Bloom Energy SOFC Deals, 2.8 GW Oracle Agreement, $2.65 B AEP Pact, and 11 Data Center Contracts (2021-2026)

Data Center Adoption, Fuel Cell Projects Bypass Grid Constraints

Hyperscale data center operators are now deploying fuel cells as a primary power source to circumvent grid interconnection delays that can last from five to ten years, representing a strategic pivot from their historical use as a backup power system. This move is driven by the urgent need to power a new generation of AI infrastructure, where speed to market is the primary economic driver, not the marginal cost of electricity.

- Between 2021 and 2024, fuel cell applications in the data center sector were characterized by smaller-scale pilots and backup power installations. The significant shift in 2026 is marked by multi-gigawatt, baseload power agreements, exemplified by an unprecedented $7.65 billion in contracts secured in a 90-day period.

- The core value proposition has changed from redundancy to speed. A fuel cell installation can be deployed in a fraction of the time required for new high-voltage transmission lines, allowing AI data centers to become operational years ahead of schedule.

- This adoption is an execution strategy driven by necessity. The voracious power demand of AI GPU clusters has created a physical constraint that the existing grid infrastructure cannot meet on the aggressive timelines required by technology companies.

Investors Target Data Center Power Ecosystem

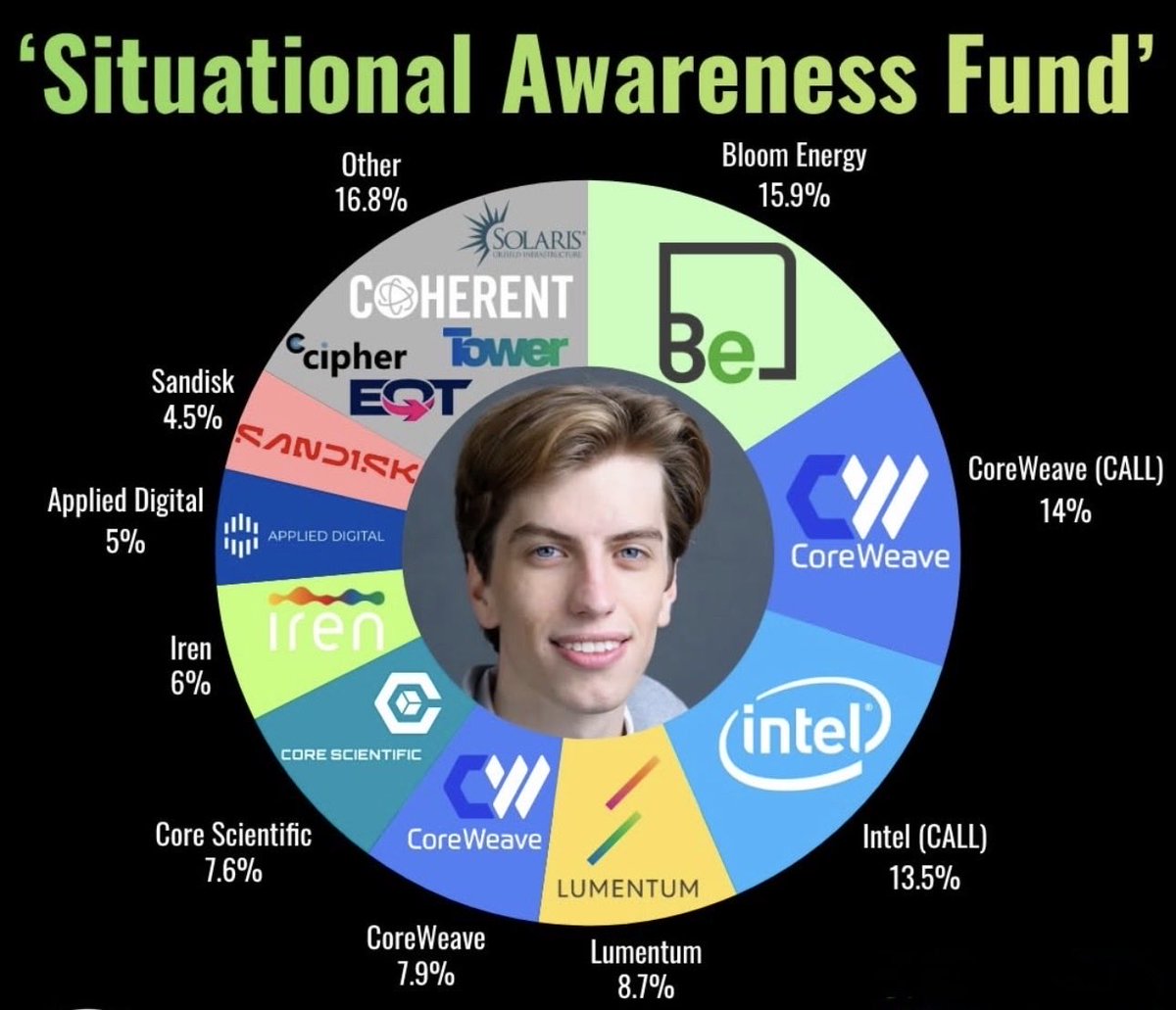

This chart shows an investment fund portfolio that validates the adoption trend by allocating capital to fuel cell maker Bloom Energy alongside key data center and AI infrastructure players.

(Source: Twitter)

$7.65 B in Agreements, Bloom Energy Data Center Deals Lead Market

The first quarter of 2026 saw a rapid series of multi-billion-dollar offtake agreements, confirming that hyperscale operators are directly funding the manufacturing scale-up of fuel cell producers to secure their own power supply chains. These are not speculative investments but capital expenditures for critical infrastructure, analogous to building the data center itself.

- The agreements are structured as long-term master services agreements (MSAs) and power purchase agreements (PPAs), providing fuel cell manufacturers with a de-risked order book that underpins manufacturing expansion. Bloom Energy‘s total backlog surged to approximately $20 billion following these deals.

- These large-scale commitments from blue-chip technology companies serve as a major validation point for the fuel cell industry, unlocking access to lower-cost capital and enabling the capacity expansions needed to meet demand.

- This financial structure shifts the role of the fuel cell provider from a simple equipment vendor to a strategic partner in enabling the core business growth of the world’s largest technology companies.

Table: Major Fuel Cell Investments and Commercial Agreements (2026)

| Company / Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bloom Energy / Oracle | Apr 2026 | Expanded master services agreement for Oracle to procure up to 2.8 GW of fuel cell capacity to power its global AI and cloud data centers. This is a framework agreement to secure long-term power. | Barron’s |

| Bloom Energy / American Electric Power (AEP) | Jan 2026 | An AEP subsidiary exercised an option to purchase approximately $2.65 billion worth of Bloom Energy‘s SOFCs, totaling 900 MW, to supply power to a data center campus in Cheyenne, Wyoming. | Yahoo Finance |

| Fuel Cell Energy / SDCL | Jan 2026 | Strategic collaboration to explore the development and financing of up to 450 MW of on-site fuel cell systems for data centers globally, signaling a move to capture the same market segment. | Fuel Cell Energy, Inc. |

| Ballard Power Systems / New Flyer | Mar 2026 | A commercial agreement for Ballard to supply 50 MW of fuel cell engines to power New Flyer‘s hydrogen buses, representing the largest single order for bus engines for the company. | Ballard Power Systems |

Oracle and AEP Partnerships, Bloom Energy Secures Gigawatt-Scale Pacts

The nature of industry partnerships has matured from exploratory pilots to binding, multi-gigawatt strategic alliances, indicating deep conviction from technology giants that on-site power is a mission-critical infrastructure component. The deal structures provide long-term revenue visibility and de-risk the massive capital investment required for manufacturing expansion.

- The Bloom Energy–Oracle master services agreement for up to 2.8 GW is a clear execution strategy. It provides Oracle with a framework to secure power capacity at speed across its global operations, creating a competitive advantage in deploying AI services.

- The $2.65 billion AEP deal for a 900 MW Wyoming data center is a 20-year power purchase agreement, demonstrating the bankability of fuel cells for project financing and long-term infrastructure planning.

- This trend toward large-scale stationary power contracts contrasts with the mobility sector, where progress is marked by strategic consolidation. For example, Toyota aims to join the cellcentric joint venture with Volvo Group and Daimler Truck to standardize fuel cells for heavy-duty trucking.

- In a sign of strategic realignment in the automotive sector, Honda and General Motors announced the dissolution of their fuel cell manufacturing joint venture in 2026, opting to pursue independent development paths amid slow passenger vehicle adoption.

US Market Focus, Data Center Power Demand Drives Regional Activity

The United States has emerged as the unequivocal epicenter for large-scale fuel cell deployment, a direct result of the concentration of AI data center construction that is outpacing the capacity of regional electrical grids. While policy provides tailwinds, this geographic focus is primarily a market-based response to a critical infrastructure bottleneck.

- Major projects announced in 2026, such as the 900 MW installation in Cheyenne, Wyoming, are located in the U.S. to serve the power needs of hyperscale computing campuses.

- This contrasts with the period from 2021 to 2024, when market activity was more geographically dispersed and often focused on policy-driven mobility projects in Europe and Asia, such as hydrogen bus deployments or port decarbonization.

- While Europe continues to see strategic activity, such as the Centrica and Ceres partnership for on-site power and the development of hydrogen production by firms like AFC Energy, the sheer scale of capital being committed to fuel cells for U.S. data centers in 2026 marks a decisive geographic shift in market gravity.

SOFC Commercial Scale, Bloom Energy Technology Reaches TRL 9

The recent surge in gigawatt-scale contracts is enabled by the maturation of Solid Oxide Fuel Cell (SOFC) technology to a high Technology Readiness Level (TRL 8-9). This makes it a bankable, commercially proven solution capable of supporting mission-critical, baseload power applications for the world’s most demanding customers.

- The dominant technology in the major 2026 data center deals is SOFC, prized for its high electrical efficiency and fuel flexibility. Current deployments primarily use natural gas, offering significant emissions reductions over diesel generators, with a future pathway to operate on green hydrogen.

- This marks a shift from the 2021-2024 period, when much of the public focus was on Proton Exchange Membrane (PEM) fuel cells, largely for mobility applications which require different performance characteristics like rapid start-up times.

- The selection of natural gas-fed SOFCs for these immediate, large-scale deployments underscores that the primary driver is solving the immediate power and timeline problem, with the transition to 100% hydrogen as a future-proofing feature rather than a day-one requirement.

SWOT Analysis, Fuel Cell Contracts and Market Dynamics

The fuel cell market’s core strength is its unique ability to solve the immediate power and deployment timeline crisis for AI data centers, creating a massive new demand driver. However, this opportunity is paired with significant execution risks related to manufacturing scale-up and a dependency on volatile natural gas prices in the near term.

Table: SWOT Analysis for Data Center Fuel Cell Market

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High reliability; lower emissions than diesel backup generators; modularity. | Proven TRL 8-9 for SOFC; established manufacturing processes. | Validated: The 2.8 GW Oracle and 900 MW AEP deals in 2026 confirm that speed-to-deployment is now the paramount strength, valued in the billions by hyperscalers. |

| Weaknesses | Higher Levelized Cost of Energy (LCOE) than grid power; reliant on natural gas; limited manufacturing scale. | Customer concentration in niche markets; perception as a transitional technology due to CO 2 emissions. | Unchanged: The dependency on natural gas remains the key weakness. The 2026 deals amplify this exposure, tying project economics directly to commodity price volatility. Manufacturing scale-up is now the central execution risk. |

| Opportunities | Growing data center power demand; corporate ESG goals; potential to use hydrogen. | Grid-connection queues grow to 5+ years; AI power demand grows exponentially. | Validated & Accelerated: The AI power crunch has turned the theoretical opportunity into a $7.65 billion near-term market. The opportunity is no longer future-looking; it is the primary driver of execution today. |

| Threats | Competition from other clean-power technologies (e.g., batteries, renewables); policy uncertainty. | Sustained low natural gas prices needed for favorable economics; risk of technology obsolescence from SMRs or geothermal. | New Threat Emerged: Extreme customer concentration. A significant portion of the industry’s backlog is now tied to a few large tech companies. A slowdown in AI spending by one of these customers poses a systemic risk. |

Forward Outlook, Hydrogen Supply and Customer Diversification

If fuel cell providers can secure large-scale green hydrogen offtake agreements for these data center installations, they will validate the long-term decarbonization pathway and secure their position as a permanent clean energy solution. Without this, they risk being categorized as a transitional technology that will eventually be replaced.

- The most critical forward-looking catalyst is the announcement of a large-scale green hydrogen supply agreement for a major data center fuel cell project. This would de-risk the ESG profile and prove the viability of the “hydrogen-ready” claims.

- Watch for similar multi-hundred-megawatt announcements from competitors like Fuel Cell Energy or the entry of new players. This would confirm a broad market shift rather than a trend dependent on a single supplier’s success.

- Successful execution on manufacturing expansion is critical. Investors will closely monitor quarterly earnings from Bloom Energy to verify progress on its planned capacity ramp-up to 2 GW and its ability to maintain margins while delivering on its massive backlog.

- Another key signal will be the diversification of the customer base. Announcements of large-scale fuel cell deployments for other power-intensive industries, such as advanced manufacturing, would indicate that the market is expanding beyond the AI data center niche.

The questions your competitors are already asking

This report covers one angle of the commercial shift to fuel cells as primary power for data centers. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the fuel cell market for data center primary power?

- What is the outlook for fuel cell deployment in AI data centers by 2030?

- Which hyperscale operators besides Oracle are adopting on-site fuel cells as a primary power source?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.