Hydrogen Reality Check 2026: Why Project Cancellations Expose a Deep Viability Gap

Hydrogen Project Risks: Ambition Collides with Commercial Reality

The global hydrogen market is undergoing a structural correction as a wave of project cancellations in 2024 and 2025 exposes a deep viability gap between ambitious production targets and current economic realities. The period from 2021 to 2024 was characterized by a surge in mega-project announcements, but since early 2025, the industry has shifted to a phase of retrenchment. This is driven by a failure to secure bankable offtake agreements, persistent cost inflation, and policy uncertainty, forcing developers to abandon projects that are no longer financially tenable.

- Between 2021 and 2024, the market was defined by large-scale announcements, such as Australia’s 12 GW Hy Energy project and Air Products‘ $4.5 billion Texas green hydrogen joint venture, reflecting high investor optimism.

- The period from 2025 to today has been marked by a reversal, with the cancellation of these same flagship projects. Air Products exited its Texas JV in November 2024, and the Hy Energy project was halted, signaling a market-wide pivot away from speculative, large-scale developments.

- The “ambition and implementation gap” is now a dominant theme, with less than 4% of the globally announced 520 GW of hydrogen capacity to 2030 having entered construction. Only 3.6 million tonnes per annum (mtpa) of binding offtake is in place, insufficient to support the vast pipeline of proposed projects.

- Cancellations span all applications, from industrial decarbonization (Shell’s Aukra project) and fertilizer production (Fortescue’s Gibson Island) to clean mobility (Air Products‘ New York plant), indicating that the economic challenges are sector-agnostic and systemic.

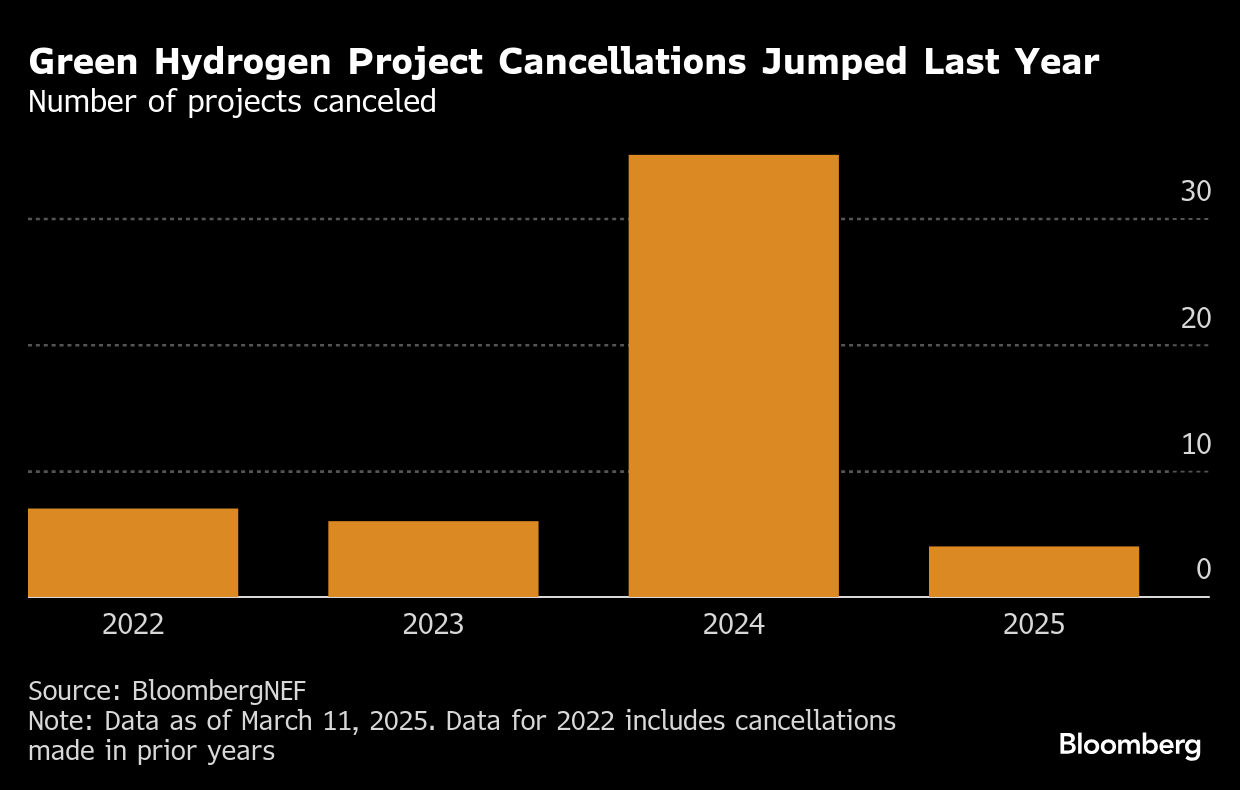

Project Cancellations Surged Dramatically in 2024

This chart directly illustrates the ‘wave of project cancellations in 2024’ mentioned in the section, providing clear visual evidence for the market’s structural correction.

(Source: Energy Connects)

Hydrogen Cancellation Analysis: A Market Correction in Motion

The extensive project cancellations across 2024 and 2025 are not isolated incidents but a systemic market correction driven by a mismatch between high production costs and the price end-users are willing to pay. This “viability gap” has been exacerbated by unfavorable regulatory shifts and rising capital costs, leading major industrial players to write off hundreds of millions in investments and exit high-profile ventures. The data shows a clear trend of projects being shelved after feasibility studies revealed untenable economics or after crucial government support was withdrawn.

Policy Uncertainty Is Primary Driver of Cancellations

This chart supports the section’s analysis by identifying policy and market uncertainty as the leading causes of cancellations, reinforcing the argument that commercial and regulatory issues are derailing projects.

(Source: Global Hydrogen Hub)

Table: Major Hydrogen Project Cancellations and Postponements (2024-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power New York Plant | 2025 | Abandoned North America’s planned largest green hydrogen plant due to market conditions; space sold to a data center. | Industrial Info |

| California Hydrogen Hub | 2025 | The Trump administration canceled a $1.2 billion contract for California’s flagship hydrogen hub, part of a broader termination of DOE awards. | Politico Pro |

| bp‘s Australian Renewable Energy Hub (AREH) | July 2025 | bp withdrew from the massive 26 GW project, a cornerstone of Australia’s green hydrogen export ambitions. | PV-Tech |

| Hy Stor Energy Electrolyzer Deal | December 2024 | Canceled a significant reservation for over 1 GW of electrolyzer capacity with Nel, citing a slower-than-hoped market development. | Reuters |

| Air Products Texas JV | November 2024 | Withdrew from a $4.5 billion, 1.4 GW green hydrogen joint venture in Texas, citing a strategic portfolio re-evaluation. | Renewables Now |

| Shell‘s Aukra Blue Hydrogen Project | September 2024 | Halted the 2.5 GW blue hydrogen project in Norway, intended to produce 1, 200 metric tons per day, due to a lack of sufficient offtake demand. | S&P Global |

Partnership Dynamics: Alliances Dissolve Amid Economic Headwinds

The trend of project cancellations is mirrored by the dissolution of major partnerships and joint ventures, indicating that even alliances between industry giants are not immune to the sector’s harsh economic realities. The period from 2021 to 2024 saw the formation of numerous large-scale consortiums to de-risk development. However, since late 2024, several of these foundational partnerships have been terminated as lead partners reassess financial exposure and strategic priorities in a market with uncertain returns.

Table: Notable Partnership Exits in Hydrogen Projects

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| bp / Australian Renewable Energy Hub (AREH) | July 2025 | bp‘s exit from the AREH consortium, a project designed for large-scale green hydrogen export, removes a key industrial anchor and jeopardizes the project’s future. | PV-Tech |

| Stanwell Corporation / Gladstone Project | July 2025 | The state-owned utility exited a major green hydrogen project in Gladstone, Queensland, which was planned to scale up to 2.88 GW of electrolysis capacity. | pv magazine Australia |

| Air Products / Texas Green Hydrogen JV | November 2024 | Air Products pulled out of its JV for a $4.5 billion green hydrogen project, effectively ending what was slated to be the largest facility of its kind in the U.S. | C&EN |

| Province Resources & Total Eren / Hy Energy Project | 2024 | The 12 GW Hy Energy green hydrogen project in Australia was halted, reflecting the immense challenge of financing and securing offtake for mega-projects even with strong partners. | Cleantech Group |

Geographic Analysis: Policy and Cost Headwinds Stall Projects Globally

The wave of hydrogen project cancellations is a global phenomenon, with distinct regional drivers exposing unique vulnerabilities in North America, Europe, and Australia. While the ambition to establish regional hydrogen economies was a common goal from 2021-2024, the period since 2025 has highlighted how specific policy missteps, regulatory uncertainty, and unfavorable local cost structures are derailing projects across all major aspiring production hubs.

Cancelled Capacity Dwarfs Operational Capacity Globally

This chart visualizes the global scale of the problem discussed in the section, highlighting how cancelled capacity, particularly in the US and Australia, vastly exceeds the current operational base.

(Source: National Mining Day)

- North America: The U.S. has been hit by abrupt shifts in government policy. The 2025 cancellation of the $1.2 billion contract for California’s Hydrogen Hub and uncertainty surrounding the 45 V tax credit rules were primary drivers for Air Products abandoning three U.S. projects and Plug Power scrapping its New York facility.

- Europe: Projects are stalling due to a combination of regulatory delays, insufficient subsidies, and high energy costs. Repsol froze 350 MW of projects in Spain in October 2024, blaming a new windfall tax. In Norway, Shell halted its massive Aukra blue hydrogen project, citing a lack of demand, while the planned Germany-Norway hydrogen pipeline was shelved.

- Australia: Once seen as a future hydrogen superpower, Australia is now a leader in cancellations. The exits of bp from AREH and Trafigura from its Port Pirie project, along with Fortescue’s project write-offs, were all driven by feasibility studies revealing prohibitive costs, particularly for renewable electricity.

Technology Maturity: Commercial Viability, Not Technical Readiness, Is the Bottleneck

The current market correction is not a failure of hydrogen technology itself, but a failure of the commercial ecosystem needed to support its deployment at scale. While the period from 2021 to 2024 saw significant advances in electrolyzer manufacturing and announcements of new gigafactories, the cancellations of 2025 demonstrate that technical readiness does not guarantee economic viability. The core issue is the immaturity of the market structure, including a lack of offtake security and transport infrastructure.

Uncontracted Projects Highlight Commercial Viability Gap

This chart directly quantifies the section’s main point—that commercial viability is the bottleneck—by showing the high volume of at-risk projects lacking secured buyers (‘uncontracted’).

(Source: Carbon Credits)

- From 2021 to 2024, companies like Fortescue invested in manufacturing capacity, planning a 2 GW PEM electrolyzer factory in Gladstone. However, in May 2025, the company announced it was considering mothballing the factory due to a lack of orders, a direct consequence of project cancellations.

- The cancellation of Hy Stor Energy‘s order for over 1 GW of electrolyzer capacity in December 2024 is a clear signal that manufacturing capacity is outpacing real-world project deployment, creating a supply-side glut with insufficient demand.

- The shelving of critical infrastructure, such as the Norway-Germany hydrogen pipeline and the Heartland Greenway CO 2 pipeline in the U.S., underscores the classic “chicken-and-egg” problem: production projects cannot proceed without transport infrastructure, and infrastructure will not be built without committed production.

- The issue is not whether green or blue hydrogen *can* be produced, but whether it can be produced at a price competitive with alternatives and with enough demand certainty to secure financing. Ørsted‘s Flagship ONE project cancellation due to offtake difficulties exemplifies this commercial bottleneck.

SWOT Analysis: De-Risking Becomes the New Imperative

The hydrogen market is at a critical inflection point where initial optimism has been tempered by financial and logistical realities. A SWOT analysis reveals an industry with proven technological potential but facing severe commercial weaknesses and external threats that have stalled its near-term growth trajectory. The key change from the 2021-2024 hype cycle to the 2025 reality check is the validation of high costs and weak demand as primary barriers, forcing a strategic shift from ambition to execution.

Table: SWOT Analysis for the Global Hydrogen Market

| SWOT Category | 2021 – 2024 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Growing pipeline of mega-projects; strong policy support announced (e.g., U.S. IRA, REPower EU); increasing electrolyzer manufacturing capacity. | Proven ability to develop smaller-scale, localized projects; established industrial players (Shell, bp, Air Products) remain engaged despite setbacks. | The underlying technology is not the primary barrier. The market has validated that the core challenge is commercial, not technical. |

| Weaknesses | High projected production costs (the “green premium”); reliance on anticipated subsidies; lack of binding offtake agreements. | High capital costs and interest rates make projects unbankable; offtake demand remains largely speculative; ambition-implementation gap widens significantly. | The weakness of speculative project economics was validated. The “if you build it, they will come” model failed, confirmed by cancellations from Shell and Repsol citing lack of demand. |

| Opportunities | Decarbonization of hard-to-abate sectors (steel, chemicals, shipping); potential for large-scale energy export (e.g., Australia to Asia). | Pivot to smaller, co-located projects with guaranteed industrial offtakers (e.g., refineries, ammonia plants) to ensure bankability. | The market is being forced to prioritize realistic, demand-led projects over speculative mega-hubs, creating an opportunity for more resilient business models. |

| Threats | Potential for policy changes; supply chain bottlenecks for key components; competition from other decarbonization pathways. | Policy volatility becomes reality (U.S. DOE funding cuts, EU windfall taxes); persistent cost inflation for equipment and electricity; slow development of midstream infrastructure. | The threat of policy risk was validated by the cancellation of the California Hydrogen Hub and Air Products‘ projects. High costs were validated as the reason for shelving projects in Australia and Germany. |

Scenario Modelling and 2026 Outlook

If the fundamental viability gap between high production costs and weak demand persists, the hydrogen market will continue to consolidate, with more cancellations of large, speculative projects expected through 2026. The most critical signal to watch for a market recovery is the signing of binding, long-term offtake agreements at a scale sufficient to underpin project financing. The primary strategic action for developers is to pivot away from standalone mega-projects and toward smaller, phased developments that are co-located with committed industrial buyers.

Demand Gap Defines Market’s Cautious Outlook

This chart provides context for the section’s cautious outlook by illustrating the significant gap between current, traditional demand and the ambitious new applications required for a net-zero scenario.

(Source: Global Hydrogen Hub)

- Watch this signal: The volume and value of Final Investment Decisions (FIDs). A continued drought of FIDs for large-scale projects will confirm the market stagnation, while a pickup in FIDs for smaller, demand-led projects will signal the start of a more sustainable growth phase.

- This could be happening: A flight to quality. Investors will increasingly favor projects with secured offtake, clear regulatory support, and a phased development plan. The cancellations by giants like Shell, bp, and Air Products have taught the market that even the largest players cannot overcome poor project economics.

- Traction Gaining: Co-located projects. The most resilient models will involve producing hydrogen adjacent to its point of consumption, such as a refinery or steel mill. This eliminates transportation costs and offtake risk, which have been fatal flaws in many canceled projects.

- Losing Steam: Speculative export hubs. The vision of countries like Australia becoming massive hydrogen exporters is fading rapidly. The cancellations of AREH and the Hy Energy project indicate that the economics of producing, converting (to ammonia), and shipping hydrogen are currently unworkable without massive, sustained subsidies.

Frequently Asked Questions

Why are so many major hydrogen projects being canceled in 2024 and 2025?

Projects are being canceled due to a “deep viability gap” where the high cost to produce hydrogen far exceeds the price end-users are willing to pay. This economic challenge is worsened by three key factors: a failure to secure binding, long-term purchase contracts (offtake agreements); rising capital costs and inflation; and policy uncertainty, such as the cancellation of government subsidies or the introduction of new taxes.

Does this mean the technology for producing green or blue hydrogen is the problem?

No, the article clarifies that the issue is commercial, not technical. The technology to produce hydrogen, such as electrolyzers, is considered ready. The primary bottleneck is the immature commercial ecosystem, including a lack of guaranteed buyers, missing transport infrastructure, and an unbankable business case. Projects are failing because they are not economically viable at scale, not because they are technically impossible.

Are these cancellations happening in one specific region, or is it a global problem?

It is a global phenomenon affecting all major aspiring production hubs. In North America, projects have been stalled by abrupt policy shifts and subsidy uncertainty. In Europe, high energy costs and regulatory delays are key factors. In Australia, once seen as a future hydrogen superpower, projects are being shelved after feasibility studies revealed prohibitive costs, particularly for renewable electricity.

What types of hydrogen projects are most at risk of being canceled?

The projects most at risk are large-scale, speculative “mega-projects” and those focused on long-distance exports. These ventures, such as Australia’s AREH and Hy Energy projects, often lack committed buyers and face unworkable transportation economics. The market is shifting away from the “if you build it, they will come” approach that defined the 2021-2024 hype cycle.

Given these setbacks, what does the future of the hydrogen industry look like?

The future of the hydrogen industry is likely to be more pragmatic and focused on de-risking projects. The trend is shifting away from speculative mega-hubs and toward smaller, phased developments that are co-located with committed industrial buyers (e.g., refineries, ammonia plants). This model eliminates transportation costs and guarantees demand, making projects more bankable and resilient.