Woodside Energy LNG De-Risking, $5.7 B Stonepeak Deal, $378 M Williams Sale, and 2 Major Partnerships (2025)

Woodside Energy $17.5 B Louisiana LNG Project, US Market Pivot (2025)

In 2025, Woodside Energy transitioned its Louisiana LNG project from a high-risk concept to a financially secured reality by orchestrating a series of pre-FID equity sell-downs, a model that contrasts sharply with the traditional approach of seeking partners after sanctioning a mega-project.

- Prior to 2025, the Louisiana LNG development represented a proposal with immense capital exposure for Woodside. The company’s growth portfolio was concentrated in its Australian assets, making a large-scale U.S. investment a significant strategic and financial hurdle.

- The pivotal change in 2025 was the execution of a financial strategy to de-risk the project before final approval. Woodside secured a $5.7 billion commitment from infrastructure firm Stonepeak and a $378 million deal with U.S. pipeline operator Williams, all ahead of its final investment decision.

- This strategy effectively pre-sold approximately 50% of the project’s equity, validating its economic projections to the market and providing strong momentum for the April 28, 2025, final investment decision. This reduced Woodside’s direct construction capital expenditure from $17.5 billion to a more manageable $11.8 billion.

- The model also brought in specialist partners to mitigate execution risk. Stonepeak provides deep infrastructure investment expertise, while the partnership with Williams secures a top-tier operator for the critical midstream infrastructure required to transport feed gas.

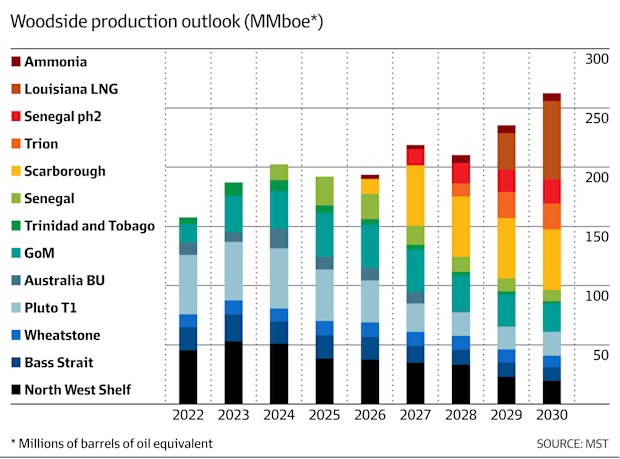

Louisiana LNG Key to Woodside’s Post-2028 Growth

This chart directly states the strategic importance of the Louisiana project to Woodside’s future, perfectly aligning with the section’s focus on the $17.5B Louisiana LNG investment.

(Source: AFR)

$11.8 B in Net CAPEX, Woodside Energy’s Financial De-Risking Strategy

The $17.5 billion total investment in Louisiana LNG was strategically structured to place a majority of the early-years capital burden on partners, enhancing Woodside’s capital efficiency and preserving its balance sheet during the peak construction phase.

- The $5.7 billion investment from Stonepeak, secured through a binding agreement on April 7, 2025, is a crucial component of the funding mix. It significantly covers a large portion of the capital expenditure during the most intensive construction years, reducing Woodside’s peak financial exposure.

- The transaction with Williams, announced on October 22, 2025, monetized a 10% stake in the LNG holding company and an 80% stake in the associated Driftwood Pipeline. This deal provided $378 million in upfront proceeds and offloaded a majority of the pipeline construction and operational responsibility.

- Woodside’s remaining net share of construction costs, approximately $11.8 billion, is now spread over the project’s timeline to its targeted 2029 start-up. This creates a more predictable and manageable capital profile for the company and its investors.

Woodside’s Net Debt Rises to $8.7B in 2025

The chart’s focus on Woodside’s net debt provides a concrete financial metric that illustrates the context for the company’s CAPEX and financial de-risking strategy mentioned in the section.

(Source: Seeking Alpha)

Table: Woodside Energy’s Louisiana LNG Investment Structure (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Williams Equity Sale | Oct 2025 | Sale of a 10% interest in Louisiana LNG LLC and an 80% interest in the Driftwood Pipeline for $378 million. This secured a strategic midstream partner and monetized infrastructure assets. | Wall Street Journal |

| Louisiana LNG FID | Apr 2025 | Final investment decision for the $17.5 billion project. Woodside’s net construction cost was reduced to $11.8 billion following partnership agreements. The project is designed for a >13% IRR. | Reuters |

| Stonepeak Equity Agreement | Apr 2025 | Binding agreement for Stonepeak to acquire a 40% interest in the infrastructure holding company by providing $5.7 billion towards capital expenditure. This was the primary financial de-risking transaction. | Offshore Energy |

Louisiana Showcases Multi-Billion Dollar Capital Investments

This chart provides the broader investment climate in Louisiana, offering essential context for the table that details Woodside’s specific investment structure within the state.

(Source: Site Selection Magazine)

Partnership Strategy, Woodside Energy Sells 50% of Louisiana LNG

Woodside’s partnership strategy in 2025 was twofold: secure capital through equity sales to financial and strategic partners and validate the project’s commercial viability through binding offtake agreements with creditworthy customers.

- The equity partnership with infrastructure investor Stonepeak provided the primary financial de-risking for the Louisiana LNG project. This transaction, completed on June 24, 2025, demonstrated strong third-party confidence in the project’s long-term value.

- The strategic partnership with Williams secured deep expertise in U.S. natural gas pipeline development and operations. This is critical for ensuring reliable and cost-effective feed gas supply, a key factor for the plant’s operational efficiency.

- Commercial validation was achieved on April 17, 2025, with the signing of a binding Sale and Purchase Agreement (SPA) with German utility Uniper. The agreement for 1.0 Mtpa provided a foundational offtake commitment that was essential for supporting the final investment decision.

- Ongoing discussions with other major players, including reports of a potential deal with Saudi Aramco in November 2025, signal Woodside’s continued strategy to bring in global energy leaders as equity partners and offtakers to further diversify risk and secure revenue.

Table: Woodside Energy’s Key LNG Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Williams | Oct 2025 | Strategic partnership and equity sale. Williams acquired a 10% stake in the LNG facility and an 80% stake in the pipeline, becoming a key midstream operator for the project. | Wall Street Journal |

| Stonepeak | Jun 2025 | Equity sell-down completion. The finalization of the deal brought in $5.7 billion in partner capital, significantly de-risking Woodside’s financial commitment. | Stonepeak |

| Uniper | Apr 2025 | Offtake agreement. Signed binding SPAs to supply 1.0 Mtpa from Louisiana LNG and up to 1.0 Mtpa from its global portfolio, anchoring the project’s commercial case. | Woodside |

| Baker Hughes | Mar 2025 | Technology Development Agreement (TDA). Formed a partnership to develop a small-scale, low-carbon LNG technology for future projects, focusing on improved efficiency and reduced emissions. | Turbomachinery Magazine |

Global LNG Market to Near $200B by 2030

This chart quantifies the massive global market opportunity, providing a compelling rationale for why Woodside is forming the key partnerships listed in the accompanying table.

(Source: TechSci Research)

US Gulf Coast Focus, Woodside Energy’s Strategic Geographic Shift

In 2025, Woodside Energy decisively shifted its long-term growth focus from its historical base in Australia to the U.S. Gulf Coast, positioning itself to capitalize on low-cost U.S. natural gas and direct market access to both the Atlantic and Pacific basins.

- Historically, Woodside’s LNG growth was centered in Western Australia with its legacy North West Shelf project and the more recent Pluto and Scarborough developments. The Scarborough project, targeting a 2026 start, represents the final major investment wave in this region for the foreseeable future.

- The selection of Calcasieu Parish, Louisiana, for the $17.5 billion Louisiana LNG project leverages the mature and highly liquid U.S. natural gas market, a robust pipeline network, and a skilled local workforce experienced in large-scale energy projects.

- This U.S. Gulf Coast location provides a significant logistical advantage. It offers competitive shipping routes to European markets seeking to diversify energy sources, as well as to high-demand markets in Asia through the Panama Canal, enhancing Woodside’s global supply flexibility.

- By establishing a major operational hub in the U.S., Woodside diversifies its geopolitical risk profile away from a concentration in the Asia-Pacific region and gains exposure to a different regulatory and market environment.

US LNG Infrastructure Market Hits $46.3B in 2025

The chart’s data on the substantial US LNG infrastructure market directly supports and justifies the section’s theme of Woodside’s strategic geographic shift towards the US Gulf Coast.

(Source: Persistence Market Research)

Woodside Energy Small-Scale LNG Tech, Baker Hughes Agreement (2025)

While the Louisiana LNG project relies on proven, large-scale liquefaction technology to ensure reliability and secure financing, Woodside is simultaneously investing in next-generation, lower-carbon LNG solutions to address future emissions requirements and improve cost-competitiveness.

- The initial phase of the Louisiana LNG project, comprising three trains with a total capacity of 16.5 Mtpa, will utilize established and bankable liquefaction technology from a major provider. This approach was critical for securing the project’s financing and ensuring it meets its 2029 first-production target.

- However, looking toward future needs, Woodside signed a technology development agreement in March 2025 with Baker Hughes. This partnership is focused on creating a more efficient, small-scale, and lower-carbon LNG technology that could be deployed for future expansion trains or new greenfield projects.

- This dual-track technology strategy mitigates the risk of deploying unproven solutions at a mega-project scale while actively creating a pathway to decarbonize future LNG production. This is a necessary step as the entire energy industry pursues emissions reductions, with parallel efforts seen in other sectors, such as Hyundai‘s work on advanced carbon capture technologies.

LNG Industry Revenue Mix Shifting Towards New Tech

This chart illustrates the industry-wide trend of new technology driving revenue, explaining the strategic ‘why’ behind Woodside’s specific agreement with Baker Hughes for small-scale LNG tech.

(Source: MarketsandMarkets)

SWOT Analysis, Woodside Energy LNG Project Execution Model

Woodside’s 2025 strategy fortified its long-term growth prospects by leveraging its project development strengths and executing a masterful de-risking plan, but it also introduced new execution risks in a highly competitive market.

Global LNG Market Forecasts Steady Growth

This chart visualizes a key ‘Opportunity’ for a SWOT analysis by showing the positive global market trend, which is a fundamental component of analyzing Woodside’s project execution model.

(Source: Fortune Business Insights)

Table: SWOT Analysis for Woodside Energy’s 2025 LNG Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong balance sheet post-BHP merger; extensive experience in Australian LNG project development. | Demonstrated capability in complex financial structuring; established a strong U.S. partner network with Stonepeak and Williams. | Woodside validated its ability to de-risk and finance mega-projects in a new geography, moving beyond its traditional Australian comfort zone. |

| Weaknesses | Limited operational presence in the U.S. LNG market; growth portfolio heavily weighted to Australia. | Increased net debt to fund growth projects; reliance on a single project (Louisiana LNG) for transformational growth post-2029. | The company addressed its U.S. presence gap but took on significant project execution responsibility and increased its financial leverage to do so. |

| Opportunities | Forecasted long-term growth in global LNG demand; access to low-cost U.S. natural gas. | Secured position to supply LNG to Europe and Asia; potential to expand Louisiana LNG to 27.6 Mtpa total capacity. | The 2025 FID and partnerships crystallized the opportunity to capture value from the U.S. gas market, moving it from a theoretical option to a concrete, funded project. |

| Threats | Uncertainty over project financing; potential for cost inflation; regulatory hurdles in the U.S. | A forecasted global LNG supply glut starting around 2027; construction cost overruns; volatility in hub-linked gas prices. | While financing risk was mitigated, market risk (a potential supply glut) and construction execution risk are now the primary threats to the project’s projected 13% IRR. |

Global LNG Production Capacity Forecasted to Grow

Complementing the SWOT analysis table, this chart illustrates a critical external factor—rising global production capacity—which could be interpreted as a ‘Threat’ (competition) or an ‘Opportunity’.

(Source: Mordor Intelligence)

13% IRR Target, Woodside Energy’s Feed Gas & Offtake Execution

The critical variable for Woodside’s success following the Louisiana LNG FID is its ability to secure advantageous long-term feed gas supply contracts while layering in additional offtake agreements to fully subscribe the plant’s capacity before its 2029 startup.

- If Woodside successfully secures long-term feed gas pricing at a significant discount to international LNG offtake price benchmarks, the project’s projected 13% internal rate of return will be validated. Watch for announcements of major gas supply and transport agreements through 2026 and 2027.

- If additional high-quality offtake partners, such as the rumored deal with Saudi Aramco, sign on for equity and volumes, it will further de-risk the project’s revenue stream and enhance market confidence. Watch for further equity sell-down or SPA announcements through 2026.

- These could be happening: Woodside is likely leveraging its strategic partnership with Williams to access favorable gas transport and supply arrangements from various U.S. basins, using Williams’ extensive network to optimize its feed gas procurement strategy well ahead of the plant’s commissioning.

Asian Long-Term LNG Demand to Surge

This chart directly addresses the ‘offtake execution’ part of the section heading, as surging Asian demand is critical for securing the long-term sales agreements needed to meet the project’s 13% IRR target.

(Source: S&P Global)

The questions your competitors are already asking

This report covers one angle of Woodside Energy’s U.S. LNG market strategy. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the U.S. LNG export project market?

- Woodside Energy investments and funding. Is the Louisiana LNG project on track for its first cargo target?

- Which LNG developers are adopting Woodside’s pre-FID equity sell-down model?

- What are the opportunities for infrastructure funds like Stonepeak in the LNG project finance market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.