Heidelberg Materials CCUS Strategy, $226 M Canadian Gov’t Partnership, $522 M UK Project, and 10+ Agreements (2021 to 2026)

Heidelberg Materials Project Execution: From Feasibility Studies to Commercial Scale CCUS

Heidelberg Materials’ strategy for decarbonization has decisively shifted from planning and feasibility assessments to full-scale project execution and commercial operation, a transition defined by a deep reliance on public-private partnerships. The period between 2021 and 2024 was characterized by foundational work, including engineering studies and securing initial funding commitments. The subsequent phase, from 2025 to 2026, is marked by final investment decisions, operational milestones, and the materialization of both financial opportunities and regulatory risks, validating its model while exposing its dependencies.

- Between 2021 and 2024, the company focused on laying the groundwork for its major Carbon Capture, Utilization, and Storage (CCUS) projects. This included engaging Worley for Front-End Engineering Design (FEED) at the Padeswood plant in February 2024, entering a partnership with the Canadian government in April 2023 for the Edmonton project, and securing U.S. Department of Energy funding for a Carbon SAFE study at its Mitchell, Indiana site in February 2023.

- From 2025 onwards, the strategy moved into the execution phase, with tangible progress and setbacks. The company reached a Final Investment Decision (FID) on the $522 million Padeswood project in September 2025 and its Brevik plant in Norway became operational, capturing its first 1, 000 metric tons of CO₂ by May 2025.

- This period also highlighted the inherent risks of the public-funded model. A prospective $500 million grant from the U.S. Department of Energy was cancelled in May 2025, and the company withdrew its environmental permit for the Slite CCS project in Sweden in March 2026, demonstrating the impact of political shifts and regulatory hurdles on its project pipeline.

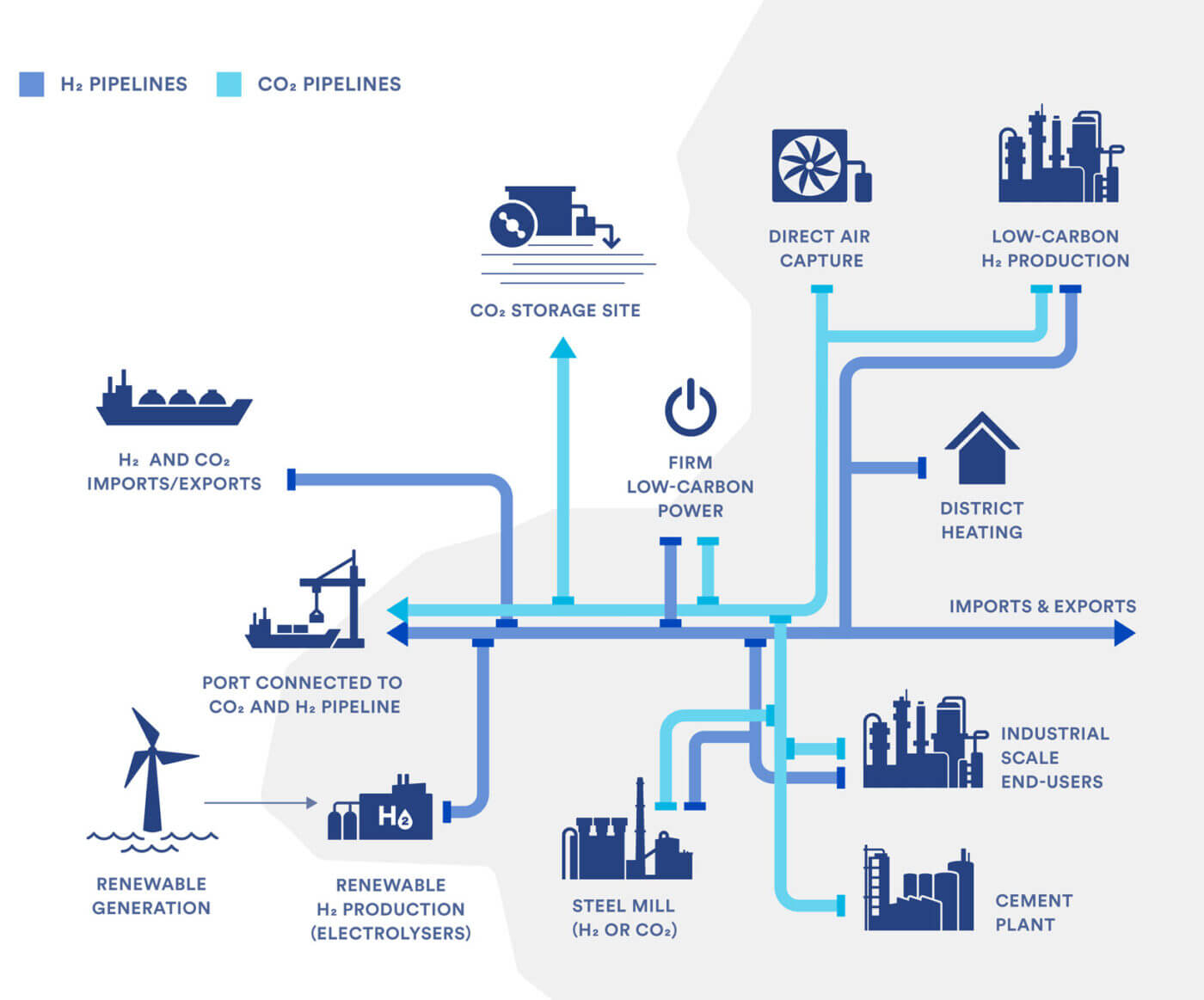

Diagram Shows Integrated CCUS Ecosystem

This diagram visualizes how CO2 from a cement plant is captured and moved to storage, illustrating the full-scale project execution discussed in the section.

(Source: Clean Air Task Force)

$522 M Padeswood FID, Heidelberg Materials Public Funding Reliance

Heidelberg Materials’ investment strategy is critically dependent on securing substantial public funding to de-risk the immense capital expenditure required for its large-scale decarbonization projects. This public-private partnership model was validated by major funding awards in Canada and Europe but was simultaneously tested by a significant grant cancellation in the United States, underscoring both the model’s effectiveness and its vulnerability to political and administrative risk.

Global Government Funding for CCUS Accelerates

This timeline highlights major public funding commitments for CCUS, directly supporting the section’s theme of Heidelberg’s reliance on a public-private partnership model.

(Source: IEA)

- In March 2025, the Canadian government committed up to $226 million to support the Edmonton CCUS project, a key component for building North America’s first full-scale net-zero cement plant.

- The company’s European decarbonization efforts received a major boost in November 2025 when the EU Innovation Fund selected four of its CCUS projects in Belgium, France, Italy, and Poland for grant agreement preparation.

- In the United Kingdom, Heidelberg Materials made a Final Investment Decision (FID) on its $522 million (£400 million) Padeswood CCS project in September 2025, a project backed by the UK Government.

- The high-risk nature of this dependency was exposed in May 2025, when a previously awarded $500 million grant from the U.S. Department of Energy for a CCUS project was cancelled, illustrating the financial volatility associated with reliance on a single government’s support.

Table: Heidelberg Materials Strategic Investments & Cancellations

| Project / Funding Source | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| EU Innovation Fund | Nov 2025 | Four CCUS projects in Belgium, France, Italy, and Poland were selected for grant agreements, accelerating decarbonization across Europe. | Heidelberg Materials |

| Padeswood CCS Project | Sep 2025 | A Final Investment Decision was reached for the $522 million project, supported by the UK Government, to build the country’s first carbon capture-enabled cement plant. | Carbon Herald |

| U.S. DOE Grant (Cancelled) | May 2025 | A previously awarded $500 million grant for a CCUS project in Louisiana was cancelled, highlighting the political and financial risks of the company’s funding strategy. | E&E News |

| Government of Canada Funding | Mar 2025 | Received a commitment of up to $226 million to support the construction of the Edmonton CCUS facility, North America’s first full-scale project in the cement sector. | Government of Canada |

| Edmonton CCUS Feasibility | Sep 2024 | Awarded $49 million from Canada’s Strategic Innovation Fund to support the feasibility study and planning for its full-scale CCUS project. | The Logic |

Heidelberg Materials 4 Key Government & Tech Partnerships (2021 to 2026)

Heidelberg Materials constructs a diverse partnership ecosystem designed to address distinct phases of its decarbonization strategy, engaging governments for funding, technology specialists for project execution, and infrastructure firms for logistical support. This multi-faceted approach allows the company to secure financial backing, access specialized engineering capabilities, and ensure the viability of CO₂ transport and storage for its large-scale projects.

The Four Stages of the CCUS Value Chain

This diagram breaks the CCUS process into capture, transport, and storage, representing the different phases that require the specialized government and tech partners mentioned in the text.

(Source: IEA)

- Government Partnerships for Funding: The company’s core strategy involves collaborating with national governments to secure financial backing. The partnership with the Government of Canada, solidified in March 2025 with up to $226 million in funding, and the support from the UK Government for the Padeswood project, are primary examples of de-risking capital-intensive projects.

- Technology & Engineering Partnerships for Execution: For project delivery, Heidelberg Materials partners with specialized firms. In December 2025, it selected Worley and Mitsubishi Heavy Industries (MHI) to deliver the Padeswood carbon capture facility, leveraging Worley’s construction services and MHI’s capture technology.

- Infrastructure Partnerships for Logistics: Recognizing that capture is only one part of the equation, the company forms alliances with infrastructure operators. The March 2024 partnership with Fluxys in Belgium aims to develop the CO₂ transmission pipelines necessary for the Anthemis CCUS project.

- Circular Economy & Innovation Partnerships: The company also engages in innovative collaborations to advance circularity and test new technologies. A July 2025 project with Seabound pilots a novel marine carbon capture system on a cement-carrying vessel, with plans to use the captured CO₂ at the Brevik plant.

Table: Heidelberg Materials Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Worley and MHI | Dec 2025 | Selected to provide engineering, procurement, and construction services using MHI’s technology for the Padeswood carbon capture facility in the UK. | Worley |

| Etex | Oct 2025 | Launched the CEMLOOP XL project to recycle fibre cement waste into a low-carbon raw material, supported by the EU’s LIFE programme. | Etex Group |

| Government of Canada | Mar 2025 | Entered a partnership to support the Edmonton CCUS project with funding of up to $226 million to build the world’s first net-zero cement plant. | Government of Canada |

| Fluxys | Mar 2024 | Partnered to develop CO₂ transmission infrastructure for the Anthemis CCUS project at the Antoing facility in Belgium. | Fluxys |

| Fortera | Mar 2021 | Partnered to implement a process that captures CO₂ from kiln exhaust and converts it into a cementitious material at the Redding, California plant. | Heidelberg Materials US |

North America vs. Europe, Heidelberg Materials CCUS Project Locations

Heidelberg Materials pursues a diversified geographic strategy, developing a portfolio of flagship CCUS projects across North America and Europe to mitigate political risks and capitalize on regional funding opportunities. While the 2021-2024 period involved parallel planning in both regions, the 2025-2026 timeframe has seen these paths diverge, with strong federal support in Canada contrasting with political volatility in the U.S. and broad EU-level backing being challenged by local regulatory issues in specific European nations.

North America and Europe Lead CCUS Market

This forecast identifies North America and Europe as the key CCUS markets, providing the exact geographic context for Heidelberg’s diversified regional strategy.

(Source: MarketsandMarkets)

- North America: The company’s focus is on two major projects. The Edmonton, Canada project has emerged as a strategic priority, securing up to $226 million from the Canadian government in March 2025 to become the world’s first full-scale net-zero cement plant. In contrast, U.S. ambitions faced a major setback with the May 2025 cancellation of a $500 million DOE grant, highlighting the region’s political risk. The Mitchell, Indiana project continues with earlier funding for a test well.

- Europe: The strategy in Europe is characterized by a multi-country approach. The Brevik plant in Norway became the world’s first operational industrial-scale CCUS plant in the cement industry in 2025. The $522 million Padeswood project in the UK reached a final investment decision in September 2025. Furthermore, the EU Innovation Fund selected four additional projects in Belgium, France, Italy, and Poland for grant preparations in November 2025.

- Geographic Risk Mitigation: The diversified portfolio acts as a hedge. While the company withdrew its environmental permit for the Slite project in Sweden in March 2026 due to local regulatory challenges, progress in Canada, the UK, and at the broader EU level ensures the overall corporate strategy remains on track. This geographic diversification is essential for navigating the complex and unpredictable landscape of public funding and permitting.

CCUS Commercialization, Heidelberg Materials 400 k Tonne Brevik Plant

Heidelberg Materials has successfully transitioned its CCUS capabilities from the development stage to commercial reality, a move validated by the operational start of its Brevik plant and the market introduction of its evo Zero® carbon-captured cement. The focus has pivoted from technological feasibility, which dominated the 2021-2024 period, to operational scaling and market creation in 2025 and beyond.

Chart Pinpoints CO2 Source in Cement Production

This flowchart identifies the kiln as the main CO2 source, explaining the specific industrial process targeted by Heidelberg’s commercial carbon capture technology at the Brevik plant.

(Source: Clean Air Task Force)

- The period from 2021 to 2024 was defined by technology selection and project design, such as planning for a hybrid oxyfuel and post-combustion capture unit in Belgium. The primary goal was to establish the technical and engineering foundation for its global project portfolio.

- A significant milestone was achieved in 2025 when the Brevik CCS plant in Norway, the world’s first industrial-scale capture facility in the cement industry, became operational. With a capacity of 400, 000 tonnes of CO₂ per year, the plant had already captured and stored its first 1, 000 metric tons by May 2025.

- This technological achievement was immediately translated into a commercial product with the launch of evo Zero®, marketed as the world’s first carbon-captured, near-zero cement. This product creates a tangible output for the company’s massive CCUS investments.

- The company continues to advance its technology pipeline with pilot projects such as the Re Concrete process and enforced carbonation facilities, aiming to create a closed loop for materials and further reduce emissions.

SWOT Analysis, Heidelberg Materials Public Funding Strategy

Heidelberg Materials’ aggressive, publicly funded CCUS strategy establishes it as a first-mover in a hard-to-abate sector, creating a significant competitive advantage. However, this approach introduces a critical dependency on government support, making the company vulnerable to political shifts and regulatory delays, a weakness that was clearly demonstrated between 2025 and 2026.

- Strengths: The company’s primary strength is its first-mover advantage in deploying full-scale CCUS, evidenced by the operational Brevik plant and the advanced status of its Edmonton and Padeswood projects. This is supported by a geographically diversified portfolio that mitigates single-country risk.

- Weaknesses: The strategy’s main weakness is its heavy reliance on public funding, which exposes it to political and administrative volatility. The cancellation of the $500 million U.S. DOE grant is a direct example of this vulnerability.

- Opportunities: The primary opportunity lies in creating and dominating a new market for premium, low-carbon cement like evo Zero®. Increasing carbon pricing and regulatory pressure on competitors create a favorable market environment for these products.

- Threats: The strategy faces threats from complex and lengthy regulatory processes, as seen with the withdrawal of the Slite permit in Sweden. Competition from other major players like Holcim and the inherent risks of executing multi-billion-dollar industrial projects also pose significant challenges.

Table: SWOT Analysis for Heidelberg Materials’ CCUS Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Formulated a multi-regional CCUS strategy and secured initial partnerships (Worley, Gov’t of Canada). | Brevik plant became operational, Padeswood reached FID, and Edmonton project secured major funding. | The first-mover strategy was validated through the successful launch of the world’s first operational CCUS cement plant. |

| Weaknesses | The high capital requirement and theoretical dependence on public funding were identified as strategic risks. | The $500 million U.S. DOE grant was cancelled, making the theoretical risk a material reality. | The dependency on public funds was confirmed as a significant vulnerability, subject to sudden political shifts. |

| Opportunities | The concept of a “green premium” for low-carbon cement was a forward-looking market assumption. | Launched evo Zero® and Evo Build™ brands, creating tangible low-carbon products to capture market value. | The ability to monetize CCUS investments through premium products shifted from a concept to a commercial strategy. |

| Threats | Regulatory hurdles and competition were known but largely prospective challenges. | Withdrew the environmental permit for the Slite, Sweden project, a direct impact of regulatory complexity. | The threat of local permitting and regulatory delays was validated as a major potential obstacle to project execution. |

Heidelberg Materials 2026 Outlook, Monitoring Edmonton & Padeswood

The key indicators for Heidelberg Materials’ CCUS strategy over the next 18-24 months will be its ability to execute on its two flagship construction projects and translate its technological leadership into market-based financial returns. Any deviation in the project timelines for the Edmonton and Padeswood facilities will be a critical signal regarding the scalability and economic viability of its entire decarbonization model.

Carbon Capture Market Forecasted for Strong Growth

The projected 25% annual growth in the carbon capture market illustrates the future financial opportunity that Heidelberg’s 2026 outlook is banking on.

(Source: MarketsandMarkets)

- Monitor Flagship Project Execution: Adherence to budget and construction schedules for the Edmonton, Canada and Padeswood, UK projects is paramount. These projects are the primary validators of the company’s ability to deliver complex, capital-intensive facilities and are being closely watched by the industry.

- Finalization of EU Funding: The final grant agreements with the EU Innovation Fund for the four projects in Belgium, France, Italy, and Poland should be monitored. The specific funding amounts and attached timelines will determine the pace of decarbonization across its key European operations.

- Market Adoption of Low-Carbon Products: Track the commercial performance, pricing, and customer uptake of evo Zero® carbon-captured cement. The ability to command a sustained “green premium” is essential to justifying the long-term economics of the CCUS investments.

- Resolution in Sweden: Following the withdrawal of the environmental permit for the Slite CCS project, the company’s next actions are a key indicator. Whether it re-engages with a revised plan or reallocates capital will signal its approach to overcoming regulatory setbacks.

The questions your competitors are already asking

This report covers one angle of commercial-scale CCUS deployment in the cement sector. The questions that matter most depend on your work.

- Heidelberg Materials’ activities in North America. Is the Canadian government partnership progressing from announcement to commercial deployment?

- Heidelberg Materials investments and funding. Is the $522M Padeswood CCUS project on track for its final investment decision?

- Which cement producers are gaining or losing ground in the race to deploy commercial-scale CCUS?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.