Data Center Grid Constraints, 1, 000 TWh Demand by 2026, 40% Operational Shortfalls, and 20% Connection Delays (2021 to 2026)

Grid Instability Risks, Data Center Demand Surge Exposes Infrastructure Limits

The rapid, concentrated growth of data centers is outpacing the development of electrical grids, creating a high-probability risk of connection delays, operational constraints, and localized power shortages. The core issue is a fundamental mismatch in development cycles: data centers can be built in 18-24 months, while essential high-voltage transmission projects often require a decade or more for planning, permitting, and construction. This temporal gap, a manageable concern in the 2021-2024 period, has now escalated into a critical infrastructure bottleneck threatening to stall digital economic growth.

- The International Energy Agency (IEA) projects global data center electricity demand will surge from 460 TWh in 2022 to over 1, 000 TWh by 2026, a level of consumption equal to that of Japan.

- Gartner forecasts that by 2027, power shortages will operationally constrain 40% of all AI data centers, a direct consequence of generative AI’s energy needs outpacing utility capacity.

- The IEA further warns that up to 20% of new data center capacity planned between 2025 and 2030 could face significant connection delays due to grid constraints, directly impacting deployment timelines.

- This strain is geographically concentrated in hubs like North Virginia, which had a demand of 3, 000 MW in 2022. In such regions, clusters of facilities create demand loads equivalent to entire cities, overwhelming local grid infrastructure.

$1 B+ in PPAs, Hyperscalers Fund New Energy to Secure Power

In response to grid limitations and to meet sustainability targets, hyperscale operators have become the dominant force in corporate energy procurement, using their immense purchasing power to directly fund new renewable energy generation through long-term Power Purchase Agreements (PPAs). These companies have shifted from being passive energy consumers to active, strategic procurers, underwriting the development of gigawatt-scale energy projects to secure their power supply years in advance. This strategy provides the revenue certainty needed for developers to finance and build new solar, wind, and even nuclear projects.

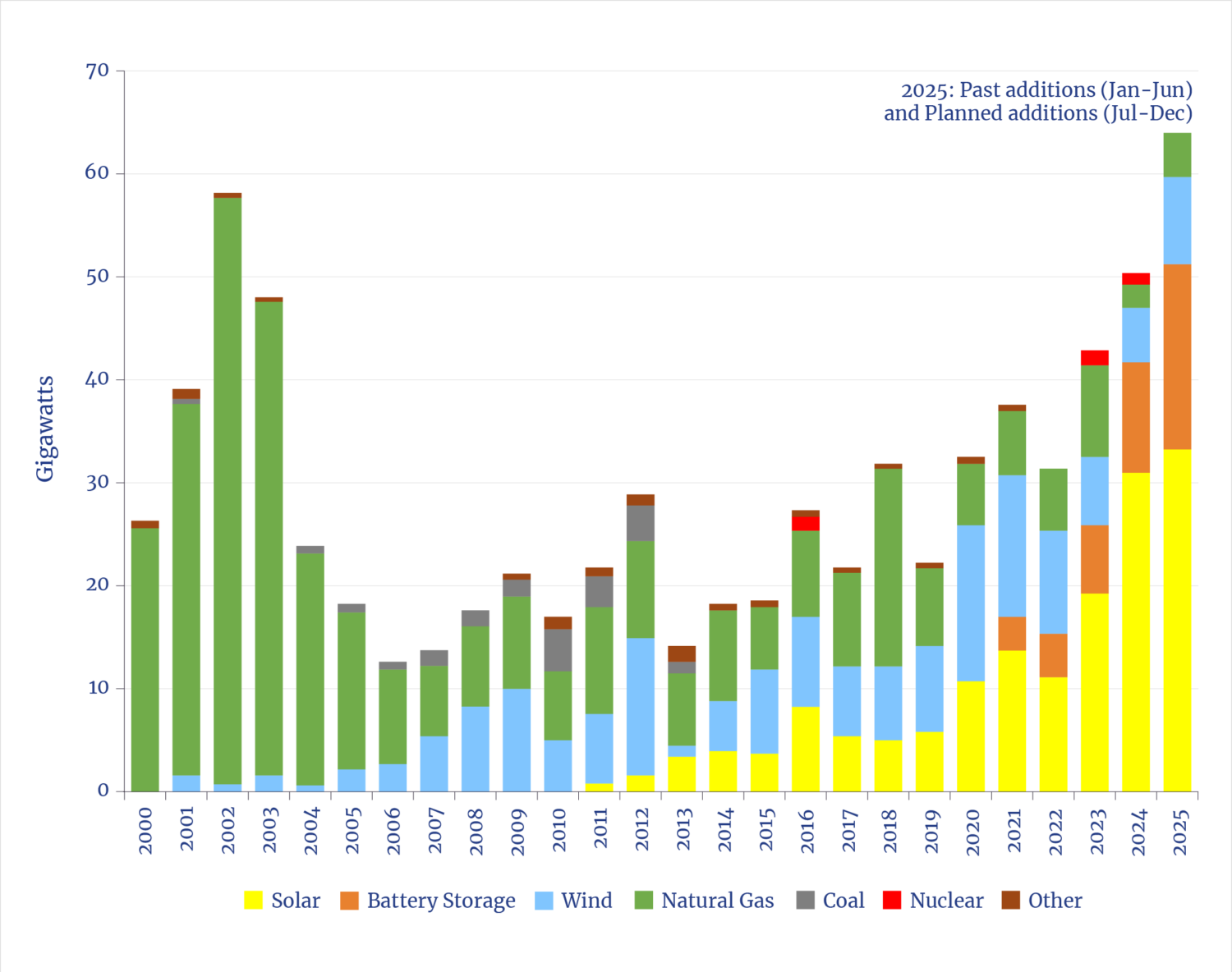

Renewables Dominate New US Grid Capacity

This chart shows the surge in new solar, wind, and storage capacity, which directly visualizes the outcome of hyperscaler PPA investments. Their funding is underwriting the massive expansion of renewable energy sources on the grid.

(Source: National Center for Energy Analytics)

- Hyperscalers like Amazon, Microsoft, and Google are the world’s leading corporate buyers of renewable energy, using 12 to 15-year PPAs to hedge against price volatility and secure clean power.

- In a significant strategic shift, these agreements are now expanding beyond traditional renewables. In October 2025, Google and Next Era Energy signed a PPA enabling investment to restart the Duane Arnold nuclear power plant, explicitly to provide 24/7 carbon-free energy for data centers.

- The scale of these deals is massive. In February 2026, Google partnered with Total Energies to deliver 1 GW of new solar capacity through two long-term PPAs to power its data centers in Texas.

- This procurement strategy directly addresses the grid bottleneck by stimulating the construction of new generation, although it does not solve the separate, and often more difficult, challenge of building the transmission lines to deliver that power.

Hyperscaler Partnerships, Google and Microsoft Forge Energy Alliances

Hyperscale operators are evolving beyond transactional power purchases to form deep strategic partnerships with energy producers and utilities, aiming to co-develop and secure gigawatt-scale capacity through integrated infrastructure planning. While the 2021-2024 period was characterized by a rapid increase in standard Virtual Power Purchase Agreements (VPPAs), the period from 2025 has seen a clear shift toward broader, more structural collaborations that address both generation and infrastructure challenges.

- In December 2025, Google and Next Era Energy announced a landmark strategic partnership to scale multiple gigawatts of data center capacity and associated energy infrastructure across the U.S., signaling a move toward co-development rather than just procurement.

- Microsoft announced a long-term strategic collaboration with ENGIE in February 2026, centered on multiple renewable PPAs, demonstrating a portfolio approach to securing power across different grid regions and technologies.

- This collaborative strategy marks an evolution from earlier deals, such as the November 2024 agreement where Repsol signed six long-term VPPAs with Microsoft, which were primarily financial contracts to support renewable generation off-site.

- These deeper alliances reflect a recognition that securing power for AI requires a more integrated approach, where data center planning and energy infrastructure development are executed in tandem.

Table: Key Hyperscaler Energy Partnerships (2024-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Microsoft and ENGIE | Feb 2026 | A long-term strategic collaboration focused on multiple renewable PPAs, designed to secure a large portfolio of clean energy for Microsoft’s expanding data center fleet. | Microsoft |

| Google and Total Energies | Feb 2026 | Two new long-term PPAs to deliver 1 GW of solar capacity specifically to power Google’s data centers in Texas, securing a massive block of regional power. | Total Energies |

| Google and Next Era Energy | Dec 2025 | A landmark strategic partnership to co-develop multiple gigawatts of data center capacity and the associated energy infrastructure, moving beyond procurement to integrated planning. | Next Era Energy |

| Google and Next Era Energy | Oct 2025 | A PPA enabling investment to restart the Duane Arnold nuclear plant, a strategic move to secure 24/7 carbon-free baseload power. | Next Era Energy |

| Microsoft and Repsol | Nov 2024 | Six long-term virtual power purchase agreements (VPPAs) to supply Microsoft with renewable electricity, representative of the large-scale financial hedges common before the shift to more direct partnerships. | Repsol |

US vs Europe, Regional Hotspots Strain Local Power Grids

The global data center energy problem is manifesting as a series of intense, local crises in specific geographic hotspots, with North America and Western Europe facing the most acute grid challenges. In the United States, 15 states account for 80% of the national data center load, creating extreme concentrations of demand that strain regional infrastructure and provoke regulatory responses. Europe faces a similar clustering issue, forcing governments to enhance monitoring and efficiency standards.

- In the U.S., states like Virginia, Iowa, and Nebraska are projected to have data centers consume over 20% of their total state electricity by 2030, a massive load increase driven by hyperscale growth.

- Europe’s data center market is heavily concentrated in Germany (~450 facilities), the United Kingdom (~400), and France (~250), creating intense pressure on dense, aging grid networks.

- Governments are now responding to this strain. The European Commission is preparing a “Data Centre Energy Efficiency Package” for Q 1 2026 to improve compliance, while Singapore’s Green Data Centre Roadmap from May 2024 incentivizes operators to adopt more efficient equipment.

Grid Infrastructure, Transmission Bottlenecks Stall Data Center Growth

The primary technological constraint limiting data center growth is the immaturity and slow development cycle of the energy transmission and distribution grid, not a lack of power generation technology itself. The core of the problem is the inability of legacy grid infrastructure to connect new, massive data center loads to available generation sources quickly and reliably. This bottleneck is exacerbated by supply chain shortages and lengthy regulatory processes.

- The critical weakness is the temporal mismatch: data centers are built in 18-24 months, while new high-voltage transmission lines require over a decade to permit and construct, creating a chronic power delivery gap.

- Supply chain constraints for critical grid components, especially high-voltage transformers, have become a major challenge, delaying both data center and utility projects and adding another layer of uncertainty to deployment schedules.

- While innovations like advanced liquid cooling systems promise greater energy efficiency at the facility level, many have a low Technology Readiness Level (TRL), which hinders widespread adoption and their ability to mitigate the larger, system-level grid problem.

- The rapid maturity of AI computation and its associated hardware, including advanced semiconductors, is the primary driver of demand, while the slow, legacy pace of grid modernization acts as the primary supply-side constraint.

SWOT Analysis, Data Center Energy Concentration Dynamics

The extreme concentration of data center energy demand among a few hyperscale operators presents a fundamental duality for the energy sector. This concentration creates severe grid stability risks and infrastructure bottlenecks. At the same time, the consolidated purchasing power of these few operators has become a primary driver for large-scale renewable energy investment, accelerating the energy transition in ways no other industry can.

Hyperscalers Drive Explosive Power Demand

This chart visualizes the core dynamic of the SWOT analysis: the concentration of power demand among hyperscalers. Their exponential growth is the primary driver of both grid risks and renewable investments.

(Source: National Center for Energy Analytics)

- Strengths: The immense, consolidated purchasing power of hyperscalers provides the demand certainty needed to de-risk and finance gigawatt-scale renewable energy projects through long-term PPAs.

- Weaknesses: The geographic and corporate concentration of demand creates single points of failure, strains local grids, and is constrained by a fundamental mismatch in development speeds between digital and energy infrastructure.

- Opportunities: This challenge creates an opportunity for a new paradigm of integrated planning, where utilities and data center operators co-develop infrastructure, and for regulators to mandate that these large energy users provide grid stability services.

- Threats: The primary threats are widespread project delays due to a lack of grid connection capacity, operational curtailment due to power shortages, and the potential for a public and regulatory backlash that could lead to building moratoria.

Table: SWOT Analysis for Digital Energy Concentration

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Hyperscalers were major buyers in the corporate PPA market, using VPPAs to meet sustainability goals. | Hyperscalers became the dominant force underwriting new renewable and even nuclear generation via direct, strategic PPAs (e.g., Google/Total Energies 1 GW deal). | The role of hyperscalers shifted from being just customers to being primary financiers of new energy generation. |

| Weaknesses | Analysts warned of future grid strain from projected data center growth and long interconnection queues. | IEA and Gartner validated these warnings with concrete forecasts: 20% of new capacity facing connection delays and 40% of AI centers facing operational constraints. | The weakness shifted from a theoretical risk to a quantified, near-term business constraint backed by major industry analysis. |

| Opportunities | The focus was on improving facility-level PUE and procuring renewable energy credits. | The opportunity has scaled up to system-level integration, with proactive utility planning for “future-ready” data center parks and strategic partnerships like Google/Next Era. | The solution space moved from optimizing individual data centers to redesigning the interaction between data centers and the grid itself. |

| Threats | The primary threat was seen as rising electricity costs and potential carbon taxes. | The threat evolved to fundamental physical constraints: an inability to get power at any price due to grid connection unavailability and component shortages for transformers. | The core threat is now about physical access to power, a more immediate and harder-to-solve problem than cost management. |

2026 Scenario, Will Gridlock Stall the AI Economy’s Growth?

The single most critical variable for 2026 is whether regulatory and utility actions to accelerate grid infrastructure permitting can keep pace with the exponential growth in AI-driven energy demand. The future of AI development is now inextricably linked to the physical constraints of the power grid, and the primary signal to watch is the speed of transmission development and interconnection reform.

AI Demand May Stall Economic Growth

This forecast shows AI’s role in driving data center energy use to over 5% of the global total, creating a potential gridlock scenario. It quantifies the ‘exponential growth in AI-driven energy demand’ that threatens to stall the AI economy.

(Source: National Center for Energy Analytics)

- If this happens: If efforts to streamline permitting for energy infrastructure, like the proposed bill in the U.S. Congress, gain traction and utilities begin to proactively develop “future-ready” industrial zones for data centers.

- Watch this: A reduction in interconnection queue times, an increase in announced utility-hyperscaler co-development projects, and a rise in investment in manufacturing capacity for critical components like high-voltage transformers.

- This could be happening: AI’s growth trajectory could continue with only regional friction, as hyperscalers concentrate investment in jurisdictions that successfully align energy and digital infrastructure policy, creating a new form of competitive advantage for those regions.

- Conversely: If permitting and grid investment continue to lag, the energy bottleneck will become the single greatest limiting factor on AI’s growth. Watch for an increase in data center project cancellations, a pivot to smaller and less efficient on-site generation, and hyperscalers shifting major investments to countries with excess power capacity, altering the geopolitical map of digital infrastructure.

The questions your competitors are already asking

This report covers one angle of the concentration of digital energy consumption and its impact on grid stability. The questions that matter most depend on your work.

- Which hyperscalers, like Amazon and China Mobile, are gaining or losing ground in the race to secure power for AI workloads?

- What is the outlook for new data center deployment in constrained hubs like North Virginia, given the IEA’s warning of 20% connection delays?

- Are the hyperscalers’ PPA strategies sufficient to mitigate Gartner’s projected 40% operational shortfall for AI data centers by 2027?

- What are the opportunities for on-site power generation and grid infrastructure providers created by the data center energy crunch?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.