Solar Growth in 2026: Why Battery Storage Is No longer Optional

Solar Project Viability: How Battery Storage Integration Became Mandatory

By 2025, the viability of new, large-scale solar projects shifted from being measured by peak generation capacity to a dependency on integrated battery energy storage systems (BESS). The market now requires solar assets to be dispatchable, grid-stabilizing resources, a fundamental change from the standalone photovoltaic (PV) projects that characterized the sector between 2021 and 2024. This evolution is driven by grid constraints and the demand for reliable, 24/7 carbon-free energy.

- In the 2021-2024 period, battery storage was often a value-add. However, landmark 2024 announcements signaled it was becoming a core requirement. The most significant of these was Google’s partnership with Intersect Power to develop co-located energy parks, backed by a $20 billion investment plan to provide constant, clean power to data centers, a goal unachievable with intermittent solar alone.

- The project pipeline in 2024 was dominated by hybrid systems. For example, Canadian Solar’s e-STORAGE division secured a deal in July 2024 to supply a massive 498 MWh of its Sol Bank battery solutions for Aypa Power’s Bypass Project in Texas, highlighting that storage capacity is now a defining project metric.

- This market maturation is reflected in the financial landscape of 2025. While global solar installations are stabilizing at a projected 493 GWdc, overall corporate funding contracted by 16% to $22.2 billion. This indicates a flight to quality, with capital flowing towards de-risked, dispatchable assets rather than purely speculative PV capacity.

- The operational reality of this integration was proven by projects reaching commercial operation. In May 2024, SN Aboitiz Power Group’s 24 MW/32 MWh Magat BESS project in the Philippines went live, demonstrating the model of co-locating storage with renewable assets to enhance grid services.

Solar Investment 2026: Capital Shifts to Integrated Energy Systems

The 16% year-on-year decrease in solar corporate funding in 2025 does not signal a market decline but a strategic pivot by investors. Capital is now decisively moving away from speculative, standalone PV ventures and toward more capital-intensive, lower-risk integrated Solar + Storage projects that offer multiple revenue streams and act as critical grid infrastructure.

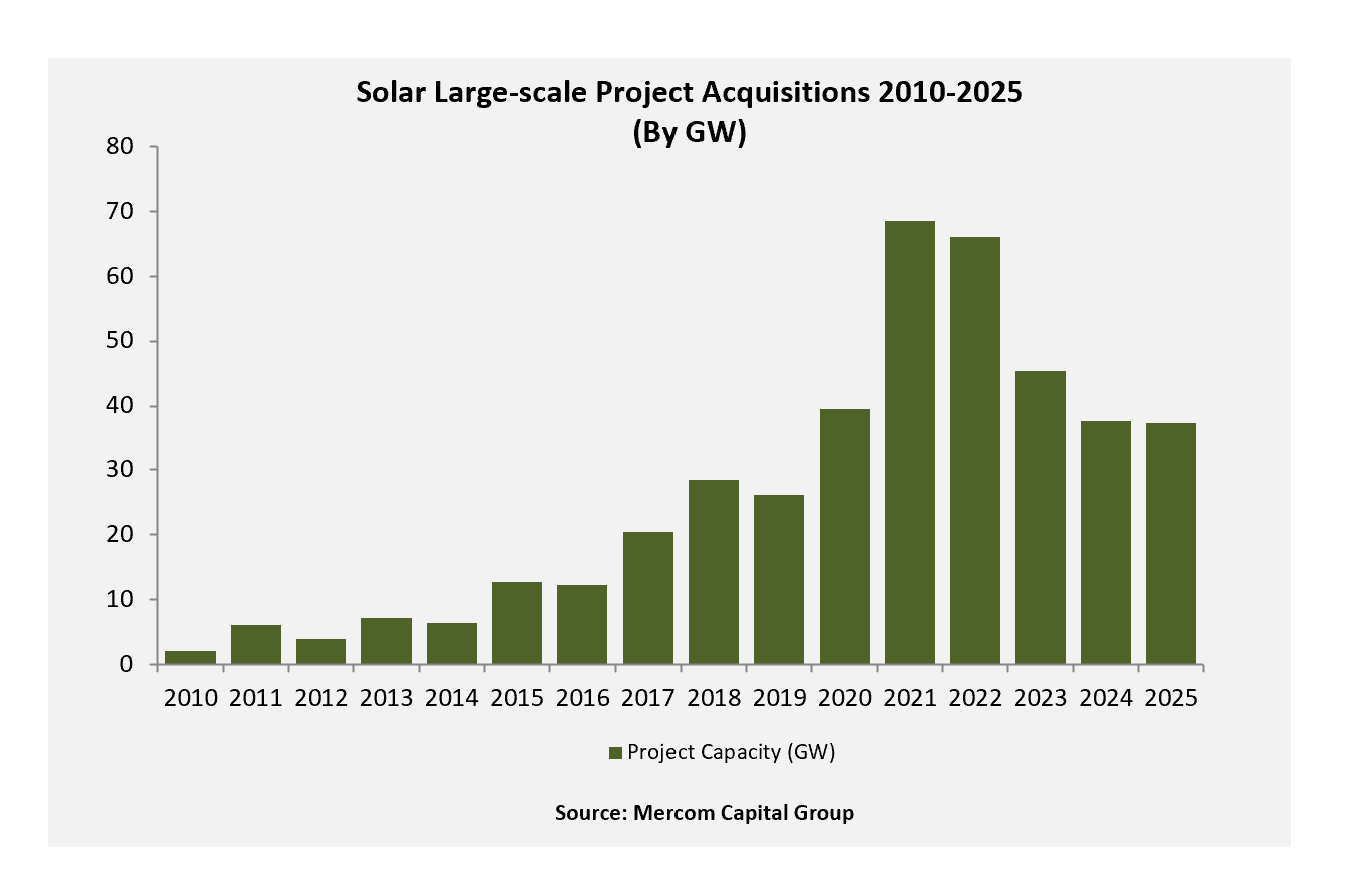

Solar Project Acquisitions Decline After 2022 Peak

This chart shows the decline in traditional project acquisitions mentioned in the text, providing the quantitative backdrop for the section’s argument about a strategic capital pivot towards integrated systems.

(Source: Mercom Capital Group)

- The $20 billion investment framework announced by Google and Intersect Power in late 2024 is the clearest evidence of this shift. Capital is being allocated to “energy parks” designed for 24/7 reliability, establishing a new precedent for corporate renewable procurement that fundamentally requires storage.

- Public funding is reinforcing this trend. In May 2024, the U.S. Department of Energy announced its STRIVES program, providing up to $31 million for R&D focused on integrating and validating solar technologies within the power system, directly addressing the challenges of intermittency that BESS resolves.

- Merger and acquisition activity in 2025 underscores a focus on mature, integrated portfolios. Transactions reached valuations of $2.3 billion for companies like Plenitude and AYANA, with institutional investors such as Ares, TPG, and Brookfield acquiring established assets that increasingly include storage capacity.

Table: Key Investments in Solar + Storage Integration

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google / Intersect Power | Dec 2024 | A $20 billion investment plan for co-located solar and storage parks. The strategic purpose is to power data centers with 24/7 carbon-free energy, setting a new standard for corporate PPAs. | Utility Dive |

| U.S. Department of Energy (STRIVES Program) | May 2024 | Up to $31 million in funding for R&D to improve power systems simulation and validation. This directly supports the technical integration of solar and storage into the grid. | U.S. Department of Energy |

| International BESS Consortium | 2024 Goal | A consortium of over 10 countries aimed to secure 5 GW of BESS commitments by the end of 2024. This initiative creates a massive, government-backed market for energy storage deployment. | Global Energy Alliance |

Solar Partnerships 2026: Alliances Form to Deliver Dispatchable Power

Strategic partnerships formed in 2024 and 2025 have coalesced around the singular goal of combining solar generation with energy storage. These alliances are no longer just about project development; they represent the formation of new value chains designed to produce and sell reliable, dispatchable clean power as a service.

Solar M&A Activity Highlights Major 2025 Investments

This chart exemplifies the large-scale M&A investments occurring in the solar sector, mirroring the types of high-value deals detailed in the section’s table.

(Source: Mercom Capital Group)

- The alliance between energy consumer and developer, epitomized by the Google and Intersect Power deal, creates a powerful demand-pull for integrated assets. This model is becoming the blueprint for decarbonizing energy-intensive sectors like data centers.

- Component manufacturers are repositioning themselves as key solution providers in this new ecosystem. Canadian Solar’s e-STORAGE arm is not just a panel maker but a critical BESS supplier, as demonstrated by its 498 MWh deal with Aypa Power, showing a successful pivot to meet integrated project needs.

- Energy majors are using partnerships to accelerate their strategic transition. Total Energies’ December 2024 agreement with Partners Group is designed to advance its portfolio of renewables and storage, confirming that large, incumbent players see integrated systems as central to their future.

- The ecosystem is also expanding to include distributed assets. The partnership between Nuvve and Great Power, announced in April 2024, focuses on vehicle-to-grid (V 2 G) technology, which turns EV fleets into a vast storage network capable of absorbing intermittent solar power.

Table: Notable Partnerships Driving Solar + Storage

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google / Intersect Power | Dec 2024 | Development partnership for co-located energy parks. This alliance directly links a major energy user with a developer to create a new model for corporate renewable energy procurement. | Utility Dive |

| Canadian Solar / Aypa Power | Jul 2024 | Canadian Solar’s e-STORAGE to supply 498 MWh of batteries for Aypa Power’s project. This solidifies the role of PV manufacturers as critical BESS technology suppliers for utility-scale projects. | Canadian Solar |

| Total Energies / Partners Group | Dec 2024 | Strategic agreement to advance Total Energies’ integrated power strategy. This move allows the energy major to leverage private capital to scale its renewables and storage portfolio. | Total Energies |

| Nuvve / Great Power | Apr 2024 | Partnership to accelerate EV integration and V 2 G adoption. This alliance aims to create a distributed energy storage network from EVs, providing a crucial buffer for variable solar generation. | Nuvve |

Global Solar Hotspots: Where Solar and Storage Converge

While China continues to lead the world in sheer scale of solar deployment, North America and parts of Europe are establishing the most advanced and valuable markets by pioneering the regulatory and commercial models for integrated Solar + Storage. These regions are defining the future of dispatchable renewable energy, shifting the focus from megawatts of capacity to megawatt-hours of reliable delivery.

Global Solar PV Capacity Surges Sharply in 2024

This chart visualizes the massive global scale of solar deployment, directly supporting the section’s point about China’s dominance in sheer capacity and giga-scale projects.

(Source: REN21)

Top Global Solar Module Manufacturers Ranked for 2025

The section mentions PV manufacturers becoming critical technology suppliers, and this chart ranks those key players, underscoring their importance in the new partnership ecosystem.

(Source: AFSIA)

- China’s dominance in PV scale is undisputed, with giga-scale projects like the 15, 600 MW Gonghe Talatan Solar Park. However, market signals around project structure are more prominent elsewhere.

- The United States is the clear leader in large-scale Solar + Storage integration. This is evidenced by projects like the 690 MW Gemini Solar Project in Nevada with its 380 MW battery, the 498 MWh BESS for the Texas-based Aypa Power project, and the landmark Google/Intersect Power deal centered in the US.

- Canada has become a key growth market for dispatchable renewables. BC Hydro’s 2024 call for power, which heavily favored members of the Canadian Renewable Energy Association with dispatchable projects, and the development of North America’s largest urban solar park (325 MW) in Medicine Hat, Alberta, highlight this trajectory.

- Europe is creating the regulatory frameworks essential for attracting private investment into hybrid assets. Italy’s new procurement mechanism for large-capacity storage auctions, announced in September 2024, and Cyprus’s EU-funded policy for hybrid storage systems, create stable, predictable markets for developers.

Solar Technology Maturity: Dispatchable Power Becomes Commercial Standard

By 2025, the core technology of standalone solar PV is fully mature, but its primary system-level weakness, intermittency, has rendered it insufficient for grids requiring high reliability. The co-deployment of BESS has now moved from a pilot-phase concept to the new commercial standard for any utility-scale solar project seeking financing and a grid connection agreement.

Solar Panel Technology Reaches New Power, Efficiency Highs

The section states that PV technology is now mature. This chart provides direct evidence by showcasing the high power, efficiency, and advanced cell types of leading 2025 modules.

(Source: Clean Energy Reviews)

- The 2021-2024 period served to validate large-scale BESS co-location and move it to standard practice. The successful commercial operation of the SN Aboitiz Power hybrid project in the Philippines in May 2024 was a key milestone, proving the technical and commercial case for retrofitting and co-locating BESS with renewable assets.

- In 2025, the market narrative has shifted completely. Discussions around major international projects, such as the UAE’s Mohammed bin Rashid Al Maktoum Solar Park, now center as much on their integrated storage capabilities (both BESS and CSP) as their PV capacity. Projects without a clear storage strategy are viewed as incomplete.

- An important forward-looking signal is the emergence of alternative battery chemistries to mitigate lithium-ion supply chain risk. The planned deployment of 2 MW of iron-sodium batteries by Inlyte Energy at a data center, while small, points to a critical technological evolution needed to secure the vast amount of storage required for a fully renewable grid.

- The economic viability of the integrated model is now proven. Despite high interest rates of 7-9% in 2025, solar projects continue to deliver strong returns of 8-12%. This resilience is enhanced by the firming capacity and additional revenue streams (e.g., ancillary services) that only an integrated BESS can provide.

Solar + Storage SWOT Analysis: Market Dynamics in 2026

The mandatory integration of battery storage has fundamentally reshaped the solar industry’s risk and opportunity profile. It has solved the critical weakness of intermittency, opening up new markets for grid services, but has simultaneously introduced new dependencies on battery mineral supply chains and increased project capital requirements.

Utility-Scale Solar Installation Costs Increased in 2025

This chart directly supports the section’s SWOT analysis by illustrating the “increased project capital requirements” that have emerged as a key weakness for new integrated projects.

(Source: SEIA)

Table: SWOT Analysis for Integrated Solar + Storage Projects

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Lowest Levelized Cost of Energy (LCOE) for new generation. | Ability to provide dispatchable, firm power and ancillary grid services. Strong ROI (8-12%) despite high interest rates. | The value proposition shifted from “cheapest energy” to “cheapest reliable, dispatchable energy, ” resolving the intermittency weakness. |

| Weaknesses | Intermittency, grid curtailment risk, and negative wholesale pricing during peak solar hours. | Higher upfront capital expenditure. New supply chain dependencies on battery minerals (lithium, cobalt, nickel). | The core weakness of intermittency was resolved, but it was replaced by new financial and supply chain vulnerabilities tied to BESS. |

| Opportunities | Corporate PPAs based on annual energy consumption. | 24/7 carbon-free energy contracts for entities like data centers (e.g., Google). Accessing new revenue from capacity markets and grid stabilization. | The market opportunity expanded from simple energy sales to providing high-value grid reliability and 24/7 clean power as a service. |

| Threats | Grid connection queue congestion and saturation in high-penetration areas. | Rising interest rates disproportionately affect more capital-intensive hybrid projects. Increased competition from other dispatchable technologies. BESS supply chain volatility. | The threat shifted from being unable to get power onto the grid to securing the capital and materials needed to build a dispatchable project in the first place. |

2026 Solar Outlook: The Race for Dispatchable Capacity

If corporate demand for 24/7 carbon-free energy continues to accelerate, the most critical signal to watch in 2026 will be the security of the battery supply chain. This will become the primary bottleneck for solar growth, superseding grid connection queues or panel manufacturing as the industry’s main constraint.

Utility Solar Installations Forecast to Decline Post-2025

As the section discusses a future constrained by bottlenecks, this forecast visualizes a potential market impact, showing a decline and stabilization after a 2025 peak.

(Source: SEIA)

- If this happens: Corporate giants beyond Google announce multi-billion dollar, 24/7 clean energy procurement goals. Watch this: The project backlogs of integrated developers like Intersect Power and the order books of BESS suppliers such as Canadian Solar‘s e-STORAGE. A rapid expansion in these areas will confirm the trend is systemic.

- This could be happening: A surge in M&A and venture capital investment targeting companies with commercially viable, non-lithium battery chemistries. Watch for deals involving sodium-ion, iron-air, or flow battery technologies as strategic hedges against mineral price volatility and geopolitical supply risks.

- This could be happening: A growing divergence in global solar market growth. Regions with clear regulatory support for storage, like Italy and parts of the US and Canada, will see accelerated deployment, while regions focused only on solar LCOE will experience investment stagnation and higher curtailment.

- This could be happening: The 16% decline in solar corporate funding seen in 2025 reverses as the financial community becomes fully confident in the de-risked, higher-margin business model of dispatchable Solar + Storage power plants.

Frequently Asked Questions

Why is battery storage now considered mandatory for new large-scale solar projects?

According to the text, battery storage is now mandatory because the market requires solar assets to be dispatchable and grid-stabilizing resources. This shift is driven by grid constraints and a growing demand from large consumers, like Google’s data centers, for reliable, 24/7 carbon-free energy, a goal that intermittent, standalone solar projects cannot achieve.

The article mentions a 16% decrease in solar corporate funding in 2025. Does this mean the solar market is declining?

No, the article clarifies that the 16% decrease in funding does not signal a market decline but rather a ‘strategic pivot’ by investors. Capital is shifting away from speculative, standalone solar projects and towards more capital-intensive, lower-risk integrated Solar + Storage projects that are viewed as critical grid infrastructure with multiple revenue streams.

What is ‘dispatchable power’ and why has it become so important?

Dispatchable power is electricity that can be stored and then deployed to the grid on demand, rather than only when it is being generated. It has become critical because it solves solar power’s main weakness: intermittency. By integrating battery storage, solar projects can provide firm, reliable power and ancillary grid services, meeting the needs of a modern grid and enabling 24/7 carbon-free energy contracts.

Which regions are leading the development of integrated Solar + Storage projects?

While China leads in the sheer scale of solar deployment, the United States is identified as the clear leader in large-scale Solar + Storage integration, citing projects like Gemini Solar and the Google/Intersect Power deal. Canada and parts of Europe (like Italy and Cyprus) are also highlighted as key hotspots, as they are pioneering the regulatory and commercial models necessary to attract investment in dispatchable renewable assets.

What are the new risks or weaknesses associated with this shift to Solar + Storage?

The SWOT analysis in the article indicates that while integrating storage solves the problem of intermittency, it introduces new weaknesses and threats. These include higher upfront capital expenditure, new supply chain dependencies on critical battery minerals like lithium and cobalt, and increased vulnerability to rising interest rates and BESS supply chain volatility. The security of the battery supply chain is identified as the potential primary bottleneck for future growth.