Hitachi Energy Grid Infrastructure 2026, $4.5B for Amazon

Power Transformer Shortages, 4-Year Lead Times from Hitachi Energy, a 116% Demand Surge, and 30% US Supply Deficit (2025 to 2026)

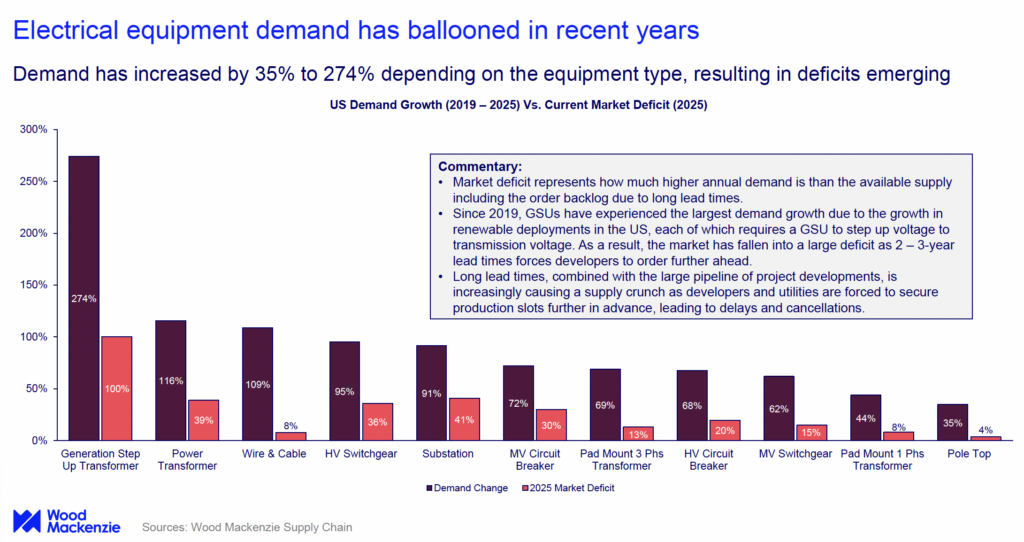

Grid Expansion Risks from 4-Year Transformer Lead Times and 116% Demand Surge

The global power transformer supply chain has buckled under a demand supercycle, creating a critical bottleneck that is actively stalling grid expansion and the energy transition. A convergence of demand from AI data centers, renewable energy projects, and grid modernization efforts has stretched manufacturing capacity to its absolute limit. This has inflated prices and extended lead times for large power transformers (LPTs) to between two and five years, a dramatic increase from historical norms and a primary risk for any large-scale energy or infrastructure project planned through 2028.

- Prior to 2024, typical lead times for LPTs were manageable. However, the period from 2025 to 2026 has seen a structural shift, with wait times extending to four years, directly jeopardizing project schedules and financial models for developers.

- The demand surge is not a stylized forecast; it is a material constraint. Analysis from 2025 projected the U.S. would face a power transformer supply shortfall of 30% to 40%, a deficit that directly impedes the connection of new power sources and loads to the grid.

- This supply-demand imbalance has caused prices to escalate dramatically. By 2025, transformer costs had already increased by 70% to 100%, forcing developers to re-evaluate project economics and secure financing for significantly higher capital expenditures.

- The voracious energy needs of tech companies like Amazon, Google, and Microsoft for their AI infrastructure are a primary driver. U.S. power demand from data centers alone is projected to grow from 4 GW to 123 GW by 2035, requiring a massive and rapid build-out of new grid infrastructure.

Transformer Demand Surge Creates 100% Market Deficit

The section heading’s mention of a ‘116% Demand Surge’ directly corresponds to the chart’s headline ‘Transformer Demand Surge Creates 100% Market Deficit,’ illustrating the core risk to grid expansion.

(Source: POWER Magazine)

Manufacturing Investment, Hitachi Energy $4.5 B Capacity Expansion

In response to the unprecedented demand and crippling backlogs, major transformer manufacturers and governments have initiated significant capital investments and policy actions to expand production capacity. However, the long construction timelines for new factories mean these efforts will not provide meaningful relief to the market until after 2027, ensuring the bottleneck remains a medium-term constraint for developers.

- Hitachi Energy, a key market shaper, has committed $4.5 billion globally to expand its manufacturing capabilities for transformers and other grid infrastructure. This includes a $1.5 billion initiative specifically targeting capacity growth, with $500 million dedicated to North American facilities through 2027.

- The U.S. government has also begun to intervene. In July 2025, the “One Big Beautiful Bill Act (OBBBA)” was passed, creating uncertainty by modifying or repealing clean energy tax credits, a key demand driver. This policy headwind could temper the growth of renewable projects.

- To counter domestic production shortfalls, the U.S. administration invoked the Defense Production Act in 2025 to address grid equipment shortages, aiming to stimulate domestic manufacturing of transformers and their core components.

- Further legislative support emerged with the proposed “One Big Beautiful Bill Act, ” which, despite its disruptive elements, signaled a federal focus on addressing supply chain vulnerabilities through policy, although its net effect on clean energy demand remains a significant risk.

Transformer Investment Surges Amidst Shortages

The section’s focus on ‘Manufacturing Investment’ and capacity expansion is perfectly visualized by the chart ‘Transformer Investment Surges Amidst Shortages,’ which shows a direct industry response to the supply problem.

(Source: POWER Magazine)

Strategic Procurement Shifts as Tech Firms Bypass Traditional Channels

The extreme lead times and supply uncertainty have forced large power consumers to abandon traditional procurement methods in favor of proactive, long-term strategic partnerships with manufacturers. This shift, led by major technology companies and large utilities, is fundamentally reshaping the market by prioritizing access for well-capitalized players and creating new risks for smaller developers.

- Starting around 2025, major technology companies and utilities began entering into direct, multi-year supply agreements with manufacturers. This strategy involves securing production slots three to four years in advance of project construction, effectively de-risking their development pipelines.

- This procurement model mirrors the strategies seen in other constrained markets, where securing supply chain capacity becomes as critical as project financing. The actions of large buyers like Dominion Energy and data center operators are creating a new competitive dynamic.

- The risk for the broader market is that this trend will crowd out smaller utilities, renewable developers, and industrial players who lack the scale and capital to pre-order equipment years in advance, potentially fragmenting the market and slowing deployment for those outside these strategic alliances.

- This has created an adjacent opportunity for consortium buying and advisory services that can help smaller entities aggregate their demand to gain purchasing power and compete for limited production capacity.

US Data Center Equipment Sourcing Shifts from China

The section discusses ‘Strategic Procurement Shifts as Tech Firms’ change their sourcing. The chart ‘US Data Center Equipment Sourcing Shifts from China’ provides a concrete example of this trend, as data centers are a key area for tech firm investment.

(Source: Coalition For A Prosperous America)

Table: Strategic Procurement and Policy Actions (2025-2026)

| Entity/Action | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Major Tech and Utility Buyers | 2025-2026 | Began entering direct, multi-year procurement agreements with manufacturers to secure production slots 3-4 years in advance, de-risking massive data center and utility project pipelines. | fjinno |

| “One Big Beautiful Bill Act (OBBBA)” | July 4, 2025 | Passage of legislation that repeals or modifies key clean energy tax credits, creating significant policy uncertainty for renewable energy projects, a primary source of transformer demand. | Columbia University |

| Hitachi Energy | Feb 2026 | Announced a $4.5 billion global investment to expand production capacity for transformers and other critical grid infrastructure in response to the massive order backlog. | Macro-Notes |

Power Transformer Market to Reach $28.2B in 2026

The section, a table detailing actions for ‘2025-2026,’ is contextualized by this chart, which provides a market size forecast specifically for the year ‘2026,’ aligning the policy timeframe with market projections.

(Source: Persistence Market Research)

US Market Exposure from 80% Import Reliance on Power Transformers

The United States is uniquely exposed to the global power transformer shortage, a vulnerability created by decades of offshoring manufacturing capacity. With domestic production meeting only a small fraction of its needs, the nation’s grid expansion and energy security are heavily dependent on a fragile global supply chain and volatile trade policies.

- The U.S. relies on imports for approximately 80% of its large power transformers and 50% of its distribution transformers. This heavy import dependency makes the nation’s infrastructure goals susceptible to foreign supply disruptions, shipping delays, and geopolitical tensions.

- Domestic manufacturing capacity is critically low. A 2024 Department of Energy report found that the U.S. can produce a maximum of only 343 LPTs per year, a volume that meets just 20% of its total demand.

- This contrasts sharply with the global supply landscape, where major manufacturing hubs are overwhelmed. By March 2026, reports indicated that major Chinese transformer manufacturers were already fully booked with orders through 2027, leaving few options for buyers needing near-term supply.

- The problem is compounded by non-equipment bottlenecks. In Europe, permitting for new transmission lines, which are necessary to connect transformers, can take an average of 12 to 17 years, creating a multi-layered obstacle to grid modernization.

US Transformer Imports Shift From China to Mexico

The section on ‘US Market Exposure from… Import Reliance’ is supported by this chart, which illustrates the dynamic nature of this reliance by showing a ‘US Transformer Imports Shift From China to Mexico,’ a key strategic response to geopolitical and supply chain risks.

(Source: Coalition For A Prosperous America)

Technology Status: Mature TRL 9 Transformers Face Manufacturing Hurdles

The power transformer shortage is a crisis of industrial capacity, not technological innovation. The core technology for conventional transformers is at Technology Readiness Level 9 (TRL 9), meaning it is fully mature and proven. The challenge lies entirely in scaling a manufacturing base that has been neglected for decades, a problem that emerging technologies are not positioned to solve in the near term.

- The mature status of transformer technology is a double-edged sword. While there is no R&D risk, it also means there are no immediate technological breakthroughs that can alleviate the supply crunch. The solution is building more factories, which requires immense capital and time.

- Alternative technologies like Solid State Transformers (SSTs) are often cited as a potential long-term solution. However, as of 2025, SSTs remain at a lower TRL for high-voltage applications and face significant challenges related to cost, reliability, and scalability. They are not a viable replacement for LPTs in the current decade.

- The focus of innovation has shifted from core technology to ancillary features. Trends for 2026 include the development of eco-friendly transformers using biodegradable ester fluids and incorporating CO 2-neutral materials to meet corporate sustainability goals.

GSU and Power Transformers Face Severe Shortfalls

The section explains that mature transformer technology faces ‘Manufacturing Hurdles.’ This chart, ‘GSU and Power Transformers Face Severe Shortfalls,’ quantifies the direct outcome of these manufacturing bottlenecks.

(Source: Citrini Research)

Forward Outlook: Transformer Shortage to Persist Beyond 2028

The power transformer bottleneck will remain the defining constraint for the energy and technology sectors for at least the next three to five years, with a return to a balanced market unlikely before 2029. Strategic focus must shift from expecting near-term relief to actively managing this long-term constraint and investing in technologies that optimize existing grid capacity.

- The most critical catalyst to monitor is the progress of new manufacturing capacity expansions, particularly the timelines for Hitachi Energy’s new facilities coming online. Any delays will prolong the shortage.

- Policy remains a wild card. The implementation of the post-OBBBA legislative landscape and any resolution on potential Section 232 tariffs on imported transformers will directly impact equipment costs and availability in the U.S. market.

- The shortage creates a significant adjacent opportunity for Grid-Enhancing Technologies (GETs). Solutions like dynamic line rating and advanced power flow control, which can unlock over 80 GW of capacity on the existing U.S. grid, will see accelerated adoption as a cost-effective way to mitigate the transformer bottleneck.

Power Transformer Market to Reach $46.4B by 2033

This section provides a ‘Forward Outlook’ that the shortage will ‘Persist Beyond 2028.’ The chart’s long-term projection of the market reaching a new high ‘by 2033’ provides the data to support this long-range forecast.

(Source: Persistence Market Research)

The questions your competitors are already asking

This report covers one angle of the power transformer supply chain risk stalling grid expansion. The questions that matter most depend on your work.

- Which power transformer manufacturers are gaining or losing ground in the race to expand production capacity?

- What is the outlook for connecting new AI data center and renewable projects to the grid by 2028, given the 4-year LPT lead times?

- Hitachi Energy activities in LPT manufacturing. Is its capacity expansion progressing to meet the 116% demand surge?

- Which data center operators and renewable developers are most exposed to the 30% US transformer supply deficit?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.