Doosan Fuel Cell Maritime SOFC Pilots, $2.89 B Market, Shell Partnership, and 120 k W MODEC Trial (2021 to 2026)

Maritime Fuel Adoption Risks, Doosan and Multi-Fuel Hedging

The maritime industry’s decarbonization strategy is defined by fragmentation, with shipping lines hedging across LNG, Methanol, and Ammonia, which creates adoption risks and highlights the long-term value proposition of fuel-flexible Solid Oxide Fuel Cell technology.

- Between 2021 and 2024, LNG dominated new vessel orders as the primary “bridge fuel” due to mature technology and relatively developed bunkering infrastructure, while methanol and ammonia were largely confined to pilot projects and strategic discussions.

- A significant shift occurred from 2025 to 2026, where methanol emerged as the pragmatic leader for new orders, with major commitments from operators like Wallenius Wilhelmsen and Mitsui O.S.K. Lines (MOL), driven by its easier handling properties compared to cryogenic LNG and toxic ammonia.

- The rise of “ammonia-ready” vessel designs from shipping lines such as NYK Group and Grimaldi Group signals the industry’s consensus on ammonia as the long-term zero-carbon solution, even as engine technology is still being finalized.

- This fragmented fuel choice validates the strategic importance of fuel-agnostic power generation like SOFCs, which can operate on hydrogen, ammonia, methanol, or natural gas, mitigating the billion-dollar risk of investing in assets tied to a single fuel pathway.

$130 M S. Korea Investment, Doosan and Ammonia Tech Development

Public and private capital is flowing into production infrastructure for both near-term and long-term fuels, signaling a dual-track investment thesis where methanol is scaled for immediate use while foundational investments are made for the future ammonia economy.

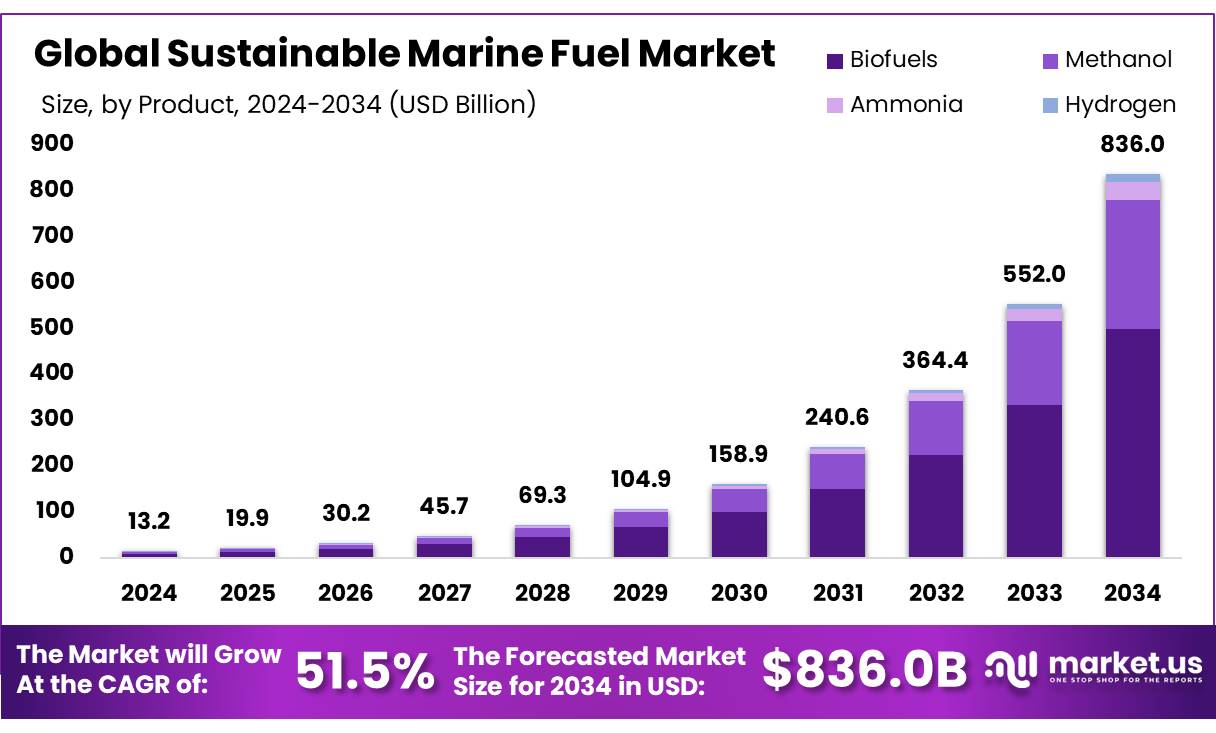

Sustainable Marine Fuel Market to Exceed $830B

This forecast quantifies the massive investments flowing into fuel infrastructure, projecting an $836 billion market by 2034 and supporting the dual-track thesis with methanol dominating early and ammonia gaining share later.

(Source: Market.us)

- Major investments are being directed at scaling green methanol supply to address a key adoption barrier, highlighted by Southern Energy Renewables’ $1.4 billion commitment to a new production facility in Louisiana.

- Targeted government support, such as South Korea’s $130 million investment to develop ammonia-fired gas turbines and fuel-supply systems, validates ammonia as the strategic long-term bet for achieving true zero-carbon shipping.

- Investment in LNG infrastructure continues, exemplified by Exmar’s conversion of an LNG carrier into a floating storage and regasification unit (FSRU), but the strategic focus is shifting toward bio-LNG to maintain its environmental and commercial relevance.

- The SOFC market is projected to reach $2.89 billion in 2026 and grow at a CAGR of 41.73%, with capital beginning to flow into pilot projects aimed at demonstrating the technology’s superior efficiency in marine applications.

Table: Maritime Fuel Strategic Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Southern Energy Renewables | March 2026 | Announced a $1.4 billion investment for a green methanol and sustainable aviation fuel (SAF) production facility, directly addressing the supply-side constraint for methanol-fueled vessels. | Southern Energy Renewables |

| South Korean Government | February 2026 | Committed $130 million to accelerate the development of ammonia-fired gas turbines and fuel-supply systems, aiming to establish a first-mover advantage in the ammonia ecosystem. | Argus Media |

| First Ammonia | March 2026 | Developing a green ammonia production facility at the Port of Victoria with a target capacity of 1.1 million tonnes per year by 2027, explicitly targeting the maritime fuel market. | Fuel Cells Works |

Doosan Fuel Cell 3 Major Maritime Partnerships (2021 to 2026)

Strategic partnerships are forming across the value chain, from fuel production to engine manufacturing and bunkering, to de-risk the complex transition and accelerate the technical and commercial validation of new fuels.

Visualizing Maritime Fuel Pathways to Zero Emissions

This chart illustrates the complex value chains that strategic partnerships are building, showing how key fuels can transition from fossil-based production to bio-fuels and ultimately to zero-emission e-fuels.

(Source: SEA-LNG)

- The collaboration between engine manufacturer Wärtsilä and vessel operator Simon Møkster Shipping to test ammonia as a main fuel in dual-fuel engines is a critical step in proving its operational viability and addressing safety concerns.

- Bunkering infrastructure is being proven out through practical alliances, such as Mitsui O.S.K. Lines’ (MOL) participation in Japan’s first ship-to-ship methanol bunkering operation, which builds confidence for wider adoption.

- The collaboration between Doosan Fuel Cell, energy major Shell, and shipbuilder Korea Shipbuilding & Offshore Engineering (KSOE) demonstrates a vertically integrated approach to commercializing marine SOFC systems for high-efficiency power.

- Fuel suppliers and shipowners are forming direct offtake agreements, such as the two-year biomethanol supply deal between Equinor and Wallenius Wilhelmsen, to secure fuel for upcoming dual-fuel vessels and de-risk investment in newbuilds.

Table: Maritime Fuel Ecosystem Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Doosan Fuel Cell, Shell, KSOE | March 2026 | A partnership to develop and manufacture marine SOFC systems, combining Doosan’s low-temperature SOFC technology with Shell’s energy expertise and KSOE’s shipbuilding leadership. | Riviera Maritime Media |

| Equinor & Wallenius Wilhelmsen | March 2026 | Equinor signed a two-year biomethanol supply agreement to fuel Wallenius Wilhelmsen’s new methanol-capable vessels, securing a green fuel pathway for the roll-on/roll-off carrier. | gasworld |

| Genevos (HELENUS Project) | February 2026 | As part of a Horizon Europe initiative, Genevos is leading the development of a modular SOFC power unit specifically designed for sustainable shipping in commercial and cruise sectors. | Genevos |

| Wärtsilä & Simon Møkster Shipping | February 2026 | An active collaboration to explore the feasibility of using ammonia as the main fuel in dual-fuel engines on offshore vessels, tackling technical and safety challenges. | Ammonia Energy Association |

Asia vs. Europe, Doosan and the Maritime Fuel Infrastructure Race

Asia and Europe are the primary hubs for developing and deploying new maritime fuel technologies and infrastructure, driven by strong government support and proactive industrial conglomerates creating distinct regional advantages.

- Asia is positioning itself as a leader in deploying next-generation fuel infrastructure, with South Korea’s $130 million government investment in ammonia technology and Japan’s execution of its first methanol bunkering operation.

- Europe is focusing on advanced technology research and development through initiatives like the EU’s Horizon Europe program, which is funding the HELENUS project to develop modular SOFC power units for commercial shipping.

- North America is emerging as a key production center for green fuels, highlighted by the $1.4 billion Southern Energy Renewables facility in Louisiana, aiming to supply the global maritime market with low-carbon methanol.

SOFC Pilot Stage, Doosan and LNG’s Commercial-Scale Dominance

In 2026, maritime fuel technologies exist on a wide spectrum of maturity, with LNG at full commercial scale, methanol rapidly scaling, ammonia in advanced pilots, and SOFCs entering initial marine trials.

- LNG (TRL 9): As the most mature alternative fuel, LNG is at full commercial scale with established bunkering infrastructure. The focus has shifted from technology validation to developing bio-LNG and e-LNG to address methane slip and extend its viability.

- Methanol (TRL 8): Methanol is quickly moving from pilot to commercial scale, with dual-fuel engines commercially available and major carriers placing orders. The primary remaining challenge is scaling the global production of green methanol to meet projected demand.

- Ammonia (TRL 6-7): Ammonia engine technology is in advanced pilot stages with engine manufacturers like Wärtsilä. The first commercial engines are just now being deployed, but widespread adoption is contingent on finalizing safety protocols and addressing toxicity concerns.

- SOFC (TRL 5-6): SOFCs for maritime applications are in the early pilot phase. Projects like the 120 k W trial on an FPSO unit by MODEC and Delta Electronics are critical for demonstrating the technology’s durability and high-efficiency potential in a demanding marine environment.

2027 Outlook, Doosan Fuel Cell and the Methanol-Ammonia Race

If green methanol production continues to scale with large-scale investments and offtake agreements, it will solidify its dominance as the primary transition fuel through 2030, but watch for key signals from ammonia and SOFC pilot projects that could alter long-term fleet strategies.

Future Fuel Mix Shows Rise of Alternatives

This forecast provides context for the methanol-ammonia race by showing the projected decline of traditional fuels, the rise of LNG as a transitional fuel, and the eventual dominance of carbon-neutral fuels that are competing for long-term market share.

(Source: Ammonia Energy Association)

- If this happens: Watch the first large-scale ammonia-fueled vessels from operators like NYK Group. Any operational issues or safety incidents could slow industry momentum and extend methanol’s lead, while successful voyages will accelerate investment in ammonia infrastructure.

- Watch this: Monitor the results of early maritime SOFC pilots, such as the HELENUS project. Successful demonstrations of high efficiency and fuel flexibility will likely trigger the first commercial orders for SOFCs as auxiliary power units, representing the next phase of the transition.

- These could be happening: Port authorities and bunkering operators will accelerate partnerships to create multi-fuel hubs capable of supplying both methanol and ammonia, moving away from risky, single-fuel infrastructure investments and acknowledging the fragmented market reality.

The questions your competitors are already asking

This report covers one angle of the maritime fuel transition, focusing on shipping line commitments and the strategic role of fuel-flexible technology. The questions that matter most depend on your work.

- Doosan Fuel Cell’s activities in maritime SOFCs. Is the partnership with Shell progressing from pilot to commercial deployment?

- What is the outlook for maritime SOFC deployment by 2026, given the industry’s fragmentation across LNG, methanol, and ammonia?

- How does fuel-flexible SOFC technology compare to dedicated methanol or ammonia engines for mitigating long-term investment risk?

- Which shipping lines like MOL are committing to methanol newbuilds, and which like NYK Group are designing ‘ammonia-ready’ vessels?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.