Top 10 SOFC & Grid Stocks, PG&E’s 10 GW Pipeline and Bloom’s 2 GW Capacity Amid $800 B Buildout (2024-2025)

The insatiable power demand from the AI data center buildout is forcing a strategic pivot in infrastructure investment, with a new focus on on-site power generation like Solid Oxide Fuel Cells (SOFC) and grid-scale providers to overcome critical electricity constraints. With global data center capital expenditure projected to reach $800 billion, the market’s primary bottleneck is no longer real estate but power procurement. This is evidenced by utility demand pipelines swelling to 10 GW in a single service area, as seen with PG&E, and the corresponding rise of on-site specialists like Bloom Energy, which is ramping up to 2 GW of annual production capacity to meet this need. The dominant theme for 2025 is that power availability dictates development, compelling tech giants to fund their own energy infrastructure and creating a gold rush for the companies that build, power, and connect these digital factories.

1. Next Era Energy (NEE)

Company: Next Era Energy

Role/Capacity: A leading utility scaling its renewable energy capacity to provide 24/7 green power.

Applications: Powering large-scale data centers with a focus on green energy partnerships with tech giants.

Source: Powering the AI boom: Investing in energy, infrastructure, and the …

2. The Williams Companies, Inc. (WMB)

Company: The Williams Companies, Inc.

Role/Capacity: A major pipeline operator leveraging its extensive natural gas infrastructure.

Applications: Providing reliable, direct baseload power to data centers, complementing intermittent renewables.

Source: 5 Natural Gas Stocks to Buy as AI Data Centers Devour Power in 2026

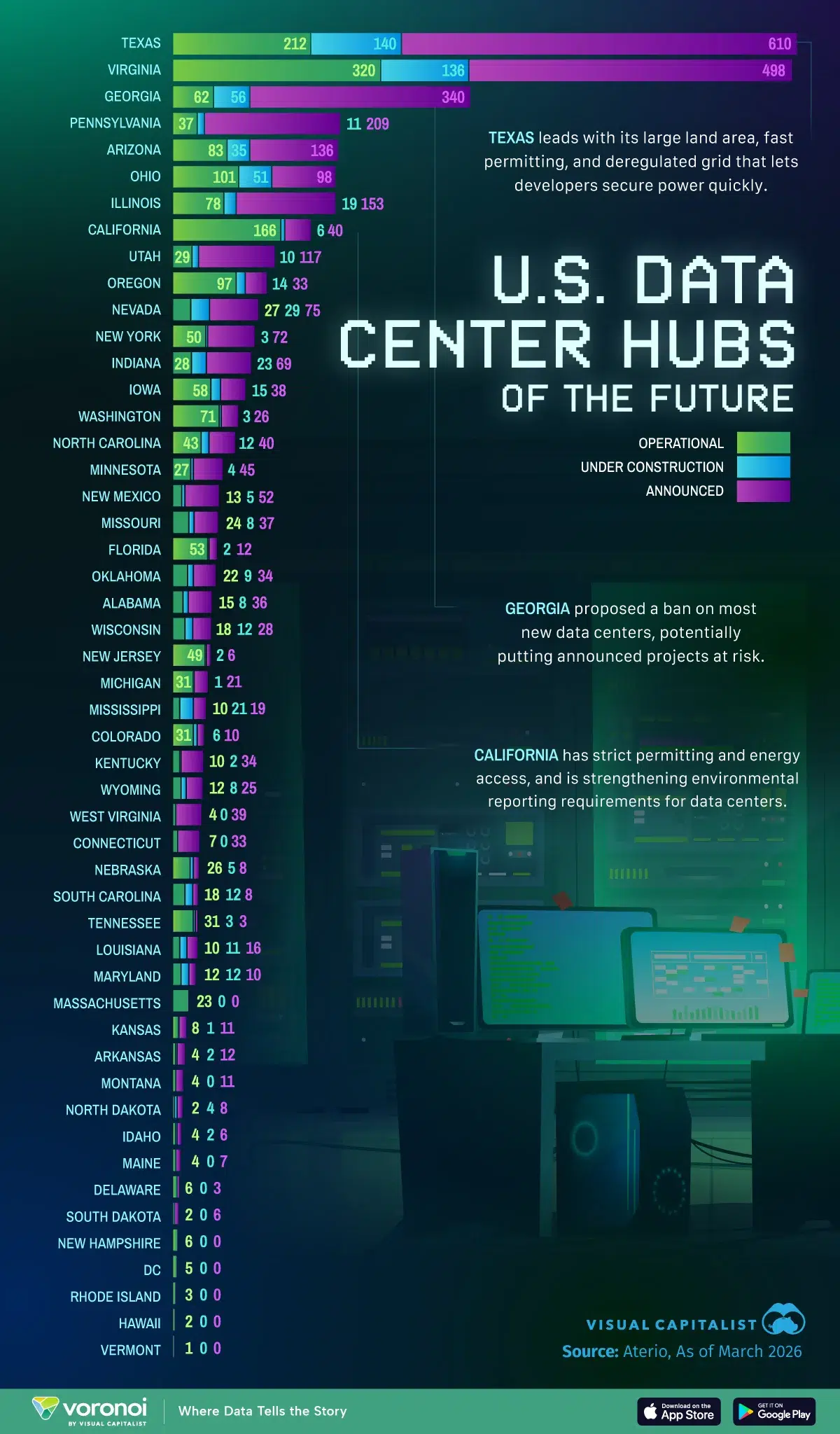

US States Ranked by Data Center Construction

This chart, ranking states by data center construction, identifies key growth markets. For a natural gas infrastructure company like Williams, this data is crucial for planning pipeline expansions to fuel the power plants supporting these new data centers.

(Source: Visual Capitalist)

3. Equinix (EQIX)

Company: Equinix

Role/Capacity: A global data center REIT with an $80.75 billion market cap.

Applications: Providing critical colocation and ultra-low-latency interconnection services for AI deployments.

Source: Top 5 AI Data Center Stocks Delivering Exceptional Returns in 2025 …

US Dominates Global Data Center Count

The chart highlights the strategic importance of the U.S. market in the global data center landscape. This provides context for the section on Equinix, a leading global data center provider with a significant presence in the dominant U.S. market.

(Source: Brightlio)

4. Digital Realty (DLR)

Company: Digital Realty

Role/Capacity: A major data center REIT developing physical real estate for AI infrastructure.

Applications: Owning, operating, and developing data center campuses to meet surging demand.

Source: From Power Grids to Data Centers: The Overlooked Winners in the …

US Data Center Construction Boom Mapped

As a leading data center developer, Digital Realty is a primary driver of the construction boom shown on the map. The chart visually represents the geographic scope of DLR’s development activities and target markets across the United States.

(Source: Visual Capitalist)

5. Vertiv Holdings Co (VRT)

Company: Vertiv Holdings Co

Role/Capacity: A premier supplier of advanced cooling and power management solutions.

Applications: Handling the high thermal loads of AI servers, with facilities now needing 60+ k W per rack.

Source: Top 5 AI Data Center Stocks Delivering Exceptional Returns in 2025 …

Key Players in the AI Data Center Ecosystem

This chart positions Vertiv within the broader AI data center ecosystem, serving as an excellent introduction to the company profile section by visually identifying Vertiv as a critical enabler of power and cooling infrastructure.

(Source: EBC Financial Group)

6. Eaton (ETN)

Company: Eaton

Role/Capacity: An industrial company specializing in electrical equipment and grid infrastructure.

Applications: Upgrading electrical grids and power transmission infrastructure connecting to and within data centers.

Source: 6 Stocks Set to Benefit From AI Data Center Boom: Bank of America

IT and Facility Costs Dominate Data Center Spending

Eaton is a key provider of power management equipment, which is a major component of the ‘Facility Costs’ category shown in the chart. The chart illustrates the significant portion of data center spending that Eaton’s products and services address.

(Source: IoT Analytics)

7. Arista Networks (ANET)

Company: Arista Networks

Role/Capacity: A market leader in high-speed data center switches and Ethernet networking.

Applications: Providing the essential connectivity fabric for large-scale AI clusters.

Source: 7 Best AI Infrastructure Stocks to Buy in 2025 – Stocks To Trade

Nvidia Dominates AI GPU Market with 92% Share

The chart’s focus on Nvidia’s dominance sets the stage for the AI ecosystem where Arista Networks operates. Arista’s high-speed networking is essential for connecting large clusters of Nvidia GPUs, making this chart critical context for understanding Arista’s role.

(Source: IoT Analytics)

8. Amphenol (APH)

Company: Amphenol

Role/Capacity: A key supplier of high-performance interconnects, connectors, and cable assemblies.

Applications: Physically linking servers, racks, and power systems inside a data center.

Source: Unlock AI’s Hidden Gems: 3 Must-Buy Stocks Fueling the Data …

9. Quanta Services (PWR)

Company: Quanta Services

Role/Capacity: A leading construction and engineering firm for energy infrastructure.

Applications: Building high-voltage transmission lines and substations to deliver power to data center campuses.

Source: AI Data Centers Continue To Fuel Builders. These Stocks Are In Buy …

AI Data Center Project Costs Skyrocket

Quanta Services specializes in the construction of large-scale infrastructure, including data centers. The chart’s depiction of skyrocketing project costs is directly relevant to Quanta’s business, impacting project bids, revenue scale, and operational complexity.

(Source: Epoch AI | Substack)

10. Bloom Energy (BE)

Company: Bloom Energy

Role/Capacity: A fuel cell company with a path to 2 GW of annual production capacity.

Applications: Providing reliable, on-site SOFC power to mitigate grid-related delays and constraints for AI data centers.

Source: Bloom Energy says it’s on track for 2 GW annual production capacity

Flexible AI Data Centers Can Add Grid Capacity

The chart’s headline describes a key benefit of Bloom Energy’s on-site fuel cells. These systems provide reliable power and can support the grid, directly enabling the ‘flexible’ data center concept that can ‘add grid capacity’.

(Source: Deloitte)

Table: AI Data Center Infrastructure Leaders (2024-2025)

| Company | Role/Capacity | Applications | Source |

|---|---|---|---|

| Next Era Energy | Leading utility scaling renewable capacity | 24/7 green power for data centers | Powering the AI boom: Investing in energy, infrastructure, and the … |

| The Williams Companies, Inc. | Major natural gas pipeline operator | Reliable baseload power for data centers | 5 Natural Gas Stocks to Buy as AI Data Centers Devour Power in 2026 |

| Equinix | Global data center REIT ($80.75 B market cap) | Colocation and low-latency interconnection | Top 5 AI Data Center Stocks Delivering Exceptional Returns in 2025 … |

| Digital Realty | Major data center REIT | Developing physical real estate for AI | From Power Grids to Data Centers: The Overlooked Winners in the … |

| Vertiv Holdings Co | Advanced cooling and power management supplier | Handling high thermal loads (60+ k W/rack) | Top 5 AI Data Center Stocks Delivering Exceptional Returns in 2025 … |

| Eaton | Electrical equipment and grid infrastructure | Upgrading grids and power transmission | 6 Stocks Set to Benefit From AI Data Center Boom: Bank of America |

| Arista Networks | High-speed data center switch leader | Connectivity fabric for AI clusters | 7 Best AI Infrastructure Stocks to Buy in 2025 – Stocks To Trade |

| Amphenol | High-performance interconnect supplier | Connectors and cables for servers/power | Unlock AI’s Hidden Gems: 3 Must-Buy Stocks Fueling the Data … |

| Quanta Services | Energy infrastructure construction firm | Building transmission lines and substations | AI Data Centers Continue To Fuel Builders. These Stocks Are In Buy … |

| Bloom Energy | On-site SOFC power provider (2 GW capacity path) | Grid-independent power for AI data centers | Bloom Energy says it’s on track for 2 GW annual production capacity |

Market Map of the AI Data Center Stack

This market map provides a perfect visual framework for a ‘Table of Leaders’ by illustrating the different layers of the AI data center stack. It helps the reader understand where each leading company fits within the technology ecosystem.

(Source: Bessemer Venture Partners)

Data Center Power, A Diverse Mix from SOFC to Grid-Scale Renewables

The immense and immediate need for data center power has catalyzed an “all-of-the-above” strategy for energy sourcing, leading to broad industry adoption of diverse technologies. The market is not placing a single bet but is instead building a portfolio of solutions. We see this in the simultaneous rise of large-scale renewable projects from utilities like Next Era Energy, the reliance on natural gas for baseload power from pipeline operators like The Williams Companies, and the critical grid-building activities of firms like Quanta Services. Crucially, the inclusion of Bloom Energy highlights the growing acceptance of on-site SOFC technology as a primary power source, capable of bypassing grid constraints entirely. This diversity implies that the challenge is too large for one solution; data center developers are de-risking their power procurement by engaging grid-scale utilities, transmission builders, and on-site generation specialists in parallel.

Data Center Power Demand to Double by 2030

The chart’s projection that power demand will double underscores the necessity for the ‘diverse mix’ of power solutions, from on-site Solid Oxide Fuel Cells (SOFC) to grid-scale renewables, discussed in the section.

(Source: Bessemer Venture Partners)

USA Focus, PG&E’s 10 GW Pipeline Highlights Regional Power Strain

The geographic epicenter of the AI data center buildout is overwhelmingly concentrated in the United States, as reflected by the featured companies and market data. The core players—from utilities like Next Era to REITs like Equinix and component suppliers like Amphenol—are largely US-based entities servicing a domestic boom. The most striking evidence of this regional focus is the report from PG&E that its data center demand pipeline has swelled to 10 GW in its California service area alone. This single data point illustrates the immense strain being placed on specific regional grids. It explains why tech companies are desperate for solutions and why the US market is the primary theater for this infrastructure expansion, driving opportunities for local construction firms, utilities, and technology providers.

Northern Virginia Dominates Global Data Center Market

The chart identifies Northern Virginia as the world’s largest data center market. This extreme concentration is the primary cause of the ‘regional power strain,’ highlighted by PG&E’s challenges, that is discussed in the section.

(Source: Statista)

Vertiv’s Dominance in High-Density Cooling for AI Servers (2024-2025)

The list of key players demonstrates that the AI buildout is a story of scaling commercially mature technologies, not one of research and development. The infrastructure being deployed is proven and robust. Vertiv’s position as the “AI Capacity King” for its advanced cooling solutions, which are essential for racks now exceeding 60 k W, shows the market is rewarding existing leaders who can deliver specialized, mission-critical hardware at scale. Similarly, Arista Networks‘ leadership in high-speed switches and Equinix’s vast interconnection ecosystem are established strengths being leveraged for AI. The most significant indicator of technology maturation is the ascension of Bloom Energy’s SOFCs. Once considered a niche alternative, its role in providing reliable, on-site power for data centers marks its transition to a mainstream, commercially viable solution for one of the world’s most demanding applications.

AI Data Center Power Demand to Explode

The explosion in AI-specific power demand, as shown in the chart, directly correlates to a massive increase in heat generation. This creates the market for the advanced, high-density cooling solutions in which Vertiv is a dominant player.

(Source: Deloitte)

$800 B Investment, Bloom Energy’s On-Site Power Adoption

The most critical strategic trend to monitor is the accelerating move by tech companies and data center operators to bypass traditional utility grid constraints through on-site power generation and direct energy partnerships. This shift elevates companies like Bloom Energy from component suppliers to pivotal strategic partners.

- If hyperscaler capital expenditure continues its aggressive trajectory, with giants like Microsoft and Amazon committing hundreds of billions, then demand for grid-bypass solutions will move from a niche to a standard requirement, directly benefiting Bloom Energy’s order book.

- If grid interconnection queues and permitting times continue to lengthen, expect a surge in direct partnerships between data center operators and on-site power providers. Bloom’s announced 2 GW production capacity ramp is a direct signal that it is preparing to meet this specific demand surge.

- If natural gas remains a cost-effective and reliable fuel source, companies like The Williams Companies will gain from providing direct pipeline access for data centers operating their own gas-fired generation, including those using SOFC technology.

Data Center Infrastructure Market Nears $1 Trillion

The chart shows the total addressable market for data center infrastructure approaching $1 trillion. This massive market size provides the context for the ‘$800 B Investment’ and growing adoption of on-site power solutions like Bloom Energy’s.

(Source: IoT Analytics)

The questions your competitors are already asking

This report covers one angle of the infrastructure stocks winning from the AI data center power buildout. The questions that matter most depend on your work.

- Which utility and on-site power companies are gaining or losing ground in the race to power AI data centers?

- What is the outlook for on-site power deployment, like SOFCs from Bloom Energy, in AI data centers by 2025?

- Which tech giants are funding their own power infrastructure, and who are their key utility and technology partners?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.