Thyssen Krupp Hydrogen 2026, 2.5 Mtpa Stegra Plants

Top 10 Green Hydrogen Steel Plants, Thyssen Krupp €1.8 B Project & >700 MW Electrolyzer Deals (2024-2026)

The global steel industry is on the verge of a significant transformation, with the first wave of commercial-scale green steel plants using hydrogen-based Direct Reduced Iron (H₂-DRI) technology expected to be operational by 2026. This marks a critical move away from coal-based blast furnaces. However, this transition is defined by a steep cost premium, which presents a major challenge to widespread market adoption. Groundbreaking projects from companies like Thyssen Krupp and Stegra are targeting 2026 operations, but the green premium is estimated at a substantial 30% to 40% over conventional steel, driven by green hydrogen costs of $4 to $6 per kg. The dominant theme for 2025 is this fundamental tension between ambitious project timelines and the economic reality of the green premium. While European producers are seeing premiums of €120 to €180 per tonne, a 2024 survey found only 20% of steel consumers were willing to pay more than $75 per tonne, highlighting a stark gap between production costs and market appetite.

1. Thyssen Krupp Steel (tk H 2 Steel)

Company: Thyssen Krupp Steel

Capacity: 2.5 Mtpa

Application: The project involves a Midrex technology-based DRI plant with two smelters, designed for initial operation on natural gas before transitioning to green hydrogen. Total investment is estimated at €1.8 billion.

Source: Is German steel giant stumbling over green steel?

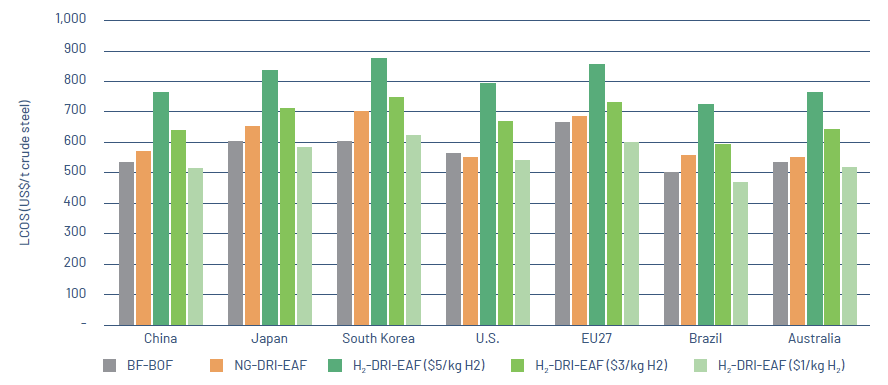

Green Steel Cost Competitiveness Depends on Hydrogen Price

Section 0 describes the Thyssen Krupp H2 Steel project. The project’s financial viability is directly tied to the cost of green hydrogen, making this chart, which highlights the dependency of cost competitiveness on hydrogen price, a perfect fit.

(Source: Global Efficiency Intelligence)

2. Stegra (formerly H 2 Green Steel)

Company: Stegra

Capacity: 2.5 Mtpa (initial phase)

Application: Set to be the world’s first commercial-scale green steel mill operating on 100% hydrogen DRI from startup. The facility will be powered by an electrolyzer with a capacity over 700 MW.

Source: DRI UPDATE – Sponge Iron Manufacturers Association (SIMA)

Green Steel Competitiveness Hinges on Hydrogen Price

Section 1 focuses on the Stegra (H2 Green Steel) project. As with other hydrogen-based steelmaking efforts, Stegra’s ability to compete with traditional steel hinges on the price of hydrogen, a core concept illustrated by this chart.

(Source: Global Efficiency Intelligence)

3. Dillinger and ROGESA

Company: Dillinger and ROGESA

Capacity: 2.0 Mtpa

Application: This joint venture will use MIDREX® Flex technology, which allows for operation with natural gas, hydrogen, or a blend of both, enabling a phased transition to green production.

Source: The Transition to Carbon Neutral Iron – World Steel Association

4. HYBRIT (SSAB, LKAB, Vattenfall)

Company: HYBRIT (SSAB, LKAB, Vattenfall)

Capacity: 1.3 Mtpa (sponge iron)

Application: A pioneering industrial-scale demonstration plant aiming to produce fossil-free sponge iron using 100% green hydrogen by its 2026 operational target.

Source: Scaling Up Hydrogen: The Case for Low- Carbon Steel

Green Steel Costs Hinge on Hydrogen Price

Section 3 details the pioneering HYBRIT project. The chart’s message, that green steel costs are dependent on hydrogen prices, is the central economic challenge and variable for this specific hydrogen-based steelmaking venture.

(Source: Transition Asia)

5. Baosteel

Company: Baosteel

Capacity: Not specified (described as “world’s largest”)

Application: A large-scale H₂-DRI plant in China, which sources indicate began operating at full capacity in late 2025.

Source: Europe’s quest for green steel | Canary Media

6. JSW Green Steel

Company: JSW Green Steel

Capacity: 0.9 Mtpa

Application: An existing DRI unit in Salav, India, was transferred to the new entity in March 2025 to convert existing assets for low-carbon production.

Source: JSW Green Steel Salav plant – Global Energy Monitor

Green Steel Market Projected to Exceed $74B

Section 5 describes the JSW Green Steel project in India. A chart projecting a significant future market size provides the commercial rationale and context for JSW’s investment in entering the green steel sector.

(Source: Market.us)

7. Shanxi Taihang Mining

Company: Shanxi Taihang Mining

Capacity: 0.3 Mtpa

Application: A DRI plant in China scheduled for completion in 2026 that will utilize a mix of coke oven gas and hydrogen as a reductant.

Source: WORLD DIRECT REDUCTION STATISTICS

8. Blastr Green Steel

Company: Blastr Green Steel

Capacity: Not specified

Application: An integrated green steel plant planned for Finland, incorporating DRI and Electric Arc Furnace (EAF) technology to leverage the region’s renewable energy resources.

Source: Blastr Inkoo steel plant – Global Energy Monitor

Green Steel Projected to Displace High-CO2 Steel by 2050

Section 7 covers Blastr Green Steel, a new venture. A chart projecting the long-term displacement of conventional steel illustrates the disruptive potential and total addressable market that underpins the strategy of a ‘greenfield’ player like Blastr.

(Source: calstart)

9. Arcelor Mittal (XCarb®)

Company: Arcelor Mittal

Capacity: >2 Mtpa combined

Application: As part of its XCarb® initiative, Arcelor Mittal is making substantial investments in hydrogen-based DRI, though full commercial plants are targeted for after 2026.

Source: How Does Arcelor Mittal Company Work?

Green Steel Prices Projected to Decline Sharply

Section 8 features Arcelor Mittal’s XCarb® initiative. For a major incumbent launching a branded green product, a chart showing a sharp future price decline is crucial to illustrating the path to mass adoption and the long-term commercial strategy.

(Source: CleanTechnica)

10. Indian National Green Hydrogen Mission Pilot Projects

Company: Indian National Green Hydrogen Mission

Capacity: Pilot/Demonstration scale

Application: Three government-sanctioned pilot projects, sanctioned in 2024, to demonstrate the use of green hydrogen in steel production and build domestic capacity.

Source: Launch of Pilot projects in Steel Sector under the National Green …

Hydrogen Steelmaking to Capture 26% of Market by 2050

Section 9 discusses India’s National Green Hydrogen Mission. A chart that quantifies the future market share of hydrogen-based steelmaking provides the strategic justification for a national-level investment in pilot projects.

(Source: Wood Mackenzie)

Table: Top 10 Green Steel DRI Projects by 2026

| Project / Company | Planned Capacity (Mtpa) | Application / Technology | Source |

|---|---|---|---|

| Thyssen Krupp Steel (tk H 2 Steel) | 2.5 | Midrex DRI technology, initial operation on natural gas. | Is German steel giant stumbling over green steel? |

| Stegra (formerly H 2 Green Steel) | 2.5 | 100% hydrogen-based DRI from startup, with >700 MW electrolyzer. | DRI UPDATE – Sponge Iron Manufacturers Association (SIMA) |

| Dillinger and ROGESA | 2.0 | MIDREX® Flex technology, using a mix of natural gas and hydrogen. | The Transition to Carbon Neutral Iron – World Steel Association |

| HYBRIT (SSAB, LKAB, Vattenfall) | 1.3 | Industrial-scale demo plant for 100% fossil-free sponge iron. | Scaling Up Hydrogen: The Case for Low- Carbon Steel |

| Baosteel | Not specified | Described as the ‘world’s largest’ hydrogen-fueled ironmaking plant. | Europe’s quest for green steel | Canary Media |

| JSW Green Steel | 0.9 | Existing DRI unit converted for low-carbon production. | JSW Green Steel Salav plant – Global Energy Monitor |

| Shanxi Taihang Mining | 0.3 | DRI plant using a mix of coke oven gas and hydrogen. | WORLD DIRECT REDUCTION STATISTICS |

| Blastr Green Steel | Not specified | Planned integrated green steel plant with DRI and EAF. | Blastr Inkoo steel plant – Global Energy Monitor |

| Arcelor Mittal (XCarb®) | >2.0 | Long-term investments in hydrogen-based DRI. | How Does Arcelor Mittal Company Work? |

| Indian National Green Hydrogen Mission | Pilot-scale | Government-sanctioned pilot projects for H 2-DRI. | Launch of Pilot projects in Steel Sector under the National Green … |

Green Steel Adoption, Stegra’s 2.5 Mtpa Mill Signals a Commercial Shift

The range of projects targeting 2026 operations demonstrates two distinct pathways for industry adoption. On one hand, ambitious greenfield projects like Stegra in Sweden and Blastr in Finland represent an all-in strategy, building entirely new ecosystems around 100% hydrogen from day one. This approach is concentrated in regions with abundant and low-cost renewable energy. On the other hand, a more common strategy involves retrofitting or augmenting existing facilities. Projects by Thyssen Krupp in Germany and JSW Green Steel in India exemplify this transitional approach, converting brownfield sites and utilizing flexible fuel technologies to manage capital expenditure and de-risk the shift away from fossil fuels. This dual-track adoption implies that while the industry’s future is green, the path to get there will be highly regionalized and tailored to existing industrial infrastructure.

Analysis of Green Steel Market Forces

This section’s title, ‘Green Steel Adoption…Signals a Commercial Shift,’ is best explained by a chart that analyzes the underlying market forces (e.g., supply, demand, competition, policy) driving that shift.

(Source: Coherent Market Insights)

European Leadership, Thyssen Krupp and HYBRIT Drive Green Steel Projects

Geographically, Europe is the clear epicenter of the green steel movement, with Germany and Sweden at the forefront. Projects like Thyssen Krupp‘s 2.5 Mtpa plant, HYBRIT‘s pioneering demonstration, and Stegra‘s massive greenfield build are driven by strong regulatory tailwinds, including the EU’s carbon pricing policies. These initiatives position the continent as a leader in decarbonizing heavy industry. However, Asia is developing its own powerful green steel sector. China’s Baosteel has already commissioned what has been described as the “world’s largest” hydrogen-based plant, signaling a national push to dominate this emerging market. Concurrently, India’s strategy, combining commercial retrofits like JSW Green Steel with government-backed pilot programs under its National Green Hydrogen Mission, indicates a focus on building domestic capacity and technological self-reliance. This creates a competitive dynamic where Europe’s policy-driven leadership is being challenged by Asia’s scale and speed.

Chart Details European Green Steel Project Pipeline

The section heading, ‘European Leadership…Drive Green Steel Projects,’ is a perfect match for the chart’s headline, which explicitly details the ‘European Green Steel Project Pipeline,’ visually representing the section’s core topic.

(Source: EUROMETAL)

€1.8 Billion, Thyssen Krupp Investment Shows H₂-DRI-EAF Tech is Commercial

The scale of investment, highlighted by Thyssen Krupp‘s €1.8 billion commitment, confirms that H₂-DRI-EAF technology has graduated from the pilot stage to commercial readiness. The existence of multiple multi-million-tonne-per-annum projects like those from Stegra (2.5 Mtpa) and Dillinger (2.0 Mtpa) proves the core technology is considered viable for industrial-scale production. The adoption of flexible systems like MIDREX® Flex, which can operate on natural gas, hydrogen, or a blend, reflects a mature, pragmatic approach to navigating the energy transition. This allows steelmakers to begin decarbonization immediately without waiting for green hydrogen to become widely available and affordable. The primary bottleneck is no longer the steelmaking technology itself, but the upstream supply chain. The current green premium of 30-40% is a direct function of the high cost and limited availability of green hydrogen, making its production at scale the most critical factor for the technology’s long-term economic viability.

Green Steel Nears Cost Parity with Other Methods

The section claims a major investment proves the technology is ‘commercial.’ The chart provides direct support for this by showing green steel ‘nears cost parity,’ which is the definition of becoming commercially viable.

(Source: RMI)

Stegra’s Green Steel Economics, €120-€180/tonne Premium Challenges Adoption (2025-2026)

The most critical factor to monitor through 2026 is whether early off-take agreements and market demand can absorb the high green premium. If end-users resist paying premiums in the range of €120-€180 per tonne, it could force producers to either delay expansion plans or absorb significant financial losses, undermining the business case for these capital-intensive projects.

- Signal to Watch: The progress of large-scale electrolyzers, such as the >700 MW unit planned for the Stegra plant, is the primary leading indicator for future cost reductions. Any delays in their construction or commissioning will directly translate to a persistently high green premium.

- Gaining Traction: Government financial support and carbon pricing mechanisms are proving essential to bridge the production cost gap. The significant public funding secured for projects like Thyssen Krupp‘s plant in Duisburg shows that policy is a key enabler for first-movers.

- Losing Steam: Downstream customer willingness-to-pay remains a powerful headwind. Data from late 2024 showing that some low-carbon steel premiums were capped by market resistance at just $20 per tonne is a strong negative signal that the cost cannot be easily passed on.

- Possible Scenario: If green hydrogen costs remain elevated near $4-$6/kg, the industry may see a strategic pivot. Investment could shift away from ambitious 100% hydrogen greenfield projects toward more brownfield conversions and hybrid natural gas/hydrogen models, slowing the pace of full decarbonization but offering a more financially viable near-term path.

Green Steel Commands Price Premium in Europe

The section heading specifically quantifies a ‘€120-€180/tonne Premium’ for green steel. The chart’s headline, stating that green steel ‘Commands Price Premium in Europe,’ is a direct and perfect illustration of this point.

(Source: EUROMETAL)

The questions your competitors are already asking

This report covers one angle of the first commercial-scale hydrogen steel projects and the economics of the green premium. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the race to operate the first commercial-scale H₂-DRI plants by 2026?

- Thyssen Krupp investments and funding. Is the €1.8 billion tk H2Steel project on track for its 2026 operational target?

- What is the cost breakdown of the green premium, from green hydrogen at $4-$6/kg to the final steel product?

- Which steel consumers are adopting green steel despite the 30-40% premium?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

Green Steel Market to Exceed $800B by 2035

This strategic section about ‘questions your competitors are already asking’ implies a need for forward-looking data. A chart projecting a massive future market size directly answers the key competitor question: ‘What is the scale of the opportunity?’

(Source: Dimension Market Research)