Bloom Energy SOFC Contracts, $2.65 B AEP Deal, 2.8 GW Oracle Agreement, and $5 B Brookfield Partnership (2021 to 2026)

SOFC Commercial Scale, Bloom Energy Captures $7.65 B in Data Center Deals

Solid Oxide Fuel Cells (SOFCs) have become the primary commercially viable solution for the acute power deficit facing AI data centers, shifting from a niche backup power source to a primary generation asset between 2024 and 2026. The inability of traditional power grids to meet the explosive demand from AI compute has created an urgent need for behind-the-meter power, a market Bloom Energy now dominates. The company secured a staggering $7.65 billion in data center-related contracts in a 90-day period in early 2026, confirming the market’s acceptance of natural gas-fueled SOFCs as the most bankable and rapidly deployable power solution.

- Between 2021 and 2024, fuel cell adoption in data centers was characterized by smaller-scale pilots and backup power applications, such as Microsoft’s 250-kilowatt PEM fuel cell test in Dublin. These projects served as technical validation but did not address primary power needs at the campus scale.

- The period from 2025 to today marks a strategic inflection point, driven by grid interconnection queues that extend for years. In April 2026, Oracle signed a master services agreement for up to 2.8 GW of Bloom Energy’s SOFC systems, moving well beyond pilot-scale and establishing fuel cells as a core infrastructure component for its AI expansion.

- The market shift is further solidified by utility and infrastructure players entering the space. In January 2026, American Electric Power (AEP) finalized a $2.65 billion, 20-year offtake agreement for up to 1 GW of SOFC capacity, signaling that utilities now view fuel cells as a viable way to serve large industrial loads that the grid cannot accommodate.

- This commercial momentum contrasts sharply with alternative technologies. While PEM fuel cells and green hydrogen represent a long-term zero-carbon goal, their supply chains and cost structures are not mature enough to meet the gigawatt-scale demand emerging today.

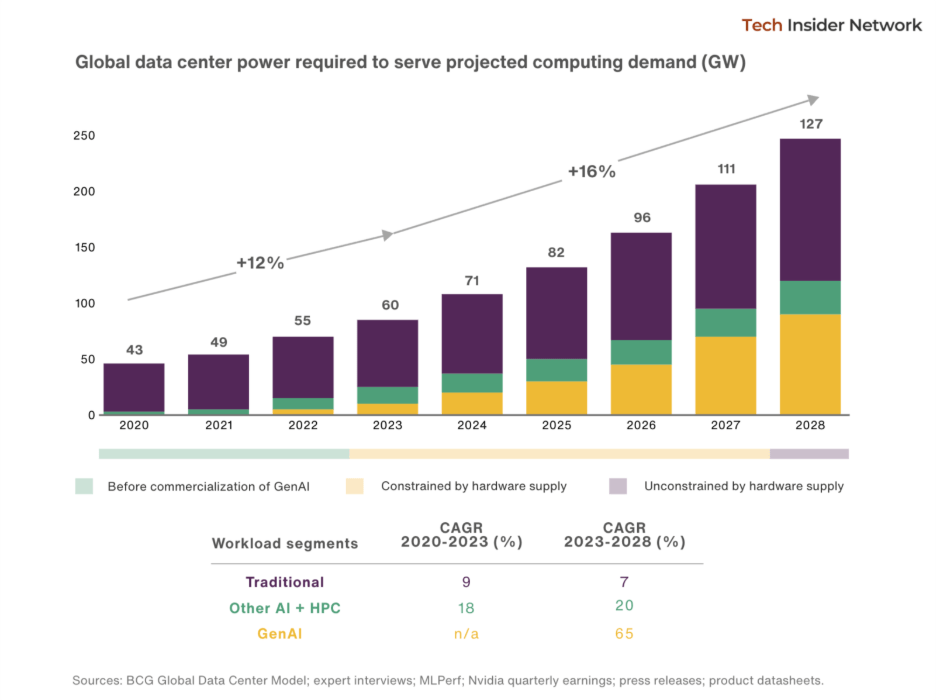

AI Creates Acute Data Center Power Deficit

This chart quantifies the explosive power demand from AI, which is the primary market driver for Bloom Energy’s on-site power solutions mentioned in the section.

(Source: Seeking Alpha)

Partnership Analysis, Bloom Energy Secures Data Center Deals with Oracle and AEP

Bloom Energy’s recent partnerships reveal a focused strategy of locking in cornerstone agreements with hyperscale data center operators and major utility providers, effectively creating a captured market for its SOFC technology. These deals are not just for equipment sales but are structured as long-term power delivery and financing arrangements, indicating a maturing business model designed to support multi-billion-dollar infrastructure projects.

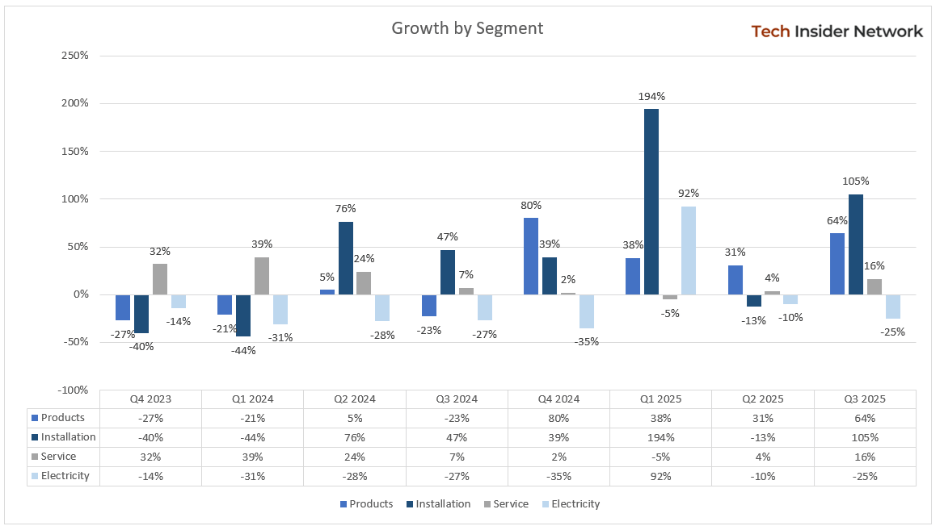

Partnerships Drive Explosive Deployment Growth

Reflecting the success of its partnership strategy, this chart shows massive growth in the company’s ‘Installation’ segment, indicating a rapid ramp-up of projects.

(Source: Seeking Alpha)

Table: Bloom Energy Strategic Data Center Partnerships (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Oracle | April 2026 | Master services agreement to procure up to 2.8 GW of SOFC systems. This secures a primary power source for Oracle’s AI data centers, bypassing grid constraints and accelerating time-to-market for new capacity. | DCD |

| Brookfield | March 2026 | A $5 billion financing partnership to fund the deployment of power solutions for AI data centers. This de-risks capital-intensive deployments and provides a streamlined financial vehicle for customers. | Yahoo Finance |

| American Electric Power (AEP) | January 2026 | A $2.65 billion, 20-year offtake agreement to deploy up to 1 GW of SOFCs. This positions Bloom Energy as a solution provider for utilities struggling to meet data center load growth. | Yahoo Finance |

US Focus, Bloom Energy SOFC Deployments Target Domestic Data Center Power Crisis

The geographic concentration of SOFC deployments is overwhelmingly centered on the United States, directly correlating with the locations of major data center alleys and regions with constrained grid capacity. The power demand from U.S. data centers is projected to add 65-90 GW of peak load by 2030, and regional transmission organizations like PJM are forecasting load growth of 5.3% annually, creating a fertile ground for on-site power generation solutions.

- Between 2021 and 2024, fuel cell projects were geographically diverse but smaller in scale, with notable activity in both the U.S. and Europe. The focus was on demonstrating capability in different regulatory environments.

- Starting in 2025, the commercial focus has pivoted sharply to the U.S. market. The major agreements with Oracle, AEP, and the financing partnership with Brookfield are all primarily aimed at supporting the rapid build-out of AI infrastructure within the United States.

- While markets like South Korea show interest in hydrogen, exemplified by Hyundai’s planned $6.3 billion hub with a 200 MW PEM electrolyzer, these projects have longer development timelines (2029 completion) and are not yet addressing the immediate gigawatt-scale data center power needs seen in the U.S.

- North America leads regional adoption with 34% of the fuel cell market for data centers, driven by the hyperscale demand and readiness of solutions like Bloom Energy’s SOFCs to deploy at scale.

Technology Maturity, Bloom Energy Commercial SOFC Validation for Data Centers

SOFC technology has achieved full commercial maturity for large-scale, baseload power applications in the data center sector, a status validated by the size and financial commitment of recent contracts. The technology’s high electrical efficiency and ability to run on readily available natural gas give it a decisive advantage in deployment speed and operational economics over competing low-carbon alternatives in the current market.

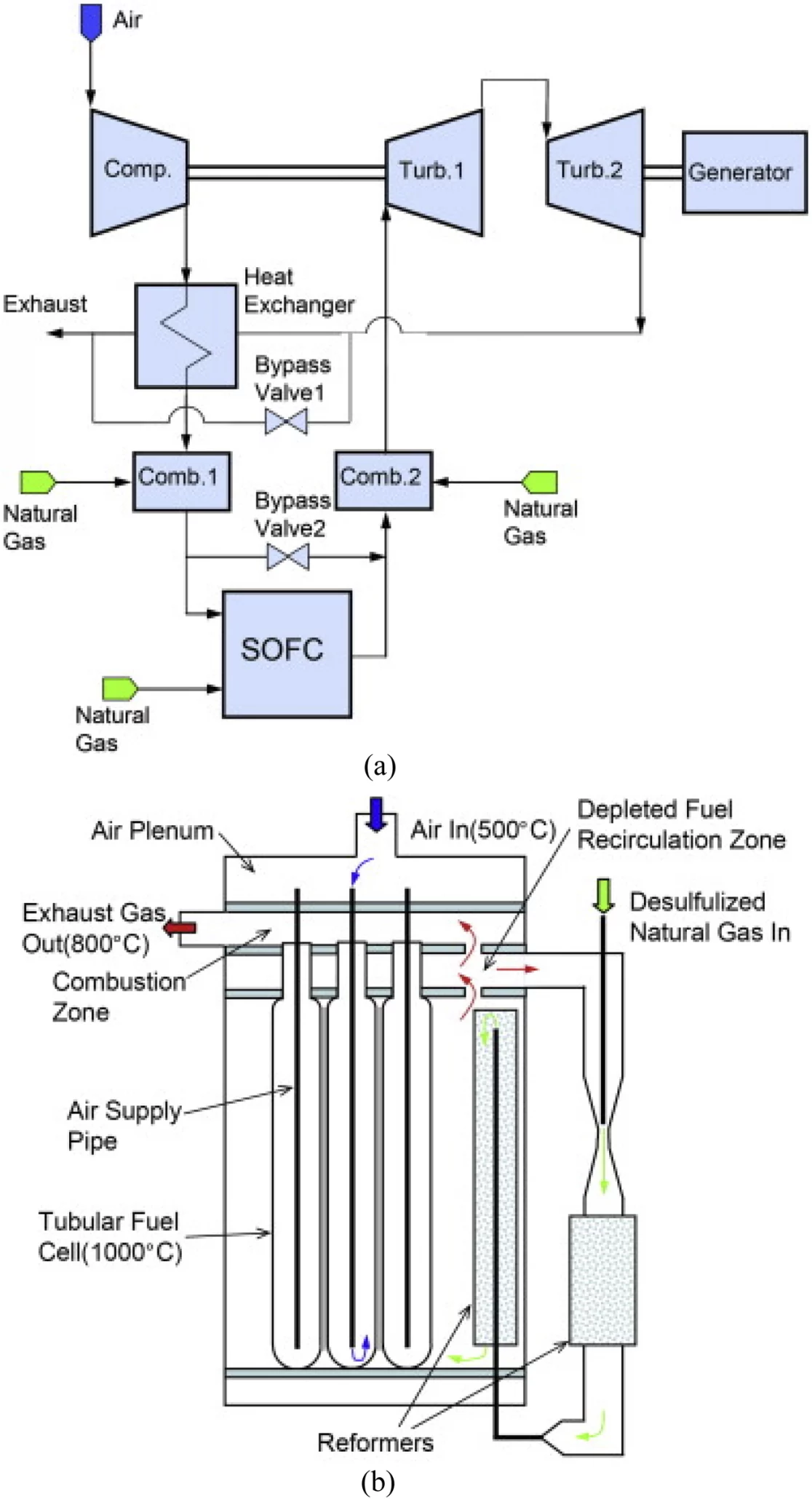

SOFC Technology Generates On-Site Power

This schematic illustrates how a Solid Oxide Fuel Cell (SOFC) system works, directly supporting the section’s discussion of the technology’s commercial maturity and advantages.

(Source: Frontiers)

- In the 2021-2024 period, the debate often centered on the technical merits of SOFC versus PEM fuel cells. While SOFCs offered higher efficiency, PEMs had faster startup times. The choice was application-dependent, and neither had been proven for multi-hundred-megawatt primary power deployments.

- The key shift in 2025-2026 is the market’s verdict that SOFC’s operational characteristics are better suited for the baseload power profile of data centers. The massive 2.8 GW Oracle deal and 1 GW AEP agreement serve as definitive validation points that have resolved previous questions about scalability and bankability.

- Operational risks, such as stack degradation, remain a technical consideration but have been deemed manageable by customers, as evidenced by 20-year offtake agreements. An expert call noted the cost per k Wh is a premium to combined cycle gas plants, but this premium is acceptable in exchange for speed and location flexibility.

- The fuel flexibility of SOFCs provides a crucial element of future-proofing. While operating on natural gas today, they offer a clear pathway to blend or fully transition to blue or green hydrogen as supply becomes available, mitigating the risk of stranded assets under future carbon regulations.

SWOT Analysis of Bloom Energy’s SOFC Data Center Strategy

The current market dynamics present a clear set of strengths and opportunities for SOFC technology in the data center sector, but they are coupled with tangible weaknesses and long-term competitive threats. Bloom Energy’s strategy successfully leverages its core strengths to capitalize on an urgent market need, but it remains exposed to fuel price volatility and the advancement of alternative clean energy technologies.

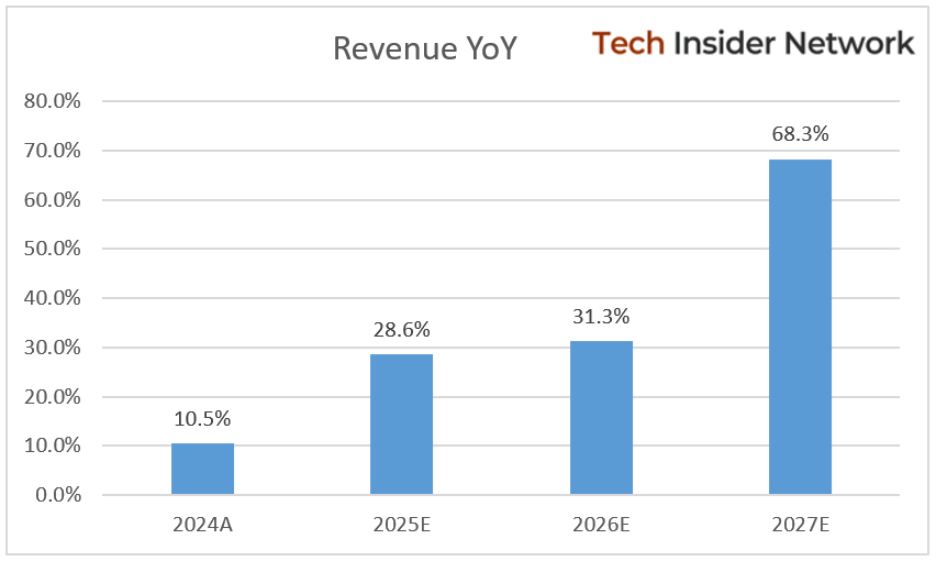

Revenue Growth Validates Data Center Strategy

Forecasted revenue growth surging to nearly 70% validates the ‘Opportunity’ aspect of the SWOT analysis, showing the financial success of capitalizing on the data center power crisis.

(Source: Seeking Alpha)

Table: SWOT Analysis for Bloom Energy SOFCs in Data Centers

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency, fuel flexibility (natural gas, hydrogen), lower emissions than grid average. | Demonstrated rapid deployment capability (1-2 years vs. multi-year grid upgrades), proven scalability to hundreds of megawatts per site. | The Oracle (2.8 GW) and AEP (1 GW) agreements validated that deployment speed is the most critical competitive advantage, justifying a cost premium. |

| Weaknesses | Higher LCOE than traditional grid power, reliance on natural gas infrastructure, concerns over long-term stack degradation. | Continued dependence on natural gas feedstock creates carbon emissions exposure. The cost per k Wh remains higher than combined cycle gas plants. | The market confirmed its willingness to accept a higher LCOE in exchange for speed. Natural gas dependence is accepted as a near-term compromise with a future hydrogen option. |

| Opportunities | Growing data center power demand, increasing corporate decarbonization goals, potential for hydrogen blending. | Explosive AI-driven power demand creating a 65-90 GW U.S. market opportunity. Grid interconnection queues are now a primary business constraint for data center operators. | The AI boom transformed the market from a steady growth opportunity into an urgent, supply-constrained crisis that perfectly matches SOFC’s value proposition of rapid, on-site power. |

| Threats | Competition from other clean energy sources (solar, wind), potential for stricter emissions regulations on natural gas. | Next-generation geothermal projects demonstrate a 70% reduction in deployment timelines to under 3 years. Methane pyrolysis (“turquoise hydrogen”) emerges as a potential low-cost, low-carbon fuel source. | Geothermal has emerged as the most credible long-term threat, offering 24/7 carbon-free baseload power. Its timeline improvements make it a direct competitor for projects on a 3-5 year horizon. |

Scenario Modelling and Forward-Looking Summary

For data center developers and investors, the critical action for projects requiring power before 2029 is to secure on-site generation capacity, with SOFCs representing the most viable path. If AI-driven power demand continues to outpace grid capacity expansion at the current rate, expect SOFC manufacturers like Bloom Energy to face a growing backlog, potentially leading to increased prices and longer equipment lead times. The primary signal to watch is whether SOFC producers can scale their manufacturing capacity to meet the multi-gigawatt demand now materializing. A failure to do so would create an opening for competing technologies to capture market share. Conversely, continued success will solidify SOFC’s position as the dominant bridge technology for the next five years of data center development.

The questions your competitors are already asking

This report covers one angle of the commercial adoption of on-site power generation for AI data centers. The questions that matter most depend on your work.

- Which power technologies—SOFC, PEM, SMR, or Geothermal—are gaining or losing ground in the AI data center market?

- What is the outlook for SOFC deployment in AI data centers by 2030?

- How do SOFCs compare to alternatives like PEM fuel cells and SMRs on cost and deployment speed for data centers?

- Which hyperscale data center operators are adopting on-site power, and who have they signed contracts with?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.