DAC Offtake Agreements, $40 M Deep Sky Grant, Lufthansa Deal, and 5 Corporate Pacts Validating Project Bankability (2021-2026)

DAC Commercial Scale, Deep Sky Offtakes Signal Shift from Pilot to Bankable Projects

Corporate offtake agreements for Direct Air Capture (DAC) credits are shifting the market from venture-funded research pilots to bankable infrastructure projects, mirroring the corporate Power Purchase Agreement (PPA) model that successfully scaled the renewable energy sector. This evolution from exploration to execution marks the most significant strategic development in the carbon removal industry, with companies like Deep Sky leveraging these contracts to secure project financing.

- Between 2021 and 2024, the market was characterized by smaller, often exploratory, carbon credit purchases as companies tested the waters. The period from 2025 to 2026 saw a fundamental shift to binding, multi-year offtake agreements from major corporations, including Lufthansa Group, TD Bank Group, and ENGIE, all committing to purchase future credits from Deep Sky.

- These long-term agreements provide the revenue certainty required to de-risk investments and unlock the massive project financing needed for capital-intensive DAC facilities. This was a critical barrier to scale prior to 2025, and its resolution is a primary catalyst for current growth.

- The strategy for buyers has also matured. For airlines like Lufthansa, these deals represent an offensive move to secure a long-term supply of high-permanence removals in an anticipated supply-constrained market, moving beyond short-term ESG goals to active, strategic procurement.

- This commercial model allows project developers to transition from the venture-backed R&D phase toward becoming bankable infrastructure developers. Securing a blue-chip offtaker provides the commercial validation needed to attract project-level debt and equity for construction.

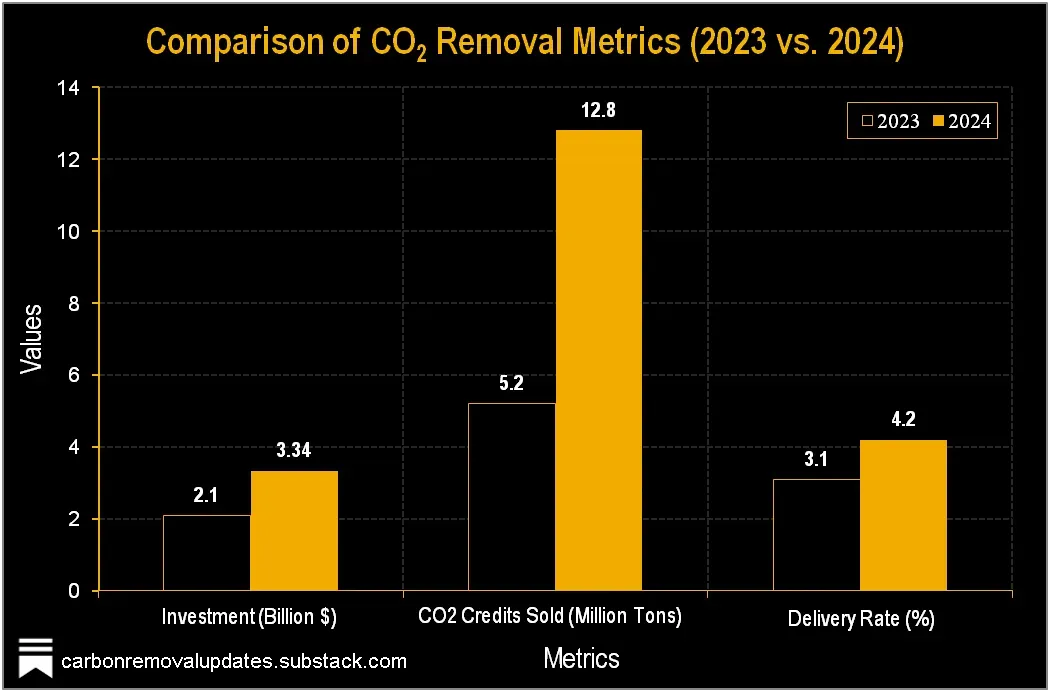

Carbon Removal Metrics Surge in 2024

The chart’s depiction of a surge in carbon removal metrics provides direct quantitative evidence for the section’s assertion that the DAC industry is shifting from pilot programs to bankable, commercial-scale projects.

(Source: Carbon Removal Updates – Substack)

Deep Sky $40 M Grant, Breakthrough Energy Signals Investor Confidence in DAC Offtake Model

Major grants and the financial weight of large offtake agreements demonstrate a new phase of investment confidence in the carbon capture sector, predicated on secured future revenue streams rather than purely speculative technology bets. The combination of catalytic philanthropic capital and binding commercial contracts is creating the financial architecture necessary for project deployment.

- Deep Sky’s $40 million grant from Breakthrough Energy Catalyst in December 2024 was a pivotal moment. The grant, a first for a Canadian company and a DAC project from the fund, validated the company’s project developer model before the major offtake agreements were announced in 2026.

- Government policy created the foundational investment landscape. The U.S. Inflation Reduction Act’s enhanced 45 Q tax credit (up to $180 per ton) and the Department of Energy’s $1.2 billion in initial funding for DAC Hubs established the public-sector support structure.

- The series of corporate offtake agreements in 2025 and 2026 function as a powerful investment catalyst. They make DAC projects attractive to traditional infrastructure investors by providing predictable, long-term revenue streams, which are essential for securing non-dilutive project finance.

Table: Key Commercial Agreements Underpinning DAC Investment

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Deep Sky and TD Bank Group | Jun 2026 | A 10-year offtake agreement for over 18, 000 DAC carbon removal credits. The deal provides Deep Sky with a long-term revenue stream and helps TD Bank secure high-quality credits for its decarbonization goals. | Newswire |

| Deep Sky and Lufthansa Group | May 2026 | A multi-year offtake agreement for verified DAC credits. This allows Lufthansa to diversify its climate portfolio beyond Sustainable Aviation Fuel (SAF) and secure a supply of high-permanence removals. | PR Newswire |

| Deep Sky and ENGIE | Apr 2026 | Agreement for ENGIE to procure up to 15, 000 carbon removal credits. This partnership advances Deep Sky’s commercial viability and supports ENGIE’s carbon neutrality objectives. | PR Newswire |

| 1 Point Five and JPMorgan Chase | Jun 2025 | Agreement for 50, 000 metric tons of carbon removal credits. This deal was among the early large-scale commitments that signaled growing corporate demand for DAC solutions. | 1 Point Five |

Aviation Sector Partnerships, Airbus and Lufthansa Lead DAC Credit Offtake Strategy

The aviation industry has emerged as a key anchor customer for the DAC market, with major players like Lufthansa Group and Airbus forming strategic partnerships to secure a future supply of high-permanence carbon removal credits. These alliances are crucial for an industry facing intense pressure to decarbonize its hard-to-abate emissions.

- Before 2025, airline partnerships in the DAC space were more exploratory. A key example was Lufthansa joining Airbus’s carbon removal initiative in December 2023, which was anchored by a larger credit purchase from 1 Point Five.

- By 2026, these collaborations matured into direct, multi-year offtake agreements. This is clearly demonstrated by Lufthansa’s landmark deal with Deep Sky and easy Jet’s commitment to purchase carbon removal credits sourced via Airbus between 2026 and 2029.

- These partnerships are strategic hedges against future Sustainable Aviation Fuel (SAF) scarcity and price volatility. By diversifying their decarbonization portfolios with credible, technology-based solutions like DAC, airlines are building more resilient net-zero pathways.

- The emergence of intermediaries like the carbon credit procurement company Senken, which facilitated the Lufthansa and Deep Sky deal, indicates a maturing market structure with specialized brokers emerging to manage these complex transactions.

CDR Cost-Competitive for Shipping Decarbonization

While focused on shipping, this chart serves as an analogy for the aviation sector discussed in the section. It demonstrates that carbon removal is becoming a viable decarbonization pathway for hard-to-abate transport industries, supporting the rationale for aviation partnerships.

(Source: Marginal Carbon – Substack)

Table: Airline and DAC Partnership Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Lufthansa Group and Deep Sky | May 2026 | Multi-year offtake agreement for high-quality DAC carbon removal credits. The deal is a core part of Lufthansa’s revamped climate strategy to increase its portfolio of permanent carbon removal projects. | Carbon Herald |

| easy Jet and Airbus | May 2026 | Commitment to purchase carbon removal credits between 2026 and 2029. The credits will be sourced through Airbus’s carbon removal initiative, demonstrating a supply chain approach to procurement. | Green Air News |

| Lufthansa Group and Climeworks | Mar 2024 | Lufthansa Group and its subsidiary SWISS signed a carbon removal agreement with DAC pioneer Climeworks, an early move to build a portfolio of high-quality removal solutions. | ESG Today |

| Lufthansa Group joins Airbus Initiative | Dec 2023 | Lufthansa became a member of the Airbus carbon removal program, which is anchored by a 400, 000-tonne credit purchase from 1 Point Five’s DAC technology. | ESG Today |

Canada vs. US Policy, Deep Sky and 1 Point Five Lead Regional DAC Hub Growth

North America has become the undisputed center of gravity for large-scale Direct Air Capture development, with Canada and the United States creating distinct but equally powerful policy environments that are attracting major project investments and driving regional specialization.

- The United States is fostering massive-scale projects driven by the Inflation Reduction Act’s $180/ton 45 Q tax credit and the Department of Energy’s $3.5 billion DAC Hubs program. This policy framework directly supports the development of projects like 1 Point Five’s Stratos facility in Texas, which aims to capture 500, 000 tons per year initially.

- Canada, particularly Quebec, has established itself as a highly attractive jurisdiction for DAC development due to a different set of advantages. The Canadian government offers a supportive investment tax credit of up to 60% for DAC projects, which, when combined with Quebec’s abundant and low-cost hydropower, creates an ideal environment for Deep Sky’s energy-intensive operations.

- This represents a significant geographic shift. Prior to 2024, much of the commercial DAC activity and leadership was associated with Europe, primarily through Climeworks’ pioneering Orca and Mammoth plants in Iceland. The period from 2024 to 2026 has been defined by a decisive pivot towards North American gigaprojects.

Key Players in the Carbon Capture Market

This chart provides the broader competitive landscape for the section, which focuses on specific players like Deep Sky and 1 Point Five. It helps contextualize their role within the overall market discussed.

(Source: CTVC)

$180/Ton Subsidies, DAC Technology Moves from TRL-6 Pilot to TRL-8 Commercial Risk

Direct Air Capture technology is navigating the perilous transition from proven pilot-scale operations (Technology Readiness Level 6-7) to the immense execution risk of first-of-a-kind commercial plants (TRL 8-9). This leap is not guaranteed and is enabled almost entirely by a combination of binding offtake agreements and substantial government policy support.

- The period leading up to 2024 was primarily focused on scientific validation and small-scale deployments to prove that different DAC chemistries, like solid sorbents and liquid solvents used by companies such as Climeworks and Carbon Engineering, were technically viable.

- From 2025 onward, the central challenge has pivoted from technological possibility to commercial execution. The critical question is no longer “can it work?” but rather “can it be built on time, on budget, and operate reliably and economically at a massive scale?”.

- High costs, currently estimated between $400 and $1, 000 per tonne of CO 2 removed, remain the single greatest barrier to widespread adoption. Offtake prices are not public, but their economics are inextricably linked to subsidies like the U.S. 45 Q credit of $180/ton, which bridges a critical portion of this viability gap.

- Deep Sky’s model of building a hub to test and deploy multiple DAC technologies is a deliberate risk-mitigation strategy. It acknowledges that a single winning technology has not yet emerged and that extensive operational learning across different systems is necessary to drive down costs for the entire industry. Other technology providers in this space include Remora, Jeevan Climate Soln, SCW Systems, Sustaera, and Air Capture.

DAC Costs Projected to Decrease With Scale

This chart illustrates the cost-reduction curve that is central to the technology’s path to commercialization. It provides the economic rationale for how subsidies can bridge the viability gap until DAC achieves scale and moves from a TRL-6 pilot to a TRL-8 commercial risk level.

(Source: Climate Money – Substack)

SWOT Analysis, Deep Sky Leverages Offtakes Amidst High DAC Execution Risks

The Direct Air Capture market’s primary strength is the powerful demand signal from corporate buyers seeking high-integrity carbon removals. However, this is balanced by significant threats from high costs and policy dependence, with bankable offtake agreements emerging as the key opportunity to overcome immense execution hurdles.

Table: SWOT Analysis for Direct Air Capture Market (2021-2026)

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong government policy support announced (e.g., U.S. IRA). Growing corporate net-zero pledges creating theoretical demand. | Demand materialized into bankable, multi-year offtake agreements from blue-chip buyers (Lufthansa, TD Bank, JPMorgan Chase). Strong policy support in both U.S. and Canada. | The market validated that corporate demand is real and can be converted into the long-term contracts needed to underpin project finance. |

| Weaknesses | Extremely high theoretical costs ($600-$1, 000/ton) and energy requirements. Lack of commercial-scale operational data. | Proven high capital expenditure for first-of-a-kind plants. Costs remain high, far from the industry’s $100/ton target. Technology is still at TRL 6-7 for most developers. | The financial and technical challenge of scaling was confirmed to be as large as anticipated. The cost curve has not yet started to bend significantly. |

| Opportunities | Opportunity to secure venture capital funding based on technology promise and small-scale pilot results. | Leverage offtake agreements to secure project-level debt and equity. Opportunity to become a technology-agnostic project developer (Deep Sky’s model). | The financing model shifted from speculative venture capital to bankable infrastructure finance, a crucial step for scaling capital-intensive projects. |

| Threats | Technology risk: the possibility that DAC processes would not be viable at scale. Competition from lower-cost but lower-quality offsets. | Execution risk (construction delays, cost overruns). Policy risk (future governments changing subsidies like 45 Q). Market integrity risk (any scandal questioning MRV). | The primary risk shifted from “will the science work?” to “can we build and finance it affordably and will the supporting policies remain stable?”. CCUS strategies from companies like BP and Wacker also compete for investment. |

DAC Bankability Test, Watch Deep Sky’s First Final Investment Decision (FID)

The single most critical signal for the entire Direct Air Capture sector in the next 12 to 18 months will be whether a developer like Deep Sky can successfully translate its portfolio of high-profile offtake agreements into a Final Investment Decision (FID) for its first commercial-scale plant.

- If Deep Sky announces it has secured full project financing for a large-scale facility, it will serve as the ultimate validation of the “offtake-to-bankability” model for DAC. This would likely trigger a wave of similar project developments and financing deals across the industry as it provides a proven playbook for investors and developers.

- Watch for competing airlines and corporate buyers to accelerate their own procurement strategies. A successful FID at Deep Sky will intensify the race to secure a finite supply of high-quality credits, potentially leading to a flurry of new offtake agreements from players like IAG (British Airways) and Air France-KLM.

- Conversely, a significant delay or failure to reach FID would send a chilling signal to the market. It would suggest that even with strong policy support and anchor customers, the current economics are still insufficient to de-risk the massive capital requirements, potentially stalling the industry’s transition from pilot to commercial scale.

The questions your competitors are already asking

This report covers one angle of how corporate offtake agreements are making Direct Air Capture projects bankable. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the market for bankable Direct Air Capture projects?

- What is the outlook for DAC offtake agreements in the aviation sector?

- Deep Sky’s partnership with Lufthansa. Is this offtake agreement progressing from a corporate pact to a financed project?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.