BESS Cost Leadership, $90/k Wh LFP Systems, 24 GW US Deployment, and Albemarle’s 30% Lithium Demand (2025-2026)

BESS Supply Chain Risks, Albemarle Navigates FEOC Rules and 43% Demand Growth

The rapid, large-scale adoption of Battery Energy Storage Systems (BESS), driven by cost-competitiveness and explosive new demand from artificial intelligence, is forcing a critical realignment of the global supply chain. The industry’s focus is shifting from a pure cost-reduction model, which characterized the 2021-2024 period, to one that now prioritizes geopolitical resilience, regulatory compliance, and security of supply. This transition creates significant execution risks and opportunities for upstream suppliers like Albemarle and downstream project developers.

- Between 2021 and 2024, the primary industry focus was on scaling manufacturing and driving down costs, leading to a heavy reliance on established Chinese supply chains for materials and components.

- Starting in 2025, the implementation of the U.S. Inflation Reduction Act (IRA), particularly its Foreign Entity of Concern (FEOC) rules, began to fundamentally reshape procurement strategies. This created a strong incentive for developing non-Chinese supply chains, even at a potential cost premium.

- The sudden, massive increase in electricity demand from AI data centers has become the single most powerful driver for new BESS deployments in 2026. This has intensified pressure on an already strained supply chain and exacerbated grid interconnection bottlenecks.

- This strategic shift is evident in Albemarle’s positioning, where its low-cost lithium operations in Chile and Australia become not just an economic advantage but a crucial geopolitical asset for Western BESS markets. The company projects BESS will account for approximately 30% of global lithium demand in 2026.

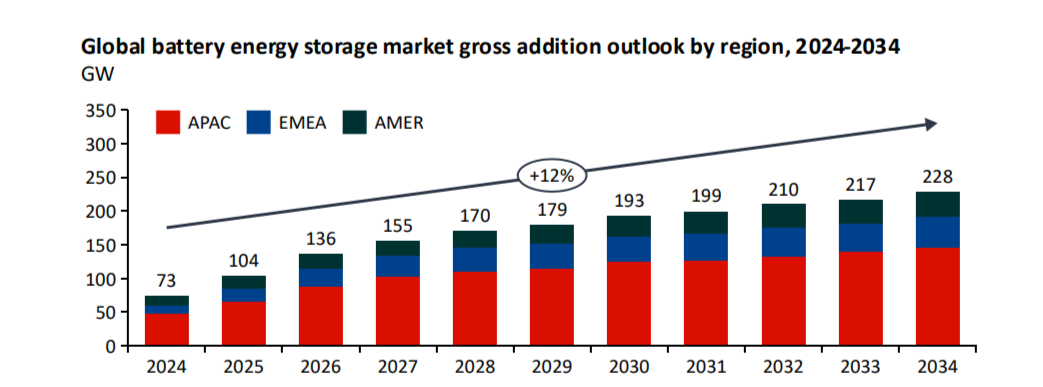

Global BESS Market Set for 12% Annual Growth

The section discusses macro-level supply chain risks and demand growth. This chart provides the global context for this growth, quantifying the market’s annual expansion rate, which is a key driver underpinning the supply chain challenges and demand figures mentioned.

(Source: ESS News)

US vs China, Albemarle BESS Deployment & Policy Impact

While BESS deployment is accelerating globally, the market is geographically bifurcating due to divergent policy and economic drivers, with the U.S. and China emerging as the two primary, but distinct, growth poles. The U.S. market is driven by strong policy incentives and the urgent need to support new load growth, while China continues to lead on manufacturing scale and absolute cost leadership, creating a complex global dynamic for companies like Albemarle that serve both markets.

- In the U.S., developers plan to add a record 24 GW of utility-scale storage in 2026, a significant increase from the previous year. This surge is directly supported by the IRA’s 30% standalone storage investment tax credit, which has made project economics highly attractive.

- China’s market continues to define the global cost floor. In 2026, installed costs for 4-hour Lithium Iron Phosphate (LFP) systems in China can be as low as $90/k Wh, compared to a range of $90 to $320/k Wh in other global regions, reflecting its manufacturing dominance.

- This geographic split creates a premium for IRA-compliant and non-FEOC supply chains. Albemarle’s ability to supply lithium from allied nations positions it to directly benefit from the policy-driven demand in the U.S. and Europe.

- The strain on U.S. infrastructure is a major regional challenge, with long interconnection queues cited as a primary bottleneck preventing gigawatts of planned BESS projects from connecting to the grid in a timely manner.

North America BESS Market to Exceed $50B by 2031

The section focuses on the US market, policy, and deployment in a competitive context with China. This chart quantifies the significant expected growth of the North American market, providing crucial context for the discussion of US policy impact and deployment scale.

(Source: Mordor Intelligence)

Albemarle and LFP Dominance in BESS Technology (2025-2026)

By 2026, lithium-ion has solidified its position as the dominant commercial technology for stationary energy storage, with Lithium Iron Phosphate (LFP) chemistry emerging as the definitive choice for grid-scale applications. This technological consolidation simplifies the upstream supply chain, increasing the strategic importance of reliable, low-cost lithium producers like Albemarle, while alternative chemistries continue to advance but have not yet achieved comparable market scale.

- During the 2021-2024 period, a mix of chemistries, including Nickel Manganese Cobalt (NMC), competed for the stationary storage market. By 2026, LFP has become the primary technology due to its superior safety profile, longer cycle life, lower cost, and avoidance of cobalt.

- Alternative technologies are emerging but remain at earlier stages of maturity. Sodium-ion batteries are progressing from lab-scale prototypes (TRL 4–6) toward commercial readiness, representing a potential long-term alternative but not a significant commercial competitor in 2026.

- The market’s expansion has attracted a diverse set of players, from large-scale system integrators like Sungrow aiming for massive US capacity, to specialized project developers such as Spearmint Energy managing significant project queues in key markets like ERCOT and CAISO. Legacy industrial firms like Rolls-Royce are also deploying BESS for grid services, while innovators such as Form Energy are advancing alternative long-duration chemistries like iron-air.

- Albemarle’s core business, the production of lithium, is directly aligned with the dominant LFP technology, securing its role as a critical enabler of the entire BESS ecosystem’s growth.

Electrochemical Storage to Capture 27% of Market in 2026

The section highlights the dominance of LFP battery chemistry, a type of electrochemical storage, in the 2025-2026 timeframe. The chart directly supports this by forecasting the market share that electrochemical storage will capture in 2026.

(Source: Coherent Market Insights)

BESS SWOT Analysis, Albemarle’s Cost Leadership and Market Risks

Albemarle’s strategic position is defined by the strength of its low-cost lithium assets, which directly addresses the immense opportunity of surging BESS demand. However, the company and the broader industry face significant external threats from complex supply chain regulations and infrastructure bottlenecks, creating a dynamic risk-reward environment in 2026.

- The company’s primary strength is its access to low-cost lithium resources, a crucial advantage that is becoming more valuable under new geopolitical trade rules.

- A key opportunity is the new, massive demand vector from AI data centers, which is accelerating BESS adoption beyond previous forecasts.

- The most significant threat is regulatory and infrastructural, including navigating stringent FEOC rules and overcoming chronic grid interconnection delays that can stall projects.

Energy Storage Market Drivers and Restraints Visualized

This section conducts a SWOT analysis, examining factors like cost leadership and market risks. The chart, which visualizes market drivers (Opportunities/Strengths) and restraints (Threats/Weaknesses), provides a perfect visual representation of the core components of a SWOT analysis.

(Source: Coherent Market Insights)

Table: SWOT Analysis for Albemarle and the BESS Market

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Albemarle operated as a leading low-cost lithium producer, primarily serving a rapidly growing EV market. | Low-cost assets in Chile and Australia are identified as a key strategic advantage for supplying IRA and FEOC-compliant BESS markets. | The geopolitical value of non-Chinese, low-cost resources was validated, shifting the asset’s worth from purely economic to strategic. |

| Weaknesses | High exposure to the cyclical nature and price volatility of the lithium market. | The company states a strategy of improving margins independent of price, but analyst upgrades and market perception remain tightly linked to lithium price recovery. | An internal strategy to mitigate the weakness was articulated, but external market validation still hinges on the commodity price itself. |

| Opportunities | The primary growth driver was the accelerating global adoption of electric vehicles. BESS was a secondary, albeit growing, market. | Explosive electricity demand from AI data centers emerges as a new, powerful demand driver for BESS, which is now expected to consume 30% of lithium supply. | A massive, inelastic, and grid-critical demand vector for BESS emerged, fundamentally increasing the size and urgency of the market opportunity. |

| Threats | Risks included standard commodity price fluctuations and competition from other lithium producers. | Complex regulations (FEOC rules) and physical infrastructure limits (grid interconnection queues) become the primary bottlenecks threatening market growth. | The nature of risk shifted from market-based to regulatory and infrastructural, indicating a more mature but constrained industry. Source: Recharge News, DNV. |

24 GW in 2026, Albemarle BESS Market Execution

For the remainder of 2026, the primary uncertainty facing the BESS market is not demand, which is effectively assured by grid needs and AI-driven load growth, but the industry’s collective ability to execute deployment at scale. The critical factors to watch are the industry’s success in navigating both regulatory and physical infrastructure constraints that currently cap the pace of growth.

- If federal and regional efforts to streamline grid interconnection queues show tangible progress, watch for an acceleration of project construction as the 24 GW of planned U.S. capacity for 2026 is pulled through the development pipeline faster than anticipated.

- If compliance with FEOC rules proves more complex or costly than developers have budgeted, watch for a potential wave of project delays or repricings. This could challenge the BESS cost-reduction curve for the first time in years.

- These could be happening now: The recent 17% single-month increase in battery-grade lithium carbonate prices, reported in early 2026, may be an early signal that surging demand from the BESS sector is beginning to outstrip the available near-term supply, confirming the market’s tightness.

US Adding 24.3 GW of Battery Storage in 2026

The section heading points to a specific execution target of “24 GW in 2026.” The chart provides a near-identical forecast, stating that the US will add “24.3 GW of Battery Storage in 2026,” directly corroborating the section’s central data point.

(Source: ESS News)

The questions your competitors are already asking

This report covers one angle of the BESS supply chain’s strategic pivot from pure cost reduction to geopolitical resilience. The questions that matter most depend on your work.

- Which lithium suppliers are gaining or losing ground in the North American BESS market due to FEOC rules?

- What is the outlook for BESS deployment to power AI data centers, and how are supply chain constraints impacting this growth?

- What is the cost breakdown of a sub-$90/kWh LFP BESS system, and what is the premium for an FEOC-compliant supply chain?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.