BESS Cost Compression, 40% Price Drop to $117/k Wh, CATL-led Oversupply, and 9 GW of Project Cancellations (2023-2026)

BESS Supply Chain Risk, Chinese Dominance Creates 40% Cost Advantage

The dramatic fall in Battery Energy Storage System (BESS) costs is a direct result of manufacturing overcapacity, primarily in China, which has commoditized hardware but created significant geopolitical and supply chain vulnerabilities. This has shifted market risk from technology development to supply chain execution and geopolitical exposure.

- In the 2021 to 2024 period, the market was still balancing various battery chemistries and managing price volatility. By 2025, a massive scale-up in Chinese manufacturing led to a supply glut, causing prices to collapse. Full system quotes in China were reported as low as $65/k Wh, while similar systems in the U.S. cost $230-$320/k Wh, a cost advantage of over 40% for Chinese producers.

- The market has consolidated around lower-cost Lithium Iron Phosphate (LFP) chemistry, which now accounts for 91% of projects in mature markets like Australia. This move away from more expensive cobalt and nickel-based chemistries has helped insulate BESS costs from volatility in the electric vehicle market, but it further concentrates the supply chain in China.

- This concentration presents a direct threat to Western markets. The U.S. government has responded with tariffs that could increase BESS project costs by up to 50%. This highlights the strategic vulnerability of relying on a single region for critical energy infrastructure components.

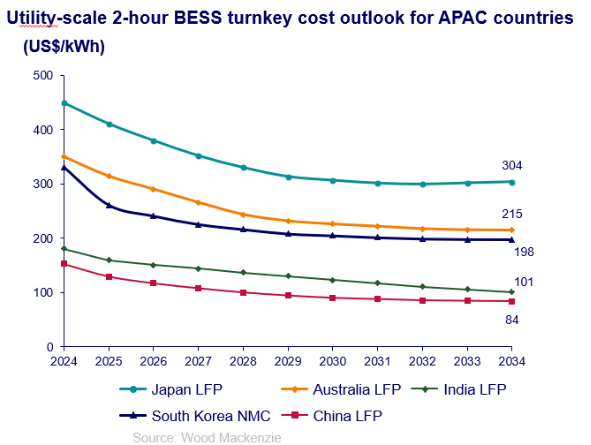

China’s BESS Cost Advantage to Persist Through 2034

The chart visualizes the persistent cost advantage China has in BESS manufacturing, directly supporting the section’s headline about Chinese dominance and the resulting 40% cost gap.

(Source: Wood Mackenzie)

$32 B in Cancellations, US Clean Energy Projects Face Policy Risk

Despite falling hardware costs that improve project economics on paper, a surge in project cancellations in 2025 reveals that non-equipment risks now represent the primary barrier to BESS deployment in the United States. These execution-level headwinds are overwhelming the benefits of cheaper hardware, stalling gigawatts of planned capacity.

- Policy and market uncertainty were the leading drivers of cancellations. In 2025, over $32 billion in U.S. clean energy projects were canceled due to shifting federal policies. In Texas, over 9 GW of renewable and storage capacity was canceled in a two-month period in 2025 due to market uncertainty, demonstrating how quickly capital can retract.

- Grid interconnection queues have become a primary bottleneck, with long wait times and high costs delaying projects indefinitely. This structural issue prevents developers from taking advantage of low equipment prices, leaving projects stranded in development pipelines.

- Supply chain policy has had a direct impact on domestic manufacturing plans. Following the announcement of new tariffs, an estimated 21 GWh of planned U.S. energy storage system cell production capacity for 2028 was canceled in July 2025, undermining efforts to build a resilient domestic supply chain.

- Local opposition is a growing constraint, with over 50 municipalities across the U.S. enacting bans or moratoriums on BESS facilities as of June 2026. This local-level resistance, often citing safety concerns, adds another layer of permitting and siting risk to project development.

NA BESS Market to Reach $19.87B by 2030

The chart quantifies the significant future value of the North American BESS market, providing crucial context for the section’s discussion on the financial impact of project cancellations and policy risks in the US.

(Source: MarketsandMarkets)

Table: BESS and Clean Energy Project Cancellations (2025-2026)

| Project / Capacity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Clean Energy Projects | 2025 | Over $32 billion in projects were canceled across the U.S. clean energy sector, with policy uncertainty cited as a major contributing factor. | Fast Company |

| U.S. ESS Cell Manufacturing | July 2025 | 21 GWh of planned domestic cell production capacity for 2028 was canceled due to new tariffs and market uncertainty, impacting domestic supply chain goals. | Energy-Storage.News |

| Texas Renewable & Storage Projects | May-June 2025 | Over 9 GW of capacity was canceled over a two-month period due to market uncertainty in Texas, reflecting investor sensitivity to regulatory risk. | Power Engineering |

China vs US/EU, BESS Cost Disparity Exceeds 40%

China has established an unassailable cost-leading position in the global BESS supply chain, creating a significant and persistent price disparity where turnkey systems in China are now less than half the cost of those in the United States. This geographic divergence defines the competitive dynamics of the global market.

- Between 2021 and 2024, global BESS supply chains saw growing Chinese influence, but a semblance of regional competition remained. By 2025, this changed decisively. Chinese manufacturing overcapacity drove a price war that solidified its market control.

- The price gap is stark. In early 2026, a complete four-hour utility-scale BESS in China could be quoted as low as $65/k Wh. In contrast, the same system cost between $180-$260/k Wh in Europe and $230-$320/k Wh in the U.S., reflecting differences in labor, permitting, and tariff impacts.

- While China’s supply-side push sets global price floors, the U.S. market is driven by demand-pull policies. The Inflation Reduction Act’s tax credits created a bankable market for standalone energy storage and are intended to foster domestic production, but this has not yet closed the significant cost gap with Chinese imports.

BESS Capex at $125/kWh Outside China/US

The chart provides a specific capital expenditure figure for BESS projects outside of China, which serves as a key data point to illustrate the cost disparity with China discussed in the section.

(Source: Energy-Storage.News)

LFP Batteries 91% Market Share, BESS Technology Maturation (2023-2026)

Lithium Iron Phosphate (LFP) chemistry has achieved full commercial maturity and market dominance for stationary storage, enabling the current cost collapse, while next-generation technologies like sodium-ion are now reaching commercial reality to drive the next cost-down cycle.

- The period from 2021 to 2024 saw LFP rapidly gain ground on the incumbent Nickel Manganese Cobalt (NMC) chemistry for stationary applications. By 2025, the transition was complete. LFP is now the default technology, accounting for over 91% of new projects in markets like Australia, chosen for its lower cost, superior safety profile, and absence of ethically and financially volatile materials like cobalt.

- This technological consolidation around LFP was a primary enabler of the price collapse to $117/k Wh. It allowed manufacturers to achieve massive economies of scale and optimize production lines for a single, stable chemistry.

- The technology landscape continues to evolve. In June 2026, battery giant CATL launched its TENER Sodium-Ion BESS, marking a critical step towards the commercialization of non-lithium chemistries. These alternative technologies promise to further reduce costs and mitigate raw material risks.

- At the same time, companies like Energy Dome (CO 2-based) and Form Energy (iron-air) are focused on developing multi-day storage solutions, addressing a separate grid need that four-hour lithium-ion systems cannot, signaling a future market segmentation by application duration.

SWOT Analysis, BESS Market Faces 50% Tariff Risk

The BESS market’s primary strength is its rapidly falling cost curve, but this is directly linked to its greatest weakness and threat: an over-reliance on a geographically concentrated supply chain vulnerable to geopolitical tensions and tariffs. The market has effectively traded a technology cost problem for a geopolitical execution problem.

- The central tension is between the low-cost hardware (Strength) and the concentrated supply chain (Weakness/Threat). The opportunity to meet new demand from AI data centers is significant, but this is contingent on overcoming execution risks like grid access and policy stability.

- The most critical change from 2021 to 2026 is the shift in the location of risk. Previously, risk was centered on high battery costs and technology immaturity. Today, the hardware is cheap, but the risk has moved to the port, the grid interconnection point, and the local permitting office.

BESS Market to Reach $108B by 2034

The chart’s projection of significant global market growth to $108B is a critical ‘Opportunity’ to be discussed within a SWOT analysis of the BESS market.

(Source: Market.us)

Table: SWOT Analysis for BESS Market Cost Compression

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Improving cost curve; growing policy support; technology validation with NMC and LFP. | Extreme price collapse ($117/k Wh); LFP dominance (91% share); strong demand-pull from IRA tax credits; proven bankability of projects. | The cost reduction thesis was validated beyond expectations. BESS is now a cost-competitive mainstream asset class, not a niche technology. |

| Weaknesses | High capital costs; reliance on cobalt and nickel; nascent supply chain. | Extreme supply chain concentration in China; long grid interconnection queues; significant project cancellations ($32 B in 2025); growing local opposition. | The primary weakness shifted from hardware cost to execution bottlenecks. The supply chain became more efficient but far less resilient. |

| Opportunities | Renewable energy firming; grid ancillary services; peak shaving applications. | Massive new demand from AI and data centers; market for long-duration storage (beyond 4 hours); development of new, cheaper chemistries (sodium-ion). | The addressable market expanded beyond the traditional grid. AI power demand emerged as a potential multi-billion dollar demand driver. |

| Threats | Raw material price spikes (lithium, cobalt); competition from other grid technologies. | Geopolitical tariffs (up to 50% cost increase on Chinese imports); abrupt policy reversals; sustained high interest rates impacting project finance. | Geopolitical risk fully replaced technology risk as the primary threat to market growth. Policy became both a key driver (IRA) and a key threat (cancellations). |

$117/k Wh Price Point, BESS Integrators Focus on Software

With BESS hardware rapidly becoming a low-margin commodity, the critical path to profitability in 2026 and beyond depends on software-driven revenue stacking and successfully mitigating non-hardware risks like grid access, permitting, and policy shifts.

- If hardware costs continue their downward trend, watch for the remaining project value to concentrate in software, integration, and market optimization services. This is already happening, as the ability to “stack” multiple revenue streams (arbitrage, ancillary services) via software is now the key determinant of project profitability.

- If geopolitical tensions between the U.S. and China escalate, watch for a potential bifurcation of the global market. One segment will feature high-cost, secure Western supply chains, while the other will be a low-cost, China-dominated ecosystem. The cancellation of 21 GWh of planned U.S. cell manufacturing capacity is an early signal of this trend.

- If electricity demand from AI and data centers materializes as projected, watch for BESS to become a required, co-located asset for new data centers to manage power loads and ensure reliability. This could create a massive new demand segment for the energy storage 2026 market, independent of traditional utility procurement cycles.

Battery Costs Fell 20% Annually Last Decade

The section highlights a specific low price point for BESS. The chart provides the essential historical context, showing the rapid annual cost decline that made such a price point achievable.

(Source: Energy-Storage.News)

The questions your competitors are already asking

This report covers one angle of the global battery storage market. The questions that matter most depend on your work.

- Data centers building co-located battery storage

- Sodium ion battery grid storage projects

- New US battery manufacturing plants under construction

- Battery storage revenue stacking software companies

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.