TEPCO LNG Supply Strategy, $2.2 B Vietnam Project, CF Industries JV, and 6.5 M Tonne US Offtake (2021-2025)

LNG Stranded Asset Risk, TEPCO’s 6.5 M Tonne US LNG Commitment

In 2025, Tokyo Electric Power Company (TEPCO), through its joint venture JERA, is executing a high-stakes strategy to secure long-term Liquefied Natural Gas (LNG) supply, which creates a significant stranded asset risk as Japan simultaneously accelerates its decarbonization mandates. The company’s actions reveal a calculated decision to prioritize near-term energy security by locking in decades of fossil fuel supply, betting that the transition to cleaner alternatives will be gradual enough to ensure the profitability of these assets.

- Before 2025, TEPCO’s strategy was largely focused on managing a volatile spot market and stabilizing supply in the wake of the Fukushima disaster. The period from 2025 onward marks a definitive shift toward securing massive, long-term, and geographically concentrated LNG volumes to insulate Japan from price shocks and geopolitical instability.

- This strategic shift was validated in 2025 when JERA signed new agreements for up to 5.5 million tonnes of U.S. LNG annually, in addition to a specific offtake agreement for 1 million mt/year from the Alaska LNG project. These deals concentrate a significant portion of Japan’s future energy supply in the United States.

- These multi-decade commitments to fossil fuels are in direct conflict with Japan’s own climate targets, outlined in its 7 th Strategic Energy Plan. The planned introduction of a national carbon levy on fossil-fuel importers starting in fiscal year 2028 will progressively increase the operational cost of these LNG assets, testing their long-term economic viability.

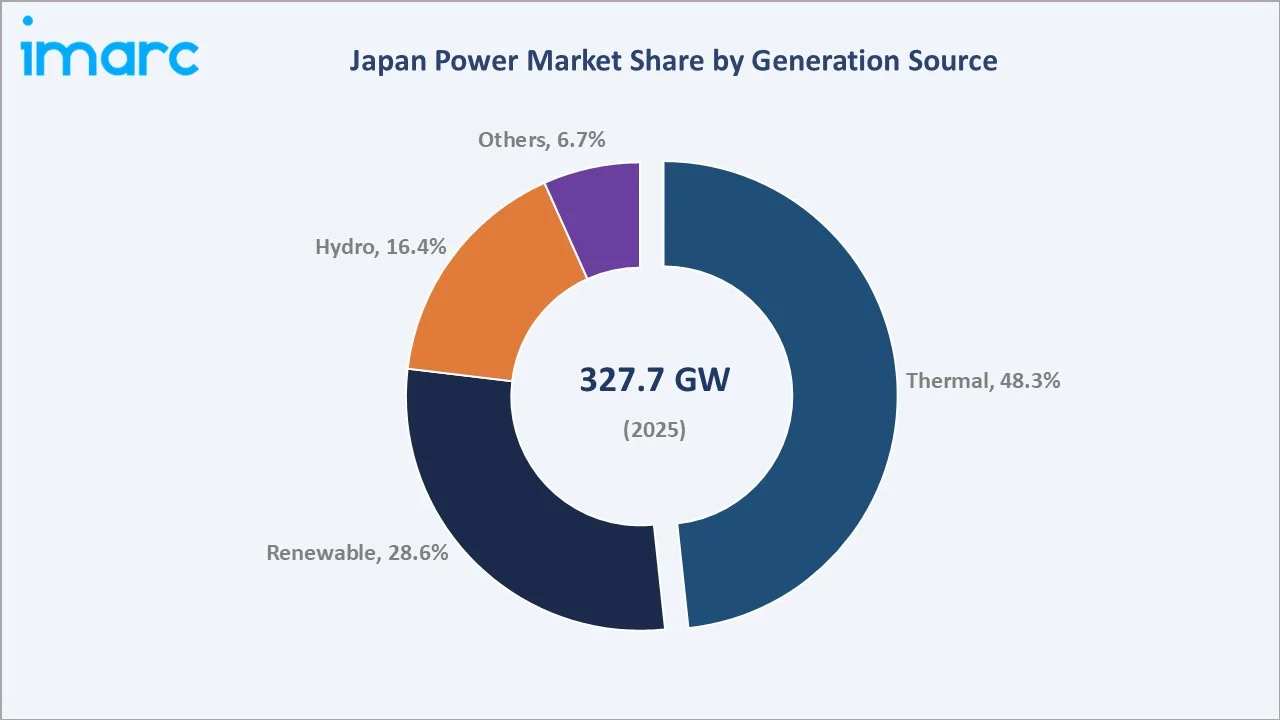

Thermal Power Dominates Japan’s 2025 Energy Mix

The chart shows that thermal power is the foundation of Japan’s energy supply. This context is crucial for understanding Section 0, as it explains the scale of TEPCO’s fossil fuel operations and why its large LNG commitments represent a significant stranded asset risk as the country navigates the energy transition.

(Source: IMARC Group)

$2.2 B Investment, JERA’s Vietnam LNG Power Plant Expansion

JERA‘s capital allocation in 2025 is clearly split between reinforcing its core LNG business and making foundational investments in next-generation clean fuels. The scale of its investments shows a dual focus: expanding its international LNG-to-power footprint while building a supply chain for the low-carbon fuels intended to eventually replace natural gas.

- A major international investment is the planned $2.2 billion for the Nghi Son LNG Power Plant in Vietnam. This project aims to replicate JERA‘s successful LNG-to-power model in a growing Southeast Asian market, establishing a new revenue stream and exporting its infrastructure development expertise.

- Simultaneously, JERA entered a landmark joint venture on April 8, 2025, with CF Industries and Mitsui & Co. to develop a world-scale low-carbon ammonia production facility in the United States. This represents a tangible capital commitment to securing the upstream supply of a key decarbonization fuel.

- These investments are supported by a broader US-Japan energy security agreement, which facilitates up to $550 billion in investments across the energy sector. This government-level framework de-risks private sector investments in US-based LNG export facilities and new energy technologies, including carbon capture and critical minerals.

Kanto Region Dominates Japan’s Power Market

The chart illustrates the concentration of Japan’s power market in the Kanto region, the home market of TEPCO (a JERA co-owner). This mature domestic market provides the strategic impetus for JERA to seek high-growth opportunities overseas, such as the Vietnam LNG power plant.

(Source: IMARC Group)

Table: JERA Strategic Investments in 2025

| Project / Investment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| US-Japan Energy Investment Agreement | Oct 2025 | A broad $550 billion government agreement supporting private investment in US energy, including LNG and low-carbon fuels, facilitating JERA‘s offtake agreements. | S&P Global |

| Nghi Son LNG Power Plant | Sep 2025 | JERA plans a $2.2 billion investment to develop a major LNG-to-power project in Vietnam, marking a significant international expansion. | VIR |

| Blue Point Ammonia Facility | Apr 2025 | A joint venture with CF Industries and Mitsui to construct a world-scale low-carbon ammonia production facility in the US to supply fuel for decarbonization. | CF Industries |

JERA’s 3 Key Alliances for Ammonia and LNG Supply (2025)

The partnerships announced by TEPCO and JERA in 2025 were structured to secure control over the entire energy value chain, from upstream fuel production with American partners to downstream clean energy delivery with corporate customers in Japan. These alliances create a network that supports both the existing LNG business and the future hydrogen and ammonia ecosystem.

- The most strategically significant partnership of 2025 is the joint venture with CF Industries and Mitsui & Co. This alliance establishes a production base for low-carbon ammonia, which is critical for JERA‘s plan to co-fire the fuel in its thermal power plants to reduce CO 2 emissions.

- Domestically, TEPCO Energy Partner’s multi-year, off-site Power Purchase Agreement (PPA) with Subaru, which commenced in February 2025, signals a move into the renewable energy services market, positioning TEPCO as a supplier of green electricity to large corporate clients.

- At the same time, TEPCO and Tokyo Gas renewed their foundational ties with fossil fuel producers through a Heads of Agreement (HOA) with Conoco Phillips. This agreement creates a framework for future long-term LNG supply, reinforcing the company’s dependence on established hydrocarbon partners for its baseload energy needs.

Japan’s Power Industry Value Chain Explained

The chart outlines the power industry’s value chain. This is a perfect fit for Section 3 as it visually situates JERA’s alliances for LNG and ammonia supply within the upstream (fuel procurement) and ‘Generation’ segments of the industry.

(Source: IMARC Group)

Table: TEPCO and JERA Strategic Partnerships in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Subaru Corporation | Nov 2025 | A three-party PPA where TEPCO Energy Partner supplies renewable energy to Subaru, demonstrating a move into downstream green energy services. | Subaru Corporation |

| Pertamina NRE | Jan 2025 | A joint development agreement to study a low-carbon hydrogen and ammonia supply chain from Indonesia, aimed at diversifying clean fuel sources for Japan. | OSTI.gov |

| CF Industries, Mitsui & Co. | Apr 2025 | A joint venture to build a leading low-carbon ammonia production facility, securing a future supply of clean fuel for JERA‘s power plants. | CF Industries |

US vs. Asia, TEPCO and JERA Geographic Investment Focus

In 2025, the geographic focus of TEPCO and JERA‘s energy procurement strategy pivoted decisively toward North America for both conventional LNG supply and new clean fuel production. This marks a strategic consolidation away from a more diversified global portfolio, aiming to leverage the scale and relative stability of the U.S. market.

- The United States became the central pillar of JERA’s supply strategy in 2025, cemented by agreements for up to 6.5 million tonnes of LNG and a major investment in a US-based ammonia plant with CF Industries.

- This heavy concentration in the US is a deliberate move to mitigate the price volatility and geopolitical risks associated with other supply regions. This contrasts with the 2021-2024 period, which relied on a more varied mix of suppliers from the Middle East, Australia, and Southeast Asia.

- While anchoring its supply in the US, JERA is simultaneously exporting its operational model to Southeast Asia. The $2.2 billion Nghi Son project in Vietnam serves as a blueprint for expanding its LNG-to-power business into high-growth emerging markets.

- Separately, TEPCO’s partnership with Indonesia’s Pertamina NRE to explore a hydrogen and ammonia supply chain indicates a continued interest in developing alternative clean fuel sources from the Asia-Pacific region, complementing its US-centric strategy.

APAC Power Generation Market to Reach $340B

Section 5 discusses investment focus in Asia. This chart provides the commercial rationale for that strategy by quantifying the immense size of the Asia-Pacific power generation market, highlighting the scale of the opportunity TEPCO and JERA are targeting.

(Source: Market Research Future)

LNG vs. Ammonia, TEPCO’s Dual-Track Technology Approach

TEPCO‘s technology strategy in 2025 is bifurcated, operating on two distinct timelines: aggressively scaling commercially mature LNG infrastructure for immediate energy security while making foundational investments in less mature low-carbon fuels like ammonia to enable future decarbonization. This dual-track approach reflects the reality of the energy transition, where legacy systems must be maintained while new ones are built.

- LNG liquefaction, transport, and combined-cycle gas power generation are proven, bankable technologies. JERA’s investments in long-term US LNG offtake and the Vietnam power plant are based on the reliability and commercial maturity of this existing technology stack.

- In contrast, large-scale low-carbon ammonia production and its use as a power generation fuel are still in a pre-commercial or early-commercial phase. The 2025 joint venture with CF Industries is a decisive move to advance this technology from the pilot stage toward commercial-scale viability.

- A related Japanese initiative to develop e-methane using existing LNG infrastructure at the Cameron LNG plant in the U.S. represents another forward-looking technology pathway. This approach aims to decarbonize the gas value chain by creating a synthetic, carbon-neutral replacement for natural gas, though the technology remains in early development. This effort complements work by companies like Occidental on large-scale CO 2 utilization.

Renewables & Gas Dominate New Power Generation

The chart shows that natural gas is a dominant choice for new power generation. This directly supports the ‘LNG’ part of TEPCO’s dual-track strategy discussed in Section 6, providing market validation for their continued investment in gas-fired power.

(Source: World Nuclear Industry Status Report)

SWOT Analysis, TEPCO’s LNG Strategy Execution Risks

The strategic actions taken by TEPCO and JERA in 2025 have solidified the company’s strengths in energy procurement but also introduced significant new risks related to the pace of the energy transition. The analysis below contrasts the company’s position before and after the major strategic commitments of 2025.

- Strengths: Enhanced energy security through large-scale, long-term LNG contracts.

- Weaknesses: High financial exposure to fossil fuel price volatility and future carbon pricing.

- Opportunities: First-mover advantage in securing low-carbon ammonia supply chains.

- Threats: The risk of stranded assets if the transition to renewables and clean fuels accelerates faster than anticipated.

Japan Power Market Faces Dueling Pressures in 2025

This chart, depicting dueling pressures like decarbonization vs. energy security, directly illustrates the ‘Threats’ and ‘Opportunities’ in the external environment that are central to the SWOT analysis in Section 7. It provides the high-level context for TEPCO’s strategic risks.

(Source: IMARC Group)

Table: SWOT Analysis for TEPCO’s LNG and Decarbonization Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Managed a diverse but volatile LNG portfolio. Extensive operational expertise in thermal power generation. | Secured up to 6.5 million tonnes of long-term US LNG supply. Established a leading position in the future ammonia market via the CF Industries JV. | The 2025 strategy validated JERA‘s ability to execute large-scale procurement deals, significantly enhancing Japan’s energy supply security. |

| Weaknesses | High dependence on LNG imports with exposure to spot market price spikes. Slow progress on domestic nuclear restarts. | Increased long-term financial commitment to fossil fuels. The economic viability of ammonia co-firing at scale remains unproven. | The company doubled down on its dependence on imported fossil fuels, albeit through long-term contracts, increasing its exposure to future carbon pricing mechanisms. |

| Opportunities | Potential to leverage its purchasing power to shape the Asian LNG market. Opportunity to invest in emerging clean energy technologies. | Leverage the $2.2 B Vietnam project to expand its international LNG-to-power footprint. Use the Pertamina and CF Industries JVs to build a global clean fuel portfolio. | JERA acted decisively in 2025 to seize the opportunity in low-carbon ammonia, moving ahead of competitors to secure a large-scale production source. |

| Threats | Competition from renewables and declining domestic electricity demand. Global pressure to phase out unabated fossil fuels. | Significant stranded asset risk from multi-decade LNG contracts. A faster-than-expected nuclear restart in Japan could reduce LNG demand. The FY 2028 carbon levy. | The 2025 commitments significantly raised the stakes. The company is now financially exposed if Japan’s decarbonization or nuclear restart timeline accelerates. |

TEPCO’s Stranded Asset Test: What to Watch in 2026

The critical uncertainty for TEPCO and JERA moving into 2026 is whether their decarbonization initiatives can scale fast enough to mitigate the mounting financial and regulatory risks of their long-term LNG commitments. The company’s ability to manage this transition will be tested by progress on its new clean fuel ventures and the hardening of climate policy in Japan.

- If the low-carbon ammonia from the CF Industries joint venture proves to be cost-competitive, watch for JERA to announce firm offtake volumes and concrete conversion schedules for co-firing at its domestic thermal power plants. This would be the first major validation of its fuel-switching strategy.

- If the development of US LNG export projects, such as Port Arthur LNG Phase 2, faces significant delays or cost overruns, this could disrupt the economic basis of JERA‘s long-term supply agreements and force a re-evaluation of its procurement strategy.

- The most important signal to watch is the implementation details of Japan’s carbon levy, set to begin in FY 2028. A high price on carbon would directly threaten the profitability of TEPCO‘s newly secured LNG assets and dramatically increase the urgency of its pivot to carbon-free and carbon-neutral fuels.

Japan’s Power Market Forecasted to Reach $276.5B

The chart provides a specific financial forecast for Japan’s power market. This projection serves as a key benchmark for the ‘stranded asset test’ in Section 9, as the realization of this market value is a critical factor in whether TEPCO’s assets remain profitable.

(Source: Market Report Analytics)

The questions your competitors are already asking

This report covers one angle of JERA’s LNG strategy and its exposure to stranded asset risk. The questions that matter most depend on your work.

- What is the status of JERA’s 6.5 M tonne US LNG offtake commitment and the $2.2 B Vietnam LNG-to-power project?

- What is the financial outlook for JERA’s long-term LNG assets with the introduction of Japan’s 2028 carbon levy?

- Which utilities are following TEPCO’s strategy of locking in long-term US LNG, and which are pursuing alternatives?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.