DAC Funding Volatility: $3.5 B DOE Program, Occidental Hubs Face $7.5 B Cut, $24 B Reinstated (2021 to 2026)

Political Risk in DAC, DOE’s $3.5 B Hub Program Exposes Commercial Constraints

The U.S. Direct Air Capture industry’s trajectory shifted from government-catalyzed growth between 2021 and 2024 to a state of high alert due to extreme policy volatility in 2025 and 2026, establishing political risk as the primary constraint on commercial-scale deployment. While the initial federal backing created the market, the subsequent funding turmoil revealed the sector’s acute dependency on stable, long-term public support to de-risk multi-billion-dollar infrastructure projects.

- The 2021-2024 period was defined by foundational policy actions, including the $3.5 billion Regional Direct Air Capture (DAC) Hubs program established by the Bipartisan Infrastructure Law (BIL) and enhanced 45 Q tax credits from the Inflation Reduction Act (IRA), which together spurred the initial hub selections.

- A pivot occurred in October 2025 as a new administration initiated a review that led to the announced termination of over $7.5 billion in funding across 223 energy projects, creating widespread uncertainty and directly impacting at least 10 DAC projects.

- The two flagship hubs, Project Cypress in Louisiana and the South Texas DAC Hub, were placed on a list for review, pausing development momentum and signaling a potential collapse of the U.S. carbon removal strategy.

- Although the DOE restored the funding in April 2026, the episode injected a significant risk premium into future project financing, forcing developers to accelerate efforts to secure a diversified mix of revenue streams, including corporate offtakes and tax credits, to build resilience against policy instability.

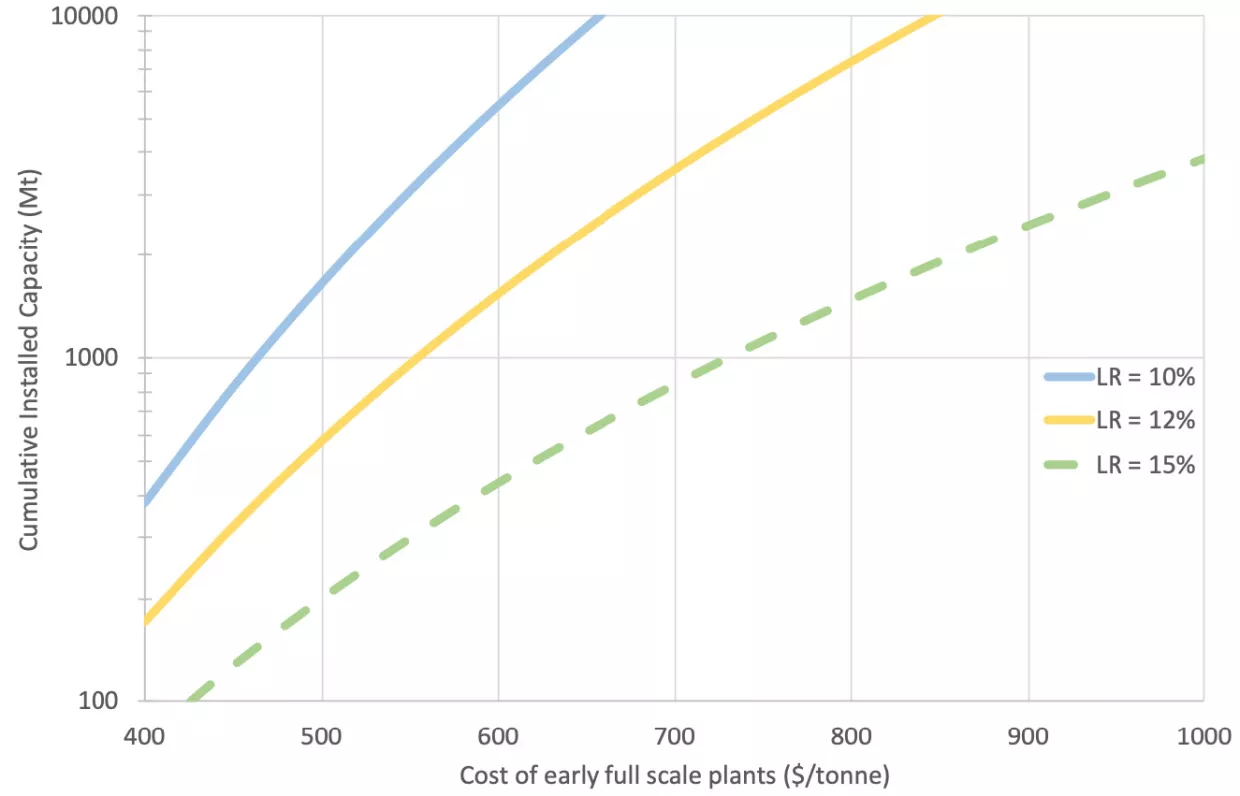

DAC Scale Hinges on Initial Plant Costs

This chart directly illustrates the ‘commercial constraints’ mentioned in the section heading. It shows that high initial plant costs are a primary barrier to scaling Direct Air Capture, which is a central theme of the section’s discussion on political and commercial risks.

(Source: Belfer Center)

$7.5 B in Cuts, DOE DAC Hubs Program Faces Funding Reversal

The funding lifecycle of the DAC Hubs program illustrates a dramatic boom-bust-recover cycle driven by political change, with an initial multi-billion-dollar allocation followed by a near-cancellation and subsequent, precarious reinstatement. This volatility underscores the financial fragility of first-of-a-kind clean energy infrastructure projects that rely on federal backing.

- The program was founded on the $3.5 billion allocation from the BIL. The first major milestone was the August 2023 award of up to $1.2 billion from this pool to stand up the first two commercial-scale hubs in Texas and Louisiana.

- A severe market shock occurred in October 2025 when the new administration announced a review threatening to terminate over $7.5 billion in funding for clean energy projects, which directly ensnared the DAC Hubs program and its cornerstone projects.

- The crisis was resolved in April 2026 when the DOE confirmed it would “retain or modify” nearly 2, 000 clean technology projects, restoring approximately $24 billion in federal awards and providing a critical lifeline to the major DAC hubs.

US CDR Scaling Pathways to 1 Gt/yr by 2050

The section discusses a major funding reversal. This chart shows the long-term carbon removal scaling pathway that such funding is intended to support. The chart provides crucial context by visualizing the ambitious goal that is now jeopardized by the budget cuts.

(Source: Clean Air Task Force)

Table: DOE DAC Hubs Program Funding Status (2025-2026)

| Event | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Funding Reinstated | Apr 17, 2026 | DOE restored funding for nearly 2, 000 projects totaling ~$24 B, including Project Cypress and the South Texas DAC Hub, reaffirming federal support after months of uncertainty. | Reuters |

| Major Hubs Threatened | Oct 8, 2025 | Project Cypress (Louisiana) and the South Texas DAC Hub were placed on a review list, putting their substantial federal funding at risk of cancellation. | Carbon Herald |

| Initial Cancellations Announced | Oct 3, 2025 | A new administration initiated a review and announced the termination of over $7.5 B across 223 energy projects, including at least 10 DAC projects. | E&E News |

| First Hub Selections | Aug 11, 2023 | DOE awarded up to $1.2 billion in initial funding for the development of the first two commercial-scale DAC hubs in Texas and Louisiana. | Canary Media |

US Emissions Dominated by Power and Industry

This chart provides the fundamental rationale for the funding program detailed in the table. It shows the primary sources of U.S. emissions, illustrating the scale of the problem that the DOE DAC Hubs program and its funding are designed to tackle.

(Source: Congressional Budget Office)

DOE DAC Hubs Program, 2 Flagship Hubs, 4 Key Tech Partners (2023 to 2026)

Despite policy turbulence, the underlying structure of the DAC Hubs program is built on strategic partnerships between established energy players, specialized technology providers, and major corporate offtakers, forming a commercial foundation intended to withstand market shocks. This ecosystem of public-private collaboration is essential for scaling a capital-intensive industry.

- The two selected hubs are managed by consortia. Project Cypress is led by the research organization Battelle with technology from Climeworks and Heirloom, while the South Texas DAC Hub is led by 1 Point Five, a subsidiary of Occidental, using technology from Carbon Engineering.

- Private sector demand provides a crucial parallel revenue stream, exemplified by Microsoft’s purchase of 833, 000 tonnes of removal credits and Airbus‘s commitment for 400, 000 tonnes from 1 Point Five, demonstrating long-term commercial interest.

- Other major corporations like Amazon are also providing critical demand signals through offtake agreements, which helps validate the business case for these large-scale projects and attract private financing.

- The acquisition of Carbon Engineering by Occidental for $1.1 billion in 2023 signals a strategic move toward vertical integration, allowing a single entity to control the capture technology, project development, and sequestration, thereby streamlining execution.

DOE’s Retained Awards Portfolio Detailed by Sector

The section focuses on the specific structure of the DAC Hubs program, including its flagship hubs and tech partners. This chart complements the text by providing a visual breakdown of the DOE’s awards portfolio, likely reflecting the types of partners and projects involved.

(Source: CTVC)

Table: Major U.S. Regional DAC Hub Partnerships

| Project / Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Project Cypress | 2023 – 2026 | Led by Battelle with technology providers Climeworks and Heirloom. Aims to capture 1 million metric tons of CO₂ annually in Louisiana. The consortium structure diversifies technological risk. | ESG Today |

| South Texas DAC Hub | 2023 – 2026 | Led by 1 Point Five (Occidental) using Carbon Engineering technology. Also targets 1 million metric tons of CO₂ annually in Texas, leveraging Occidental’s expertise in large-scale energy projects and CO₂ handling. | Department of Energy |

| Microsoft & 1 Point Five | Jul 2024 | Microsoft agreed to purchase 500, 000 metric tons of carbon removal credits from the South Texas DAC Hub, providing a bankable offtake agreement that supports project financing. | Occidental |

| Frontier & 280 Earth | Jul 2024 | The Frontier buyer coalition signed a $40 million offtake agreement with DAC company 280 Earth, illustrating a growing ecosystem of corporate buyers willing to fund emerging technologies. | CDR.fyi |

Map Details US Carbon Capture Projects

This map is the ideal visual accompaniment for a table listing major U.S. regional partnerships. It allows the reader to see the geographic distribution and clustering of the carbon capture projects and hubs mentioned in the table.

(Source: ClearPath)

U.S. Gulf Coast, DOE DAC Hubs Program Cements Regional Dominance

The DOE’s selection of Texas and Louisiana for the first DAC hubs strategically concentrates development in the U.S. Gulf Coast, leveraging the region’s existing industrial infrastructure, deep geologic storage potential, and skilled energy workforce. This geographic focus accelerates deployment but also centralizes both economic opportunity and systemic risk.

- The 2021-2024 period established the strategic framework, with the DOE’s site selection criteria clearly favoring regions with favorable geology for CO₂ sequestration and access to low-cost, low-carbon energy.

- The August 2023 selection of Calcasieu Parish, Louisiana, for Project Cypress and Kleberg County, Texas, for the South Texas DAC Hub officially solidified the Gulf Coast’s role as the epicenter of U.S. DAC deployment.

- This geographic concentration offers operational efficiencies but also creates systemic risk, as demonstrated when the October 2025 funding review threatened the entire region’s nascent DAC economy in one stroke.

- While future funding opportunities, such as the $1.8 billion NOI announced in September 2024, may encourage geographic diversification, the first-mover advantage and integrated infrastructure hub are now firmly anchored in the Gulf Coast.

US Dominates Announced DAC Project Capacity

The section highlights the U.S. Gulf Coast’s regional dominance. This chart places that regional story into a global context, showing how leadership in areas like the Gulf Coast contributes to the overall U.S. dominance in announced DAC capacity.

(Source: Internationale Politik Quarterly)

SWOT Analysis, DOE’s DAC Hub Program Risks and Strengths

The DAC Hubs program’s foundational strength lies in its robust initial federal backing and strong alignment with corporate climate goals. However, its profound weakness is a structural dependency on continued political goodwill, which the events of 2025-2026 proved to be a significant threat to long-term operational and financial stability.

DAC Technology Costs Projected to Decline With Scale

A SWOT analysis requires evaluating opportunities and strengths. This chart perfectly illustrates a central opportunity for the DAC program: the potential for significant cost reduction as the technology is deployed at scale, turning a current weakness (high cost) into a future strength.

(Source: Clean Air Task Force)

Table: SWOT Analysis for the DOE DAC Hubs Program

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong bipartisan support for the BIL; lucrative 45 Q tax credits ($180/ton); growing corporate offtake market (e.g., Microsoft, Frontier). | Core incentives (45 Q) and corporate demand remain; the program’s survival of a political challenge demonstrated some underlying resilience and industry lobbying power. | The core value proposition of federal-plus-private funding was validated, but its stability was proven to be fragile. The market demonstrated it could successfully advocate for itself. |

| Weaknesses | High technology costs ($400-$1, 000/ton); immense clean energy requirements; reliance on nascent CO₂ transport and storage infrastructure. | Acute dependency on federal funding became a realized liability; public and political opposition to CO₂ pipelines and storage wells intensified. | The theoretical weakness of government dependency was validated as a real-world, acute business risk. Execution risks around infrastructure moved to the forefront. |

| Opportunities | Achieve cost reductions toward the $100/ton goal through learning-by-doing; establish U.S. as a global leader in carbon removal technology. | Force industry to build more resilient business models less dependent on a single grant; accelerate focus on securing long-term private offtake agreements. | The near-crisis created an opportunity for the industry to mature, forcing a greater emphasis on financial resilience beyond just securing initial government grants. |

| Threats | Potential for shifts in political support; permitting delays for large infrastructure projects; public opposition. | The primary threat of political volatility was fully realized, with a new administration temporarily halting over $7.5 billion in funding. | The political threat shifted from a hypothetical risk to a tangible event, fundamentally repricing risk for all future federally supported energy projects. |

DAC vs. BECCS: Comparing Key Technology Trade-offs

A SWOT analysis table would assess the strengths and weaknesses of the program’s core technology. This chart provides a direct comparison between DAC and an alternative (BECCS), highlighting the specific trade-offs that would inform such an analysis.

(Source: Green Fuel Journal)

DOE DAC Hubs Program: Will Policy Stability Hold for Occidental’s Hub?

For the year ahead, the single most critical factor for the U.S. DAC industry is demonstrating durable policy stability, as project developers must now secure final financing and offtake agreements in a market that has priced in significant political risk. The focus shifts from winning awards to executing projects under a new cloud of uncertainty.

- If the restored funding flows without further interruption or administrative delay, watch for Final Investment Decisions (FIDs) for Project Cypress and the South Texas DAC Hub. An FID would signal that private capital confidence is returning despite the recent turmoil.

- If there are further administrative audits or slow-downs, as hinted at in early 2026 reports, expect project timelines to slip and private investors to demand more favorable terms or remain on the sidelines, stalling momentum.

- A key signal to monitor is the structure of new corporate offtake agreements. Watch for contract clauses that explicitly account for political risk or a preference for shorter-term commitments, which would indicate the market is adapting to ongoing uncertainty around the direct air capture tax credit and other incentives.

- The market’s response to the DOE’s second funding opportunity notice for $1.8 billion will be a crucial barometer. A high volume of strong applications would suggest the industry’s appetite for growth remains, while a tepid response would indicate the risk introduced in 2025 has had a chilling effect on new investment.

The questions your competitors are already asking

This report covers one angle of how funding volatility and political risk are constraining the commercial deployment of U.S. Direct Air Capture infrastructure. The questions that matter most depend on your work.

- What is actually happening with Project Cypress and the South Texas DAC Hub since the DOE funding was reinstated in April 2026?

- What is the outlook for commercial-scale DAC deployment in the U.S. by 2030, given the heightened political risk?

- Which DAC developers are best positioned to navigate policy instability with diversified revenue from corporate offtakes and tax equity?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.