Grid Optimization Software, 40% Capacity Gains, 175 GW Virtual Transmission & 300+ Utility Deployments (2021-2026)

The explosive growth of Artificial Intelligence (AI) has created an unprecedented surge in electricity demand, primarily driven by the power consumption of hyperscale data centers. This demand is straining aging electrical grids globally, creating a critical bottleneck for technological advancement. While building new transmission lines is a long-term solution, it is a process that takes over a decade and faces significant regulatory and logistical hurdles. In response, AI-powered software solutions have emerged as a pivotal, near-term strategy to unlock latent capacity within existing infrastructure, offering a faster, more cost-effective way to manage the load growth from the expanding AI infrastructure.

Industry Adoption of Grid Optimization Software: From Pilots to Systemic Reliance

The adoption of AI-powered grid optimization software has accelerated from niche pilot projects to a strategic imperative, driven by the acute power demands of the AI sector. Prior to 2025, technologies like Dynamic Line Rating (DLR) and Virtual Power Plants (VPPs) were viewed as innovative but secondary tools for grid management. The period from 2025 onward marks a definitive shift, where these software solutions are now recognized as the primary near-term method to unlock capacity and connect new data center loads without waiting a decade for new physical transmission lines.

- In the 2021-2024 timeframe, adoption was characterized by isolated, utility-led pilots. For example, Wind Sim Power’s engagement with the New York Power Authority on its GLASS DLR technology reached commercial maturity (TRL 9) in 2023, proving the technology’s viability in a controlled setting.

- Post-2025, the scale of adoption has become systemic, with the International Energy Agency (IEA) estimating that broad application of AI tools could free up 175 GW of transmission capacity globally. This is a direct response to forecasts of 190 GW of new hyperscale data center capacity announced across 777 projects.

- Mature technologies like DLR are now being deployed by over 300 utilities, increasing power throughput by up to 40% on existing lines. This represents a shift from proving the technology to deploying it for immediate economic and operational benefit.

- Newer applications, such as flexible load management for data centers, have also gained significant traction. Companies like Emerald AI and Fluix AI are commercializing software that allows data centers to act as “grid-aware” flexible assets, a concept that was largely theoretical before the recent surge in AI power demand.

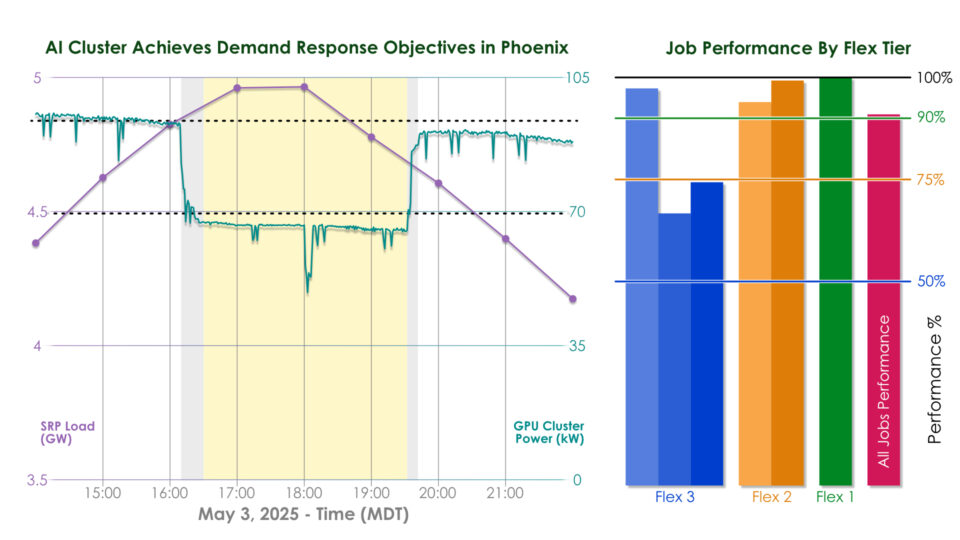

AI Cluster Shows Successful Grid Demand Response

This chart provides a specific, successful case study, which is a perfect illustration for a section discussing the industry’s progression from pilot projects to wider, systemic adoption and reliance.

(Source: NVIDIA Blog)

Smart Grid Market Growth: $52 B in 2025 Fueling GETs Investment

The economic case for AI-powered grid software is compelling, transitioning the market from a speculative growth area to a sector with a quantifiable, near-term return on investment. The escalating cost of grid congestion, estimated at $11.5 billion annually in the U.S., combined with the massive capital avoidance potential, has ignited rapid growth in the market for Grid-Enhancing Technologies (GETs) and related software platforms.

- The global smart grid market, valued at $52 billion in 2025 by Persistence Market Research, is now projected to grow at a CAGR of nearly 17%, a direct reflection of the urgent need to modernize grid operations to accommodate new loads.

- Specialized software segments show even more targeted growth. The Renewable Energy Forecasting Software market, crucial for managing an increasingly complex grid, is expected to grow from $0.67 billion in 2026 to $2.18 billion by 2036.

- The return on investment for utilities is rapid, with measurable benefits and positive returns often realized within 12-18 months of implementation. This is a stark contrast to the multi-decade payback periods for traditional transmission infrastructure projects.

- Investment is also driven by significant cost-avoidance. AI-driven optimization can deliver 5-15% CAPEX savings by reducing the need for new physical equipment and 1-3% OPEX efficiency gains through optimized operations.

GETs Offer Cheaper, Faster Grid Capacity Gains

The section discusses market growth fueled by investment in Grid Enhancing Technologies (GETs). This chart directly explains the value proposition and rationale for that investment by showing that GETs provide capacity gains more cheaply and quickly than alternatives.

(Source: Green Fuel Journal)

Table: Market Growth Projections for Grid Software

| Market Segment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Smart Grid | 2025-2032 | Valued at $52 billion in 2025, the market is projected to reach $154.1 billion by 2032 at a 16.8% CAGR, reflecting broad investment in grid modernization. | Persistence Market Research |

| Smart Grid | 2025-2033 | A separate forecast valued the market at $77.97 billion in 2025, projecting growth at a 17.6% CAGR, indicating strong consensus on rapid market expansion. | Sky Questt |

| Renewable Energy Forecasting Software | 2026-2036 | Projected to grow from $0.67 billion in 2026 to $2.18 billion by 2036, this niche is critical for integrating intermittent renewables and managing grid stability. | Meticulous Research |

| Grid-Aware AI Energy Management | 2025 | This emerging market was valued at $3.45 billion in 2025, highlighting the new premium on software that makes large loads like data centers responsive to grid needs. | Intellectual Market Insights Research |

AI in Energy Storage Market Projects Growth

The section heading indicates a table of market growth projections. This chart, while not a table, visually represents a market growth projection for a key segment of the grid software market, making it a suitable visual to accompany or represent the data.

(Source: Precedence Research)

Geographic Rollout of Grid Optimization: US Leads Amid Regulatory Shifts

The United States has become the primary geography for the accelerated deployment and policy development of AI-powered grid optimization, driven by its world-leading AI industry and proactive, if sometimes slow, regulatory bodies. While the underlying demand is global, the most significant commercial and regulatory activities are concentrated in North America, setting precedents for other regions to follow.

- In the 2021-2024 period, activity was fragmented, with states like New York and Massachusetts launching modernization plans. The federal Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) laid the financial groundwork for future deployments.

- From 2025 onward, federal action has become more pointed. The Federal Energy Regulatory Commission (FERC) set a June 2026 deadline to act on rulemaking for connecting large loads, a direct response to the data center boom, signaling a major potential shift in national policy.

- U.S. load growth forecasts now explicitly quantify the impact of AI and data centers, with peak demand projected to grow by 166 GW in five years, of which 90 GW is directly linked to data centers. This has forced U.S. utilities and regulators to prioritize software-based capacity solutions.

- While the U.S. leads in deployment, international bodies like the IEA are providing the global framework, with analyses showing AI can improve fault detection by 30-50% and provide critical data for grid operators worldwide.

Data Centers Are Largest Driver of US Power Demand Growth

This chart provides critical context for the section on the geographic rollout of grid optimization in the US. It identifies the primary driver (data center power demand) that necessitates and motivates the US to lead in adopting these technologies.

(Source: LinkedIn)

Technology Maturity for Grid Software: DLR at TRL 9, VPPs Commercially Scaled

The suite of AI-powered grid optimization tools exists on a spectrum of maturity, but the recent demand surge has accelerated the commercialization of even nascent technologies. What was once a field dominated by a single proven technology, Dynamic Line Rating, has now broadened to include a range of commercially viable software platforms addressing different facets of grid congestion and inefficiency.

- Dynamic Line Rating (DLR) is the most mature technology, having achieved Technology Readiness Level (TRL) 9. Its commercial viability was established before 2024, but its strategic importance skyrocketed after 2025 as the fastest way to increase transmission throughput.

- Virtual Power Plants (VPPs) have also reached commercial scale. Companies like CPower now manage portfolios exceeding 6.3 GW, demonstrating that aggregating distributed resources is no longer a pilot concept but a mainstream grid service.

- Topology Optimization software, from vendors like New Grid, has moved from a niche analytical tool to a critical operational platform. It provides real-time recommendations to reroute power and avoid congestion, directly addressing the bottlenecks created by inflexible data center loads.

- AI-driven forecasting and flexible load management are the newest entrants but are maturing rapidly due to direct demand from data center operators and utilities. Platforms from NVIDIA and Emerald AI show how AI workloads can be shifted to reduce grid strain, a critical capability for the future of AI infrastructure.

Grid Upgrades Compared by Capacity, Speed, and Cost

The section discusses the maturity and commercial scaling of various grid technologies. A comparative chart that evaluates different upgrade options on key metrics is a hallmark of analyzing commercially mature technologies ready for deployment.

(Source: Center on Global Energy Policy – Columbia University)

SWOT Analysis: AI-Powered Grid Software as a Capacity Solution

The strategic position of AI-powered grid software has been dramatically elevated by the energy demands of the AI boom, amplifying its strengths and opportunities while also increasing the stakes of its associated threats. The analysis shows that while the technology is robust and the market opportunity is vast, success is heavily dependent on overcoming entrenched regulatory and institutional inertia.

Grid Tech to Unlock 200+ GW of Capacity by 2033

The section is a SWOT analysis of AI grid software as a ‘capacity solution.’ This chart powerfully illustrates the ‘Strength’ and ‘Opportunity’ aspects of the SWOT by quantifying the massive potential capacity unlocked by the technology.

(Source: Third Way)

Table: SWOT Analysis for AI-Powered Grid Optimization

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated ability to increase capacity (10-40%) in pilots. Low CAPEX compared to new lines. | Rapid ROI (12-18 months) validated. Ability to unlock 175 GW of capacity recognized by IEA. Deployed by over 300 utilities. | The technology’s value proposition shifted from theoretical/niche to a proven, system-critical solution for immediate capacity needs. |

| Weaknesses | Concerns over cybersecurity of a more digitalized grid. Difficulty integrating with legacy utility OT systems. | Cybersecurity remains a primary concern. Shortage of skilled workers to manage complex AI systems becomes more acute. | The rapid push for deployment has outpaced the development of standardized security protocols and the training of a specialized workforce. |

| Opportunities | Growing renewable penetration required more grid flexibility. Early data center growth created some demand. | Explosive AI-driven demand creates a massive, urgent market. Favorable policy (FERC, IRA, IIJA). Congestion costs hit $11.5 B, making solutions more valuable. | The scale of the opportunity grew exponentially, driven by the realization that the AI boom is physically constrained by grid capacity. |

| Threats | Utility incentive models favored CAPEX (building lines) over OPEX (software). Slow regulatory approval cycles. | Regulatory inertia remains the single biggest threat. The utility business model is still not fully aligned with rewarding software-based efficiencies. | The mismatch between the speed of AI development and the speed of regulatory reform became the central conflict threatening deployment at scale. |

Scenario Modelling: Will FERC Rules Accelerate AI-Grid Software Adoption?

The single most critical factor for the widespread, rapid adoption of AI-powered grid software in the next 18 months is regulatory reform, particularly at the federal level in the United States. While the technology is ready and the economic need is undeniable, the speed of deployment hinges on whether utilities are incentivized or mandated to choose software-first solutions over traditional infrastructure builds.

- If this happens: FERC finalizes its rulemaking on large load interconnections by the June 2026 deadline with provisions that strongly encourage or mandate the use of Grid-Enhancing Technologies (GETs).

- Watch this: The immediate reaction from major utilities and the number of GETs-based solutions proposed in new interconnection requests. Look for filings from utilities in high-growth data center markets like Virginia, Ohio, and Arizona.

- This could be happening: A rapid acceleration in the deployment of DLR, topology optimization, and other GETs as utilities rush to comply and connect the massive queue of data centers and renewable projects, unlocking gigawatts of capacity in months, not years. Conversely, a weak or delayed ruling could signal a return to the slow, litigious process of building new lines, potentially stalling AI-related economic growth in power-constrained regions.

Simulator Accurately Predicts AI Power Demand

The section discusses ‘Scenario Modelling.’ This chart, which showcases a ‘simulator’ used for prediction, directly relates to the methodology of modeling and establishes the credibility of the tools used to create the scenarios discussed.

(Source: NVIDIA Blog)

The questions your competitors are already asking

This report covers one angle of the commercial adoption of grid optimization software. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the grid optimization software market as utilities move from pilots to systemic reliance?

- What is the outlook for deploying grid optimization software to connect new data center loads by 2026?

- Which utility operators are adopting technologies like Dynamic Line Rating (DLR) to manage the power demands of the AI sector?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.