Top 10 Post-Combustion Capture Deals: Google’s 1 st PPA & Microsoft’s 19 GW Push (2024-2025)

The corporate clean energy market is rapidly evolving from broad renewable procurement to highly targeted strategies aimed at achieving 24/7 carbon-free energy (CFE). This strategic shift is driven by the immense power demands of artificial intelligence and hyperscale data centers, forcing corporations to move beyond intermittent renewables. Key data from 2024 and 2025 shows a clear trend toward portfolio-based procurement that includes firm, dispatchable clean power. This is highlighted by Microsoft’s record-breaking procurement of 19 GW in 2024 and Google’s pioneering Power Purchase Agreement (PPA) for a natural gas plant equipped with carbon capture, establishing a new model for corporate decarbonization. The dominant theme for 2025 is the race to secure firm power to match hourly energy consumption, a far more sophisticated goal than simple annual renewable energy credits.

An analysis of corporate sustainability activities reveals the scale and direction of these commitments. The following installations represent the most significant deals from 2024 to 2025, ranked by year and the scale of the initiative.

1. Google’s First-of-its-Kind Carbon Capture PPA (October 2025)

Company: Google

Capacity: Not Disclosed

Application: Securing firm, 24/7 carbon-free energy

Source: The $6 Billion Blueprint: How Google’s CCS Power Deal Created a …

2. Meta’s U.S. Data Center Renewable Energy Procurement (June 2025)

Company: Meta

Capacity: 0.8 GW (800 MW)

Application: Powering U.S. data centers

Source: Meta Secures Nearly 800 MW of Renewable Energy to Power U.S. …

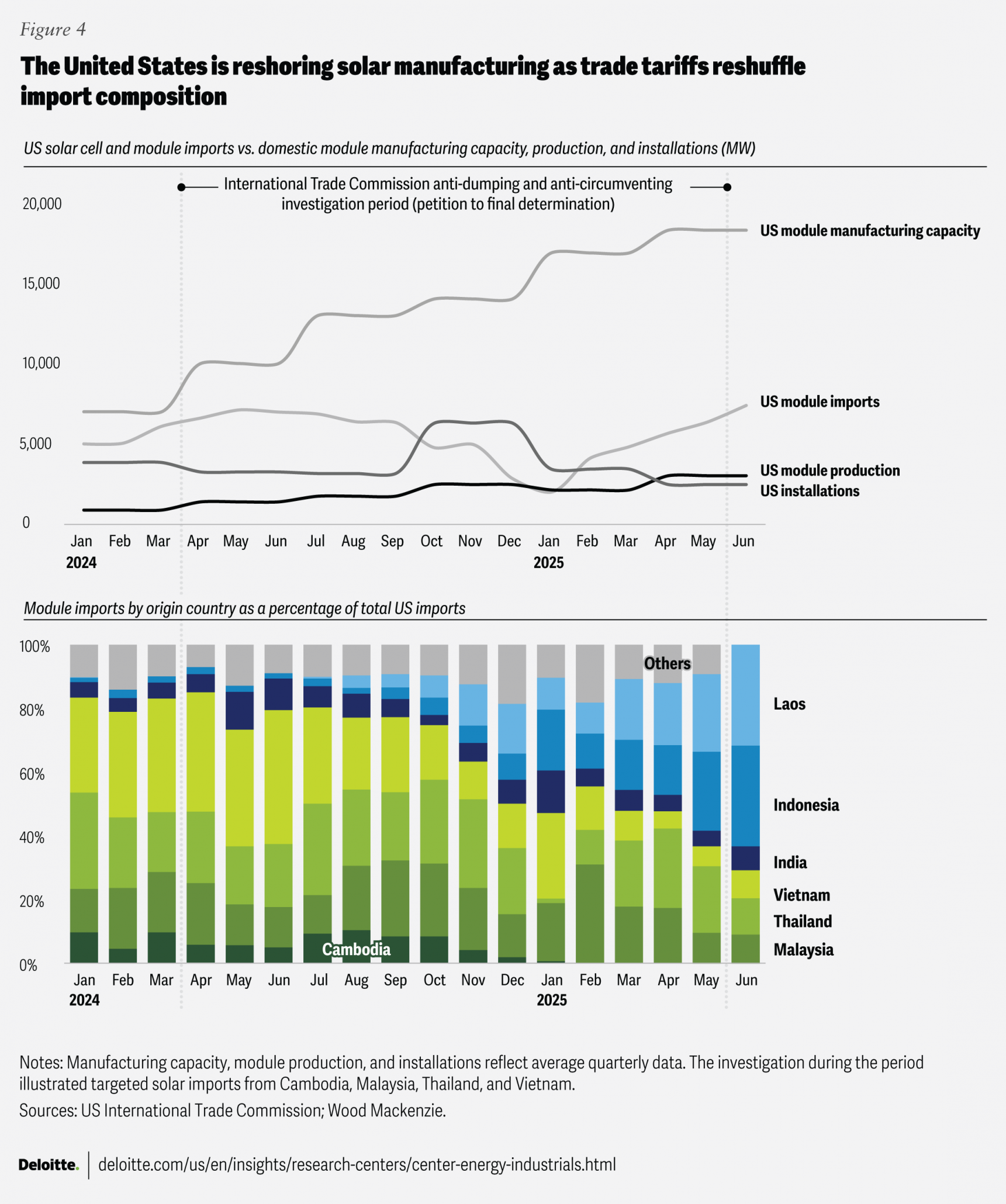

US Solar Manufacturing Ramps Up Amid Import Shifts

The section focuses on Meta’s renewable energy procurement specifically for its U.S. data centers. This chart provides critical context on the domestic U.S. solar supply chain, which is a key factor and enabler for large-scale corporate solar procurement within the country.

(Source: Deloitte)

3. Adani Green Energy’s Installed Capacity Milestone (June 2025)

Company: Adani Green Energy Limited (AGEL)

Capacity: 15 GW

Application: Large-scale grid supply and corporate portfolio growth

Source: Adani Green Energy Sets Record with Over 15, 000 MW of Installed …

4. ENGIE’s Leadership in Corporate PPA Supply (Full Year 2025)

Company: ENGIE

Capacity: 3.6 GW

Application: Supplying corporate renewable energy demand

Source: ENGIE: the world’s number one in renewable corporate Power …

5. Microsoft’s Record-Breaking Annual Procurement (2024)

Company: Microsoft

Capacity: 19 GW

Application: Powering global data center operations

Source: 2025 Microsoft Environmental Sustainability Report

6. Big Tech’s Collective Clean Power Purchase (2024)

Companies: Amazon, Microsoft, Meta, and Google

Capacity: 11.3 GW

Application: Powering data centers and demonstrating market influence

Source: Clean Energy Contracts with Fortune 500 Companies Surge in 2024

Global Corporate Climate Pledges by Sector and Region

The section is about ‘Big Tech’s Collective Clean Power Purchase.’ This high-level chart provides the perfect context by showing how the tech sector’s climate pledges fit into the broader global landscape, allowing the reader to understand the significance of this sectoral action.

(Source: Nature)

7. Re New’s PPA Portfolio Expansion (May 2024)

Company: Re New

Capacity: 2.2 GW

Application: Expansion of contracted renewable capacity for grid supply

Source: Re New Signs 2.2 GW of PPAs Boosting its Clean Energy Portfolio to …

8. Lightsource bp’s Global PPA Execution (2024)

Company: Lightsource bp

Capacity: 1.3 GW

Application: Supplying corporate offtakers across global markets

Source: 10 Power Purchase Agreements signed in 2024 – Lightsource bp

9. Iberdrola’s Consortium Wind PPA in Spain (June 2024)

Company: Iberdrola

Capacity: 0.7 GW (700 MW)

Application: Supplying a consortium of Spanish corporations with wind energy

Source: Power Purchase Agreement Market – Dimension Market Research

10. Google’s Largest Offshore Wind PPA (Early 2024)

Company: Google

Capacity: 0.478 GW (478 MW)

Application: Achieving hourly clean energy matching for operations

Source: How hyperscalers are fueling the race for 24/7 clean power – Mc Kinsey

Table: Top Corporate Sustainability Deals (2024-2025)

| Company | Capacity | Application | Source |

|---|---|---|---|

| Not Disclosed | Securing firm, 24/7 carbon-free energy | The $6 Billion Blueprint: How Google’s CCS Power Deal Created a … | |

| Meta | 0.8 GW | Powering U.S. data centers | Meta Secures Nearly 800 MW of Renewable Energy to Power U.S. … |

| Adani Green Energy | 15 GW | Large-scale grid supply & portfolio growth | Adani Green Energy Sets Record with Over 15, 000 MW of Installed … |

| ENGIE | 3.6 GW | Supplying corporate renewable energy demand | ENGIE: the world’s number one in renewable corporate Power … |

| Microsoft | 19 GW | Powering global data center operations | 2025 Microsoft Environmental Sustainability Report |

| Amazon, Microsoft, Meta, Google | 11.3 GW | Powering data centers and market influence | Clean Energy Contracts with Fortune 500 Companies Surge in 2024 |

| Re New | 2.2 GW | Expansion of contracted renewable capacity | Re New Signs 2.2 GW of PPAs Boosting its Clean Energy Portfolio to … |

| Lightsource bp | 1.3 GW | Supplying corporate offtakers globally | 10 Power Purchase Agreements signed in 2024 – Lightsource bp |

| Iberdrola | 0.7 GW | Supplying a corporate consortium in Spain | Power Purchase Agreement Market – Dimension Market Research |

| 0.478 GW | Achieving hourly clean energy matching | How hyperscalers are fueling the race for 24/7 clean power – Mc Kinsey |

Corporate PPAs: Big Tech’s 19 GW Demand Drives Tech Diversity

The primary application driving these massive deals is the powering of hyperscale data centers. However, the sheer scale of energy demand is forcing a diversification in the technologies being procured. While solar and wind PPAs remain the bedrock, as seen with Meta’s procurement of nearly 800 MW, the need for round-the-clock power is pushing companies toward new frontiers. Google’s PPA for a gas plant with Post-Combustion Capture is a landmark event. It signals that hyperscalers are now willing to underwrite the financial risk of novel, firm power technologies to meet their 24/7 CFE goals. This creates a bankable offtake model that can accelerate the deployment of other firm clean energy sources like advanced geothermal and small modular reactors, moving beyond a sole reliance on intermittent renewables.

AI Data Center Buildout Demands Gigawatts of Power

This chart directly illustrates the primary driver for the topic of the section. The section heading discusses ‘Big Tech’s 19 GW Demand,’ and the chart explains that the AI data center buildout is the cause of this massive need for power, providing essential context for the entire article.

(Source: SiliconANGLE)

US & India Lead: Adani Green Energy’s 15 GW Milestone

Geographically, the United States is the epicenter of this activity, driven by the intense concentration of data centers operated by Microsoft, Amazon, Meta, and Google. The collective procurement of 11.3 GW in 2024 by these four companies alone demonstrates their market-shaping power. However, other regions are seeing massive growth. In India, Adani Green Energy’s surge past 15 GW of installed capacity establishes it as a global renewable energy heavyweight, driven by strong domestic policy and demand. Europe also remains a key market, with significant deals like Iberdrola’s 700 MW wind PPA in Spain and Lightsource bp’s multi-regional execution of 1.3 GW in PPAs. This regional distribution shows a global trend, but leadership is currently concentrated where data center growth is most explosive.

Renewable Project Pipeline Ramps Up Through 2029

The section discusses the leadership of the US and India in renewable capacity, highlighting Adani’s milestone. This chart provides the broader supply-side context, showing the massive global pipeline of renewable projects that enables such milestones and market leadership.

(Source: Deloitte)

1 st-of-its-Kind Deal: Google’s Post-Combustion Capture PPA

These large-scale deals offer crucial insights into technology maturity. Conventional solar and onshore wind are fully commercialized and being procured at an unprecedented scale, exemplified by Microsoft’s staggering 19 GW of contracts in a single year. Offshore wind is rapidly maturing as a viable corporate procurement option, with Google’s 478 MW PPA serving as a key validator. The most significant indicator of tech evolution is Google’s PPA for electricity from a natural gas plant with CCS. This moves carbon capture from a technology largely used in industrial settings to a commercially viable component of a corporate energy strategy. By creating a PPA structure for it, Google is effectively de-risking the technology for other corporate offtakers and signaling a new phase of market adoption for firm, low-carbon power sources.

Major Firms Revise Past Carbon Emissions Upwards

The section discusses a ‘first-of-its-kind’ carbon capture deal. The chart’s finding that firms are revising emissions upwards highlights the difficulties and inaccuracies in carbon accounting, providing a strong rationale for why companies are exploring novel, directly measurable technologies like carbon capture.

(Source: Harvard Business School)

Microsoft’s 24/7 CFE Strategy: What to Expect from Portfolio PPAs

The most critical expectation for the year ahead is the acceleration of portfolio-based procurement. Corporations will increasingly move away from signing single-technology PPAs and instead contract for a blended portfolio of technologies—combining intermittent solar and wind with firm power sources like CCS, geothermal, batteries, and next-generation nuclear—to guarantee true 24/7 carbon-free energy.

- Firm Power Gains Traction: Google’s pioneering PPA for a gas plant with carbon capture in October 2025 is the strongest signal yet. It establishes a repeatable, bankable model that other hyperscalers will likely replicate to secure the firm, dispatchable power needed for hourly energy matching.

- AI Demand as a Catalyst: The massive energy requirements for AI are forcing a strategic rethink. The nearly 800 MW procured by Meta in mid-2025 for its data centers shows that this demand is relentless, making the reliability of firm power a non-negotiable requirement.

- Volumetric Matching Declines: The focus on simply matching annual energy consumption with renewable energy credits is becoming obsolete. The strategic push by leaders like Microsoft and Google toward hourly matching will force the rest of the market to adopt more sophisticated procurement strategies that value reliability and time-of-delivery over sheer volume.

Study Finds Nearly 40% of Climate Targets Fail

This chart explains the problem that advanced strategies like Microsoft’s 24/7 CFE are designed to solve. The failure of traditional, less rigorous targets creates the impetus for companies to adopt more sophisticated and impactful approaches like 24/7 matching, which the section explores.

(Source: Nature)

The questions your competitors are already asking

This report covers one angle of corporate clean energy procurement. The questions that matter most depend on your work.

- How carbon capture power purchase agreements are structured

- Big tech deals for advanced geothermal power

- Industrial companies buying firm clean power

- Impact of data center demand on electricity prices

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.