DAC Aviation Offtakes, 400, 000 Tonne Airbus Deal, 2.9 M Tonne Demand, and the $180/ton 45 Q Credit (2021 to 2026)

DAC Commercial Scale, Climeworks and 1 Point Five lead Aviation Offtakes

The Direct Air Capture industry is shifting from a speculative technology to a bankable asset class, a transition driven by large-scale, long-term offtake agreements from the aviation sector. This commercial evolution converts future carbon removal into a financeable instrument, underpinning the project economics required to build megaton-scale facilities. The primary risk is evolving from technological feasibility to execution, cost control, and policy stability.

- Between 2021 and 2024, the market was defined by smaller, technology-led pre-purchase agreements from companies like Microsoft, which established the initial price signals for high-durability credits. The 2022 letter of intent from an Airbus-led airline consortium to pre-purchase 400, 000 metric tons from 1 Point Five was a foundational signal of aviation’s strategic interest, even as total operational DAC capacity remained below 0.01 million tonnes annually.

- From 2025 to today, this model has matured with direct airline offtake agreements, including Lufthansa Group’s deal with Deep Sky in May 2026. Corporate-led demand for DAC credits reached approximately 2.9 million tonnes, creating a tangible demand signal that enables developers to secure project financing.

- The risk profile has shifted from proving the technology to proving commercial scalability and bankability. The late 2025 political uncertainty surrounding the U.S. Department of Energy’s DAC Hubs, which threatened billions in funding for projects involving Climeworks and Heirloom, highlights the sector’s acute exposure to policy risk.

- While aviation is a key anchor for permanent removal credits, the revenue model is diversifying. Other industrial and energy companies like Schneider Electric and ENGIE are also signing offtake agreements, creating a broader base of demand that validates the technology’s role across multiple decarbonization strategies.

Aviation’s 2050 Energy Demand Projection

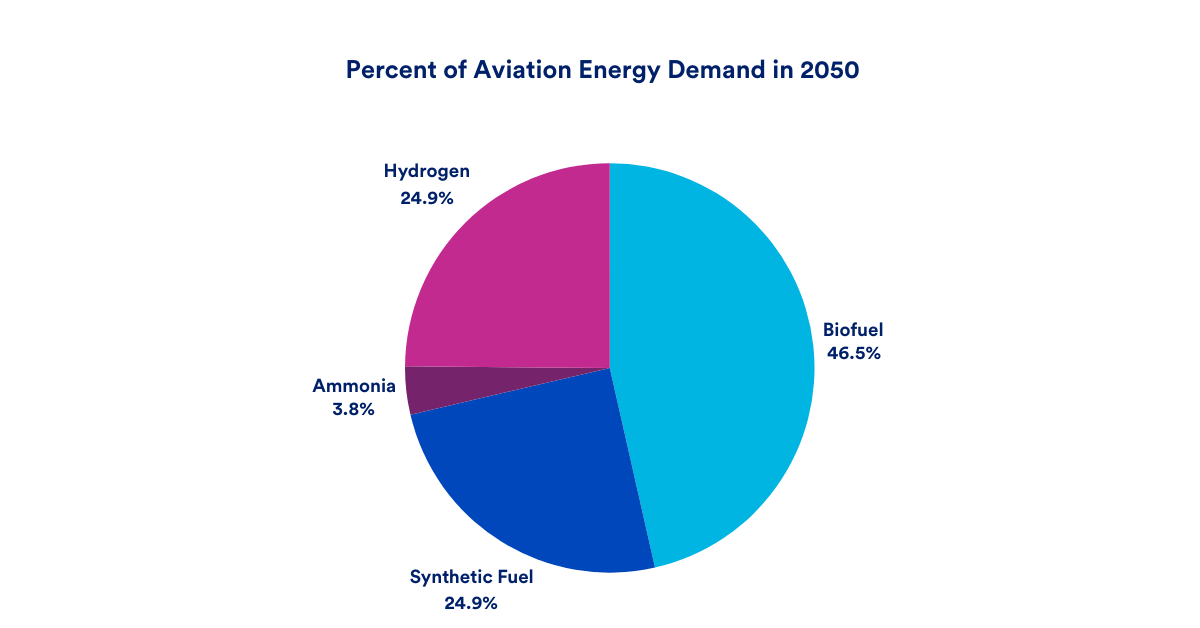

This chart provides essential context for the section’s focus on aviation offtakes by illustrating the massive future energy demand from the sector. It underscores why airlines are actively seeking solutions like DAC-derived fuels and carbon removals to meet their net-zero commitments, positioning Climeworks and 1 Point Five as key partners.

(Source: Clean Air Task Force)

Investment Volatility, 1 Point Five and the DOE’s DAC Hub Funding Shifts

Direct Air Capture investment is characterized by a dual reliance on large, policy-backed funding mechanisms and concentrated private capital, creating a volatile but ultimately upward funding trajectory. The sector’s financial health is directly tied to the stability of public incentives, which act as the primary de-risking agent for attracting the large-scale project finance needed to move from pilot to commercial scale.

- Venture and growth investment in carbon capture and removal showed significant volatility, peaking at over $2.2 billion in 2022 before contracting to less than $1 billion by 2025. This indicates a market maturation, shifting from early-stage venture funding to a more demanding project finance environment where bankable offtake agreements are essential.

- The U.S. Department of Energy’s DAC Hub program represents the most significant public investment driver. The announcement in late 2025 to potentially cancel funding for several hubs exposed the sector’s vulnerability to political shifts and created significant uncertainty for major players like Climeworks, Heirloom, and 1 Point Five.

- The subsequent preservation of federal funding for key U.S. DAC and hydrogen hubs in April 2026 provided critical stability and reaffirmed the technology’s strategic importance. However, the event underscored that policy risk remains a primary concern for investors and developers.

- The U.S. Section 45 Q tax credit, enhanced by the Inflation Reduction Act to $180 per ton for permanent storage, functions as a government-backed revenue floor. This incentive is the critical component that makes U.S.-based DAC projects bankable, directly enabling the offtake agreement model.

CO2 Removal Investment and Sales Surge in 2024

The chart’s depiction of a surge in investment provides a direct visual backdrop for the section’s discussion on investment volatility and funding shifts. It highlights the high-stakes environment in which players like 1 Point Five operate and frames the significance of major public funding injections like the DOE’s DAC Hub program.

(Source: Carbon Removal Updates – Substack)

Table: Key DAC Investment and Policy Events

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| DOE DAC Hubs (U.S.) | Apr 2026 | The preservation of federal funding for certain hubs provided crucial support and stability for major projects following a period of political uncertainty, reaffirming the strategic importance of DAC infrastructure. | Carbon Herald |

| DOE DAC Hubs (Texas, Louisiana) | Oct 2025 | A proposed cancellation of funding jeopardized billions in planned investment for projects involving leading developers Climeworks and Heirloom, highlighting the sector’s significant policy risk. | Heatmap News |

| Carbon Removal VC Funding | 2022 vs. 2025 | Venture and growth investments fell from a peak of over $2.2 billion across 90+ deals in 2022 to under $1 billion from fewer than 40 deals by 2025, showing a market shift from early-stage funding to a focus on project finance. | Cleantech Group |

Climeworks 2 Key Offtake Agreements for DAC (2025 to 2026)

Long-term offtake agreements from diverse, creditworthy buyers are the primary commercial mechanism transforming future carbon removal into a present, bankable asset. These contracts provide the revenue certainty required for developers to secure financing for capital-intensive DAC facilities, effectively bridging the gap between high upfront costs and future value.

- The aviation industry has solidified its role as a key anchor customer for DAC credits. The Lufthansa Group’s agreement with Deep Sky in May 2026 is a recent example of this trend, building on the precedent set by the 2022 Letter of Intent from an Airbus-led consortium for 1 Point Five’s credits.

- Demand is diversifying beyond aviation, with technology and industrial companies providing critical early adoption. Schneider Electric’s September 2025 agreement with Climeworks to remove 31, 000 tons of CO₂ demonstrates the broadening appeal of high-durability removals.

- Partnerships are evolving beyond simple credit transactions to include deeper strategic alignment. The April 2026 deal between ENGIE and Deep Sky combines credit procurement with joint research and market development, signaling a commitment to building the broader carbon removal ecosystem.

- The scale and duration of these agreements are increasing, providing greater financial certainty. Microsoft’s landmark 2023 agreement to purchase up to 315, 000 metric tons of CO₂ removal from Heirloom set a benchmark for large-volume, multi-year deals that the market is now emulating.

Carbon Credit Market Share Breakdown for 2025

With the section focusing on Climeworks’ offtake agreements for 2025-2026, this chart offers a perfect market snapshot. It contextualizes the agreements by illustrating the competitive landscape of the carbon credit market in 2025, which is the primary mechanism for such offtakes.

(Source: Global Market Insights)

Table: Key DAC Offtake and Partnership Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Lufthansa Group / Deep Sky | May 2026 | Multi-year offtake agreement for high-quality direct air capture (DAC) carbon removal credits, securing a key aviation partner for the Canadian DAC hub developer. | PR Newswire |

| ENGIE / Deep Sky | Apr 2026 | A partnership combining carbon credit procurement, joint research, and market development efforts to strengthen the durable carbon removal market. | Newswire Canada |

| Schneider Electric / Climeworks | Sep 2025 | Agreement for Climeworks to remove 31, 000 tons of CO₂ on behalf of Schneider Electric, demonstrating demand from the industrial technology sector for high-durability solutions. | Schneider Electric |

| Airbus & Airline Consortium / 1 Point Five | Jul 2022 | A foundational Letter of Intent to negotiate the pre-purchase of 400, 000 metric tons of carbon removal credits, signaling the aviation sector’s early strategic interest in DAC. | Skies Magazine |

US Policy Focus, 1 Point Five and the 45 Q Tax Credit

The United States dominates global Direct Air Capture project development and investment due to the unparalleled financial incentives provided by the Inflation Reduction Act’s Section 45 Q tax credit. This policy has effectively concentrated large-scale commercial activity within the U.S., making it the most commercially attractive region for building and operating DAC facilities.

- In the 2021-2024 period, DAC development was more geographically dispersed, with pioneers like Climeworks establishing initial projects in Europe, such as its Orca plant in Iceland. The U.S. had active projects, but its policy incentives were not yet the primary global driver.

- From 2025 onward, the U.S. has become the clear epicenter for large-scale DAC deployment. The enhanced 45 Q tax credit, offering $180 per ton for permanently stored CO₂, creates a decisive economic advantage. Major projects, such as 1 Point Five’s Stratos facility in Texas, are a direct result of this policy.

- The DOE’s DAC Hub program further concentrates activity in the U.S. Gulf Coast, targeting locations in Texas and Louisiana that offer advantageous geological storage formations and existing energy infrastructure.

- While other regions remain active, they lack a comparable financial pull. Canada is fostering a growing hub with companies like Deep Sky, and Europe continues to host important research and pilot facilities. However, large-scale commercial deployments are overwhelmingly targeting the robust economic case presented by U.S. policy.

Government Policy and Corporate Action Drive DAC Market

This chart’s headline perfectly mirrors the section’s theme. The section discusses the specific 45Q tax credit (Government Policy) and 1 Point Five (Corporate Action), and the chart provides the high-level thesis that these two forces are the primary drivers of the DAC market.

(Source: Verified Market Research)

$600/ton Costs, Climeworks and the DAC Scale-up Challenge

While technologically proven at a pilot scale, Direct Air Capture’s commercial maturity is constrained by high operational and capital costs. The industry’s viability and ability to attract investment depend entirely on executing a steep and credible cost-reduction curve, transitioning the technology from a subsidized niche to a competitive market solution.

- Between 2021 and 2024, the primary technical focus was on validating different technology pathways, such as solid sorbent and liquid solvent systems, and achieving operational stability for first-of-a-kind plants. During this phase, costs were frequently cited in the $600 to $1, 000 per ton range.

- From 2025 to today, the technology has matured to the point where developers are planning megaton-scale facilities. However, costs remain the primary commercial barrier, with 2026 estimates still spanning a wide range of $250 to $1, 000 per ton depending on the technology and project maturity.

- The industry’s business model is predicated on aggressive cost-reduction targets. Climeworks, a market leader, announced plans to halve its costs by 2030. The credibility of these projected cost-down curves is a critical factor for securing long-term offtake agreements and project financing.

- The market for delivered credits is highly concentrated. As of late 2025, just three companies, Climeworks, 1 Point Five, and Heirloom, accounted for 80% of all DAC credits sold. This indicates that very few developers have reached a level of technological maturity sufficient for large-scale commercial contracts, posing a systemic supply-side risk.

DAC Costs Projected to Fall with Deployment Scale

This chart directly visualizes the core concept of the section. By showing the relationship between deployment scale and cost reduction, it explains the ‘DAC Scale-up Challenge’ and illustrates the pathway from the current $600/ton cost towards commercial viability.

(Source: Clean Air Task Force)

SWOT Analysis, Climeworks and DAC Market Dependencies

The Direct Air Capture industry’s primary strength is its ability to provide high-durability, verifiable carbon removals, an asset increasingly valued by corporate offtakers. This strength is counterbalanced by significant weaknesses in cost and scale, with opportunities in policy and new markets threatened by execution risk and potential shifts in corporate climate ambition.

- The core value proposition of DAC, its permanence, has been validated through premium pricing on the voluntary market and large-scale offtake agreements from sectors like aviation.

- The industry’s reliance on a few key technologies and developers, coupled with persistent high costs and uncertain cost-down trajectories, creates significant commercial and operational fragility.

- Unprecedented policy support in the U.S. (45 Q) and growing demand from hard-to-abate sectors represent the most powerful growth drivers, creating a clear opportunity for first-movers.

- The sector remains highly vulnerable to shifts in political priorities, as seen in the 2025 funding uncertainty, as well as the risk of failing to deliver complex, first-of-a-kind industrial projects on time and on budget.

Carbon Utilisation Shown as Revenue Stabilization Strategy

This chart provides a specific example relevant to a SWOT analysis. By highlighting carbon utilization as a revenue stabilization strategy, it directly addresses the ‘market dependencies’ mentioned in the section title, representing a key opportunity or a way to mitigate threats within the DAC market.

(Source: The Percolator – Substack)

Table: SWOT Analysis for Direct Air Capture Offtake Models

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High durability and verifiability of carbon removal. | The value of permanence was validated by premium-priced offtake agreements from corporate buyers like the Airbus-led consortium and Microsoft. | The theoretical value of permanence was successfully converted into actual, bankable, multi-year offtake contracts from creditworthy counterparties. |

| Weaknesses | Extremely high cost ($600-$1000/ton), low operational scale (kilotons), and high energy intensity. | Costs remain high ($250-$1000/ton), and the market is highly concentrated, with three companies accounting for 80% of credits sold. | The weakness evolved from just high cost to the dual challenge of executing a credible cost-down curve and mitigating the supply-side risk of relying on a few key developers. |

| Opportunities | Growing corporate net-zero pledges and the general prospect of future policy support. | The U.S. Inflation Reduction Act’s $180/ton 45 Q tax credit created a powerful market pull. The aviation sector emerged as a key offtaker with demand for long-term contracts. | The opportunity shifted from a vague concept (“policy could help”) to a specific, potent financial instrument (45 Q) and a defined anchor customer segment (aviation). |

| Threats | Lack of a clear business model and the risk of technology failing to scale beyond pilots. | Policy risk (e.g., the late 2025 DOE Hub funding crisis), project execution risk, and a potential weakening of corporate climate commitments due to economic pressure. | Threats became more tangible, moving from the existential (“will this ever work?”) to the operational (“will this specific project get built on time and on budget?”). |

1 Point Five 2026 Offtake and DAC Project Finance Scenarios

The critical factor for the Direct Air Capture industry in the next 12-24 months is the successful financial close and construction start of the next wave of large-scale plants. This step will serve as the ultimate validation of the aviation offtake model’s bankability and determine the sector’s near-term growth trajectory.

- If this happens: Leading DAC developers like 1 Point Five, Climeworks, and Heirloom successfully leverage their portfolios of offtake agreements to secure non-dilutive project financing for their next major facilities, proving the model works.

- Watch this: The announcement of a final investment decision (FID) for a large-scale DAC plant that explicitly cites aviation offtake agreements as a cornerstone of its financing package. Also, monitor the price, volume, and duration of new offtake deals to gauge the health of market demand.

- These could be happening: Financial institutions begin to standardize terms and develop new products for carbon removal projects, treating offtake agreements as a distinct asset class. More airlines, particularly outside the initial group of first movers, start signing their own offtake deals, broadening the demand base and creating a more liquid market.

DAC Systems Offer Multiple Commercial Revenue Streams

This chart is fundamental to the section’s topic of project finance. Any ‘Project Finance Scenarios’ for a DAC facility would be built upon the various income sources available, which this chart visualizes, making it an essential illustration for the financial discussion.

(Source: NEG8 Carbon)

The questions your competitors are already asking

This report covers one angle of how aviation offtake agreements are underwriting the commercialization of Direct Air Capture. The questions that matter most depend on your work.

- Which DAC developers are gaining or losing ground in the aviation offtake market?

- What is actually happening with the Airbus and 1PointFive 400,000-tonne offtake agreement since it was announced?

- What is the outlook for meeting the 2.9 million tonne corporate demand for DAC credits?

- Which airlines, beyond Lufthansa Group, are actively pursuing multi-year DAC offtake agreements?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.