decarbonize Shell‘s own operations, meet regulatory requirements, and gain operational expertise in a de-risked environment. | The opportunity was scaled back from creating a new global energy market to the more pragmatic goal of using hydrogen for internal decarbonization and risk management. |

| Threat | Threats included competition from other energy majors and the pace of renewable energy deployment. | Policy uncertainty, such as the political threats to the U.S. 45 V tax credit, and the lack of binding offtake agreements from third parties create significant market risk. | The threat of unstable government support became a validated, active risk in 2025, reinforcing Shell‘s decision to focus on Europe’s more stable, albeit complex, regulatory environment. |

Green Hydrogen Demand to Surge in Power & Chemicals

Complementing a SWOT analysis table, this chart details *where* the demand growth is coming from (Power & Chemicals). This information is crucial for strategic planning and assessing the viability of targeting specific end-use sectors, adding depth to the SWOT’s ‘Opportunities’.

(Source: Market Research Future)

The 2027 Milestone, Shell’s REFHYNE 2 Project Execution

The most critical signal for Shell‘s green hydrogen strategy is the successful execution of the REFHYNE 2 project, which is scheduled for a 2027 operational start. This project serves as the real-world test for the company’s captive demand model. Its progress will determine whether this focused, de-risked approach can serve as a scalable template for decarbonizing other industrial assets.

- If construction and commissioning of REFHYNE 2 proceed on schedule and within budget, watch for Final Investment Decisions (FIDs) on similar large-scale electrolyzer projects at other Shell chemical parks. This would confirm the viability and replicability of the captive model.

- If Shell announces a significant, long-term offtake agreement for green hydrogen with a third-party entity, this could mean a strategic evolution from a self-consumption model to becoming a broader market supplier. This would signal confidence that production costs are falling enough to compete for external customers.

- If the technology from Supercritical is successfully piloted at a Shell facility, watch for its inclusion in the design of future projects. A successful pilot would be the first tangible sign that a path to cost-competitive green hydrogen, independent of subsidies, is emerging.

Green Hydrogen Market To See Explosive Growth

The chart’s headline about explosive market growth provides the high-level justification for undertaking large, capital-intensive projects like REFHYNE 2. It frames the project not as an isolated effort but as a strategic move to capitalize on a rapidly expanding market.

(Source: MarketsandMarkets)

The questions your competitors are already asking

This report covers one angle of Shell’s captive demand strategy for commercial-scale green hydrogen. The questions that matter most depend on your work.

- Which energy majors are gaining or losing ground in the commercial-scale green hydrogen market?

- Shell’s investments and funding. Is the 100 MW REFHYNE 2 project on track for its 2025 commissioning target?

- What is the cost breakdown of a 100 MW-scale green hydrogen project like REFHYNE 2?

- Which refiners and chemical park operators are adopting a captive demand strategy for green hydrogen?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.