Bloom Energy SOFC Manufacturing, 2.8 GW Oracle Deal, $5 B Brookfield Financing, and MTAR Supply Chain Ramp (2021-2026)

SOFC Adoption for Data Centers, Bloom Energy 2.8 GW Oracle Deal

The period from 2025 to today marks a definitive shift for Solid Oxide Fuel Cells (SOFCs) from a niche backup power application to a primary, gigawatt-scale solution for AI data centers, driven by grid infrastructure limitations. This transition validates the technology’s role as a core component of the digital economy’s energy supply, moving it from the periphery to the center of critical infrastructure deployment.

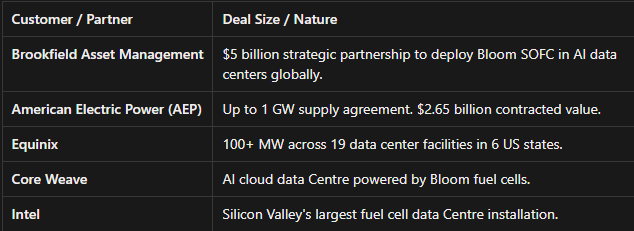

- Between 2021 and 2024, SOFC adoption was characterized by smaller, sub-100 MW deployments, often with colocation providers like Equinix, which proved the technology’s reliability but did not represent a fundamental challenge to traditional utility service. These projects established a track record for on-site, high-efficiency power but operated at a scale that supplemented, rather than replaced, grid dependency.

- Starting in late 2025 and accelerating into 2026, the market dynamic changed with the announcement of multi-gigawatt offtake agreements. The master services agreement for Bloom Energy to supply up to 2.8 GW to Oracle and a separate deal for up to 1 GW with utility American Electric Power (AEP) signify a new phase where SOFCs are procured as a primary power source to bypass grid connection queues and capacity shortfalls.

- This shift is enabled by specific technological maturation, particularly the native 800-Volt DC architecture of Bloom’s systems. This feature allows direct connection to AI server racks, eliminating multiple power conversion steps and reducing total cost of ownership by an estimated 15% to 30%, a critical factor for hyperscale customers.

$5.4 B in Commitments, Bloom Energy and MTAR Capacity Expansion

Multi-billion-dollar financing commitments and direct capital investments are de-risking the massive manufacturing expansion required by Bloom Energy and its supply chain to meet gigawatt-scale demand. These financial structures shift the burden from corporate balance sheets to dedicated project financing vehicles, enabling a more rapid and parallel expansion of both manufacturing and deployment.

Billion-Dollar Commitments De-Risk Bloom’s Expansion

A $5 billion financing partnership with Brookfield Asset Management provides the capital to fund Bloom’s fuel cell deployments for AI data centers, de-risking the required manufacturing expansion.

(Source: Bastion Research – Substack)

- In March 2026, Brookfield Asset Management committed up to $5 billion in a financing partnership specifically to support the deployment of Bloom’s fuel cells for AI-focused data centers. This provides dedicated capital for project execution, allowing Bloom Energy to focus its own resources on manufacturing and R&D.

- To meet its order book, Bloom Energy is investing to double its own annual production capacity from 1 GW to 2 GW by the end of 2026 at its Fremont, California facility. This internal expansion is a direct response to the new baseline of demand established by its large-scale agreements.

- This scale-up is critically dependent on the parallel expansion of key supplier MTAR Technologies in India. MTAR is executing a phased expansion to increase its production of “hot box” assemblies from 8, 000 units to 12, 000 units annually by the end of fiscal year 2026, requiring an initial capital expenditure of approximately ₹40 crore.

- Incentives were further aligned when Oracle was issued a warrant to purchase 3.53 million shares of Bloom Energy stock for approximately $400 million, directly linking the customer’s success to the supplier’s financial performance and providing additional capital for growth.

Table: Bloom Energy Strategic Investments and Expansions

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Oracle | Apr 2026 | Issued a warrant to purchase 3.53 million shares of Bloom Energy stock for ~$400 million. Aligns customer and supplier incentives and provides growth capital. | CNBC |

| Brookfield Asset Management | Mar 2026 | Up to $5 billion financing partnership to fund the deployment of Bloom Energy’s fuel cells at AI-focused data centers, de-risking project execution. | Yahoo Finance |

| Bloom Energy Factory Expansion | Feb 2026 | Internal investment to double annual manufacturing capacity from 1 GW to 2 GW by the end of 2026 at its Fremont, CA, facility to meet its multi-gigawatt pipeline. | Investor’s Business Daily |

| MTAR Technologies Capacity Expansion | Feb 2026 | Phased investment to increase “hot box” production capacity from 8, 000 to 12, 000 units/year by end-FY 26, with a capex of ₹40 crore for the first phase. | Value Pickr Forum |

Bloom Energy 3 Major Agreements, from Oracle to AEP (2025-2026)

Bloom Energy’s 2026 market strategy is built upon a triad of integrated partnerships that connect a hyperscale customer, a dedicated project financier, and a critical component supplier. This structure creates a synchronized ecosystem designed to support rapid, large-scale deployment while mitigating financial and supply chain risks.

- The cornerstone is the customer partnership with Oracle, which signed a master services agreement in April 2026 for up to 2.8 GW of SOFC systems. With 1.2 GW already contracted, this single agreement provides the demand signal and revenue visibility needed to justify a massive manufacturing ramp-up.

- The financing partnership with Brookfield provides up to $5 billion in project capital. This allows deployments for customers like Oracle to be financed off Bloom Energy’s balance sheet, preserving corporate capital for factory expansion and research.

- The strategic supplier partnership with India-based MTAR Technologies is the operational linchpin. As the sole supplier of critical “hot box” assemblies, MTAR’s ability to scale its production in lockstep with Bloom Energy’s order book is essential for meeting delivery timelines.

- Validation from the utility sector comes via a January 2026 agreement with American Electric Power to supply up to 1 GW of SOFCs, valued at approximately $2.65 billion, to serve large data center customers in its territory.

Table: Bloom Energy Key Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Oracle | Apr 2026 | Master services agreement for up to 2.8 GW of SOFC systems to power AI data centers, with an initial 1.2 GW contracted. Provides baseline demand for manufacturing scale-up. | Reuters |

| Brookfield Asset Management | Mar 2026 | Financing partnership for up to $5 billion to fund fuel cell deployments at AI data centers. De-risks the capital-intensive deployment phase. | Yahoo Finance |

| MTAR Technologies | Ongoing | Decade-long strategic supplier relationship. MTAR is the sole supplier of “hot box” assemblies, with 55-65% of its revenue derived from Bloom Energy. | Business Standard |

| American Electric Power | Jan 2026 | Supply agreement for up to 1 GW of SOFCs, valued at ~$2.65 billion. Validates the technology for utility-scale deployment to serve data center customers. | Fuel Cells Works |

US and India, Bloom Energy and MTAR Manufacturing Nexus

The manufacturing scale-up for data center fuel cells is a cross-continental effort, with final assembly and capacity expansion centered in the United States and critical high-precision component manufacturing concentrated in India. This geographic specialization reflects a strategy to leverage regional expertise while keeping final production close to the primary end-market.

Supplier MTAR Is a High-Tech Manufacturing Specialist

MTAR Technologies’ experience supplying critical components to the nuclear, space, and defense sectors validates its role as a high-precision manufacturing partner for AI data centers.

(Source: Bastion Research – Substack)

Bloom Energy Is Key Partner for Supplier MTAR

The strategic partnership with Bloom Energy is critical to supplier MTAR Technologies, as the fuel cell segment now accounts for over 60% of MTAR’s revenue.

(Source: Bastion Research – Substack)

- The United States, specifically Bloom Energy’s facility in Fremont, California, serves as the hub for final assembly, integration, and R&D. The company’s decision to double its capacity to 2 GW at this site solidifies its role as the demand-side manufacturing center, located in close proximity to its key data center customers in Silicon Valley and across the country.

- India has become the indispensable supply-side partner through MTAR Technologies. MTAR’s expertise in precision engineering, originally developed for the nuclear and aerospace sectors, is now being applied to mass-produce the complex “hot box” assemblies for Bloom Energy. The ramp-up to 12, 000 units positions India as a linchpin in the global SOFC supply chain.

- While the manufacturing axis is firmly US-India, deployment remains global. The 80 MW fuel cell project with SK Eternix in Chilgok, South Korea, expected to be the world’s largest upon completion, demonstrates that while manufacturing is concentrated, the market for large-scale SOFC projects extends to major technology and industrial hubs in Asia.

SOFC Technology Maturity, Bloom Energy Commercial Validation at Scale

In 2026, Solid Oxide Fuel Cell (SOFC) technology, as deployed by Bloom Energy, has crossed the threshold from a commercially proven but niche technology to a mature, industrially scalable solution for primary power generation. The transition is marked by multi-gigawatt orders from sophisticated buyers who now view the technology as a reliable and economically viable alternative to traditional utility infrastructure for their most critical operations.

- From 2021 to 2024, SOFC maturity was demonstrated through high-reliability deployments for customers with a low tolerance for downtime, such as financial institutions and colocation data centers. However, these projects were measured in megawatts, not gigawatts, and the technology was primarily valued for its resiliency as a backup or supplementary source.

- The period from 2025 to today has provided definitive validation of SOFCs as a primary, baseload power source. The scale of the Oracle (2.8 GW) and AEP (1 GW) agreements confirms that large energy users now consider the technology mature enough to power their core business operations at a scale that directly displaces the need for new utility grid build-outs.

- This maturity is reinforced by the technology’s inherent fuel flexibility. Bloom Energy’s ability to offer a system that operates on natural gas today but is “hydrogen-ready” for a future transition provides a de-risked pathway for customers to meet both immediate power needs and long-term decarbonization goals.

- The integration of efficient carbon capture with SOFCs, which produce a high-purity CO 2 exhaust stream, further solidifies the technology’s status. It is not just a power generation tool but a platform for a broader clean energy transition, making it a mature solution for the current and future energy environment.

Bloom Energy SWOT Analysis for 2026 Manufacturing Ramp-Up

Bloom Energy’s primary strength in 2026 lies in its validated technology and a massive, de-risked order book, which provides clear revenue visibility. However, this is counterbalanced by significant execution risk centered on the immense challenge of simultaneously scaling its own manufacturing and its critical international supply chain.

Supplier Profitability Highlights Potential Supply Chain Risk

A key weakness in Bloom’s expansion is supply chain risk, underscored by the volatile profitability and declining margins of its critical Indian component supplier, MTAR Technologies.

(Source: Karan’s Substack)

- The company’s core strength is its market position, secured by multi-gigawatt orders and strong financing partners, which has shifted from a theoretical opportunity to a tangible $20 billion backlog.

- Its primary weakness is its operational dependency on a single key supplier, MTAR Technologies, for a critical component, creating a potential bottleneck if MTAR fails to execute its own rapid expansion.

- The opportunity remains the vast and growing power deficit in the AI data center market, which far exceeds even Bloom Energy’s current pipeline and presents a long-term growth runway.

- The main threat is execution failure. Any significant delays in the manufacturing ramp-up or project deployment could damage credibility and provide an opening for competitors like Fuel Cell Energy or alternative on-site power solutions.

Table: SWOT Analysis for Bloom Energy’s 2026 Manufacturing Scale-Up

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Proven SOFC technology with high efficiency and reliability in niche, MW-scale deployments. Established supplier relationship with MTAR. | Massive $20 billion backlog provides revenue visibility. $5 billion financing partnership with Brookfield. Validated as primary power for AI. | The market has validated the technology at a multi-gigawatt scale, transforming a technical strength into a dominant commercial position. |

| Weaknesses | High product cost. Limited market validation at utility scale. Manufacturing capacity constrained to sub-GW annual output. | Extreme operational dependency on MTAR’s ability to scale. High capital intensity required for factory expansions. | The scale-up transforms a manufacturing constraint into a critical execution risk. The dependency on MTAR is now a strategic-level concern. |

| Opportunities | Growing data center power demand. Potential for hydrogen and carbon capture applications. | Explosive, grid-breaking power demand from AI. Hyperscalers actively seeking non-grid power solutions. | The data center power “problem” has become an acute, immediate crisis for AI, turning a general opportunity into an urgent, addressable market. |

| Threats | Competition from other fuel cell technologies (PEM, MCFC) and traditional backup generators. Policy uncertainty. | Execution risk in hitting manufacturing and deployment targets. Supply chain disruptions. Competitors like Fuel Cell Energy also targeting data centers. | The primary threat has shifted from market competition to internal execution failure. Failure to deliver on promises is now the biggest risk. |

2 GW by 2026, Bloom Energy’s Critical Execution Test

The most critical factor for Bloom Energy through 2026 is its ability to successfully execute the dual manufacturing ramp-up at its Fremont facility and at MTAR Technologies in India. This operational challenge will determine whether the company can convert its historic order book into market leadership.

- If Bloom Energy and MTAR successfully hit their respective capacity targets of 2 GW and 12, 000 units by the end of 2026, watch for the formal conversion of the remaining 1.6 GW from the Oracle master agreement into firm, contracted orders. This would signal confidence in the newly scaled manufacturing system.

- The first project announcements under the $5 billion Brookfield financing partnership are another key milestone. If these emerge in late 2026 or early 2027, it will confirm that the financial and operational pieces are working in concert to accelerate deployment.

- Conversely, if there are signs of delay, such as downward revisions in quarterly production guidance from Bloom Energy or reports of missed targets from MTAR, this could signal significant execution challenges. Such a scenario would create an opportunity for competitors and alternative technologies to capture a share of the urgent data center power market.

The questions your competitors are already asking

This report covers one angle of the fuel cell manufacturing ramp required to meet gigawatt-scale data center demand. The questions that matter most depend on your work.

- What is actually happening with the Bloom Energy 2.8 GW Oracle deployment and the broader multi-gigawatt pipeline?

- Is MTAR’s supply chain ramp on track to support Bloom Energy’s production targets for 2026?

- Which data center operators, besides Oracle, are adopting on-site fuel cells as a primary power solution?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.