BESS for Data Centers: 56 GW Planned to Bypass Grid Delays, 30% IRA Credit & 4-7 Year Payback (2025-2026)

BTM BESS Commercial Scale, Data Centers Bypass 5+ Year Grid Queues

The primary driver for Commercial and Industrial (C&I) Behind-the-Meter (BTM) Battery Energy Storage System (BESS) adoption has shifted from a tactical cost-saving measure to a strategic necessity for power-intensive industries to bypass grid constraints. For hyperscale data centers, BTM storage is now a mission-critical tool to achieve speed-to-market, transforming the investment calculus from simple ROI to one of strategic imperative.

- Between 2021 and 2024, the business case for C&I BESS was primarily built on reducing peak demand charges and participating in energy arbitrage, with payback periods often stretching to 8-10 years, limiting adoption to companies with specific load profiles and a high tolerance for long-term ROI.

- In the 2025-2026 period, this model was upended by the voracious, non-discretionary power demand from AI and data centers. Faced with grid interconnection queues of up to seven years, developers are now deploying BTM generation and storage in a “Bring Your Own Power” (BYOP) strategy to accelerate operations.

- The scale of this shift is validated by an analysis of 46 BTM data center projects revealing 56 GW of planned capacity. This confirms that BESS is no longer an ancillary benefit but a core component of critical infrastructure deployment.

- The economics are now compelling, with a convergence of declining capital costs and the 30% Investment Tax Credit (ITC) for standalone storage compressing project payback periods into a bankable 4-to-7-year range, making these strategic deployments financially viable.

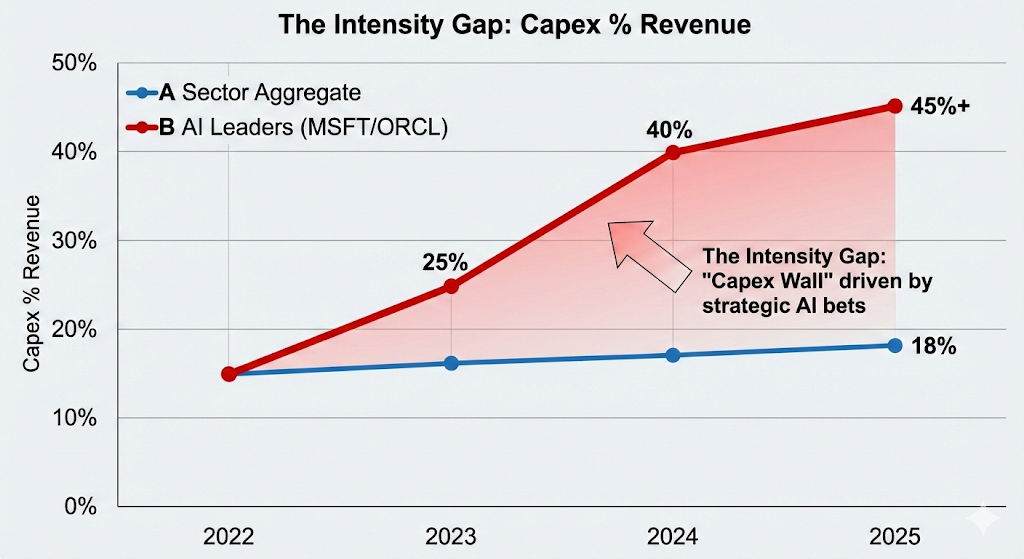

AI Leaders’ Capex Skyrockets Past Sector Average

The section discusses data centers using BESS to bypass grid queues. The chart showing skyrocketing capex from AI leaders provides the context and driving force for this trend, as AI requires massive data center expansion and reliable power.

(Source: Finance Hub)

$489 M in Project Financing, BESS Market Expansion Validates Bankability

The flow of significant, structured project financing into BTM BESS portfolios confirms that the financial community now views the asset class as bankable and self-sufficient, moving beyond speculative, single-project venture funding. This investor confidence is underpinned by predictable revenue streams from long-term contracts and the strong economics driven by new demand segments.

- A key signal of market maturity is the shift from financing individual projects to funding large portfolios of C&I systems. This demonstrates confidence in the standardized deployment model and the aggregated revenue potential.

- In Q 4 2025, Nexamp secured $350 million in long-term financing to fund the construction of its first utility-scale solar and BESS projects, indicating an ability to raise substantial capital for storage-inclusive portfolios.

- Similarly, es Volta closed $139.6 million in project financing for its Boxcar Energy Storage project in Texas, highlighting the availability of capital for large-scale BESS, even in merchant markets.

- This bankability is driven by investment models showing co-located BTM projects can achieve Internal Rates of Return (IRR) well above the typical 10% Weighted Average Cost of Capital (WACC), a threshold that standalone utility-scale projects often struggle to meet.

Table: BESS Project Financing and Investment

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Nexamp | Nov 2025 | Secured $350 million in long-term financing to fund a portfolio of solar and BESS projects. The deal signifies investor confidence in funding large-scale, storage-inclusive renewable asset portfolios. | [PDF] Green Front Energy |

| es Volta / Boxcar Project | Mar 2026 | Closed $139.6 million in project financing for its utility-scale BESS project in Texas. This demonstrates the ability to secure funding for large storage assets, even in markets with merchant risk. | Solar Builder Mag |

| Co-located BTM Projects | Nov 2025 | Analysis shows co-located projects charging behind the meter achieve IRRs significantly above the 10% WACC threshold, unlike standalone projects yielding only 4-5%. This justifies higher private investment in BTM assets. | Capstone DC |

BTM BESS Partnerships, Gridmatic 10-Year Offtake De-Risks C&I Projects

Long-term offtake agreements for BTM BESS have become the primary mechanism for de-risking projects, providing the predictable revenue streams necessary to secure non-recourse project financing. These contracts signal a maturation of the commercial model, moving from speculative merchant exposure to a more stable, utility-like cash flow profile that is attractive to institutional investors.

- Unlike the merchant-heavy models of 2021-2024, which exposed projects to volatile energy market pricing, the 2025-2026 period is defined by the use of long-term contracts like Power Purchase Agreements (PPAs) and tolling agreements to guarantee revenue.

- In June 2025, a 10-year offtake agreement was announced with Gridmatic to support four BTM solar and storage assets in California. This contract term length provides a decade of revenue certainty, making the portfolio highly attractive to lenders.

- The strategic purpose of these agreements is to remove downside revenue risk, thereby lowering the cost of capital and improving the overall project economics, which directly contributes to achieving the 4-7 year payback targets.

Table: BESS Strategic Partnerships and Offtake Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Gridmatic / California BTM Assets | Jun 2025 | A 10-year offtake agreement was signed to support four BTM solar-plus-storage assets. The long-term contract provides revenue predictability required to secure project financing. | [PDF] Fractal Energy |

| ERCOT Market | Sep 2025 | Analysis shows that offtake and tolling agreements in markets like ERCOT are critical for de-risking battery projects by providing predictable revenue streams, making them more attractive to lenders and investors. | Modo Energy |

Germany’s 2026 Blueprint for Energy Storage

While the section’s table details specific strategic partnerships, this chart on Germany’s national blueprint provides a contrasting, macro-level strategic approach. It offers a point of comparison between market-led partnership models and state-directed energy strategy in another major economy.

(Source: MateSolar)

US Dominates BTM BESS Growth, Driven by IRA Policy and Grid Constraints

The United States has solidified its position as the world’s leading growth market for BTM BESS, propelled by a powerful and unique combination of durable federal incentives, acute grid interconnection logjams, and the recent surge in electricity demand from the data center sector. While Europe and Asia continue to grow, the scale of the US opportunity is distinct due to these converging factors.

- Prior to 2025, BTM BESS growth was more evenly distributed globally, often tied to regional subsidy programs. The 2025-2026 period marks a consolidation of growth in the US, which is projected to see its BTM market expand from $26 billion in 2025 to $132 billion by 2035.

- The primary policy driver is the Inflation Reduction Act (IRA), which provides a 30% ITC for standalone storage. This was critically preserved by the 2025 One Big Beautiful Bill Act (OBBBA), insulating the storage market from rollbacks that affected other renewables and providing policy certainty.

- The most powerful catalyst is the physical constraint of the US grid. With interconnection queues for large projects stretching multiple years, BTM BESS has become an essential tool for data centers and other large power users to ensure operational timelines, a problem less acute in other regions.

- In Europe, payback periods have also contracted to a favorable 4-10 year range, as shown in analysis of markets like Spain and the UK, but the region lacks the same scale of concentrated, grid-constrained data center demand that is supercharging US deployment.

BESS Technology at Commercial Scale, CATL Leverages 95% RTE and LFP Chemistry

Lithium-ion BESS technology is now fully mature and bankable for C&I applications, with standardized performance benchmarks that meet stringent investor and operator requirements. The primary project risks have consequently shifted from technology performance and reliability to supply chain execution, permitting, and integration logistics. This transition allows developers to focus on deployment velocity rather than technology validation.

- While the 2021-2024 period saw continued debate over the optimal battery chemistry for stationary storage, by 2025 Lithium Iron Phosphate (LFP) has emerged as the dominant choice for C&I BESS due to its superior safety, longer cycle life, and lower cost compared to Nickel Manganese Cobalt (NMC).

- Key performance indicators are now standardized and bankable. High-performance systems from leading suppliers like CATL and Sungrow consistently deliver 85-95% Round-Trip Efficiency (RTE), a cycle life exceeding 8, 000 cycles, and are backed by 10+ year warranties. While LFP dominates, emerging iron-air technologies from companies like Form Energy are also being evaluated for longer-duration applications.

- This technological maturity means the conversation has moved from performance risk to execution risk. The central challenges are no longer “Will the battery work?” but “Can we secure a supply of batteries and install them on time and within budget?”

Grid Tiers Classify BESS and Generation Assets

This technology-focused section discusses BESS at a commercial scale. The chart, which classifies how BESS and other assets fit into different grid tiers, provides a technical, architectural context for deploying these technologies within the existing power system.

(Source: Climate Drift – Substack)

SWOT Analysis, BESS Market Economics vs. Interconnection Bottlenecks

The BTM BESS market’s core strength is its recently achieved economic viability, driven by falling costs and robust policy support, which is unlocking massive demand from data centers needing to bypass grid limitations. However, this rapid growth is threatened by the very grid issues it seeks to solve, alongside persistent supply chain and permitting hurdles that could constrain deployment.

Table: SWOT Analysis for Behind-the-Meter BESS Adoption

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Declining CAPEX; growing C&I interest in peak shaving. | Payback periods hit a bankable 4-7 year range. CAPEX falls to $110-$580/k Wh. LFP chemistry becomes standard, offering high cycle life (>8, 000) and safety. | The business case became self-sustaining and is no longer solely dependent on high subsidies. Technology is proven and bankable. |

| Weaknesses | High initial CAPEX was a major barrier for most businesses. Payback periods of 8-10 years were unattractive. | Grid interconnection queues remain a major bottleneck, even for BTM projects. Permitting complexity and varying local codes (UL 9540, NFPA 855) add soft costs and delays. | While CAPEX has fallen, the key weakness has shifted from hardware cost to the bureaucratic friction of project deployment. |

| Opportunities | Energy arbitrage and demand charge management were the primary use cases. | Insatiable, non-discretionary power demand from AI and data centers creates a premium customer segment. The 30% IRA tax credit for standalone storage is preserved. New Eaa S financing models emerge. | The market opportunity expanded from a cost-saving tool to a mission-critical enabler for the digital economy, creating a much larger addressable market. |

| Threats | Policy uncertainty and reliance on subsidies. Technology performance risk. | Supply chain disruptions for core components and raw materials. Geopolitical tensions and trade tariffs on equipment from China. Inability of developers to scale deployment velocity to meet demand. | The primary threat shifted from policy and technology risk to geopolitical and execution risk. The market is now vulnerable to supply-side shocks. |

BESS Market 2026 Outlook: Data Center Deployments vs. Supply Chain Constraints

The defining strategic question for the BTM BESS market in 2026 is whether the supply chain and developer ecosystem can scale rapidly enough to meet the urgent, inelastic demand from the data center industry. The outcome will determine if the sector can maintain its growth trajectory or if it will be throttled by physical and logistical constraints, leading to a bifurcation between strategic and non-strategic projects.

- If the urgent demand from data centers continues to accelerate as expected, watch for major BESS integrators and manufacturers to sign multi-year, multi-gigawatt supply agreements directly with hyperscalers, effectively reserving a significant portion of future production capacity.

- If supply chain constraints, tariffs, or raw material costs intensify, watch for a clear split in the market. Large, strategic customers like data centers will likely secure their supply at premium prices, while smaller, independent C&I projects could face significant delays and cost escalations.

- These could be happening: Reports of data center developers “restructuring for AI demand” and the identification of 56 GW in planned BTM-powered projects already confirm the demand-side momentum. The immediate focus must now shift to monitoring the supply-side response and any emerging bottlenecks in equipment or skilled labor.

The questions your competitors are already asking

This report covers one angle of the commercial acceleration for Behind-the-Meter BESS. The questions that matter most depend on your work.

- What is the outlook for BTM BESS deployment in the AI data center sector through 2026?

- What is actually happening with the 56 GW of planned BTM data center capacity?

- How does the 4-7 year payback period, including the 30% ITC, compare to previous BESS project economics?

- Which data center operators are adopting Behind-the-Meter BESS to bypass grid interconnection queues?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.