DAC Commercialization Risks, Noya’s 60% VC Funding Drop, 1 CEC R&D Project, and 3 Offtake Agreements (2021 to 2025)

DAC Adoption Challenges, Noya’s Shift from R&D to Market Failure

The Direct Air Capture (DAC) industry experienced a critical shift in 2025, where technological promise became insufficient for survival, as market demand for proven, delivered carbon removal led to the failure of pre-commercial firms like Noya. This market reckoning exposed the immense difficulty of transitioning from research and development to commercial-scale deployment in the capital-intensive climate technology sector.

- Between 2021 and 2024, the primary industry focus was on technology development, attracting venture funding and pre-purchase agreements based on future potential. During this period, Noya successfully secured early-adopter customers, including Shopify and Watershed, validating its prospective carbon removal credits.

- The market correction in 2025 saw buyers and investors pivot, prioritizing companies with operational, at-scale projects capable of delivering verified tonnes of carbon removal. The market shifted preference from future potential to currently delivered results, a change that proved fatal for firms not yet at commercial scale.

- As a direct consequence, Noya, despite securing a key research and development project with the California Energy Commission in April 2025, announced it was ceasing all activities in August 2025. This failure illustrates the perilous “valley of death” for hardware startups unable to bridge the gap from pilot projects to profitable operations.

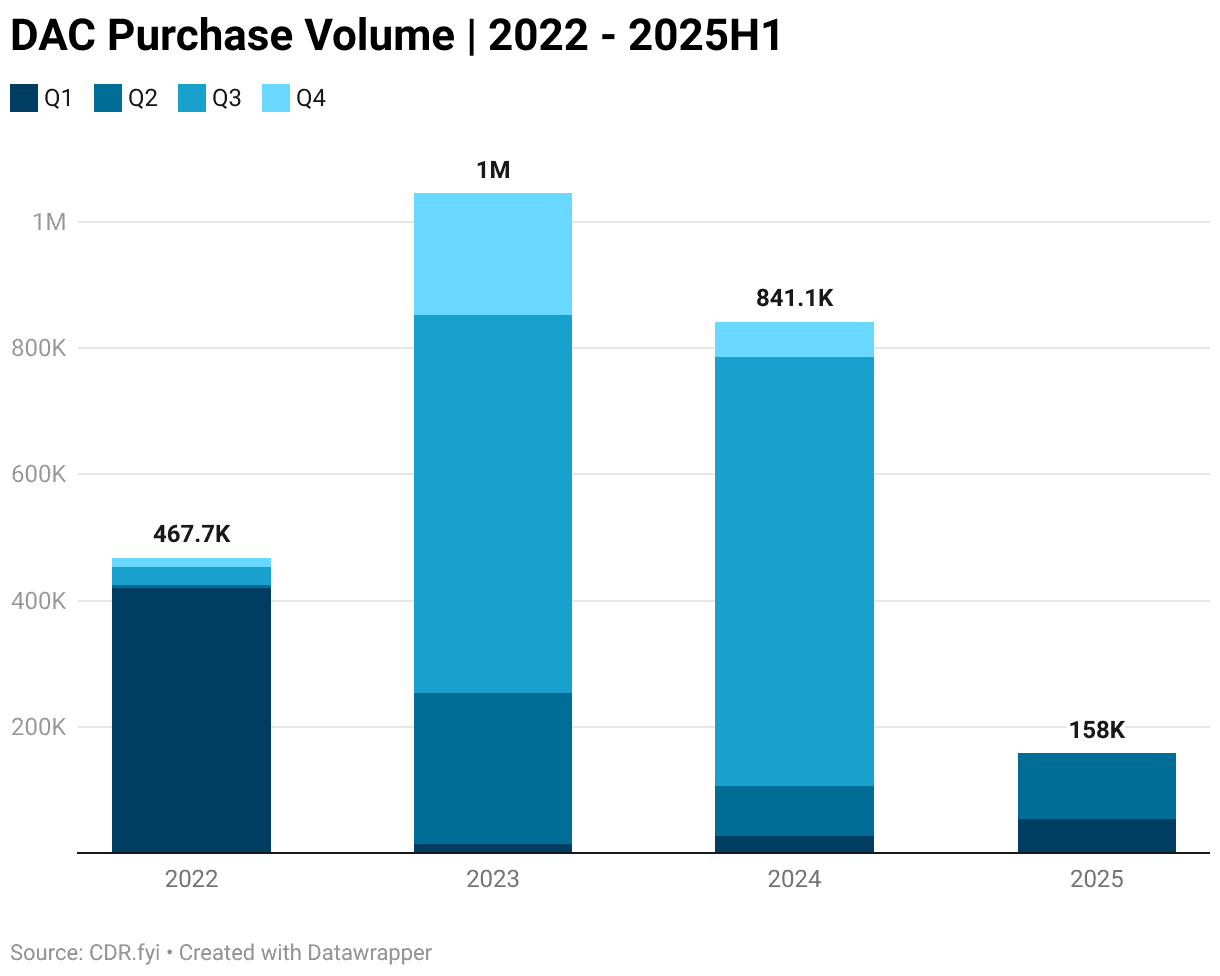

DAC Purchase Volume Plummets in 2025

This chart directly visualizes the ‘DAC Adoption Challenges’ and ‘Market Failure’ described in the section heading by showing a collapse in demand, a primary factor contributing to Noya’s failure.

(Source: CDR.fyi)

60% VC Funding Drop, Noya’s Shutdown Amid DAC Market Correction

A severe contraction in venture capital funding for the Direct Air Capture (DAC) sector in 2025 created an untenable financial environment for early-stage companies, directly contributing to Noya’s cessation of operations. The sudden scarcity of capital exposed the vulnerability of firms reliant on continuous funding rounds to finance their path to commercial scale.

- Venture funding for US-based Direct Air Capture startups plummeted by more than 60% in the first quarter of 2025 compared to previous periods, signaling a dramatic shift in investor sentiment away from pre-revenue climate technology hardware.

- This “capital crunch” removed the financial runway for companies like Noya, which required significant investment to scale its innovative technology from the lab to industrial deployment. The market was no longer rewarding technological milestones with sufficient growth capital.

- While early-stage backing from investors like Lowercarbon Capital was crucial for initial development, the tightening market made securing larger, subsequent funding rounds for capital-intensive hardware companies exceptionally challenging, leaving Noya without the resources to continue.

VC Funding for DAC Tech Collapses in 2025

The chart is a perfect match, as its headline and content directly illustrate the ‘60% VC Funding Drop’ and ‘Market Correction’ that led to Noya’s shutdown, as stated in the section heading.

(Source: Global Corporate Venturing)

Table: Noya DAC Cancellation and Market Events 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Noya | August 2025 | The company announced it was “winding down operations” after failing to secure the necessary funding to scale its technology, despite having early customer agreements and a promising technical approach. | Quantum Commodity Intelligence |

| US DAC Startups | Q 1 2025 | Venture funding for US-based DAC companies fell by over 60%, signaling a sharp market correction and increased investor scrutiny on the path to profitability for capital-intensive climate tech. | Bloomberg |

Noya 3 Offtake Agreements, Shopify and Watershed Credit Purchases (2025)

Noya’s partnerships in 2025 highlight a critical mismatch between securing early-adopter customers for future carbon credits and obtaining the substantial, long-term capital required for project deployment. The presence of high-profile offtake agreements was not enough to ensure financial solvency.

- Commercial offtake agreements with leading carbon removal buyers Shopify and Watershed, along with an unnamed university endowment, provided strong market validation for Noya’s technological approach and future credit supply.

- A research and development project grant awarded by the California Energy Commission in April 2025 demonstrated government support for its technical pathway, specifically for enhancing its sorbent materials and electric regeneration process.

- Ultimately, these partnerships, which were structured as pre-purchase agreements and R&D grants, proved insufficient to finance the capital-intensive scale-up required to build and operate commercial DAC facilities, exposing a fatal flaw in its funding strategy.

Durable Carbon Removal Purchases Grow Through 2025

This chart illustrates the growing market trend for durable carbon removal, which provides the necessary context for understanding why companies like Shopify and Watershed were making significant credit purchases and offtake agreements in 2025.

(Source: CDR.fyi)

Table: Noya Key Partnerships and Projects 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| California Energy Commission | April 2025 | A project to enhance sorbent materials and CO₂ regeneration by integrating amines with an electric heating system, aiming for TRL 5 with a target energy use of ≤1, 731 k Wh/ton. | California Energy Commission |

| Shopify & Watershed | Confirmed 2025 | Secured carbon removal credit purchase agreements with prominent corporate buyers, validating market demand for its DAC technology prior to its shutdown. | Quantum Commodity Intelligence |

US Market Dominance, Noya’s California-Based Operations and R&D Focus

The United States, particularly California, served as the epicenter for Noya’s development and ultimate failure, reflecting the region’s dual role as a global hub for climate tech innovation and a site of intense market competition and consolidation.

- From 2021 to 2024, California’s supportive policy environment, access to venture capital, and deep technical talent pool made it an ideal location for Noya to establish its operations and develop its unique DAC technology.

- This regional focus was solidified in 2025 when Noya’s most significant public-private partnership was a research project with the California Energy Commission, cementing its operational and development activities within the state.

- However, the US market, while leading in planned DAC capacity, also became the primary arena for the 2025 market correction. The failure of several US-based startups, including Noya, Nori, and Alkali Earth, signaled that even in the most developed market, survival was not guaranteed for pre-commercial entities.

US Dominates Planned DAC Project Capacity in 2025

The chart directly supports the section’s topic of ‘US Market Dominance’ by visually confirming that the US leads in planned DAC project capacity, aligning with Noya’s California-based operations.

(Source: Internationale Politik Quarterly)

Technology Readiness Failure, Noya’s TRL 5 Goal vs. Market Reality

Noya’s strategic focus on advancing its DAC technology to Technology Readiness Level (TRL) 5 proved insufficient as the market in 2025 abruptly shifted its valuation criteria from technical milestones to commercially demonstrated, at-scale operational capacity.

- Noya’s technology was based on an innovative and potentially cost-effective approach using abundant activated carbon materials and an energy-efficient electric regeneration process. It aimed for an ambitious energy performance target of less than or equal to 1, 731 k Wh per ton of CO₂.

- The 2025 project with the California Energy Commission was designed to formally validate these performance metrics and achieve TRL 5, a critical step in de-risking the technology for the next stage of investors and project financiers.

- Despite this technical progress, the market’s pivot to prioritizing immediately available, verifiable carbon removal tonnes meant that progress toward TRL 5 was no longer a compelling enough milestone to secure the necessary scale-up capital, rendering its R&D advancements commercially moot.

DAC Cost-Benefit Ratio Compared to Renewables

This chart highlights a critical aspect of ‘Market Reality’ by comparing the unfavorable cost-benefit ratio of DAC to other technologies, explaining the ‘Technology Readiness Failure’ and the gap between Noya’s R&D goals and commercial viability.

(Source: Nature)

Noya SWOT Analysis, Technical Strengths vs. Market Threats (2021-2025)

A review of Noya’s trajectory reveals a company with strong technical fundamentals and early market validation that was ultimately overcome by external market threats and its internal weakness of high capital dependency in a tightening financial landscape.

- The company’s core strengths were its innovative, low-cost sorbent approach and a clear R&D validation pathway with government backing.

- Its primary weaknesses were its pre-commercial status and a business model that required massive, continuous capital injections to cross the “valley of death” to industrial scale.

- External threats, particularly the sudden contraction of venture capital and a shift in buyer demand, proved insurmountable and were the direct cause of its failure.

DAC Market Growth Plateaus After 2023

A plateau in market growth is a classic external ‘Market Threat’ in a SWOT analysis. This chart provides a clear data point for the threat aspect of the Noya SWOT analysis section.

(Source: Technavio)

Table: SWOT Analysis for Noya DAC Initiatives 2025

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Innovative technology concept using activated carbon and low-energy regeneration. Backed by venture capital firm Lowercarbon Capital. | Secured a key R&D project with the California Energy Commission to validate performance targets (≤1, 731 k Wh/ton) and reach TRL 5. | The CEC project validated the technical premise, but this strength was insufficient to overcome market headwinds. |

| Weaknesses | Pre-commercial, pre-revenue status with high capital intensity. Reliant on future promises of carbon removal to secure funding. | Inability to secure sufficient follow-on funding to transition from pilot to commercial scale. Pre-purchase agreements did not provide enough capital. | The 2025 funding winter validated that a business model reliant on continuous VC funding for hardware scale-up is a critical weakness. |

| Opportunities | Growing demand for high-durability carbon removal credits from corporate buyers. Access to policy incentives like the 45 Q tax credit. | Early customer agreements with Shopify and Watershed demonstrated a clear path to market if the technology could be scaled. | The opportunity for early-stage companies evaporated as buyers and investors shifted focus to already operational, scaled projects. |

| Threats | Competition from more established, better-funded DAC companies like Climeworks. Long development timelines and high costs of DAC. | Venture funding for US DAC startups dropped by over 60%. The market shifted to demand delivered tonnes, not future credits. | The theoretical threat of a market correction became a reality, leading directly to the failure of Noya and other pre-commercial firms. |

1 Key Signal, Noya’s IP Acquisition and Talent Dispersal

Following Noya’s 2025 shutdown, the most critical forward-looking signal for the DAC market is the potential acquisition of its intellectual property and the dispersal of its technical team into the broader climate tech ecosystem.

- If a major competitor or a new market entrant acquires Noya’s intellectual property, particularly its unique sorbent chemistry and low-energy electric regeneration process, watch for an acceleration in their own cost-reduction and technology development roadmaps.

- This could be happening if established players like Climeworks or project developers such as Deep Sky announce new pilot projects that incorporate similar activated carbon or low-temperature electrical regeneration approaches in their next-generation designs.

- The movement of Noya’s engineering and scientific talent to other firms will also be a leading indicator. Tracking where this expertise lands could signal which competing companies are most aggressively strengthening their research and development capabilities in solid sorbent DAC technology.

Noya Hosted DAC Demo Tour in April 2025

This chart, showing a public-facing event just before the company’s collapse, serves as the ‘1 Key Signal’ of how quickly events unfolded, setting the stage for the subsequent discussion of IP acquisition and talent dispersal.

(Source: Carbon Removal Updates – Substack)

The questions your competitors are already asking

This report covers the commercialization ‘valley of death’ for DAC startups, centered on Noya’s 2025 market failure. The questions that matter most depend on your work.

- Which DAC companies are gaining ground after the 2025 market correction, and which are at risk of failure like Noya?

- What is the outlook for DAC project financing following the sector’s 60% VC funding drop and market shift?

- What is the status of pre-purchase offtake agreements from buyers like Shopify and Watershed following Noya’s shutdown?

- Which corporate buyers are still adopting DAC carbon removal, and how have their purchasing criteria changed since 2025?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

DAC Market Projected for Explosive Growth

This chart directly addresses ‘the questions your competitors are already asking’ about the market’s future after a major failure. The projection of explosive growth is a key data point for strategic planning and evaluating long-term market viability.

(Source: P&S Intelligence)